In your post, you are setting high demands for the company’s management. Primarily, a company’s job is to focus on running the business. On ensuring that projects progress and the strategy is implemented. Boards, as statutory bodies, focus on ensuring that the company operates in accordance with laws. Individuals like Warren Buffett or, from Finland, Björn Wahlroos are, in my opinion, very exceptional individuals who created significant wealth with their razor-sharp strategic moves. It would be interesting to be a fly on the wall listening to what an average listed company’s board meeting entails. Would they be worried about the stock price development at all, or about something completely different?

When I look at the interim reports of gaming companies, for example, the management of many companies seems to think that money just comes from investors and then our job here at the company is just to monitor some monthly active users metrics and EBITDA so that running costs are covered. Investors fund the investments. Companies’ interim reports must include an income statement, balance sheet, cash flow statement, and a statement of changes in equity in the tables section. Often these do not go further or deeper than what the law requires. After all, Mikael Rautanen has also said that preparing an interim report is a heavy process for a small company.

We investors look at things through different lenses than the company management. If even an average investor looks at the actions of the companies they own through rose-colored glasses (ownership effect, Endowment effect), then what about a CEO who has their own reputation, relationships, history, and self-respect at stake in addition to their holdings? Would they do a DCF calculation in the evening and comment in an interview the next morning that our stock is about 4.3% overvalued? That is, if they even have a degree in business – far from everyone does.

I disagree that taking a loan would be worthwhile for buying back shares. A buyback is a tax-efficient alternative to a dividend, but if the cost is weakening the balance sheet, I would dump the shares. I would do the same if the company went into debt just to pay dividends. As a shareholder, I am most satisfied when management and the board take care of the company.

I’ll take a concrete example from my portfolio company JM (a construction company). At the end of 2021, 23% of the company’s balance sheet was cash. I was pleased with this because I thought like you, that in a poor economic cycle, shareholder value is created through share buybacks. Then came an ice age in new construction, and the company’s cash melted from 3,981 million kronor at the end of 2021 to 417 million kronor at the end of Q2 2024.

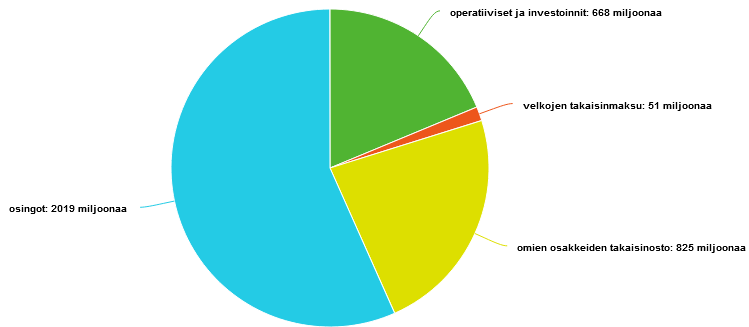

Use of funds 2021 Q4 - 2024 Q2:

Was paying dividends worthwhile instead of the company buying back its own shares? In my opinion, it was, because the stock hit rock bottom on October 23, 2023. Neither management nor investors knew where the bottom would be. With cash on hand, one was able to form their own assessment.