I don’t actively hedge my holdings, but I try to invest by taking advantage of exchange rates. This practically means that if a currency is undervalued relative to the euro compared to its historical average, I favor stocks denominated in that currency. Over time, deviations from the average tend to normalize, so if, for example, NOK trades at 10.2:1 against the euro, the currency risk is likely on the investor’s side.

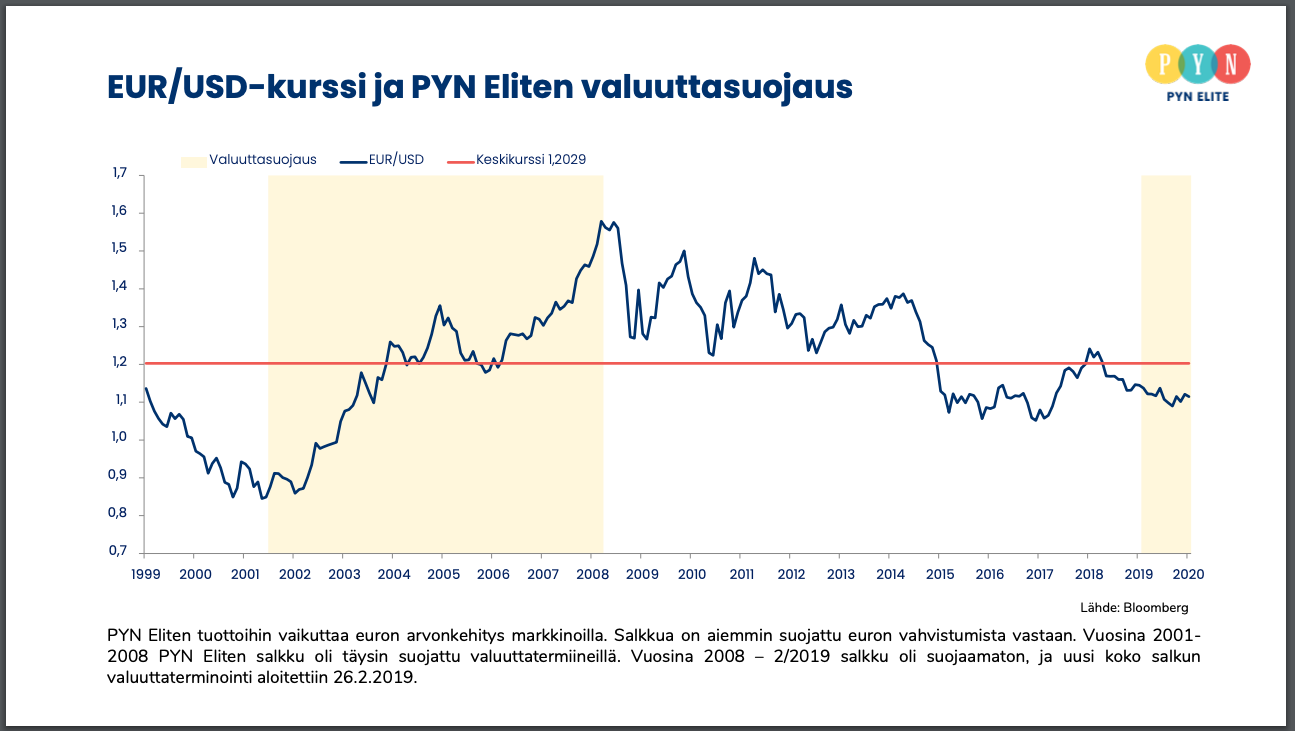

Conversely, I avoid stocks whose ratio to the euro is historically low. For example, I wouldn’t buy US stocks at all right now, not only because of their dollar-denominated expensiveness, but also because the USD hasn’t been this expensive against the euro since the early 2000s. Even if one made a good investment in the United States, there is now a lot of downside built into it. The USD, on the other hand, was a good currency to buy 10 years ago when it was cheap.

Additionally, a statistically cheap currency promotes economic growth, and stocks in growing economies generally perform better than in slow-growing ones. That is, if you buy a stock from an economic area with a cheap currency, taking advantage of currency risk, the stock itself is also slightly more likely to succeed because a cheap currency generally promotes the growth of the economic area. As a result of growth, the currency tends to appreciate relatively, and if you got in earlier, the situation is a win-win.

This is what happened, for example, with the dollar in the early 2010s. If you converted euros to dollars then, by converting back now, you would get, say, an average dollar-denominated market return of +200%, and in addition, this tripled dollar capital might still be corrected, for example, by a factor of 1.25.

At this point, I must say that I only hold stocks denominated in currencies of developed economies whose economic area I monitor to some extent. In practice, this means some European countries and the United States. Nearly 40% of my holdings are NOK and SEK denominated, purchased recently. I could also buy USD-denominated stocks, but the dollar is expensive now.

The investment target itself, of course, must be good, and one cannot be too much of a generalist always aware of everything.