Tervehdys kaikille!

Stellantis mainittiin viimeisimmässä Vernerin vartissa ja sille ei ollut vielä minkäänlaista ketjua olemassa. Yhtiö on Italian pörssiin listatuista yhtiöistä kaikista suurin markkina-arvoltaan. Stellantis ei nimenä välttämättä kovin monelle sano yhtään mitään, mutta tämän autovalmistajan merkit ovat varmasti jokaiselle tutut:

Stellantis on melko tuore kokonaisuus ja sen osakkeilla on käyty kauppaa tammikuusta 2021 lähtien. Yhtiö muodostettiin kahden autojätin fuusiolla: Fiat-Chrysler sekä PSA lyöttäytyivät yhteen. Tästä fuusiosta ei sen enempää, vaan kiinnostuneet voivat lukea tärkeimmät vaikka Wikipedian artikkelista: Stellantis - Wikipedia .

Olen ollut itse Stellantiksen omistaja kesästä 2022 alkaen ja aloitin tämän kokonaisuuden seurannan heti yhtiöiden fuusioiduttua. Välittömästi en omistajaksi ryhtynyt, koska halusin nähdä, miten pöly laskeutuu fuusion jälkeen: miten jättien taloudet konsolidoituvat ja mikä on yhtiön tavoite ja strategia. Kun asiat selvisivät ja talouslukujen valossa hinta oli erinomaisen halpa, iskin kiinni. On selvää, että yhtiön merkit eivät kaikkien silmissä ole missään nimessä sieltä hohdokkaimmasta päästä. Itselläni on kokemusta sekä Fiatin että PSA:n tuotteista lapsuudenkotini kautta, mutta mikään varsinainen merkkien fani en ole.

Ensimmäinen osatekijä, joka kiinnitti huomiotani, on yhtiön strategia. Ennen vuotta 2015 sekä Fiat-Chryslerin että PSA:n tuotteet eivät herättäneet, muutamia poikkeuksia lukuun ottamatta, mitään ihmeellisempiä tunteita. Kuitenkin automedioita seuratessani kummankin yhtiökokonaisuuden osalta huomioni kiinnittyi yhteen seikkaan: tuotteiden laatu oli parantunut ja tämä ilmeni kohonneena luotettavuutena. Tämä oli mielestäni erinomainen merkki.

Ennen fuusiota merkkeihin yhdistetty vakavin puute oli jo menossa parempaan suuntaan. Kun varsinainen Stellantiksen strategia esiteltiin eri merkkien osalta, mielestäni se oli nykyiseen epävarmaan automarkkinaan varsin osuva. Ensinnäkin kaikki Stellantiksen automerkit ovat karsineet mallistoaan ja huonoiten tuottavat mallit on tiputettu pois. Erityisen hyvin tämä näkyy Fiatin tuoteportfoliosta, josta ei ole kauheasti jäljellä. Portfoliota rakennetaan nyt jokaisen merkin kohdalla uudelleen. Toiseksi Stellantis ajaa mielestäni onnistuneesti kaksilla rattailla sähköistymisen suhteen. Stellantiksella on toki selkeä strategia malliston sähköistämiseen. Kuitenkin ennen kuin sähköistyminen lyö suuremmin läpi, myös muille voimalinjavaihtoehdoille on kysyntää. Stellantis on usean mallin kohdalla mennyt yliajalle ja tiristänyt viimeisetkin ostohalut kaikenlaisilla erikoismalleilla. Rapakon takana myyty Dodge Challenger on tästä erinomainen esimerkki. Samaan aikaan on kehitetty konsernin yhteistä alusta-arkkitehtuuria, jonka pohjalle tehtyjä malleja alkaa pian tulla markkinoille. Mielenkiintoista on myös se, että Stellantis on ensin tuonut jonkun mallin täyssähköisenä markkinoille, mutta koska kysyntää on polttomoottorille, niin mallista on sellainenkin versio sitten kehitetty. Esimerkkinä tästä Fiat 500. Asiasta voi lukea esimerkiksi Hesarin tuoreesta artikkelista (Ajoimme Vantaalla autoa, joka tulee olemaan pohjana miljoonille tuleville sähköautoille | HS.fi) Kolmanneksi mielestäni koko konsernin autoissa on löydetty muotoilullisesti hyvä linja. Tämä on toki makukysymys, mutta mielestäni jokaisella automerkillä on hienosti löydetty oma linja ja/tai moderni tulkinta historiallisesta ”sukunäöstä”. Kaiken kaikkiaan pidän Stellantiksen uutukaisia hyvännäköisinä autoina. Neljänneksi Stellantiksen yhtenä hyvänä puolena näen Kiinan markkinalla vähäisen presenssin. Niin sanottua kiinariskiä ei siis tämän autovalmistajan kohdalla ole samalla tavalla kuin monella muulla valmistajalla. Toisaalta asiaa voi ajatella myös menetettynä mahdollisuutena, mutta itse ajattelen, ettei Eurooppaan ja Yhdysvaltoihin fokusoituminen ole välttämättä huono asia.

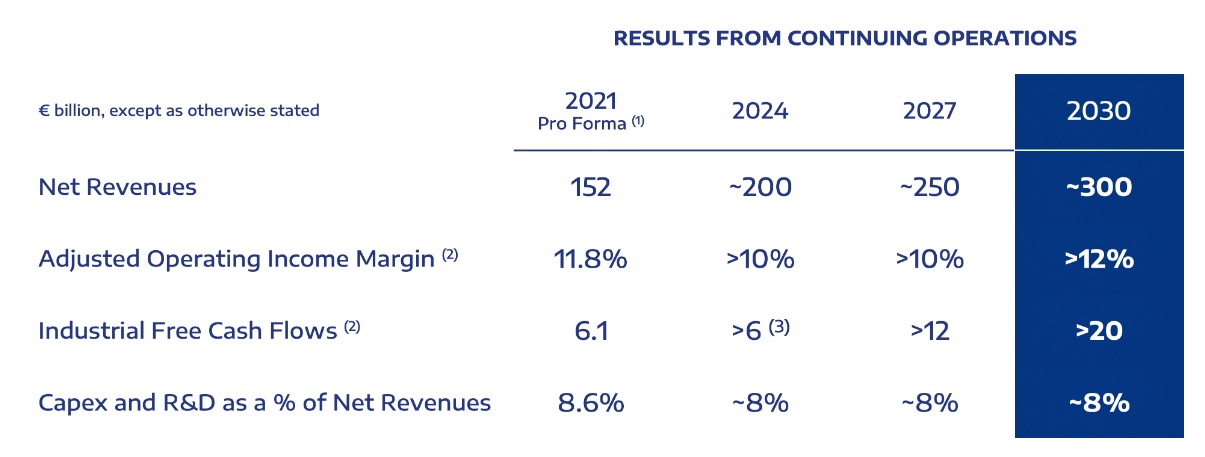

Italialais-amerikkalais-ranskalainen fuusio on herättänyt aivan ansaitusti pessimistisiä ennakko-oletuksia. Fuusioituessa Stellantis asetti monenlaisia tavoitteita, joiden kokonaisuus tunnetaan nimellä ”Dare Forward 2030”. Yhtenä ensimmäisenä tavoitteena oli luoda fuusion kautta säästöjä lähitulevaisuudessa. Tavoite asetettiin viiteen miljardiin, mutta juuri julkaistussa tilinpäätöksessä todetaan, että säästöjä on toteutunut kahdeksan miljardin arvosta. Optimointi Stellantiksella jatkuu edelleen, kuten tästä Kauppalehden jutusta ilmenee: Sähköistämisen satoa –Autojätti irtisanoo 2 500 työntekijää | Kauppalehti . Muutenkin asetetut välitavoitteet on joko saavutettu tai ylitetty todella reippaasti. Esimerkiksi kassavirtatavoite asetettiin kuuteen miljardiin ja toteutunut oli viime vuonna 12,9 miljardia. Tärkeimmät tavoitteet ilmenevät yhtiön sivuilta Dare Forward 2030 - A Bold Strategic Plan | Stellantis ja tästä kuvasta:

Taloudellisesti Stellantis on siis ollut positiivinen yllätys. En sijoittaessani uskonut, että näin hyvin voisi mennä, vaan kuvittelin, ettei tavoittesiin välttämättä päästä. Vaikka tavoitteista olisi jonkin verran jääty, oli ostohinta mielestäni silti ollut varsin edullinen. Kesällä 2022 Stellantiksen arvostuskerroin kun oli varsin matala. Sitä se on toki edelleenkin, sillä p/e on alle 5 ja osinkotuotto yli 6%. Yhtiö on nettovelaton ja sillä on 29,5 miljardin euron nettokassa. Tämä on melko massiivinen peilattuna yhtiön markkina-arvoon, joka on vain 84 mijardia euroa.

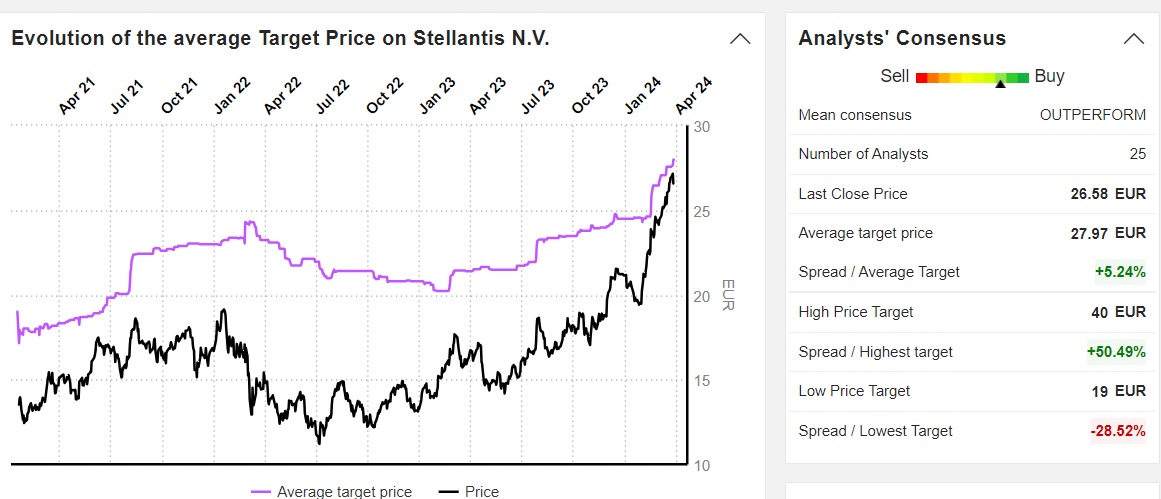

Yhtiön osakekurssi on ollut viime aikoina melkoisen rapsakassa nousussa ja analyytikko-odotukset ilmenevät seuraavasta Marketscreenerin kuvaajasta: