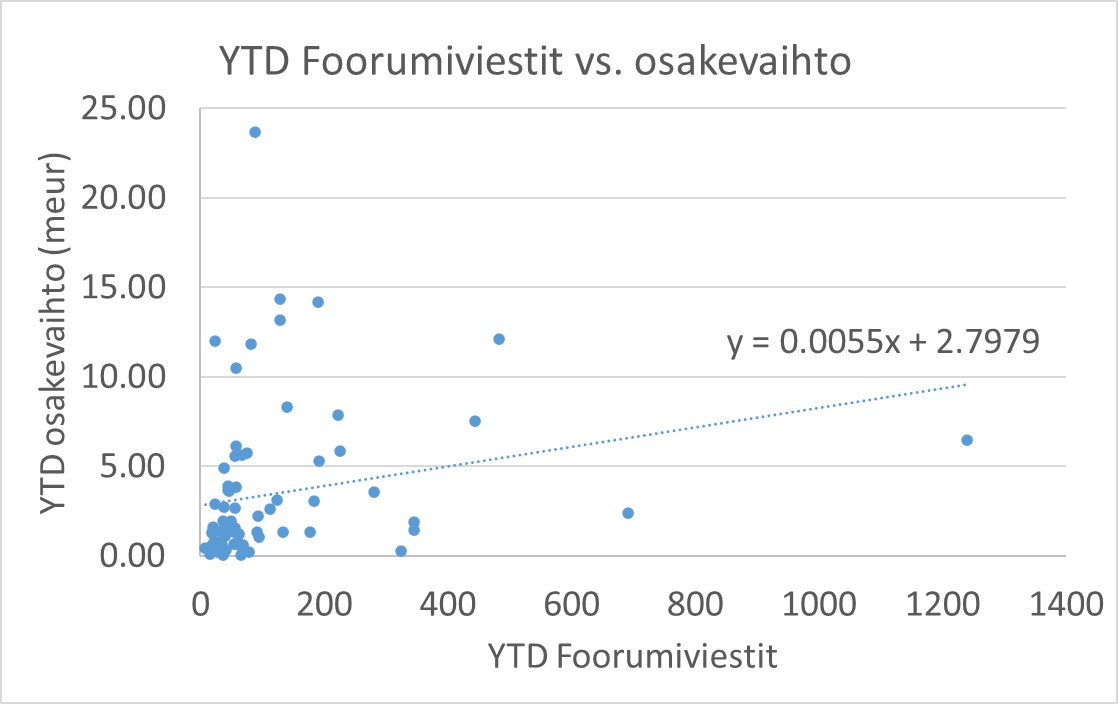

I also tested what it looks like when those two outliers are removed from the right, i.e., Optomed and Suominen, which generated a lot of discussion. After that, the scatter plot with trend lines looks like this.

The most traded one is Exel Composites, and the point at the bottom, to the right of 300, is our own Inderes.

Draw your own conclusions.

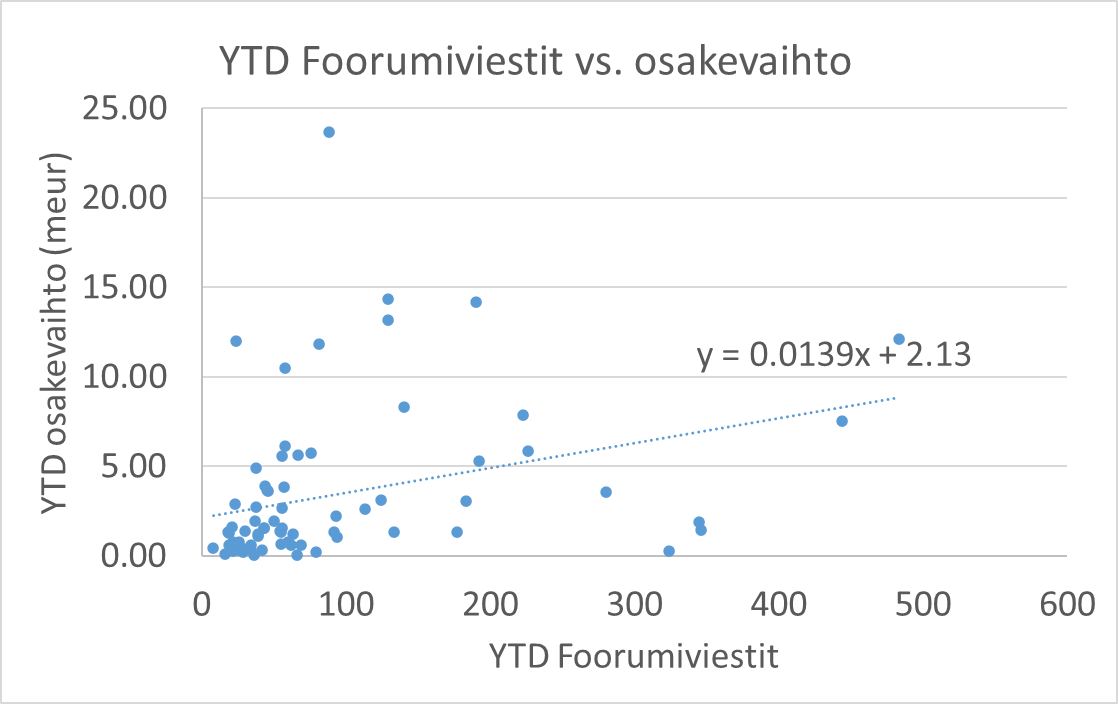

Perhaps block trades or other special situations that increase trading volume could also be excluded, though these also generate discussion. Another point of examination could also be the company’s representation on the forum.

Good reflection, the same has crossed my mind, and I have observed a correlation between trading activity and forum activity. In addition to absolute numbers, examining relative development could be meaningful, i.e., how the relative increase/decrease in the number of forum posts correlates with the increase/decrease in trading volume in different years. This would almost be a master’s thesis topic for someone. Feel free to pursue it

This message reminded me that in America, it seems to be quite common to announce if a CEO is selling X amount of shares over a period Y. I don’t know if that’s sensible with thinly traded stocks. In any case, such announcements and the systematic nature of sales would reduce speculation about kitchen renovations, the company’s status, and retirement days.

Of course not. But the better it stays on top of significant matters concerning companies (including news coverage), and the faster it communicates them to investors, the better it does its job. In this case, there was a window of over six hours between the information becoming public and the stock exchange release, so it’s not a matter of minutes.

As I alluded to in my Telia example, analysts haven’t stayed waiting for a company release before when “gossiping” about, for example, deals being made and transaction prices. And when they cite a public source in the correct way, what on earth kind of spreading of inside information is that then?

Well, yeah, but isn’t this dramatization getting a bit out of hand? I’m not just referring to your post, but it seems more like angry people want to vent their frustrations online by bashing the analyst and the research firm over something where both decisions are perfectly justifiable.

My own interpretation is that the CFO clearly broke the rules – as did QT Group, as the CFO was still the company’s CFO and one of the key persons in the company’s management, even if they were leaving soon.

What if the CFO has a document received upon resignation stating that the matter can be disclosed on Jan 29, 2026, and IR just sat on the press release until 15:30?

Analysts received the information on 28.01. A very good discussion has emerged, and thank you @Atte_Riikola for responding clearly to my message and explaining how things went down.

Knowing Fiva (FIN-FSA), charges for using undisclosed inside information will be brought against OP’s customers who utilized it when selling shares

Personnel changes in the management team are not automatically inside information that must be published via a separate release. It may or may not be. Based on the HS article, Qt and OP did not interpret the matter as inside information, and apparently, that is why Qt did not even intend to publish a release on the matter until analysts had specifically requested one. Inderes, on the other hand, stated internally from the start that the information was valuable and price-sensitive inside information, and therefore the information was not disclosed to investors.

Qt Group told HS that the company has not previously communicated management team personnel changes via a separate stock exchange release.

“After discussing with analysts, we moved toward more transparent separate communication under these circumstances,” the company stated via email.

It isn’t automatic for a CFO or even a CEO, although it is customary to disclose it; even in these instances, it’s a case-by-case matter. If you have a company strongly identified with its CEO, like Tesla, Qt, etc., a change in the CFO or other secondary figures isn’t necessarily price-sensitive information. There is no specific legal clause regarding the disclosure of a CFO change. The smartest approach would be to make it a policy to announce all management team changes via a stock exchange release, so there would be no need for guesswork.

Depending on the issuer and its organization, persons in various positions may be considered

to belong to senior management according to section 3.5.1. At least the CEO and the CFO

are considered such persons. Other changes may also be significant, in which case they

must be disclosed. Such persons may include, for example, key personnel. In such

situations, the issuer must assess materiality on a case-by-case basis, taking the

issuer’s organization and business into account. The issuer must disclose a change in senior

management when the issuer has made a decision on the matter, or when the issuer

has received information regarding such a person’s decision on the matter.

I interpret from that, that the CEO and CFO automatically belong to senior management, and thus changes must be disclosed.

You are apparently referring to the exchange rules (not the law), which have a separate section 3.1 dealing with the disclosure of inside information and sections 3.2–3.10 concerning “Other disclosure obligations” (not inside information). Therefore, the section 3.5.1 you referred to is not included in inside information according to the exchange rules, but you are correct in that regard that, according to the exchange rules, it should be disclosed unless otherwise prescribed nationally.

We have not interpreted this as being inside information. We have noted that this is currently in a bit of a gray area, and if we are at all uncertain, we will err on the side of caution.

It was more a case of Inderes assessing that the information might be price-sensitive, so they left the information out because they assumed an announcement would be issued.

Mikael, in the Qt thread you certainly gave a strong impression that you think that is inside information. 95% of the content of your messages in the Qt thread deals with inside information and the illegality of its publication, which is somewhat strange communication if this case is not about inside information. Now, a significant part of the thread is under the impression, following your messages, that publishing the information would have been illegal on Atte’s part.

Of course, I understand that, given your position, you cannot throw your employee under the bus, nor do you want to state this directly, as you would then be putting your client Qt and your colleague at OP in a difficult position with an accusation of a crime related to the disclosure of inside information.

That kind of intentional obfuscation about a “gray area” is likely the only option when your hands are tied, but in that case, it would have been better to completely omit those strong hints that Atte couldn’t publish the information because he could have committed a disclosure offense involving inside information.

Indeed, previously unpublished price-sensitive precise information—which is to say, by definition, inside information

Surely no analyst operates on the basis of intentionally withholding market-moving information or holding it back to wait for a press release? That is, if we set aside insider information etc. and speak on a general level.

It would be interesting to hear if it would have been in line with Inderes’ policy to report on the topic before the company, if, for instance, Helsingin Sanomat had leaked a news story about it beforehand. And if there were no problem with that, then it would be worth considering why using a widely-distributed source like OP’s morning review would somehow be different. Morally or legally.

In my opinion, Inderes should rethink the matter for the future. And hopefully reach a different conclusion as well. And I am specifically talking about sharing information published elsewhere. It’s a completely different matter whether to be the first to publish an email, and in that regard, the policies are certainly quite justified.

As such a particularly knowledgeable stock market expert, you surely know that, at the very least, the party/company that sent the message should have been instructed to issue a stock exchange release before the market opened. Then there wouldn’t be any problem.

The approach chosen by the analysts is in conflict with the interests of us retail investors.