I would like to open a general thread for the retail sector. There are many things that concern this sector in general, even though our shops are very different. Now good messages are scattered here and there. I don’t know if such an opening is suitable when the opener doesn’t have anything specific to say right now.

9 Likes

Good idea, the Kesko thread is terrible at least, due to the weekly price comparisons of bell peppers and toilet paper, but the moderators don’t seem to care. Meanwhile, you’re not allowed to go to the Kamux thread and mention if you can get something cheaper from Germany ![]()

6 Likes

I’ve been paying some attention to the used car trade lately; K-Auto has grown tremendously, but that’s probably due to a couple of store openings (+ a small starting position). Not so much because of a change in the overall market.

2 Likes

Grafton Group briefly shared its Q3 figures.

The slowdown in the economy and construction reduced demand at IKH.

In Finland, the slowdown in economic and construction activity reduced demand in IKH.

Let’s bring this thread back to life!

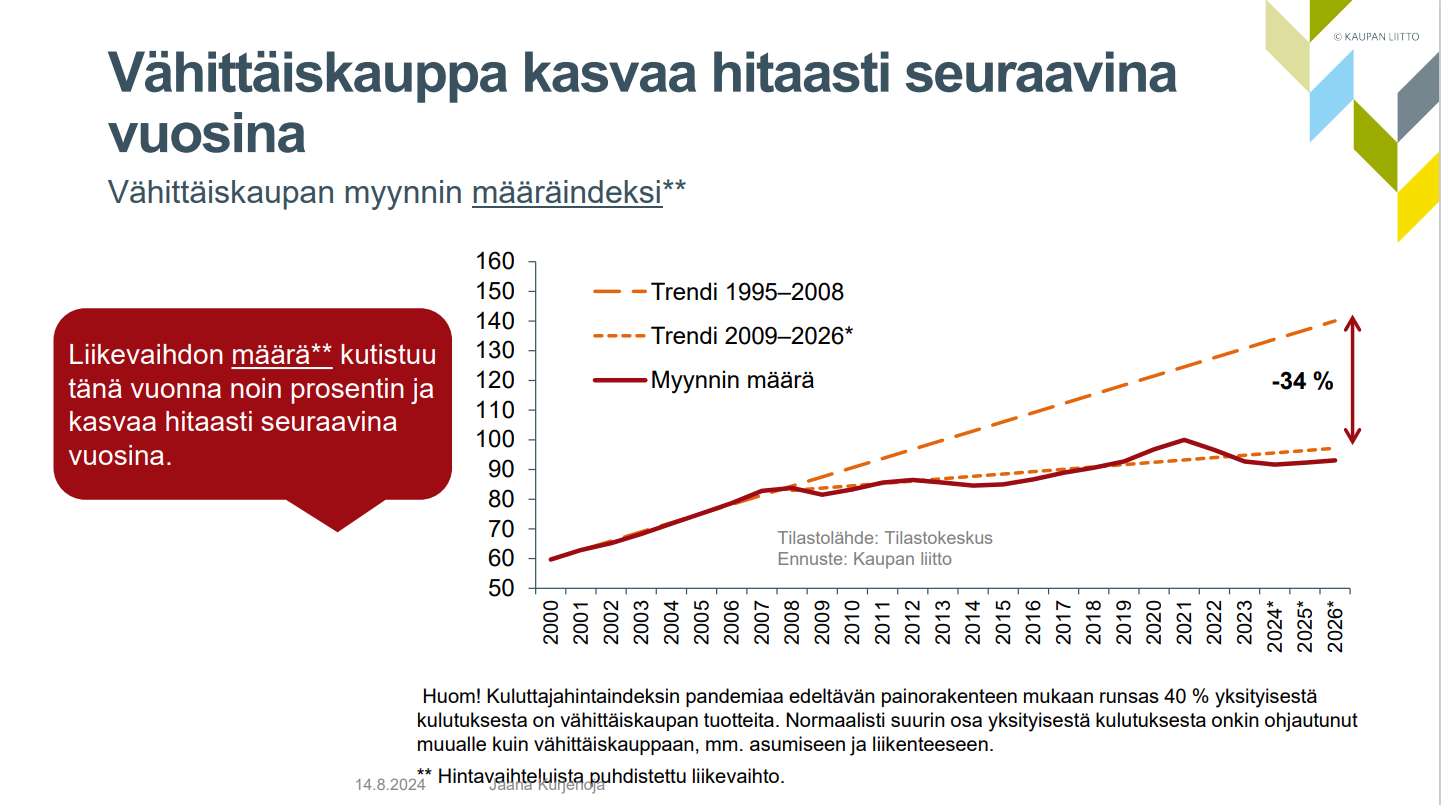

Today, the Finnish Commerce Federation released a review of recent developments and the future outlook for Finnish commerce. Below are a couple of interesting highlights:

Discount retail has recently grown faster than the retail sector as a whole. This is certainly driven by weakened consumer purchasing power, but there are a couple of other trends at play as well. Specifically, the popularity of discount stores as stores for everyone has grown, partly due to improved price-to-quality ratios. Additionally, discount store networks have expanded clearly faster than the rest of the trade sector.

Then, moving to the growth outlook. In H1’24, retail turnover was down 0.6%, while for the full year, the Finnish Commerce Federation expects a sales decline of about 1%. Predicted sales development for the coming years also looks sluggish (2025 +0.5%). If I read between the lines correctly, the reason for this sluggish growth forecast is generally predicted low GDP growth, a historically high (real) interest rate level, and the resulting consumer caution. Unfortunately, they did not break down the growth forecasts by sector.

The full review can be read here: Commerce will turn to slight growth next year – the government must support the international competitiveness of commerce with its RDI policy | Kauppa

14 Likes

So in real terms, growth is negative when the VAT increase adds 1.5% to everything except the growth in food sales?

In this sector too, forecasts could move from ruler analysis to using more complex parabolic functions, as the decline in the working-age population follows a curve of that shape ![]()

They are forecasting sales volume, so they dare to expect actual real growth. I’ll have to correct the terms in my own text!

1 Like

This was such insightful reflection that it needs to be saved here to be more easily found within the Tokmanni thread: https://keskustelut.inderes.fi/t/tokmanni-mahdollisuuksien-valintatalo/2105/2728?u=kettunen

9 Likes

I wrote about discount stores earlier this summer, using Sopuraha and its “euro market” as an example.

https://www.inderes.fi/articles/euron-tori-kiteyttaa-parhaiten-halpakaupan-idean

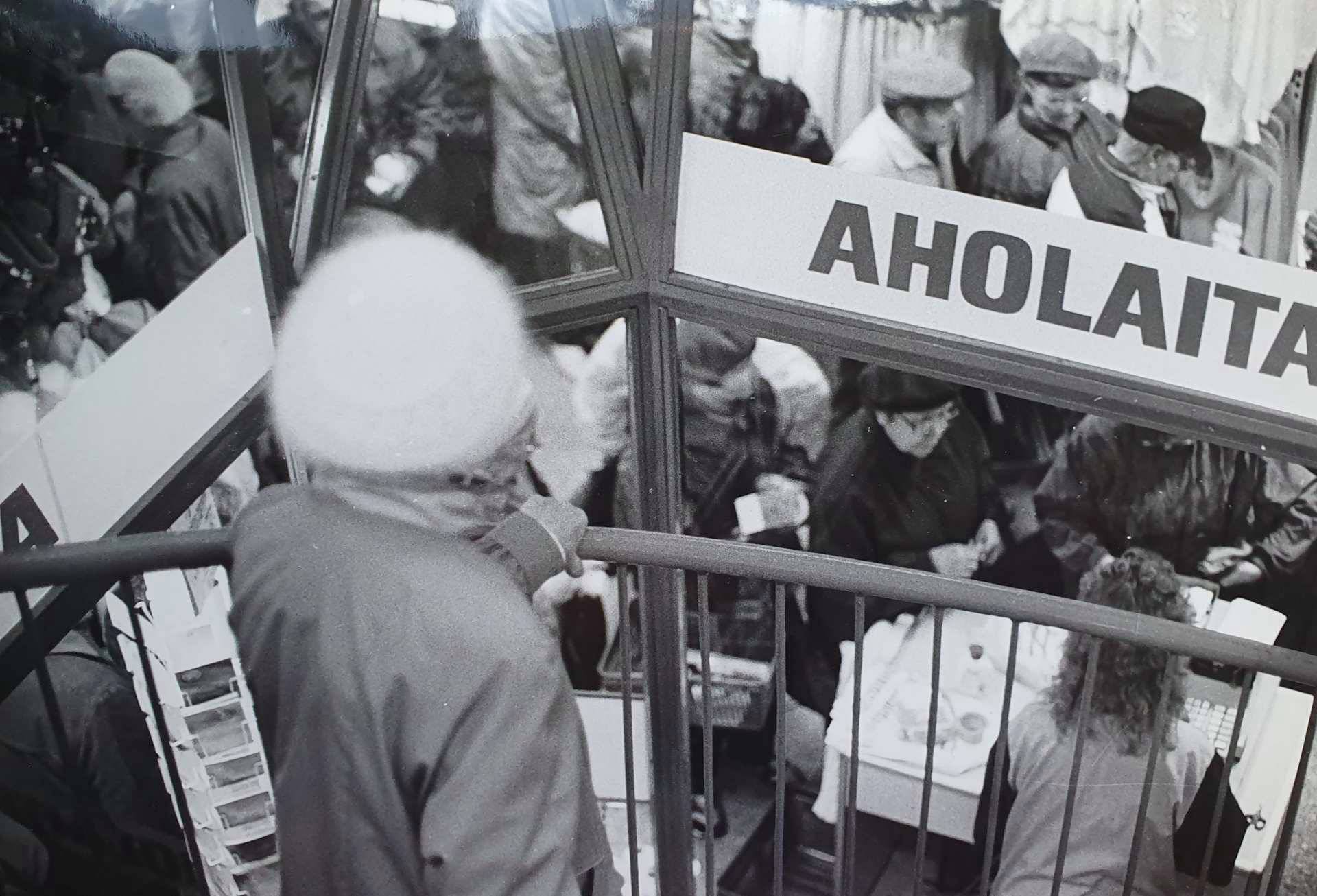

Here it is now in pictures.

Images

Early Saturday morning, it was still quiet. I picked up a few Dove shower soaps from the market for myself, which usually cost well over €2 in other stores—Tokmanni’s online store price is as high as over €4—and some soap bubbles for the child. As a fun detail, some products still had price tags from the markka era.

7 Likes

Since the blog post, newer financial figures have become available. Nearly another million euros in revenue was gathered last year, and revenue growth was a respectable 15.5%.

https://www.asiakastieto.fi/yritykset/fi/tukkusein-oy/09540724/taloustiedot

That is indeed what discount retailing is at its most authentic. If that was the discount store that brought back childhood memories for you, for me, it was a similar individual department store operating in the old premises of the Aaltonen shoe factory in Tampere. Unfortunately, it didn’t fare as well, and I remember from some newspaper article how the entrepreneur’s property was carried out of the business premises onto pallets etc. during the economically challenging times of the 1990s, and people went there to grab them without thinking much about ownership rights.

Supermyynti in the same city proved to be much more long-lived, although it operated in very modestly sized premises compared to those halls. It did, however, have a couple of downtown shops, and the selection was, to put it mildly, interesting:

http://turistinakotikaupungissani.blogspot.com/2013/03/vanhanajan-aarreaitta.html

Closer to modern-day chain discount stores in the Tampere region were Löytötavaratalo (4 stores according to Wikipedia) and Aholaita (27 stores in the Helsinki metropolitan area, Häme, and Pirkanmaa according to Wikipedia). Both of these chains went bankrupt. So, even that industry isn’t always a path to riches.

A rustle of history regarding Aholaita; I didn’t even remember that Eero Lehti was involved with that chain:

https://www.is.fi/taloussanomat/art-2000001446791.html

And regarding Aholaita, this is what the customer flow was like there too, back in the time of our ancestors, when the currency was the markka and when people believed in the eternity of marriage, the Rural Union, and the Soviet Union:

5 Likes

In Svensk Handel’s monthly e-commerce review, there was a story about the growth of foreign online stores (story on page 2). According to it, 12% of online shoppers had bought from sites like Temu/Shein. The Finnish Commerce Federation (Kaupan liitto) also mentioned that foreign marketplaces (Temu/Shein) have taken market share, while domestic trade is in quite a weak state. It remains to be seen how long their momentum lasts, but at the moment, consumers seem to be satisfied with cheap goods. Or perhaps some kind of experimental phase is underway.

It would be nice to get concrete figures on this (as well as on the GMV sales of Tori, etc.).

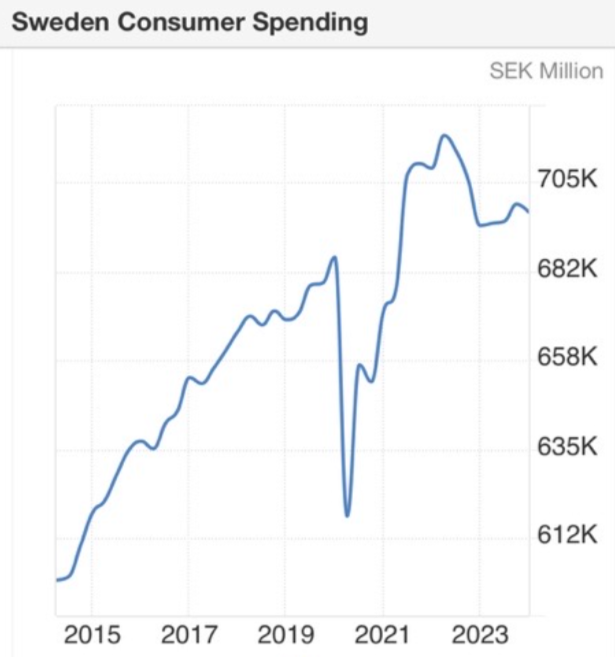

From the perspective of Verkkis (Verkkokauppa.com), it is interesting that online sales of home electronics in Sweden have risen in both Q1 and Q2.

5 Likes

Here is @Arttu_Heikura’s presentation from Inderes Day on the retail sector as an investment target. ![]()

Topics:

00:00 Introduction

00:16 Market situation

03:57 Retailers on the Helsinki Stock Exchange

05:22 Retail sector trends

13:48 Characteristics of a good retail business

16:24 Future outlook

19:58 Valuation levels

3 Likes

We recorded a podcast about retail this week with retail analyst Arhi Kivilahti! Go and listen to Arhi’s opinions on the retail sector and its future prospects.

Topics:

00:00 Introduction

00:20 Arhi Kivilahti

05:06 Kesko

13:10 Retail sector

16:26 Near future

20:18 Retail concept

30:40 Selection

37:15 Department stores

46:13 Retail location policy

50:50 Future trends

01:28:11 Favorite stores

13 Likes

The program didn’t meet my expectations. Specifically because I put it on at night thinking I’d fall asleep to the chatter, but it actually drew me in and cost me a night’s sleep. So, it was a very excellent, interesting, and suitably relaxed discussion.

One thing, however, left me wondering. I didn’t quite grasp Arhi’s arguments as to why discount retailers don’t invest more in e-commerce. There are certainly challenges with warehousing, but since those online stores exist anyway, it shouldn’t be impossible to put more effort into their technical functionality and order processing. My latest personal customer experience: I placed an order at Tokmanni on Monday. I had to try placing the entire order twice because the online store didn’t offer in-store pickup as an option at first. Now, this morning, I received confirmation that the order has been processed. So it’ll be ready for pickup sometime next week. I’m in no hurry, but those two-week delivery times are straight out of the era when you ordered things via mail order using paper coupons from the Ellos or Hobby Hall catalogs.

And I have to use Kesko’s relatively new K-Citymarket online store as a comparison. I’ve placed nearly ten orders there, and the packages have consistently been shipped within 1-2 business days. Even during the Christmas rush.

7 Likes

Work sometimes interferes with hobbies, and it was only now during my morning run that I got to listen to @Arttu_Heikura’s presentation on the retail sector as an investment destination. It was a pleasure to hear a young analyst’s insights – very good perspectives and highlights on themes that have also been raised on the Inderes retail forums. In the transformation of retail (too), short-term changes are typically overestimated and long-term changes are underestimated. D2C, marketplace-ization, circular economy, digitalization and AI, double volume benefits when growth comes from old stores (instead of new units), etc. As a new forum member but someone with some experience in retail, I have to say that Inderes is now “on the scent” – good, good!!

A good performance can still be spurred on, however, and I’d like to offer a few perspectives that should be understood and considered from an investment point of view regarding the retail sector in Finland.

Not just economies of scale & digitalization - but their combination

The 100-year trend in retail has been a transition toward ever-larger players. Because globalization & economies of scale. When you combine this with retail that is becoming digitalized, automated, and AI-driven, the combination of these has a cumulative competitive advantage effect. This is a classic “double trends, triple gains” example.

Most basic processes in consumer retail are extremely “susceptible” to the combination of economies of scale AND digitalization: Logistics (and all its stages: supply chain logs, manufacturing logs, central logs, store logs, last mile logs, and reverse logs), procurement, assortment management, pricing, marketing, sales steering, store analytics, store design, resource management, shift planning, business analytics & steering, competence management, customer service, after-sales, contact centers, etc. The basis for almost all medium-term competitiveness lies in these processes. Put simply, a retail operator’s ability to develop and invest in these processes results in linear growth in competitiveness. For example, if we take a contact center: a single excellent algorithm that handles 70%–50% of all retail customer contacts (with better customer satisfaction than a human) is not yet cheap fun. It matters whether the algorithm is bought/developed for 1k customers, 100k customers, 100m customers, or 100b customers. It won’t be long before we hear the term “cost per algorithm/customer contact” in investor calls from leading retail operators. Finland’s remote and small market slows this change, but it is not immune.

The big lie of blue-and-white glasses

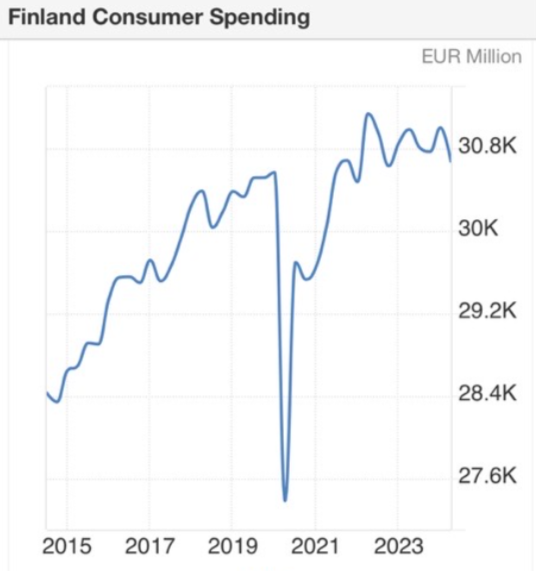

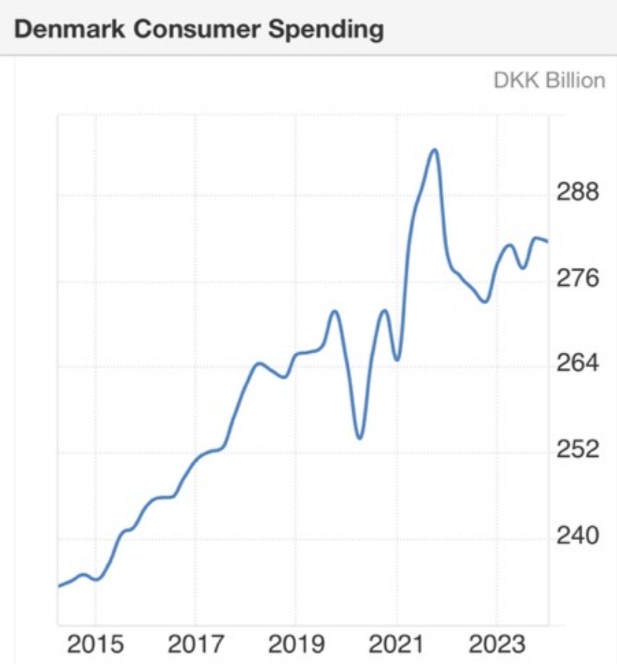

From this side (while listening to an otherwise excellent presentation), it unfortunately sounded like the investment perspective was viewed through glasses that were a bit too “blue-and-white” (nationalistic). Regarding the future outlook for retail in “Hesuli” (Helsinki), it would be fair to more honestly acknowledge the relatively high risk of the Finnish consumer’s trek through the wilderness – which continues. Right now, “the frog is still splashing in a pot where the stove has been on full blast for a long time.” Nalle (Björn Wahlroos) visits Finland once a year to remind us, “Finns, not like this.” There is no examples in economic literature where retail has relatively succeeded (compared to other industries or markets) when the population is aging and the national economy is chronically in deficit. In what year will Finnish retail again benefit from its proximity to St. Petersburg (as it did from 2000–2020)? A Finland based on the forest industry and machinery—and hopefully in the future, a “clean-cheap-energy-server-farm” Finland—does not support broad consumer market growth even if GDP starts to rise. Unfortunately, one of the only and most likely ways to increase consumer purchasing power is for interest rates to drop from 3.5% → 2%. Yes, it eases the pain, but it doesn’t cure the Finnish consumer’s underlying condition. This is because wage sum development is mainly driven by the public sector and is thus just “lengthening the blanket by cutting from the other end.” So, regarding future outlooks, it would be essential to broaden the horizon. And only by expanding the horizon to the other Nordic countries do the future prospects of retail operators change to an entirely different level. It has been a pleasure to notice strategic shifts: the faster the Tokmannis, Motonets, Verkkises, and Keskos can get into the Nordics and build competitiveness in growing consumer markets, the better. Last 10 years: FI +8%, SE +16%, and DK +21%.

An unnamed cooperative

I don’t know if I’m raising too dangerous a topic, but when following Finnish retail from a bit further away and in discussions with international market analytics firms, the Finnish retail customer’s everyday life is guided by a curiosity called a cooperative. As a retail investor in Finland, I would be very aware of this chain’s actions. No minister, MP, local politician, retail industry player, retail service provider, or market analyst understandably dares to bring this up, as the risk of becoming a job seeker or a former politician is high. What if, by 2030, in all of Finland’s towns of 30,000–40,000 consumers, there is grocery retail, all kinds of specialty retail, food, a barber chain, a gym chain, a discount chain, hobbies, a healthcare chain, a pet service chain, a beauty salon chain, an entertainment chain, a car dealership chain, a bank chain, an insurance chain, and even loans – all in prime locations, on their own plots, in their own large properties, with nominal rent… and ALWAYS in green. In every industry, they are under the competition authority’s radar, but as a combination of the “green color,” they are so powerful that an investor should be aware of it – it’s also worth remembering that a cooperative’s “quarter” is a different length than a merchant’s quarter. And this part of my text can also be seen as high praise for the cooperative for excellent work and strategic success – yet for a retail investor, the perspective is different. If/when the pie and consumer purchasing power in Finland do not grow significantly by 2030, all growth must be scraped from competitors. And one should be aware of “green card” competitiveness across many retail sectors.

I haven’t had the chance to watch Arhi’s interview yet. I hope to get to it next week.

11 Likes

What luck. ![]()

Unbeknownst to each other, we had managed to get the same interviewee. ![]()

1 Like

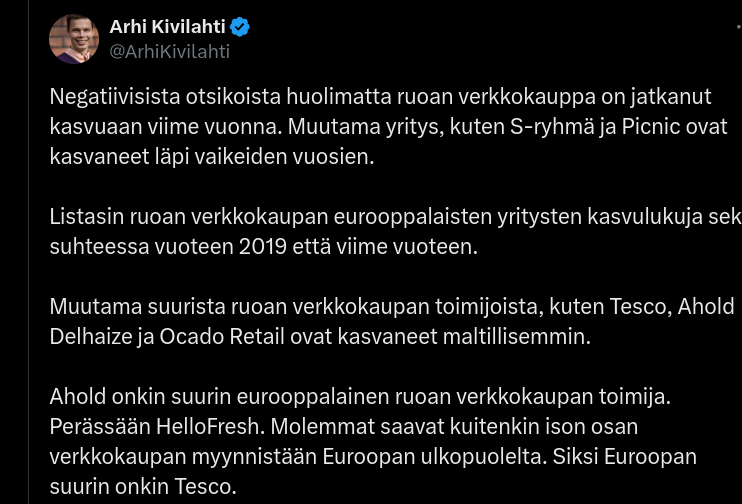

This will likely interest those following the industry and its stocks. ![]()

@Arhi_Kivilahti has been tweeting:

https://x.com/ArhiKivilahti/status/1836641355008803150

3 Likes

At least I don’t recall the Kaupan tila podcast hosted by Arhi Kivilahti being mentioned on this forum yet. (I could very well be wrong; it wouldn’t be the first time.)

I’ve been listening to it relatively actively, and the offering is very broad, including comprehensive episodes on the history of Kesko and the S Group, for example. Kivilahti has extensive networks due to his background, and the guests are of that caliber. One could say that this gives you the chance to listen to so-called industry insiders, and the relaxed format makes it possible without any particular filters. Kaupan tila can be found at least on Spotify, and presumably on other common audio services.

9 Likes

Yle reports (no paywall) on how growth in online grocery retail has stalled. Compared to the pandemic era, that is certainly the case, but the difficulties here are mainly affecting challengers smaller than Kesko and the S Group (“Ässä”). According to Yle, Foodora’s own grocery stores, Foodora Markets, are set to be closed in Finland in the coming days. In these markets, employees pick the products and deliver them to customers, meaning the online operation is not part of a physical storefront, which is presumably how it will be far into the future. As I understand it, both consumers and the largest grocery stores see the future of online retail as complementary to brick-and-mortar stores.

In Finland, Foodora intends to continue in the online grocery market by delivering food from partner stores. In practice, this will be the S Group, as Kesko is already collaborating with Wolt. According to Yle, Foodora is indeed running a home delivery service trial with S Group grocery stores in Oulu and Kuopio. At Kesko, online grocery growth has been driven by express deliveries. I don’t know about the S Group’s express deliveries, but if the collaboration with Foodora deepens and the offering expands, one can assume that competition will intensify, which is naturally mostly good for the consumer. Finally, it should be mentioned that Lidl has no online grocery presence in Finland at all.

6 Likes

Earlier this week, OP published a good overview of the development outlook for the store networks of retail companies in the Finnish market. To summarize, the network in the discount, variety, and consumer goods retail sectors will grow significantly in the coming years, competition will intensify, and corporate acquisitions are possible, if not even very likely.

Based on the group of companies included in OP’s calculations (Tokmanni, Puuilo, Rusta, Motonet, Halpa-Halli, Biltema, Normal…), the total number of stores in the Finnish market will grow by approximately 10% by 2026, provided that their current plans are fully realized and no store closures occur. Perhaps even new retail players may expand into Finland in the coming years and change the market. Normal is one example of this, though it is quite exceptional with its strong growth. In any case, 10% as a working figure certainly provides a realistic outlook on the growth of the store count.

Growing store capacity is likely to increase competition in the industry, which should be reflected in the companies’ comparable sales growth. OP considers it likely that competitors’ expansions have already been reflected in Tokmanni’s performance as sluggish growth in comparable customer numbers. Such an impact cannot be inferred from Puuilo’s performance, at least for now. This, of course, does not mean that Puuilo is immune to competition.

Intensifying competition and narrowing room for growth can lead to consolidation in the market. The profitability of companies in the sector is not particularly high, and volume is everything. Publicly listed retail companies are among the top performers, so one might assume they would take on the role of a consolidator rather than an acquisition target. On the other hand, OP’s report brings up old speculation about a possible merger between Tokmanni and Europris.

Even OP does not have access to comprehensive information on the future expansion plans of all the various operators, but to mention a few in this context: Rusta currently has a total of 6 new stores planned for the Finnish market, Jula aims to open about 5 new stores annually in Finland, and Biltema has 8 new stores on the table. Motonet is currently focused on conquering Sweden. And indeed, the store network in the grocery trade is currently being developed through new store openings, especially by Kesko.

5 Likes