Thank you @Harri_Sieppi ![]() You have been one of the most active CEOs on the forum. In the Witted thread, you have been the most active forum member. Others would do well to follow your example.

You have been one of the most active CEOs on the forum. In the Witted thread, you have been the most active forum member. Others would do well to follow your example.

16 Likes

Yeah, I’ve been active in those webcasts. But when held on the same day, they are too early, as I explained earlier.

3 Likes

I’m here and will be highlighting current themes every now and then. The channel is open, but questions are coming in quite moderately.

Earnings calls are our primary channel for answering questions, and in my opinion, they should be organized as soon as possible after the earnings release. In this case as well, this Inderes forum helps; you can post questions here that we will answer as soon as possible.

Regarding @Pohjolan_Eka’s three points; I think the first two are not an issue, but I don’t believe it’s my role to comment on the stock’s valuation.

/Kristian

26 Likes

Related to the topic. At the end of the ROAST, Capman’s Pia took a bold stand on the stock’s valuation:

“attractive valuation level” ![]()

From 42:19 onwards

From an investment firm, it is of course even more fitting to expect a view on the stock’s fair value. Time will tell how this view ages.

26 Likes

I’ll reply too, as I found this thread because of @MoneyWalker’s tag. ![]()

Regarding commenting on the stock’s value, I personally am very cautious about it. Few shareholders would want a company to comment that the stock currently seems quite expensive. Some shareholders might even get upset by that. Thus, when asked, there would be exactly two options: to say the price is cheap or to refrain from commenting. For understandable reasons, it has become common practice for companies not to comment on the stock price at all, and that’s a good thing. Of course, one can talk and write around the subject, such as the development of key figures over time, or I might, for instance, suggest looking into certain international companies when defining a benchmark.

There was also discussion about service for private investors. I understand that it would be nice to be able to ask management questions at times other than just during the stream after the earnings release. However, the majority want the company’s comments while they are fresh, and that’s why these are typically organized on the same day. In a company like Gofore at least, the days following an earnings release are extremely busy, so I personally consider the practice excellent where the same stream is shown to analysts, institutional investors, and private investors, and everyone can ask questions if they wish.

The company cannot escape the fact that large institutional owners and those considering acquiring a stake must be served immediately in the days following the earnings release if they so desire. Even if a specific party receives better service than an individual private investor, it is ultimately in the interest of all shareholders. At least I feel that Gofore’s stock being included in dozens of international actively managed funds is significant for value creation and, in the long run, in everyone’s interest.

Together with @Emmi_Berlin1 and @MIkael_Nylund, we are happy to hear how we could further improve our service regarding Gofore. Delivering the narrative and ensuring equitable transparency in all directions is by no means easy, but we are constantly trying to learn this too.

36 Likes

@Pohjolan_Eka - thanks for the provocative post. These below are my own thoughts and likely not everyone in the profession shares them with me.

(i) I believe we are hired for many roles and with different backgrounds. Fundamentally, the role is a customer service role, as you noted, but the stakeholders (management, investors, analysts, financial media, etc.) and information needs are diverse and the standards vary. Every portfolio manager and analyst has their own starting point. I have often said that “the smartest portfolio manager I’ve met studied geography at Cambridge.” That “first-level customer support person” description is true in a way; our job is to answer questions as well as filter and channel them further within the organizations.

(ii) I agree that sometimes companies may be too “guarded.” It flattens the story and takes away credibility. Our job is to know our company so well that we can answer almost any question accurately enough based on previously disclosed information. For example, the annual report contains a vast amount of information, and I would claim that over 90 percent of questions can be answered based on it, though not regarding the future.

(iii) Publicly these aren’t commented on, but of course, discussions are held with investors about valuation relative to peers. Here, we aim to avoid giving buy recommendations.

22 Likes

Today, Kamux’s Pajuharju commented on the company’s market value, saying that if you look at what they have in inventory and how much debt they have, the stock is currently quite cheap. (At 1:04:30)

")

Biohit’s Jussi Hahtela also made a similar comment at the end of this presentation, as mentioned above, stating that compared to the stock’s historical valuation, the share is currently trading below it.

Do those comments provide any added value for the investor? Everyone can decide for themselves.

17 Likes

This topic has been discussed in Finland and elsewhere. The European watchdog ESMA issued a stern warning in the spring regarding observations where significant stock movements had been seen following pre-silent calls and recommended that companies keep the calls open to everyone and publish a recording. Sweden’s FSA has issued its own recommendation on this, and some companies have already reacted. Here is an example from one of our clients: Press releases

14 Likes

Regarding the discussion on “whether a company is allowed to comment on its stock price,” FIN-FSA (Fiva) has taken a stand in connection with a bulletin regarding analyst calls. This is not surprising in itself:

- An issuer should not comment to analysts on the issuer’s value creation or the development of the value of its financial instrument, nor on an analyst’s forecast or the level of the result compiled in a consensus forecast. By providing such comments, the issuer places itself in a situation where it very easily, intentionally or unintentionally, provides analysts with such material additional information that has not been disclosed in accordance with regulations. Viewed as a whole, such information can have a significant effect on the price of the issuer’s securities and on market participants’ assessment of the issuer’s financial performance.

13 Likes

I attended a local IR conference in Denmark for the second time. It is a fun event as we rarely get to meet industry colleagues, but it was striking that in the all-day program, retail investors weren’t mentioned once in the discussions.

IR representatives complained that their job is to compete for a limited “pool of capital” and that the competition for attention is so fierce. These same companies have tens or hundreds of thousands of retail owners who represent a massive “pool of capital,” yet few lift a finger in this regard. One would think it is worth putting in effort where there is no competition for attention… The retail investor seems (outside of Finland) to be widely overlooked in the IR field, which is structurally biased towards thinking about and serving only one target group. It was telling when I asked one company’s IR about the role of retail in their team’s work, and the answer was “we have such a large single owner that it’s not a relevant segment for us at all” ![]() 10 billion euros of that company’s market value is free float outside the main owner, so it’s certainly “difficult” for a private investor to find a way to invest when even the daily turnover is under 50 million

10 billion euros of that company’s market value is free float outside the main owner, so it’s certainly “difficult” for a private investor to find a way to invest when even the daily turnover is under 50 million ![]() And this is an extremely well-known brand.

And this is an extremely well-known brand.

Finland is a positive exception in this context, thanks to the example set by several large companies. For instance, @Mirko_Sampo_IR, your successful work in this field is an interesting example in an international context ![]()

30 Likes

Thank you ![]()

What you wrote matches my own observations of IR work outside of Finland quite well. Of course, there is great variation in the IR resources of different companies, and it is an unfortunate fact that the institutional side tends to steal the lion’s share of attention. The situation isn’t exactly helped by the fact that various reporting requirements are constantly increasing, which also takes away from regular interaction with investors. However, service towards private investors can be improved with even quite simple things, starting for example with ensuring that IR pages are in good order and provide sufficient information about the company as an investment. It is also possible to increase visibility with smaller resources by utilizing external service providers and the media.

It is definitely worth investing in private investors, and at times it can even be critical. Our Topdanmark exchange offer would not have gone through if we hadn’t secured enough support from their extensive private investor base. In this, Inderes’ associate company HCA was actually a great help. We held five webinars with them aimed at Topdanmark shareholders and prepared a brochure sent by mail to all shareholders.

Summa summarum, I dare say that compared to other countries, private investors in Finland are generally served very well. Of course, one can and should always improve!

38 Likes

Closed analyst calls and subsequent stock price movements in the headlines again in Sweden

15 Likes

@Hanna from Wärtsilä sets a great example for all of us in well-managed investor communications ![]()

20 Likes

I will continue commenting on market value (or the market).

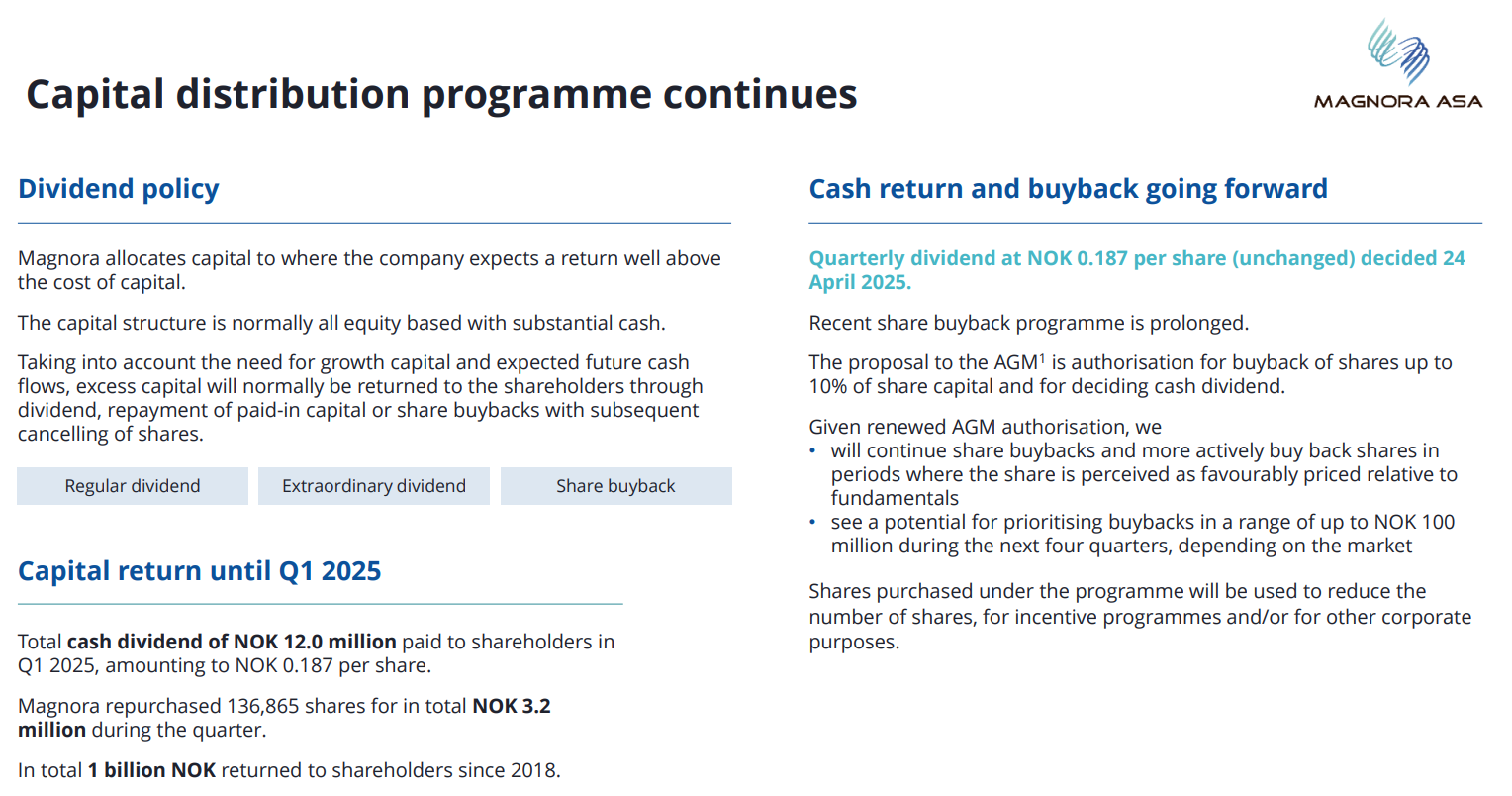

Magnora’s CEO Erik Sneve, in my opinion, took a bold stance in his Q1 monologue:

“A little bit about our dividend policy. I mentioned our dividend, NOK 12 million, down from NOK 12.5 million since we – own our own shares. We returned NOK 1 billion knocked to shareholders since 2018. And in the continuation with the weak stock market, we might be more likely that we’ll do more buybacks then increase the dividends if we have excess cash flow coming in. But this will be on the Board’s discretion based on market circumstances, when we receive the cash.”

Magnora is, by the way, a company where members of both the buyback and dividend parties can gather around the same campfire. Unfortunately, there are also members of the troublemaker party causing disruptions.

8 Likes

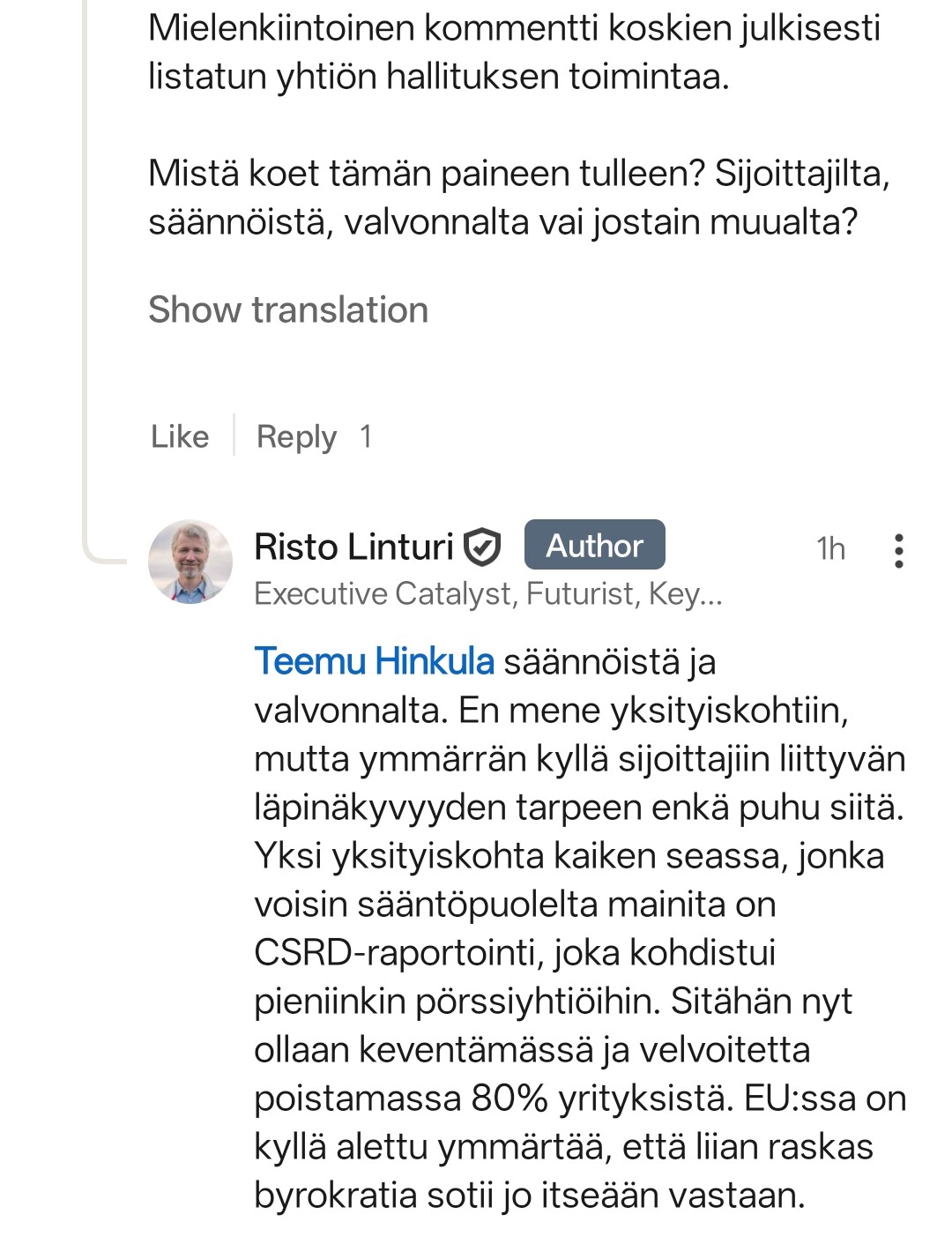

I’m sharing Risto Linturi’s opening up about a listed company’s operations here too:

13 Likes

For us, at least, this is organized with a slightly different idea:

- IR is responsible for “formal aspects” and leads the orchestra in these matters, allowing the board to focus on board work

- Meetings/decisions related to formalities are held separately as efficient Teams/correspondence meetings, with the board’s main meetings always 100% focused on the meeting theme

- Everyone understands and accepts that being subject to public trading involves regulation and is part of the job

24 Likes

I asked Linturi about this on LinkedIn.

Could there be some new business opportunity for Inderes in helping with something like this? ![]()

12 Likes

In the big picture, yes, a large part of what we do, especially on the software side, is solving the everyday challenges of IR and automating them. Regulatory and investor requirements are the most significant tensions here.

6 Likes

Since this thread is (hopefully) followed by several company representatives, I’ll also link my latest blog post here. It discusses board fees and composition.

https://www.inderes.fi/articles/elamaa-toimikunnassa-osa-3-or-suuri-hallitustutkim

9 Likes

In my opinion, this definitely belongs in this thread as well, hopefully representatives from different companies will watch that video. ![]()

![]()

5 Likes