Tervehdys kaikille!

Tältä foorumilta puuttuu ketju Mercedes-Benzistä ja yhtiön mielenkiintoisen tilanteen vuoksi sellainen pitäisi mielestäni ehdottomasti olla. Mersu on ollut salkussani jo kolmen vuoden ajan ja olen kasvattanut omistustani säännöllisesti. Tähän alkuun todettakoon, että kiinnostukseni Mercedes-Benziä kohtaan on vain sijoitusrintamalla ja minkäänlainen automerkin fani en ole. On siis hyvin epätodennäköistä, että pihastani koskaan yhtiön tuotetta löytyy, mutta salkussani osakkeet ovat varmaankin hyvin pitkään. Omaan makuuni mersut ovat turhan kalliita kulkineita eikä niiden muotoilukaan ole koskaan silmääni varsinaisesti hivellyt. Tiedostan, etten mieltymyksieni kanssa edusta kansan enemmistöä ja esimerkiksi Suomessa Mercedes-Benz on sekä miesten että naisten unelma-auto. Ohessa Iltalehden suhteellisen tuore graafi asiasta:

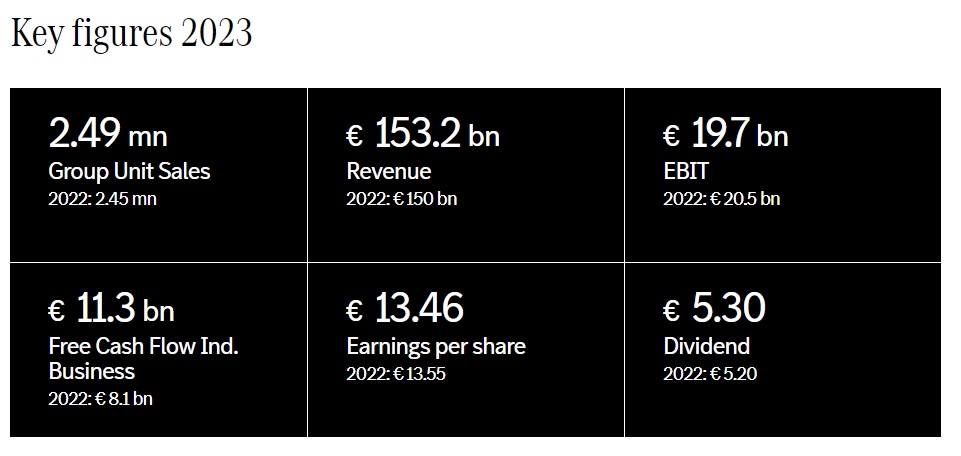

Olen sijoittajana arvo- sekä osinkosijoittaja. Yritän etsiä yhtiöitä, jotka kasvavat ja kykenevät nostamaan osinkoaan jatkossakin. Mercedes-Benz osuu tähän kategoriaan muutaman muun autovalmistajan kanssa erinomaisesti (näistä valmistajista ehkä avaan ketjun joskus myöhemmin). Yhtiössä houkuttelee kaksi seikkaa: taloustilanne sekä strategia. Taloustilanteen perusteella Mersu on hyvin matalasti arvostettu yritys. Markkina-arvo on viime perjantain päätöskurssilla vain 79 miljardia euroa. Yhtiö on nettovelaton ja nettokassan koko on 31,7 miljardia euroa. Alla olevassa kuvassa on vuoden 2023 avainluvut:

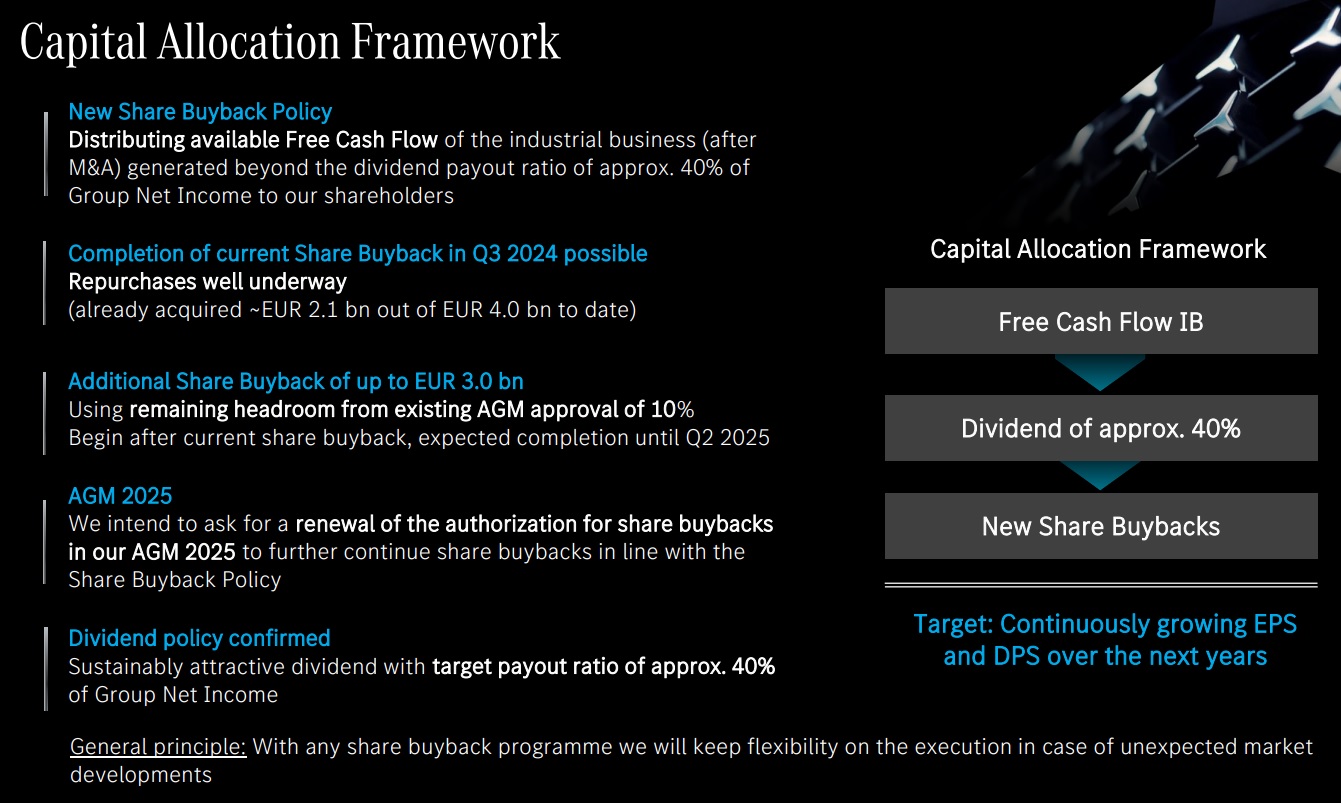

Mercedes-Benzin p/e on 5,5 ja keväällä irtoava osinko on 7%. Mersu panostaa tuotekehitykseen valtavasti, mutta siitä huolimatta vuodelta 2023 nettokassavirta oli 11,3 miljardia euroa. Kuluvana vuonna kassavirta on ohjeistuksen mukaan 8,5-10 miljardia euroa. Koska kassa on erittäin tukeva ja muutaman tulevan vuoden aikana investoinnit eivät ole räjähtämässä, niin koko kassavirta tullaan jakamaan omistajille osingon ja omien osakkeiden ostojen myötä. Mercedes-Benz on ohjeistanut, että osinko tulee kasvamaan tulevina vuosina. Omien osakkeiden ostoihin taas on allokoitu melkoisen merkittävä rahamäärä. Melko lailla tasan vuosi sitten aloitettiin neljän miljardin omien osakkeiden osto-ohjelma. Tuosta ohjelmasta on vielä 1,9 miljardia euroa käyttämättä ja oletus on, että ohjelma päättyy tämän vuoden kolmannessa kvartaalissa. Tämän jälkeen alkaa kolmen miljardin jatko-ohjelma, joka päättyy toisella vuosipuoliskolla 2025. On siis selvää, että omien ostoja kiihdytetään ja hyvin oletettavaa, että heinäkuun 2025 jälkeenkin osto-ohjelmat jatkuvat. Kaikkiaan valtuutus on toistaiseksi 10% osakekannan ostamiseksi. Ohessa mainitsemani asiat vielä sijoittajaesityksen kalvolta:

Talouslukujen puolesta olen myös pitänyt Mercedes-Benzin strategiaa pääosin fiksuna. Suuri muutos on toki liikenteen sähköistyminen, mutta olen ollut nopeuden suhteen pessimistinen. Mersulla on erittäin vahva asema polttomoottoripuolella ylemmissä hintaluokissa ja tämä markkina ei ole mihinkään lähitulevaisuudessa katoamassa. Nyt tapahtunut sähköautojen kysynnän odotettu kasvukuoppa sataa konservatiivisempien autovalmistajien laariin. Mercedes-Benz on tähän myös reagoinut ja ilmoittanut, että sähköistymisvirstanpylväät siirtynevät puolella vuosikymmenellä eteenpäin: Mercedes siirtää sähköistämistä tuonnemmas – Polttomoottorimallien tuotanto ja kehitys jatkuu | Kauppalehti . Vaikken asiasta ole ollenkaan innoissani, niin oletan, että tuleva Euroopan parlamentti ja Yhdysvaltojen poliittiset kuviot eivät sähköautoilua (tai ylipäätään vihreätä siirtymää) kiihdytä.

Osakkeen omistusaikana Mercedes-Benz on tehnyt kaksi suurempaa strategista liikettä. Ensimmäisten osakkeiden ostamisen kohdalla yrityksen nimi oli Daimler. Kuorma-autopuoli divestoitiin omaan yhtiöönsä ja nimi muuttui. Nämä saamani osakkeet myin nopeasti ja sijoitin ne takaisin Mercedes-Benziin. Toinen suurempi strateginen linja on panostaa katteisiin ja siirtyä enemmän luksusvalmistajaksi. Tämä tarkoittaa sitä, että halvemman hintapään tarjonta tullaan ajamaan alas. Siirtymä näkyy hyvin myytyjen autojen keskihinnassa. Kun se vuonna 2019 oli 51 tuhatta euroa, oli se 2023 jo 74,2 tuhatta euroa. Strategiaa kuvataan muuten tässä kalvolla:

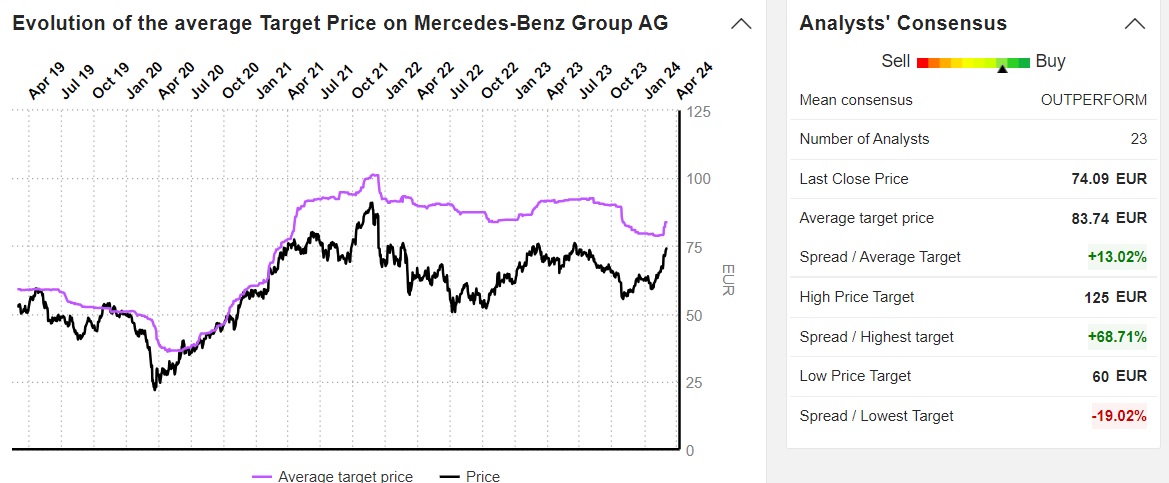

Tällä hetkellä analyytikkojen konsensusennuste on Marketscreenerin mukaan noin 83,74 euroa. Matalin tavoitehinta on 60 euroa ja korkein on 125 euroa. Arvostuskertoimet ovat matalat muiden eurooppalaisten autovalmistajien kanssa, mutta näkisin (tai toivoisin), että tähän puoleen tulee muutosta. Ei nimittäin näytä ollenkaan siltä, että perinteiset autovalmistajat olisivat surkastumassa tulevina vuosina. Toyotan kurssiin tämä oletus on tämän vuoden puolella jo varsin mukavasti tarttunut