Name: Sensys Gatso

Country: Sweden, listed on the Stockholm Stock Exchange since 2003

Industry: traffic enforcement solutions

Revenue: 624 MSEK

Market Cap: 700 MSEK

P/B: 1.11

P/S: 1.05

IR: https://www.sensysgatso.com/investors

History:

Sensys Gatso (SG) is a company that has been operating in the traffic enforcement solutions field for over 40 years. The company has grown organically and through acquisitions, the most significant being the merger with a Dutch company named Gatso about 10 years ago. Today, Sensys Gatso is a global player whose business covers several countries in Europe, North America, Asia, and Africa.

Industry and products:

Sensys Gatso specializes in providing traffic enforcement solutions that help improve road safety and efficiency. The product range can be divided as follows:

- Traffic cameras: Speed enforcement, traffic control, and intersection monitoring (red lights, etc.)

- Traffic light control systems: Intelligent systems that optimize traffic flow

- Traffic information systems: Real-time information on traffic

- Services: Installation, maintenance, and consulting

Market Situation:

SG is one of the largest players in the industry and the largest of those focused solely on this sector.

The total market is growing, and for a European company, SG is strong in the US market. One reason for this is TrAAS (traffic enforcement as a service), where a municipality or city outsources traffic enforcement to the company for a fixed term. For the public sector, this solution is asset-light and lowers the barrier to procurement. In Europe, this model is not popular, at least not yet, which is why systems are still sold in the domestic market and operations remain with the buyer.

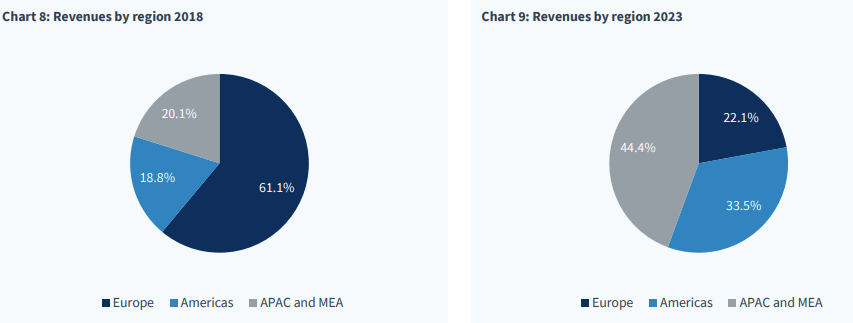

The image below shows (copyright: Kepler Cheuvreux, like the other images) the company’s internationalization in just under 10 years. At the same time, we see the relative shrinkage of the European domestic market’s share from 61% → 22%.

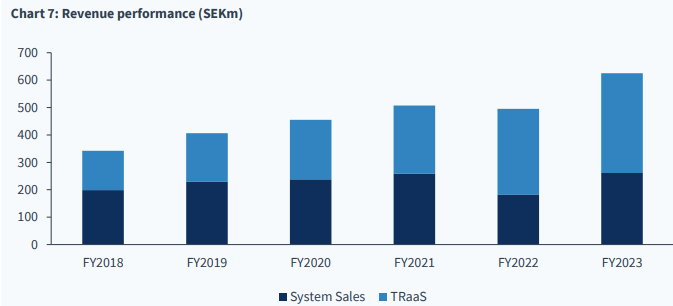

The company’s own sales mix clearly reflects the fluctuation between system sales and traffic enforcement services (TRaaS). TRaaS is growing steadily, but system sales vary according to the deals secured and their implementation schedules.

As in so many other sectors, the company is trying to smooth out seasonally fluctuating revenue streams from system sales by “servitizing” its operations and raising its margin percentage through TRaaS and aftermarket sales.

In terms of orders, they are (mostly) at the mercy of public sector procurement processes and political trends. For example, in Ohio, systems already sold are waiting for deployment permits after the administration changed approval practices. Thus, the temporal gap between sales and cash flow can depend on things other than the company’s own performance.

The company has a goal to reach over a billion kronor in sales by 2025, with TRaaS accounting for over 60%.

Since significant deals in Sweden and the Netherlands (totaling 1,250 MSEK, spread over several years) will start generating full revenue streams from next year onwards, the jump from the 2023 revenue of 624 MSEK is not impossible.

The Bottom Line and Cash flow

In system sales, the EBITDA margin has been between 10-15% in recent years, and in services, between 17-22%. Significant tender wins and the growth of the TRaaS model create front-loaded costs, and the sales mix affects the company’s annual margins. In next year’s target, the EBITDA level should be over 15%.

By the end of 2025, our ambition is to exceed SEK 1 billion in net sales, with more than SEK 600 million from TRaaS, while increasing our EBITDA margin to over 15%

Due to growth and front-loaded costs (tenders, TRaaS), the company cannot finance growth with cash flow alone, so this autumn a 30 MEUR bond loan was taken (euribor + 4.75) to finance growth and roll over previous debts.

The company is not particularly indebted. Nevertheless, one must keep an eye on large project receivables turning into cash so that growth doesn’t stall due to running out of “ammunition.” An advantage of the public sector is that the sensitivity to bankruptcy is lower than usual.

The image below clearly shows how annual Capex expenditures vary significantly. For the same reason, free cash flow fluctuates, although in the future, TRaaS income should smooth out the need for debt to cover project financing costs.

Risks and Threats

Autonomous traffic will eventually dry up one of the revenue streams, but realistically speaking, it will only bite into revenue from the late 2030s onwards, if even then. In any case, it takes time for the vehicle fleet to update. In my opinion, this known risk is perceived as larger than it actually is.

Regarding the United States, a bigger risk is the political situation—I assume a Democratic victory would be a better option for the company, although the state-specific situation likely matters more.

The competitive situation could change with AI and bring new players alongside traditional operators. However, one cannot succeed in this industry without a moderate capital requirement and credibility gained through a proven track record, so rapid disruptions are, in my opinion, unlikely.

The field is naturally competitive, so SG’s position and earnings level are not set in stone, just like with any other firm.

Why buy this too?

Why would now be a good time to buy? I’m not a real estate agent and therefore don’t advise buying all the time, but with the stock price at five-year lows (61.4 SEK), not much value is being placed on the company’s growth story and its turn towards profitability. A long downward slide is, of course, not a great reason to buy in itself.

I don’t know what negative factors the market can or cannot price in, but with basic performance and without major political upheavals, 2025 should bring growing revenue and positive free cash flow as large project deliveries are recognized as revenue. Exchange rate fluctuations add their own flavor to the game (especially the USD/SEK pair).

The gap to the Kepler Cheuvreux (buy) analysis target price of 95.0 SEK has widened significantly. Penser/Carnegie determines the DCF value to be 84 SEK and the fair value range to be 80-100 SEK. (Everyone can assign whatever value they wish to a paid analysis.)

Based on Kepler Cheuvreux’s estimates, the P/E would be around 11 with 2025 figures, with growth still around 20%. Based on the company’s comments, the largest growth investments are now behind them, so the benefits of TRaaS should be increasingly visible toward the end of the decade.

You won’t get dividends from this machine for several years yet, but instead of dividends, I’d rather enjoy the growth of the TRaaS business. (Hardcore dividend fans, put away the tar and feathers, it itches ![]() )

)

Reasons to sell the stock would be stalling growth and loosening cost discipline.

Disclaimer: If you somehow managed to trudge this far (or are just a masochist), thank you for your attention. This is not (either) a purchase recommendation, and the responsibility lies with the listener. In the writing of this, nothing was harmed except the Finnish language in the form of occasional anglicisms, limping grammar, and accidental typos.

–

Paid analyses:

It’s worth looking at these (especially the Kepler presentation) for numerical data on market size, etc., and a more detailed nuanced view. In this post, I focused on the big picture and the broad brushstrokes.

Kepler Cheuvreux: https://sponsored-research.keplercheuvreux.com/be/kepler-file/document?file=EQ360P_1069137.pdf&id=8c7ae4d2-add6-11ed-bd0b-0050568f8cb8

Penser / Carnegie: https://www.carnegie.se/pdf/commissioned_research/Y3JpZF84MDE4XzE0MTVfMQ==