Overview

I looked into Securitas’ stock and the company’s past few years. Perhaps a bit superficially, but I thought I’d share my observations here anyway.

The company’s market capitalization at the time of writing is approximately 91 billion SEK. Revenue for 2025 was 155 billion SEK and EBITA was 11.5 billion SEK. Improving the EBITA margin has been at the center of the company’s strategy, and in the second half of 2025, it broke the 8% target threshold. Last year’s net profit was 5.1 billion SEK, as depreciation, interest expenses, and one-off costs take a fairly large share of EBITA.

BUSINESS OPERATIONS

The company’s business is geographically divided into three regions: North America, Europe, and Ibero-America (including Spain, Portugal, and South America). Regarding last year, revenue was distributed such that 43% came from Europe, 40% from North America, and 10% from Ibero-America. However, 51% of EBITA comes from North America, 43% from Europe, and 10% from Ibero-America (the figures do not sum perfectly due to shared costs). This is due to the higher margin levels in the North American business.

By segment, the company’s business is divided into traditional security solutions, effectively guarding, and the Technology & Solutions segment. Across the board, the share of traditional security solutions has accounted for 64% of revenue, while Technology & Solutions has accounted for 34% of the entire company’s revenue. The share of EBITA, on the other hand, is split pretty much 50-50 between the segments. Technology & Solutions is indeed the company’s most significant driver for earnings growth now and in the future.

The company targets 8-10% annual real sales growth and had set a goal to reach an 8% EBITA margin by the end of 2025. Securitas succeeded in this, as the EBITA margin for the second half of 2025 exceeded the 8% limit. On an annual level, the EBITA margin has risen from 6.0% in 2022 to 7.4% in 2025. The company has also articulated an ambition to raise the EBITA margin to the 10% level in the long term. This is intended to happen specifically through the Technology & Solutions segment. The segment’s EBITA margin for 2025 was 11.5%. There hasn’t been a massive improvement here in recent years, as the segment’s EBITA margin in 2023 was 10.8%. Revenue for the Technology & Solutions segment has also remained nearly flat over the last couple of years, even decreasing slightly from last year. Meanwhile, the EBITA margin for traditional security services has risen from 4.9% to 6.0% from 2023 to 2025. Revenue in this segment has also declined over the past couple of years.

During this decade, the company has undergone a transformation from the traditional guarding business toward security technology and modern security solutions. The Stanley acquisition played a major role in this, laying the foundation for the current Securitas Technology business. Securitas’ foundation is in traditional security solutions, practically various guarding arrangements. To complement this, Securitas bought the electronic security solutions business from Stanley Black & Decker in 2021-2022. Stanley’s business is effectively the installation and maintenance of technical security solutions, such as camera surveillance, access control, and alarm systems. Stanley, now Securitas Technology, focuses on serving businesses instead of the lower-margin consumer business. The purchase price was $3.2 billion, or about 29 billion SEK. At the time of purchase, Securitas’ own market capitalization was hovering around 45-50 billion SEK, so the acquisition was remarkably large in size.

From the price chart, it can be seen that the market did not necessarily receive the acquisition with particular enthusiasm, although the downturn in European stock markets caused by Russia’s war of aggression certainly contributed to the price decline. In any case, an acquisition that significantly increased the debt burden and moved slightly further away from the company’s previous core industry (even though technical security solutions have better margins and grow faster) did not seem like an attractive option to many investors, especially as interest rates rose. However, the company’s share price has recovered well as the business has developed and the debt burden has decreased.

In 2022 and 2023, the reported net debt/EBITDA reached levels of 4.0-4.1 (though adjusted for one-off costs, levels were 3.3 and 2.6), but by the end of the year, it was down to 2.1. The company still has debt, but the amount has decreased steadily. The multiple has also been trimmed from the other side, meaning EBITDA has also grown after the acquisition.

GROWTH

According to the 2024 Investor Day materials above, the company expects basically low single-digit growth percentages for traditional security services, while the Technology & Solutions segment would grow faster than this. I couldn’t find the market growth figures at this moment. Relative to the market size, however, Securitas still has room for growth, even though it claims to be a top-3 player in both of its core fields. Despite this, revenue has remained stagnant in recent years. This is explained by what the company calls active portfolio management, which in practice means the company has pruned low-margin contracts and prioritized margin development at the expense of revenue growth. Examples of this include the divestments of the Argentine business and the French airport guarding business. Additionally, the company wound down its Securitas Critical Infrastructure Services (SCIS) business in North America, even though the original plan was to sell the business. The company lost its old contract in a competitive tender in the first quarter of the year, which eventually led to the shutdown of the entire subsidiary.

Organic growth for the company has, however, been around a couple of percent in recent quarters. The decrease in revenue has therefore been mainly due to business divestments, and the remaining operations are ticking along at a fairly steady but low growth of a couple of percent.

EARNINGS

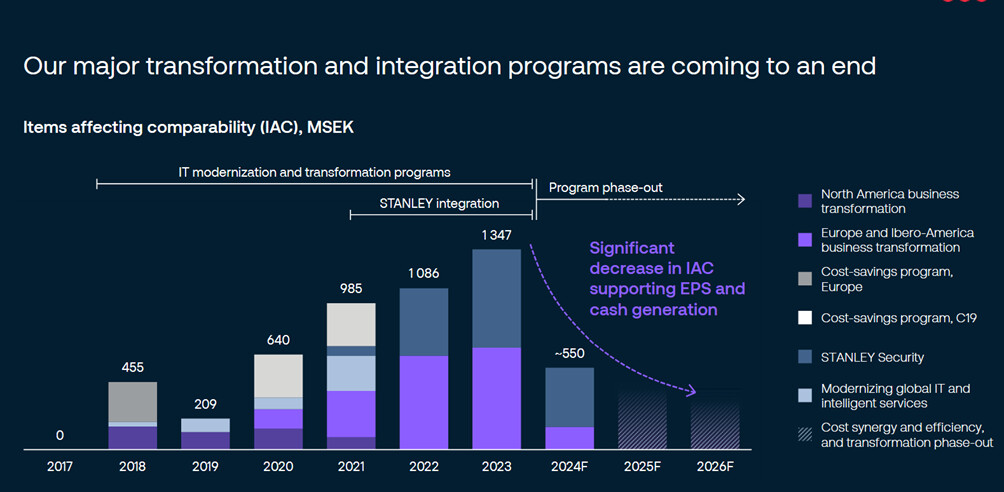

Securitas’ earnings reporting reminds me a lot of the Finnish company TietoEVRY, because there is no shortage of non-recurring items to be adjusted in the income statements. Pictured above is the source of Securitas’ one-off costs. The most significant individual reason is, of course, the Stanley integration, but businesses have also been heavily restructured otherwise. The peak in these one-off costs was seen in 2023, and they have decreased since then, although the shutdown of the SCIS business brought more items to adjust for in 2025. Because of these constant adjustments, I have personally looked more at the reported figures.

In addition to the gradual decrease in one-off costs, earnings growth is driven by the reduction in net debt. The company’s target level for the net debt/EBITDA metric is <3, so they are already at the target level. The company’s goals may involve inorganic growth in the near future within the Technology & Solutions business area, indicated by a small acquisition in Canada last year (Liferaft, revenue 134 MSEK).

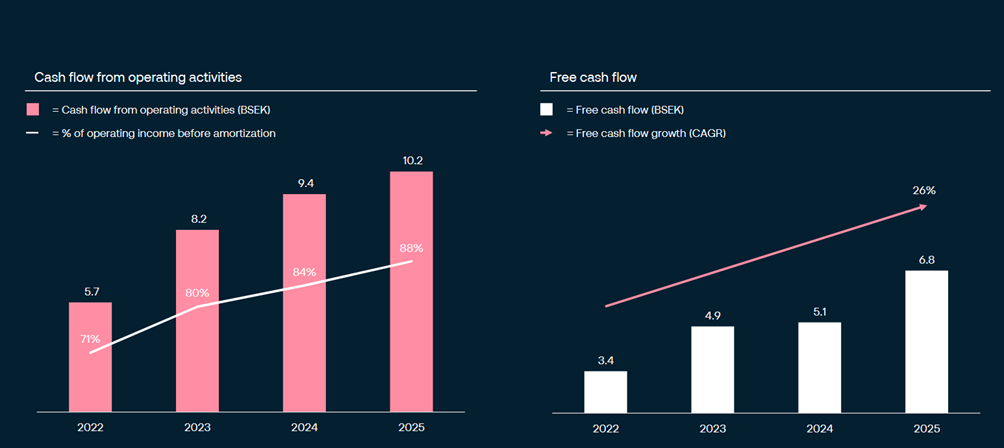

Along with earnings, the company has also managed to grow its cash flow. This is shown in the image below. The company also pays a dividend. From the 2025 result, the dividend will be 5.30 SEK. In recent years, the dividend payout has been approximately 40-60% of earnings.

VALUATION

The company is currently priced at a Forward P/E ratio of 12. The P/E ratio for 2025 is approximately 17, so the forward-looking P/E ratio already prices in earnings improvement. In my opinion, the company has made the right moves by trimming away underperforming businesses and focusing on margin improvement. The company has successfully reached its goal regarding earnings improvement by achieving an 8% EBITA margin. The next milestone will be reaching the company’s growth target.I don’t own the company myself, at least not yet. In my opinion, the multiples aren’t particularly high, but they aren’t exceptionally low either. The company has successfully completed an acquisition that was large relative to its size, which has lowered the risk level. If the growth outlook can be clarified and the current forward-looking valuation multiples are earned, I might buy some at some point.