I’m opening a thread for Raute; I’ve bought a tiny position in it. The results came out today and look quite poor in terms of orders, although apparently historically reasonable.

We can discuss Raute’s performance here.

apparently the king of its field. The stock has fallen from its peaks, but there could still be further downside.

Alright, Raute announces that it has received a design contract for a birch plywood factory in Russia.

Raute assumes that an order for the equipment could be placed within a couple of months.

@Antti_Viljakainen, you probably know off the top of your head if this is potentially a larger order.

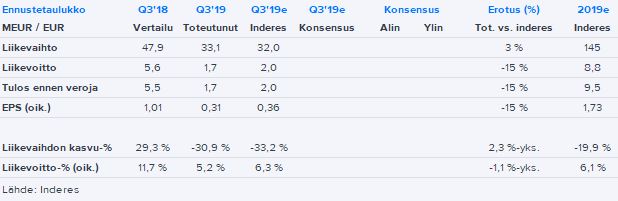

Rautia’s profitability declined sharply in Q3, as expected, but its profitability was still slightly weaker than our forecasts (part of the reason for the forecast miss is likely higher-than-normalized R&D investments). However, it was positive that the company commented that it expects the best period of the year in the fourth quarter, so there may be slight upward pressure on Q4 forecasts. The large Russian deal was already booked in Q3, but otherwise, the underlying orders were soft. Service sales, in particular, suffered badly, but this was practically due to low demand for modernizations, similar to investments. Uncertainty in the markets is growing, which is not surprising at all. The order book, which has risen to EUR 109 million, provides moderate support for the next year, but next year is far from fully sold out. Orders must increasingly be gathered also from outside the strongest competitive advantage, which increases risks.

Raute’s CEO, Tapani Kiiski, will be on ROAST on Wednesday. I’m collecting audience questions in advance (you can also ask them during the LIVE broadcast).

It seems to be the most cyclical, or at least one of the most cyclical, companies on the stock exchange.

Rautel’s extensive report came out on Wednesday. No major changes in the big picture. The competitive advantage is strong and sustainable, but in the more challenging market of the coming years, earnings growth looks tight. Multi-term multipliers have also stretched beyond their medium-term levels.

From a shorter perspective, Q4 did not see any deals that exceeded the disclosure threshold (Rautel’s limit is probably somewhere around EUR 10 million). Therefore, in terms of order flow, the Q4 report is unlikely to be a fireworks display. Revenue and profit for the end of the year were good. I will return to the matter in more detail in a pre-comment in February.

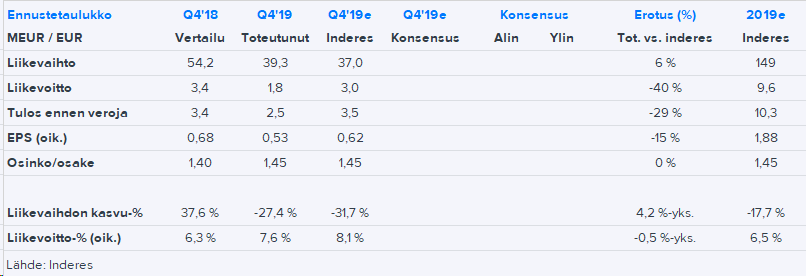

Raute’s Q4 results significantly missed our forecasts for Q4. Project challenges likely continued, and the slate had to be thoroughly cleaned to ensure a somewhat fresh start for the current year. The order flow of EUR 17 million is also sluggish. The dividend proposal was EUR 1.45, in line with our expectations.

Raute guided for stable revenue and a weakening profit for the current year. Profitability will be penalized by R&D, sales, and marketing investments in developing markets, which was not surprising in itself, but the impact on earnings is greater than we anticipated. There are also clear downward pressures on the current year’s forecasts.

Consolidated net sales 48.2 M€ (78.3 M€) decreased by 38.5% from the comparison period. New orders totaled 38 M€ (58 M€).

Operating profit -4.0 M€ (4.9 M€) decreased by 182% from the comparison period. Profit before taxes was -3.6 M€ (5.1 M€).

Earnings per share were -0.73 euros (0.94 e) and -0.73 euros (0.94 e) diluted.

In the second quarter, net sales were 24.4 M€ and operating profit was -1.0 M€. New orders in the second quarter totaled 13 M€. Order book at the end of the review period was 80 M€ (72 M€).

Raute’s net sales for 2020 are estimated to decrease from 2019, and operating profit is estimated to weaken significantly from 2019.

In ROAST, I asked if the balance sheet could be leveraged more, and I remember Tapani saying, “technically, yes, but I was already working at the company in 2008.” Now, it can be stated that this caution has been justified.

At this revenue level of roughly EUR 25 million/Q, the company is naturally in trouble, as its cost structure is higher after good years and reflecting healthy long-term prospects. A significant miss on the forecast also came through revenue. The silver lining in the numbers is that orders fell less short of forecasts than revenue, meaning there is more order backlog for H2 than we expected. However, more deals should still be made by the end of the year, so revenue would rise to a somewhat tolerable level.

We are interviewing Tapani on video today. If anyone has any specific questions for the company, I can add them to the list!

Noticed the same, one reason why I’m not considering Raute as an investment, even though it’s starting to be at interesting prices. Also, posing with a downed moose and sharing the picture on Twitter didn’t inspire confidence; it’s no longer modern.

There was a mention of a launched “significant system investment” in the report

We also launched a significant system investment during Q2, which will improve both our own operations and our technical capabilities to serve our customers.

One could ask if the CEO wants to elaborate on what this is all about?

I’d be interested to hear about the situation in China, whether there’s any development expected in the next 6 months. In my opinion, it’s a crucial market for Raute, especially given such a niche market segment. If they can’t access China, I see a weak future.

The acquisition of Hiotu was mentioned separately in the interim report. It could of course be related to that, but the wording would suggest more of an ERP system update or something similar.

Highly political have also been awarded business leaders such as Björn Wahlroos and Pekka Lundmark. If the CEO is networked with the country’s leadership, I consider it a fundamentally positive thing from an investor’s perspective.

Raute has been able to slide quite peacefully, and not even the news of the past few days seems to shake the stock. Let’s bring here, among others, Juha Varis’s tweet from yesterday: https://twitter.com/JuhaVaris/status/1301523564089217027

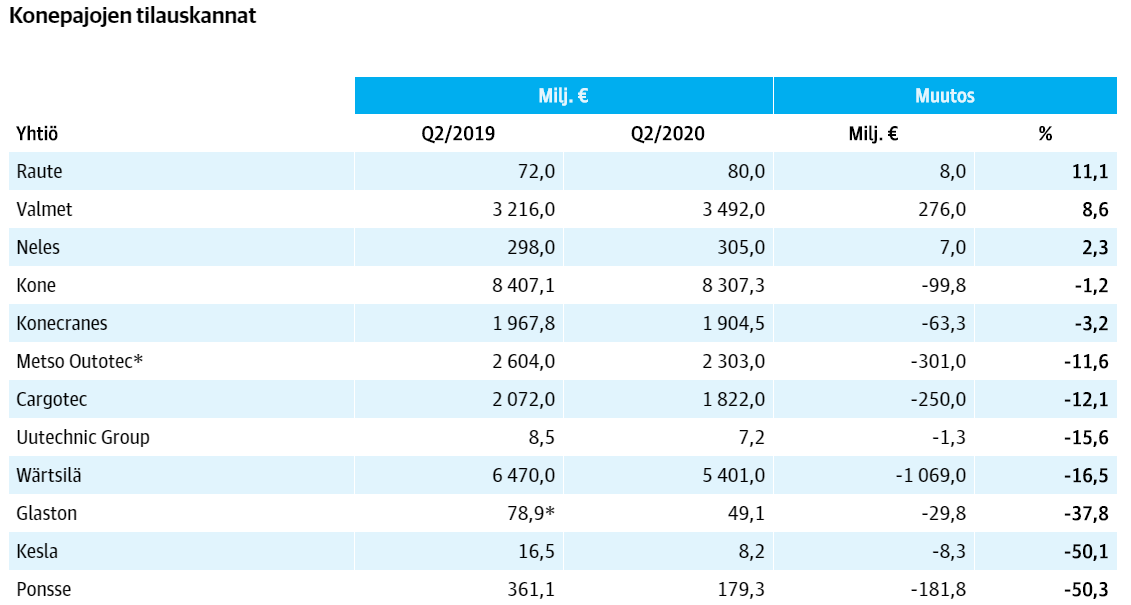

Today, Arvopaperi had an article about the order books of engineering workshops, and Raute was number one in terms of development:

The numbers for the beginning of the year are quite grim, but perhaps the trend would be upwards? I took a small (approx. 4%) position in my portfolio. Raute was a long time around 7.5€ paper, so the direction might still be downwards. Raute’s 7.5€ => 30€ was quite rapid. However, the company is debt-free, and usually, during these economic shocks, some kind of cost-cutting is done, and with a growing order book, there is again an opportunity to make a decent profit… while waiting for it.

However, let’s also add a table here about the order accumulations of engineering workshops, so that the picture doesn’t become too rosy… it’s always better to start from the bottom