It’s not too late to start even at 65. That wasn’t the point. The point was just that it’s worth starting as early as possible. If that’s 37, then good. If it’s 48, then good. You can’t turn back the clocks, so the best time to start stock saving is NOW, if you haven’t done it before (and if you’re not in the terminal phase with some serious illness, in which case it might not be worth starting to invest.)

My own recipe is to live in a small locality where living is affordable. The apartment is paid off and the maintenance fee is small. Also, that I don’t have children and currently live alone. I started exactly 10 years ago, just under thirty, and now my portfolio is about 230k, with a return of 300.98%. I consider that a pretty good performance for a blue-collar worker earning under 50k a year. For many years, I worked a lot of overtime and put a large portion into stocks, and I certainly don’t regret doing it. If I had been really frugal, my stock wealth could be considerably larger, but one must have cars and motorcycles too. If I were to do something differently, I might not have paid off the cheap mortgage faster but invested that money instead. But then again, being debt-free also feels light.

64 Likes

Today’s combined value of investment instruments approx. €127k + approx. €20k in interest-bearing accounts. The hobby was started from scratch (or actually from a deficit the size of a couple of thousand euro visa bill), if I recall correctly, in 2018 (before which there was some struggling, but nothing decisive or significant). I should read the oldest posts, that will bring this back to mind.

After that, I also opened a traditional brokerage account (AOT) with Osuuspankki, gave up my Nordnet share savings account (OST), and have now almost entirely transitioned to being an ETF and fund investor, having realized that stock picking is not for me.

23 Likes

I started my university studies in my early twenties and at the same time ended up working for a very good company. The office was close to the university, and the job basically only required being reliable and mastering the systems. Shifts were 7–8 hours long, but sometimes there were very few tasks. (However, when there were tasks – and I did my job well, tens of thousands of euros were saved for the company.) I spent my free time studying for university courses and developing various skills – and the salary kept flowing. When I came to work, I had a list of things related to work and then things I advanced during working hours. ![]() My supervisors knew about this and it had their blessing, because I did the job I was originally hired for very well. And the most ridiculous thing about this is that I could take on gigs on weekends, which then had an excellent hourly rate. I was somewhat of a workaholic back then.

My supervisors knew about this and it had their blessing, because I did the job I was originally hired for very well. And the most ridiculous thing about this is that I could take on gigs on weekends, which then had an excellent hourly rate. I was somewhat of a workaholic back then.

So, for several years as a student, my income was 3500–4000 euros per month – and I was practically able to study while getting paid for a large part of the time. I’ve thought afterwards that I was incredibly lucky. At the same time, for example, I ate 2.60 euro meals at the university every day, had all possible student discounts in use, and otherwise living costs were quite low. I feel sorry for how much pressure students are under nowadays. I’m not telling this story as if something like this would even be possible without good fortune.

I invested these accumulated funds in stocks, funds, and also sports betting (which I occasionally studied – and from which I also got side income for several years). From the very beginning, I also put quite a lot of income streams into nature restoration and various humanitarian projects. That is still important to me.

Now I have an almost debt-free apartment in one of Finland’s most expensive residential areas, forest (which I will probably never sell), stocks, various funds, money stashed away. And my primary concern in life right now is not what my investment portfolio is doing, but rather all other matters related to the future of the planet.

73 Likes

Today is a great day, I have been waiting for this day for a long time. My portfolio has finally crossed the €100,000 milestone. It feels like I haven’t achieved any big significant event in my life for many years, but this was an achievement for which I have literally worked hard and done overtime. Achieved this from a worker’s salary, under the age of 30 and in well under 10 years.

So what did this require? Mainly determined saving from monthly income and giving up many unnecessary things, e.g., frequenting bars, buying branded products, foregoing expensive hobbies, and compromising a bit on living space. I have found peace and contentment in a minimalist lifestyle. Balance of mind cannot be bought with money; it is found within oneself, through presence, and the ability to observe one’s surroundings.

So why did I save like there was no tomorrow? One of my biggest dreams is freedom, and financial freedom gives a significant advantage to that, the position to choose in many matters. But we are not at the finish line yet; the journey continues. Of course, I have now proven to myself that saving and investing work and bring enjoyment to my life, so I will continue on my chosen path, but naturally, I will also enjoy the returns along the way as my portfolio grows.

192 Likes

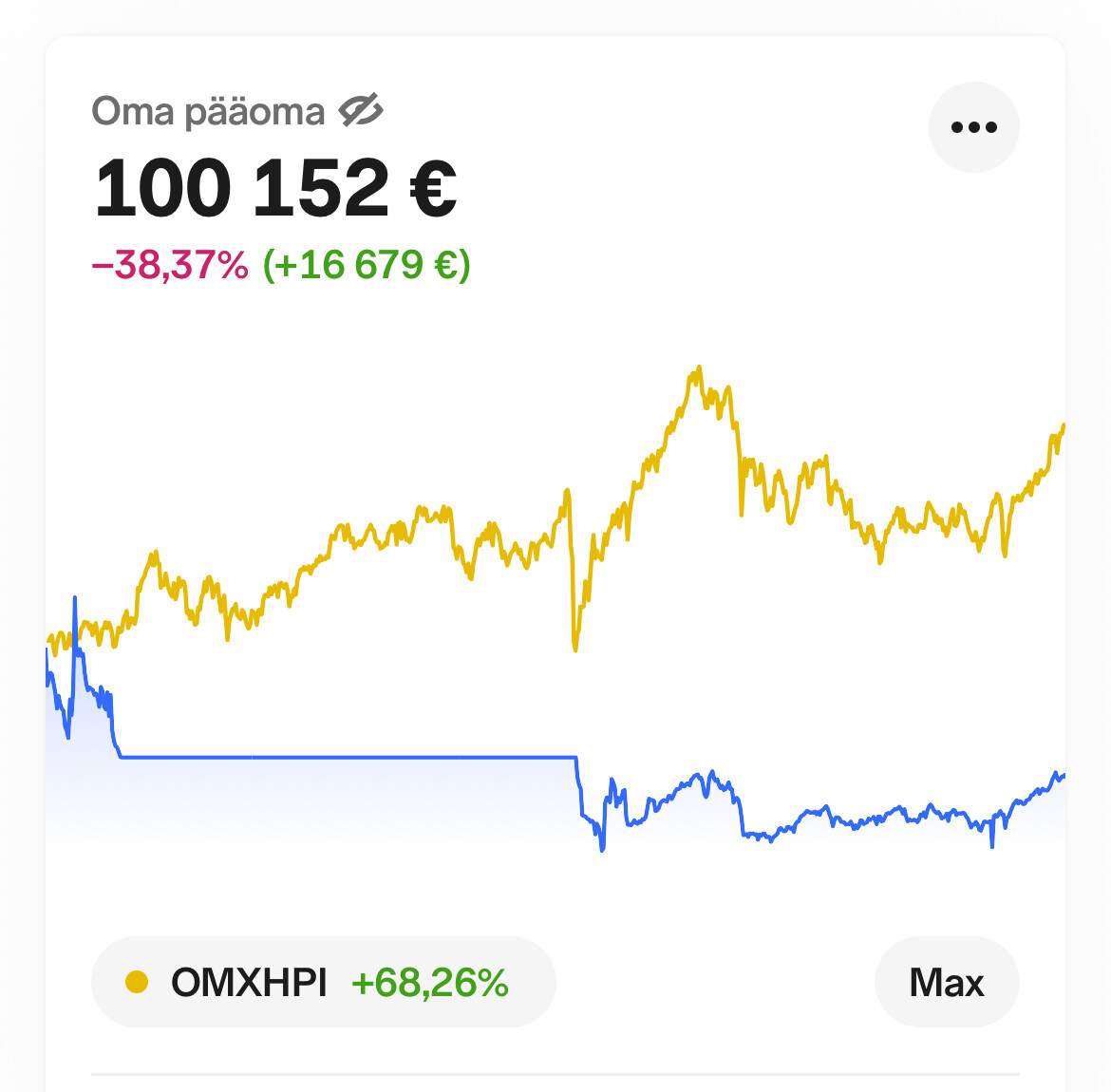

Kaipa se on aika kirjoittaa omakin muistinvarainen tarina tänne, kun tuo ”kuparinen” / ”haamuraja” meni 23.12.2025 puhki. ![]()

Kuvan aikajana on siis vain NN:n ajalta 2013-2026, mutta kuvastaa hyvin miten sijoittaminen on ollut osana omaa arkea. NN:n asiakkaaksi päädyin, kun minusta piti tulla miljonääri talvivaaran osakkeilla. ![]()

Taustalla oli tietysti se Arvopaperikeskusken ja OP:n salkku.

Mut tarkennetaan kuvioita alempana…

Kaikki lähti liikkeelle jo kun yla-asteen stipendi ja rippilahja rahat meni lähes lyhentämättömänä määräaikaistalletuksille vähän ennen vuosituhanteen vaihdetta. Puhuttiin kuitenkin varmaan jostain satasista, siis markoissa.

Mut ajatus säästämisestä oli istutettu nuoreen ja ehkä säästämällä vois saavuttaa jotain parempaa, tai suurempaa… ![]() ”Penni on miljoonan alkua” ehkä jotenkin paloi alitajuntaan lapsuudessa?

”Penni on miljoonan alkua” ehkä jotenkin paloi alitajuntaan lapsuudessa?

Samaan aikaan, tai mahdollisesti jopa aikaisemmin toisaalla, oli vanhemmat avanneet arvopaperikeskukseen mulle AOT:n minne oli saatu pesämunaksi ehkä kymmenkunta Sammon osaketta tämä nousi omina nuoruusvuosina kaikkiaan n.40kpl:n positioksi. Tässä ihmetyttää se, että Sampo on joskus jakanut Nordeaa ”osinkona”, mutta itsellä ei ole Nordean lapuista mitään muistikuvaa edes.

Osuuspankki oli joskus myös listattu ja näitä ilmaantui jostain ihan oman sijoitusvarallisuuden puitteissa ”kohtuullisesti” jopa lisää, vanhemmat tuki näissä hankinnoissa. Jossain vaiheessa oli jotain merkintäantejakin, mihin osallistuttiin.

OP:n kanssa tuli nuoruudessa tehtyä myös eläkevakuutus sopimus milleniumin hujakoilla, mihin olis kannattanut hakata rahaa huomattavasti enemmän, kuin se ensimmäinen 50€. Se jäi meinaan ainoaksi talletukseksi, mutta senkin arvo on nyt n.140€. Ehkä tässä hirvitti, että varat saa oikeasti vasta käyttöön eläkkeellä ja nuorena tää ei tuntunut yhtään hyvältä vaihtoehdolta.

Töihin mentiin heti, ku C-luokan ajokortti oli taskussa siinä 2001 kesällä. Olihan mulla ajoneuvon kuljettan perustutkinto suoritettu amiksesta. Tehtävä nimike puhtaanopitomies ja ylitöitä sai, tai joutui painamaan kirjaimellisesti paljon enemmän, mitä laki sallii. No se ei nuorta opiskelijaa haitannut päin vastoin. Tuolloin pääsi sellaisille tienisteille, että 10vuotta myöhemmin ei vakkariduunissa olis päässyt samalle tulotasolle. Palkka tais olla kaikkineen 12500mk/kk ja pari kuukautta painettiin yötä päivää. → Sinne tutulle määräaikaistalletukselle jäi kesästä varmaan 10000mk ja sama ralli heti perään seuraavana kesänä.

Tässä kohtaa 2001 viimeistään ruvettiin avaamaan omia kirjeposteja kotona ja seuraamaan tiliotetta ja tilin saldoa. Sinnehän oli makseltu jotain osinkojakin silloin tällöin.

Opiskelut jatkui toisella amistutkinnolla ja sen jälkeen oli vuorossa pääsykokeet AMK:n penkeille. Amiksen ja AMK:n välissä tuli käytyä myös intti. Intin jälkeen kesä taas töissä, ruuvaamassa autoja, ja haivainto, että tolla työllä ei kyllä rikastu, mutta elää. Muutto pois himasta intin jälkeen paljasta opiskelijalle karun todellisuuden. Opinto- ja asumistukien ei riitä opiskeluun ja elämiseen. → pakko mennä töihin ja onneks omalla koulutusalalla (autoala) oli innokkaalle myös lauantai duunia tarjolla. Tämän viikonloppu duunin ja saman työnantajan kesätöiden ansiosta ei niihin pieniin säästöihin joutunut koskemaan, mutta minkä kanssa pärjäs opiskeluajan.

AMK:n opiskeluaikoina pyörittelin jo Excelissä, korkoa korolle malleja OP:n ja Sampon osakkeilla. Osingot tais olla kaikkineen vuodessa siis joku n.200-300€. Tästä malli, että osingot takaisin pajatsoon + 1000€ vuosittain, niin nythän vois varmaan jäädä jo osa-aika eläkkeelle. ![]() Ajatusmalli oli tosin hyvä, mutta jostain kumman syystä ei koskaan ollut sitä 1000€ ylimääräistä ja osingoille löytyi myös siinä hetkessä parempaa käyttöä. Opinnot vähän venähti ja AMK:n 3 vuoden jälkeen puuttui vaan pari kurssia ja opinnäytetyö. Mut hei olihan sitä väliaikaiset katsurinpätyvyydet nyt voimassa ja kesäduuni paikka vaihtui toiselle sen aikakauden katsastusyrityksistä. Töitä oli silloin niin paljon, että mähän painoin sit vuoden duunia ja opiskeluista oli käytännössä välivuosi. Tuet piti silti nostaa täysmääräisesti, missä ei ollut mitään järkeä, mut olipahan varaa vähän harrastaa autoilua ja eka prätkäkin tuli hommattua tuolloin. No ei varmaan suuri yllätys, että Kela perus nämä tuet myöhemmin kaikki takaisin.

Ajatusmalli oli tosin hyvä, mutta jostain kumman syystä ei koskaan ollut sitä 1000€ ylimääräistä ja osingoille löytyi myös siinä hetkessä parempaa käyttöä. Opinnot vähän venähti ja AMK:n 3 vuoden jälkeen puuttui vaan pari kurssia ja opinnäytetyö. Mut hei olihan sitä väliaikaiset katsurinpätyvyydet nyt voimassa ja kesäduuni paikka vaihtui toiselle sen aikakauden katsastusyrityksistä. Töitä oli silloin niin paljon, että mähän painoin sit vuoden duunia ja opiskeluista oli käytännössä välivuosi. Tuet piti silti nostaa täysmääräisesti, missä ei ollut mitään järkeä, mut olipahan varaa vähän harrastaa autoilua ja eka prätkäkin tuli hommattua tuolloin. No ei varmaan suuri yllätys, että Kela perus nämä tuet myöhemmin kaikki takaisin.

Viina, naiset ja tupakka vei niin sanotusti vähän miestä. No koneet ja laitteet myös lähellä sydäntä, niin niiden taloudellinen vaikutus taisi olla todellisuudessa jopa suurempi. Mut en kadu, kivaa oli monesti. ![]()

Vakkari duuniin pääsi siinä n.2008, vaikka opiskelut oli vielä edelleen kesken. Tästä alkoi omasta mielestä, jos ei nyt kohtuullinen, niin ainakin tasainen kassavirta. Aina on tavoite säästöasteesta ollut korkealla, vaikka se ei olekaan toteutunut tavoitteiden mukaisesti. Eka muksu 2009 ja toinen heti perään 2011. Prätkän joutus likvidoimaan varmaan keväällä 2010 ja varat vaihtamaan uuteen pesutorniin.

2010 syksyllä tuli lyötyä kättä päälle myös omasta kämpästä. Tavoitteena oli pitää asumiskulut mahdollisimman lähellä olemassa olevia kuluja n.850€/kk + sähkö. No eihän se tietenkään onnistunut. Puolison tulot oli kuitenkin jotain satasia kuussa. Pankissa onnistuivat myöS avaamaan ASP-tilin, mihin meni se 50€/kk. Itse ajattelin, että tällä kuitataan sitten se asuntolainan viimeinen ero 25vuoden päästä. Pitäisihän siellä olla sitten se n.15000+ korot.

Palkka oli valmistumiseen saakka vähän alle 2k€/kk ja valmistumisen jälkeen varmaan 2,5k€/kk tällä tultiin toimeen ja tässä kohtaa alkoi varmaan rahasto säästäminen n.50€/kk joku pienen tuoton riskitön rahasto OP-maltillinen.

Näinä aikoina myös OP-päätti vetäytyä pörssistä ja ostaa omat lappunsa takaisin. Tuostahan tuli siis joku 8,5k€ lapaan. No nuori perheellinen laittoi tietenkin kaikki rahat ja vähän enemmänkin kunnolliseen perheautoon. Arvopaperikeskuskin tais lopetella AOT säilytyksen, niin siellä oleva tais siirtyä OP:n salkkuun. Kaikki yhdessä paikassa aika jees.

2013 sijoitukset oli muutama tonni rahastossa ja muutama tonni ehkä niissä Sammon lapuissa kiinni. Ei mitään suurempaa ja käteistä ehkä 5k€. → Olisko koko sijoitusvarallisuus huidellut jossain 10k€:n paikkeilla? OP-kiinteistö rahastoon tein näillä main varmaan myös jatkuva sopparin 50€:/kk.

Ruvettiin töissä puhumaan jostain kumman syystä Talvivaarasta, olihan se aika isosti otsikoissa. Tonni tähän kiinni, niin helposti siitä tulee 10-100k€ ku homma lähtee laukalle. Perustin puuha tilin NN:n palveluun ja pari tonnia sisään. No loppu on historiaa ja kaikki varmaan tietää kuinka hyvin siinä sit kävikään.

Tämän jälkeen alkoi n.5 vuotta kestänyt hiljainen kausi. Mikä näkyy hyvin myös tuossa kuvassa. Lapset kasvoi ja kulut nousi, mentiin aika lailla kädestä suuhun taloudessa. Tosin OP-maltillinen, OP-kiinteistö ja ASP kerrytti itseään maltillisesti, mutta tasaisesti.

Jossain vaiheessa ehkä 2015 oli duunipaikka vaihtumassa, mut palkan korotus korjas asiaa palka olikin jo n.3k€/kk. Mikä ei tosin ollut mikään maaginen kuitenkaan. Ylitöitäkin sai painaa viikottain. Peruspalkalla tultiin toimeen ja siitä jäi jopa ihan pikkaisen enemmän sukan varteen mitä aikaisemmin. Tosin verottaja ottaa aina omansa.

Olen aina myös pyrkinyt maksamaan veroja liikaa ja palautukset olen sitten pyrkinyt pistämään taas pajatsoon takaisin. Onhan ne välillä mennyt myös harrastuksiin.

Varmaan viimeistään tuossa 2015 kun käteen tuli n.2000€/kk tein ”talousmallin”, missä oli kaikki kiinteät kulut (n.1700€?) ajoitettu lähtemään tililtä palkkapäivää seuraavana päivänä. Tilille jätettiin pari sataa juokseviin kuluihin ja loput siirrettiin toiselle tilille jemmaan. Käytännössä siis ainakin kaikki ylityöt meni suoraan säästöön. Välillä joutui tietenkin käymään jemma tilillä, mutta kokonaisuudessaan se rupes jäämään plussalle kivasti.

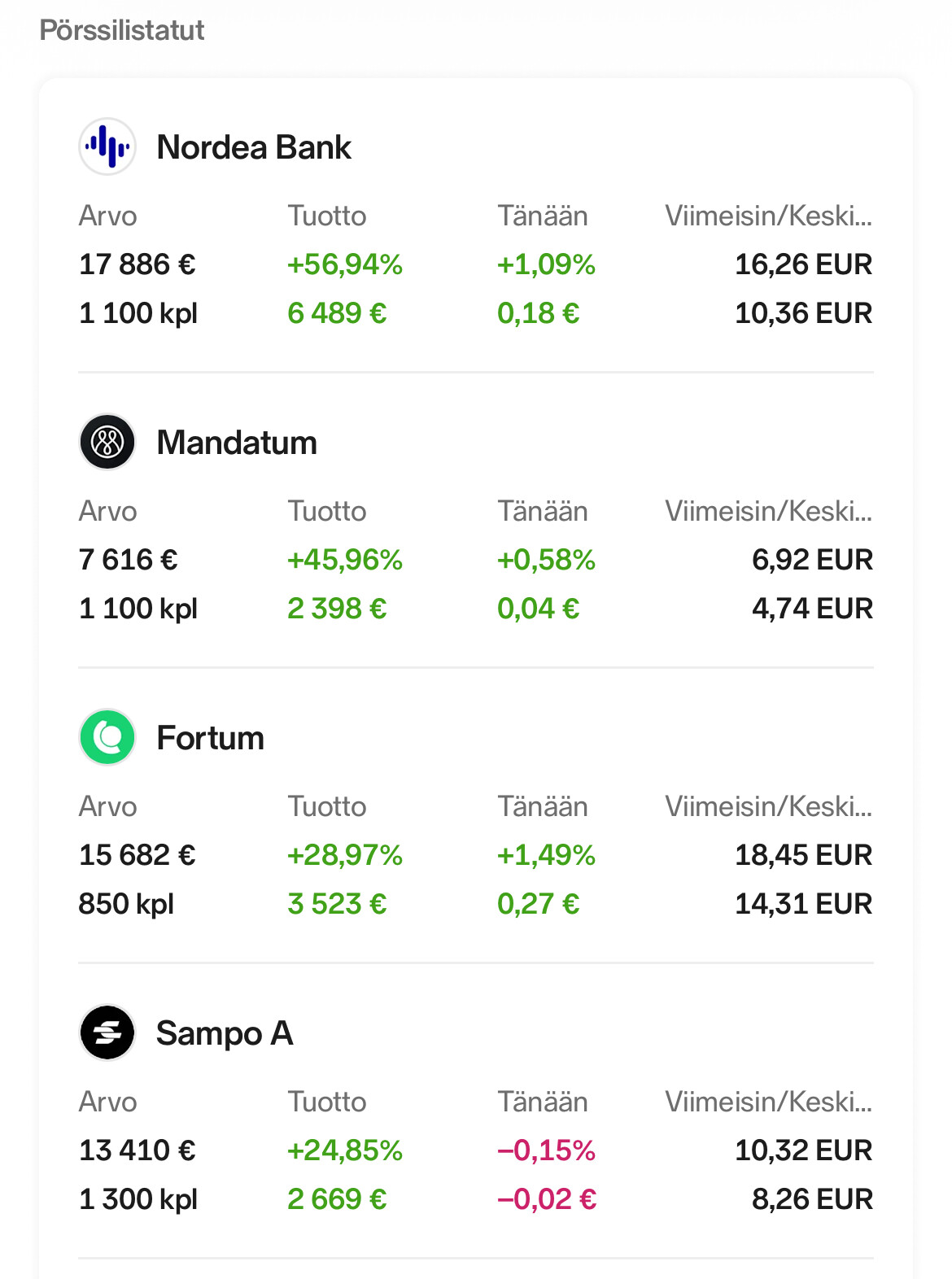

Sit muistelot niihin pieniin osinkoihin ja miten niitä sais kerrytettyä lisää. Ostelin jotain suomalaisia konepaja lappuja, Sampoa, Fortumia, UPM:ä ja Nordeaa mitkä nyt maksais edes jotain osinkoa ja saisin sen n.10vuotta sitten oivaltamani korkoa korolle homman toimimaan.

Duunipaikka vaihtui sit oikeasti 2019 ja uudessa duunissa päästiin sit melko nopsaan 4 alkavaan palkkaan. Uudessa duunissa myös käytössä työnantajan palkkiorahasto. Tähän en tajunnut heti tosin lähteä mukaan. Mut nykyään kaikki bonarit menee suoraan sinne ja taitaa siellä joku n.20k€ olla. Tämä on sellainen unohda mallinen juttu, mikä sit joskus yllättää positiivisesti.

Tuli vuosi 2020 ja joku räväkämpi influenssa tyyppinen juttu, mikä ei helpannut C-vitamiineilla. → Oliskohan säilytykset ollut yhteensä tuolloin joku 30-40k€ siis kaikki yhteensä. Tonneja tuli turpaan, mutta kokonaisuudessa jäin nipinnnapin varmaan plussalle, kun tyttären treenejä katsomossa seuratessa päätin myydä kaikki omistukset pois. Jälkiviisaana on helppo sanoa, että nythän kurssit on paljon korkeammalla, et oliko fiksua. Samaan aikaan aktivoin NN:käyttämäni uudestaan, kun se tuntui paremmalta alustalta, mitä OP. Myös varoja ohjattiin sinne suuntaan. Samalla havaitsin, että siellä oli n.tonni pölyttyneenä → ja mikä oliskaan parempi kohde tälle, kuin raketin lailla ylös syöksyvä Faron. Joo, vähän tuli takapakkia tässäkin.

2021-2022

OST mikä se sellainen on. Sehän kuulostaa hyvältä, kun sijoitusaika on sinne eläkkeelle saakka. Ostelin saman sijoitussuunnitelman mukaisesti lappuja OST:lle ja siirsin myös loput sijoitusvarallisuudet sinne. Mitä tapahtuikaan idässä? ![]() tuli taas tuulettimeen. Myin liian myöhään, mut ostin vielä alempaa takaisin, tosin tässäkin rupes laskumarkkinassa kädet tärisemään itsellä liikaa kun tein varmalla Sammolla muutaman tonnin tappiot.

tuli taas tuulettimeen. Myin liian myöhään, mut ostin vielä alempaa takaisin, tosin tässäkin rupes laskumarkkinassa kädet tärisemään itsellä liikaa kun tein varmalla Sammolla muutaman tonnin tappiot.

Jotain hyviä onnistumisiakin tuolta löytyy, mutta myös omaan mittakaavaan jäätäviä tappioita. mm. Nesteestä oli parhaimillaan reipas 6000€ tappiota. Enää vaan 2000€ onnistuneiden pienien ”tukiostojen” ja kehittyneen kurssin ansiosta.

Kokonaiskuva kuitenkin näyttää siltä, että en oikein osaa sijoittaa, mutta säästäminen onnistuu paremmin.

Tässä pari riviä, mitkä lämmittää mieltä ja kannattelee salkkua ja nehän on niitä osinkopuoleen edustajia vielä. ![]()

Mut kyllä se vaan niin on, että se sijoitussuunnitelma kannattaa tehdä ajan kanssa ja pitää siitä sitten kiinni.

Oma salkku on rakennettu hyvin maltillisella tuetulla alkupääomalla ja käytännössä voi sanoa, että niillä ylitöillä n.20vuoden aikana. Ehkä se pitkäjänteisyys rupeaa kantamaan vaan hedelmää. Päivätöitä pitäis tehdä vielä yli 20 vuotta, niin eläkesalkun rakentaminen ei pitäis olla mikään täysin mahdoton ajatus sentään.

Päivä vaihtelut rupeaa jo hirvittämään, mut helpommalla pääsee kun ei seurais aktiivisesti.

Toivotaan tosiaan, että tää ensimmäinen satku on se vaikein ja seuraavat helpompia. Kunhan ei niin, että eka on vaikee kerätä, mut toinen helppo menettää.

Hyvää ja menestyksekästä sijoitusvuotta 2026 kaikille.

142 Likes

One more story to add to the thread. In 2004, my wife and I were applying for a mortgage, and at the same time, the bank clerk “sold” us a monthly savings agreement for the bank’s own fund. Before that, investing was mostly limited to entertainment. After following the fund’s performance for a year or two, it became clear that the returns weren’t exactly dizzying. It was a heavily fixed-income weighted balanced fund. One good thing, however: an interest in investing (saving) was sparked.

Around that time, I read a lot on the discussion forum of a well-known Finnish financial magazine. It became clear that bank funds weren’t the best option for long-term saving due to their fees. At that time, Seligson’s funds were highly recommended precisely because of their low costs. People weren’t talking about ETFs back then. I sold the bank’s fund and started monthly saving into Seligson’s funds.

I started direct stock purchases in 2007. Nordea, Outokumpu, and Telia. Dividends were appealing – money in the account without having to do anything. Everything extra went into stocks and funds. A twenty-year timeline includes smaller and larger crises. They haven’t triggered any actions. In hindsight, they have been good buying opportunities.

Life has been lived and money has been spent, including on living, but expensive consumer goods have remained unbought. So, I haven’t been driving premium cars or acquired a summer cottage. Our home is “reasonably” priced. I haven’t received an inheritance or any major gifts – everything has been saved from my own salary. The home has been paid off half-and-half with my wife, which has made it possible to have more money left for investments. We’ve saved about €50k in fund portfolios as a nest egg for the children.

The strategy has been simple: buy and hold. Compound interest. Sales have been mainly for tax reasons to utilize capital losses.

The best-performing investments percentage-wise at the moment: Walmart and Neste. Portfolio allocation: about 75% stocks, the rest in funds and a small cash reserve. The stock portfolio is heavily Finnish-weighted and contains “popular retail stocks.” The largest single position is Nordea.

The purpose of the portfolio is financial security and to enable reducing or quitting the day job on my own terms. Perhaps I’ll get something back from the pension system eventually, in just over fifteen years, but you can’t rely on that alone.

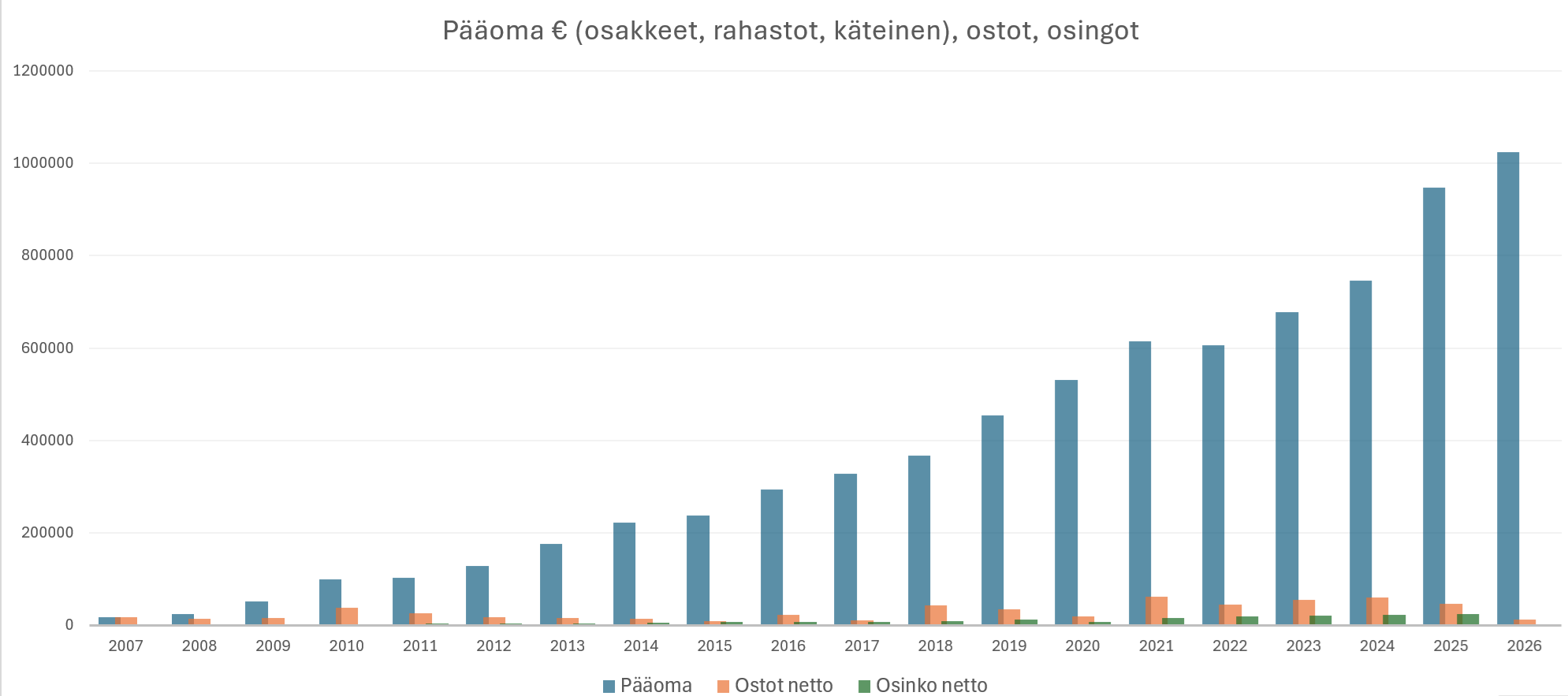

Portfolio performance

157 Likes

Recently, there has been a lively discussion about the financial literacy of Finns, and Henna Mikkonen’s article in Taloustaito raises important questions about whether we are truly as bad at managing our finances as statistics sometimes suggest. I recommend reading the attached article and reflecting on the small steps through which your own financial literacy can be transformed into practical wealth creation: https://www.taloustaito.fi/blogit/henna-mikkonen/olemmeko-me-suomalaiset-supersurkeita-omien-talousasioiden-hoidossa/#b02b182a.

Although Finns theoretically master the basics of finance relatively well, in practical actions, such as long-term saving and investing, we often lag behind many other nations. The article aptly reflects on why we are unable to translate our knowledge into practical actions and wealth accumulation.

Improving one’s own financial situation and increasing security often starts with very concrete and everyday choices. The first step is an honest look at one’s own income and expenses, as only accurate tracking of the numbers reveals true spending habits and potential areas for savings. Once the overall financial picture is clear, it is easier to set goals that motivate you to stick to the plan, even when the temptation for impulse purchases grows.

On a practical level, one of the most effective ways to strengthen your finances is the automation of saving and investing, where the agreed-upon amount is set aside immediately on payday without extra effort. This removes the need for constant self-discipline and ensures that a buffer for the future accumulates regularly. It is also important to understand the significance of time and the power of the compound interest effect, which means that starting to invest even with small amounts is significantly more sensible than waiting for larger sums to be left over for savings at some point.

Furthermore, financial peace of mind can be strengthened through continuous self-education and open discussion about money, as increasing knowledge dispels fears and uncertainty related to investing. Modern digital tools and banking apps make tracking wealth easier than ever, and utilizing them helps you stay up to date with your own progress.

13 Likes

I blame the education system. We are trained to be good employees for 10-20 years of our lives, but financial education only accounts for maybe a few weeks of that time. Perhaps, from a tax revenue standpoint, it is better that the country is full of hard-working employees and big spenders rather than frugal savers who start FIREing in their forties.

11 Likes

I’m 35, and money was never discussed when I was studying. It’s utterly absurd that in middle school, we’d sing and draw Moomins with chalk, but nothing was said about such an important topic. I’d say about 30% of my age group saves/invests. It almost feels like people prefer to buy investment properties instead. Additionally, if you can’t think financially, there isn’t much left from a worker’s salary for saving. Be that as it may, this topic should be discussed more. At home, at least, if not in school.

34 Likes

Can we get back to the topic of the thread?

You can discuss your own preferences and wishes regarding educational administration/curriculum here (I also commented in the latest messages there on the idea that everyone takes turns saying what I think is important to teach/learn. I also very gladly argued there why skiing and other physical activity is a very sensible use of time for teenagers, and why not for us older people too).

6 Likes

Yes!

It would be nice, by the way, if the great stories in this thread, according to the title, which are lost between all the philosophical reflections, could be compiled into a list. I would love to reread them sometimes.

8 Likes

A small update on my situation. I recently inherited €65,000. My portfolio was already well over €200,000 before the inheritance. I invested the entire €65,000 in AVWS, a global small-cap value ETF. My child will inherit it eventually. If all goes reasonably well, my child will receive an inflation-adjusted supplementary pension portfolio of about half a million euros solely from this investment, assuming they don’t sell it along the way.

50 Likes

Thanks for the interesting stories!

I recall encountering a study that stated, on average, 20–40% of life is what happens to you, and 60–80% is how you react to it. I think this is well illustrated in this thread.

My journey:

Starting point was a large family where the only form of saving was mortgage payments; otherwise, we lived on the poverty line. My parents were constantly stressed about money. For example, I didn’t dare to tell them when I had worms (again) because I knew the medicine was expensive.

If you wanted something, you had to earn the money yourself. Working for an almost non-existent hourly wage, I bought a Nokia 3310 at age 12. With the phone bill came regular expenses, and I had to continue working. I had entered the rat race.

I ended up in high school due to parental pressure; I would have preferred vocational school. Living at home had gradually become uncomfortable, so I moved out at 17, closer to my workplace. The rent was cheap, and the apartment was primitive; for example, there was no running water. The commute was 12 km one way, and I cycled it. After work, I washed up at the beach. I cooked pancakes for breakfast and dinner, as flour, sugar, and eggs were cheap.

I had to work a lot alongside high school to finance housing, food, school books, a driving license, a car, etc. I did my job well and received significantly more responsibility and pay than someone my age should have.

Succeeding on my own, overcoming the challenges of adolescence, a lovely girlfriend, and recognition from work gradually changed my self-perception and boosted my self-esteem. Slowly, I dared to dream bigger. This outwardly unnoticeable change was probably the most important turning point in my life.

When I told my friends I was applying to medical school, the reaction was disbelieving laughter: “you, really?” Deserved, I admit—after all, I had almost 12 years of underperformance in school. But that laughter spurred me on, and I decided to stick to my plan even more firmly. My identity began to build through my dream profession, no longer through where I came from.

Around the same time, I started thinking about how to build a life with less compulsory work. The negative impact of work on free time had become all too familiar to me. I read my first investment book, but with little money, active investing didn’t seem like a worthwhile idea. I hadn’t yet heard of passive index investing, but the seed had been planted.

After high school, I lived a fairly typical young man’s life: I worked, did my military service, traveled, chased women, drank, and got into fights. Money was tight, and the €2000 compensation I received for a broken nose felt like a small lottery win.

My 1st strategic move in accumulating wealth was to put all my efforts into getting into medical school. I stopped working, lived frugally, and studied for the entrance exams full-time for 9 months. I got in. As someone with dyslexia, university was such a challenging place for me that I didn’t have the energy to work alongside it, so there was still no money for investing.

The 2nd move was to take out as much student loan as possible and start investing. By this time, I had already understood that passive index investing was the best way to beat most investors. My inspiration included Pasi Havia’s book Erilainen ote omaan talouteen: vapaus, onni ja hyvä elämä (A Different Approach to Personal Finance: Freedom, Happiness, and a Good Life). At this point, following P.Ohatta, I also set the goal of achieving FIRE by age 35.

The 3rd and probably most important move came as a result of chasing women. I stopped trading and performed a strategic merger, as a result of which I committed to a thrifty and educated woman who had excellent long-term potential to develop into a wonderful mother for my future children.

The 4th move was buying a plot of land using student loan as cash one year before graduation. I had dreamed of building my own house since I was a little boy. Over the next 5 years, I gradually built a home for our family. When the house was finished, the mortgage was less than €200k, and the property’s value was just over €300k. The value itself is irrelevant because I want to live here until I die. The house was built to be fault-tolerant, and even considering the accumulating repair debt, living costs are low.

When I graduated, I was just under 30 years old, with approximately €0 net worth and €30k in student loans. As my income rapidly increased and I paid construction bills, my perception of the value of money changed. When making everyday purchasing decisions, I often didn’t even look at the price tag. However, by only buying what was needed, expenses remained reasonable.

Progressive taxation quickly hit me in the face during my first full year of work. And at the latest, when we had a few children, achieving FIRE at a young age became just a dream. Reconciling demanding work with the daily life of a family with children, so that I had enough time to recover and pursue hobbies, didn’t work. Quite soon, encouraged by the tax authorities, I switched to about a 70% work week. However, with expenses simultaneously rising, it was difficult to maintain even a reasonable savings rate in a family with children.

The 5th move to accumulate wealth was raising the risk level, i.e., practically introducing 10-25% leverage. With leverage, I made extra purchases in dips, and for example, I managed to time the corona dip almost perfectly by luck.

The 6th move has had the largest impact in euros, and thanks to this, I have managed to raise my savings rate to around 50%. This was achieved by minimizing pension payments, meaning I switched from being an employee to invoicing my work through a sole proprietorship.

I am now approaching 40, and it currently looks like no further moves are needed to accumulate wealth. As long as I continue to “larp” as middle-income, it’s enough to keep the machine running and well-oiled.

Net worth is now 6-8 times the family’s annual expenses, half of which is in investments. 30% of the portfolio’s value is appreciation, the rest is saved from salary. The relatively high investment risk level brought by leverage and a 100% equity portfolio increases returns, but the overall risk remains low, as the system has flexibility in many different directions.

The journey has not been without bumps. The feeling of emptiness brought by the end of the house project in the midst of the busiest years of family life made me “tilt” for a moment, which nearly caused my relationship to crash. Careful groundwork paid off, and my spouse dared to maintain her position in the midst of the turmoil; gradually, the situation improved, and we are now at ATH levels again.

I have postponed my FIRE goal significantly so that I can enjoy life with my children now. Currently, the plan is to stop putting new money into the portfolio and further reduce working hours when the youngest child goes to school. My vision is that on Fridays I prepare a nice weekend for the children, on Mondays I recover from the weekend, and Tuesday to Thursday I work for the time the children are at school. In addition, during school holidays, I will also always be on holiday. I will only allow myself to work more if the children start to miss their dad’s holiday.

Depending on market winds, I will be out of the rat race at the latest when the last child moves out of home. And if that doesn’t happen, I will have enjoyed the journey anyway.

My parents made a class leap after retiring by selling their almost debt-free house and buying an affordable apartment in a municipality experiencing population decline. They no longer have financial stress and were also able to fulfill their dream of spending winters in the warmth of the south. The role of grandparents suits them well, and our relationship is warm nowadays.

I feel deep gratitude for my situation; life is pleasantly light, but very meaningful.

196 Likes

Here’s my story, in short, from zero to half a million (basically in a year).

I started saving in 2019 with my first permanent job. In the beginning, I didn’t save much money because I like to travel and don’t really budget my expenses.

My first investments were saved monthly into an index, later adding dividend-paying REIT companies, Nordnet credit, and small speculative positions.

Between 2019 and 2025, I had accumulated 40k. Then came the collapse of spring '25, and my capital dropped to about 10k due to high leverage. I stopped to think - with diversification and saving, it would take at least 15 years to reach a million-euro portfolio, probably longer. Instead, if I threw all traditional wisdom out the window, took a lot of debt, and concentrated, the path could be faster. I had already chosen multibagger stocks before - albeit each time with too small a position and too early a sale.

Well, I didn’t take on debt; that’s why my portfolio had just exploded. However, I doubled my IREN position at 5 dollars.

By autumn, IREN had risen from 5 dollars to nearly 70 dollars, and the portfolio value was close to a hundred thousand for the first time. I had also delved into tungsten and understood that a fierce bull market was almost inevitable. I believed IREN would still go to 150-200 dollars in a few years, so I didn’t want to sell.

I had already bought EQR starting from 0.03 prices, but the position size was still too small for me to benefit significantly from my strong conviction. Between 2019 and 2025, I had more than tripled my earned income, so I certainly had the ability to pay, but capital was just missing. I ended up taking out a 60K loan and investing it in tungsten companies (EQ Resources & Tungsten West). The thesis started to materialize exactly as I had thought, and later I took another 60k loan.

Well, IREN has crashed from its highs - but at the same time, the Mandatum portfolio has grown to more than 10 times the size of the Nordnet portfolio.

My conviction in the tungsten bull market is unshakable. Even in my bear scenario, tungsten will still double this year, let alone the bull scenarios. I believe I will still make 5-10x returns in the next two years as miners grow with leverage relative to the raw material.

The next year will be extremely interesting. I’ll update here in a year to see how it went!

46 Likes

Do you really believe what you described is a horror scenario? Or has speed blindness struck?

15 Likes

I have outlined the demand and future supply for the next 5 years. There will be a huge deficit in tungsten for at least the next 2-3 years, probably longer. For many end-users, it is not crucial whether it costs $3k/mtu or $30k/mtu; what is crucial is securing the supply of the material.

A realistic bearish scenario is therefore this ~3x situation from current prices.

Of course, the whole thing could also collapse if there is a massive global recession and all demand decreases significantly. Another option is that China significantly scales up its production and starts supplying goods to the West. I don’t consider the latter to be likely.

And I don’t believe this is speed blindness, but a realistic view of what happens when a commodity with inelastic demand ends up in a crisis. I have noticed that, for example, AI also anchors the price to the previous price very strongly and cannot genuinely think about how high the price can rise.

But this is my thesis and we’re sticking with it. Let’s see how it turned out in a year!

7 Likes

I would almost dare to say that without a strong belief in one’s own thoughts, one will certainly not achieve a multi-million portfolio, although a portfolio of hundreds of thousands is possible for most. I don’t think believing in one’s own thesis is speed blindness when he has clear reasons behind his thoughts. It certainly requires courage.

Those who have truly become wealthy (i.e., usually entrepreneurs) have often at some point been all in on their company, having believed in their own thing. Believing in one’s own investment thesis and implementing it is probably no more extraordinary than mortgaging the family’s detached house to buy three excavators. Both require believing in oneself.

35 Likes

Recommendations on how to best get involved with this, are there similar ETFs available or do I need to buy a basket of different stocks?

2 Likes

There doesn’t seem to be a single ready-made basket for this. There are a vast number of projects coming into production, the first new ones likely being Tungsten West’s Hemerdon. Listed Western companies already in production include EQ Resources and Almonty, the latter of which is already very expensive.

We can continue discussing the topic here: Volframi (tungsten) ja Volframikaivokset.

3 Likes