https://www.kauppalehti.fi/lehdistotiedotteet/kl/ffc99618-2546-3493-a301-58943d4902b3

Briefing

Puuilo is organizing a webcast in Finnish today, 7 June 2021, at 11:00 AM.

The company and its plans will be presented by Puuilo’s CEO Juha Saarela and CFO Ville Ranta. After the presentation, participants will have the opportunity to ask questions to the company’s representatives.

The event can be followed as a webcast at:

https://puuilo.videosync.fi/itf

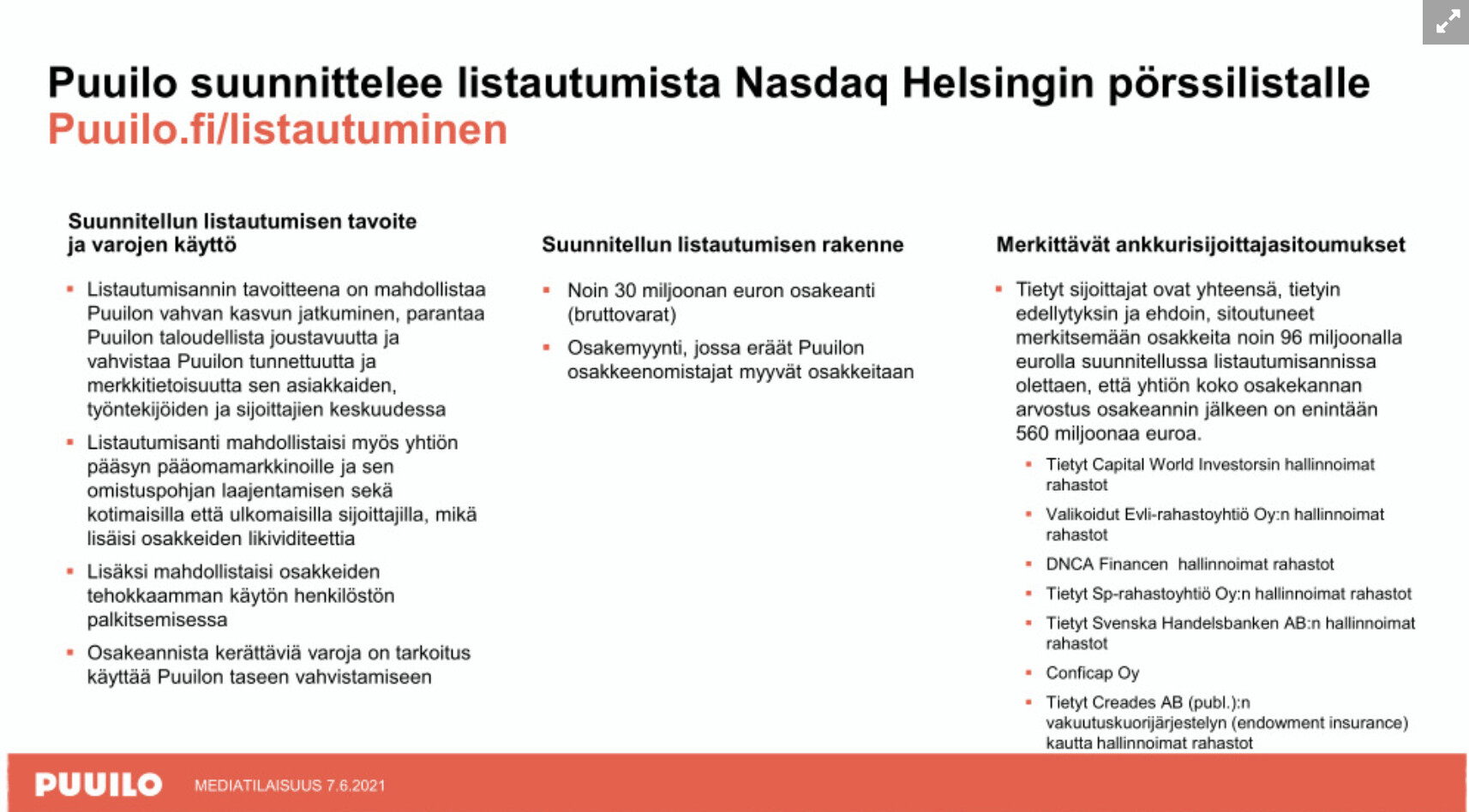

The goal of the initial public offering (IPO) is to enable Puuilo’s strong growth to continue, improve Puuilo’s financial flexibility, and strengthen Puuilo’s recognition and brand awareness among its customers, employees, and investors. These goals aim to improve Puuilo’s competitiveness and enable its access to capital markets, as well as broaden its shareholder base with both domestic and foreign investors, which is expected to increase the liquidity of the Company’s shares. The listing of shares and increased liquidity are also expected to give Puuilo a better opportunity to use its shares in remuneration.

The planned IPO is expected to consist of a share issue of approximately EUR 30 million (gross proceeds) by the Company, as well as a share sale in which certain Puuilo shareholders sell their shares. The proceeds from the share issue are intended to be used to strengthen the Company’s capital structure, including the repayment of Puuilo’s existing bank loans.

Certain funds managed by Capital World Investors, selected funds managed by Evli Fund Management Company Ltd, funds managed by DNCA Finance, certain funds managed by Sp-Fund Management Company Ltd, certain funds managed by Svenska Handelsbanken AB, Conficap Oy, and certain funds managed through Creades AB (publ.)'s endowment insurance arrangement (together “Cornerstone Investors”) have, under certain conditions, committed to subscribe for shares in the Company for a total of approximately EUR 96 million in the planned IPO, assuming that the valuation of the Company’s entire share capital after the IPO is a maximum of EUR 560 million.

The Company’s Board of Directors has set the following financial targets in connection with the IPO. Financial targets are forward-looking statements and are not guarantees of future financial performance. All financial targets presented in this announcement are targets only and not forecasts or estimates of Puuilo’s future financial performance, and should not be regarded as such.

Puuilo has set the following targets for the period 2021-2025 (financial years ending 31 January 2022 – 31 January 2026):

- Net sales to exceed EUR 400 million by the end of the financial year ending 31 January 2026, and to grow organically by more than 10 percent annually.

- Adjusted EBITA to be between 17–19 percent of net sales.

- The company aims to distribute a dividend of at least 80 percent of the profit for each financial year, depending on its capital structure, financial position, general economic and business environment, and future outlook.

- The ratio of the company’s net debt to adjusted EBITDA to be below 2.0x.

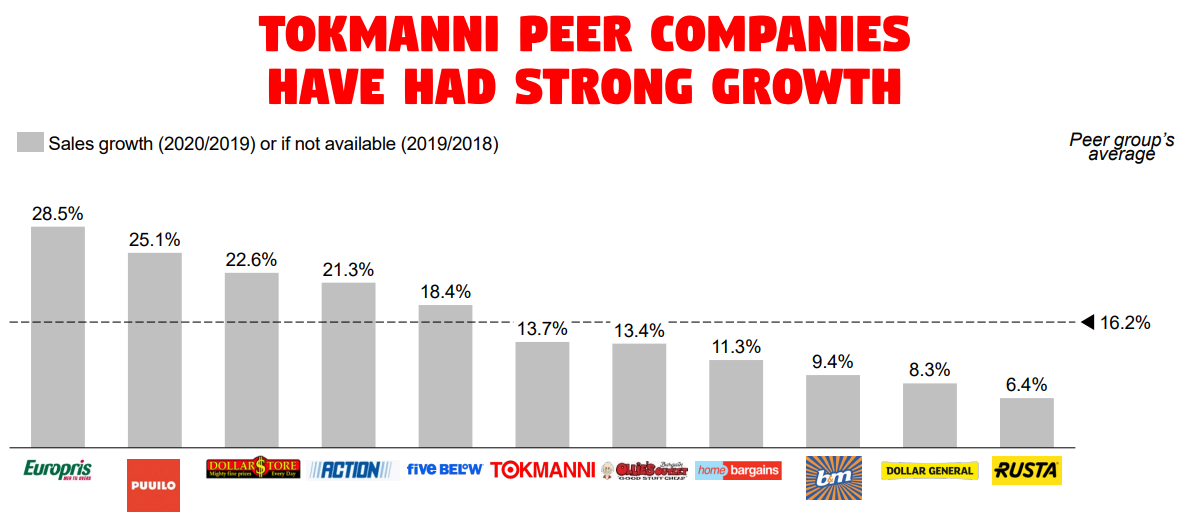

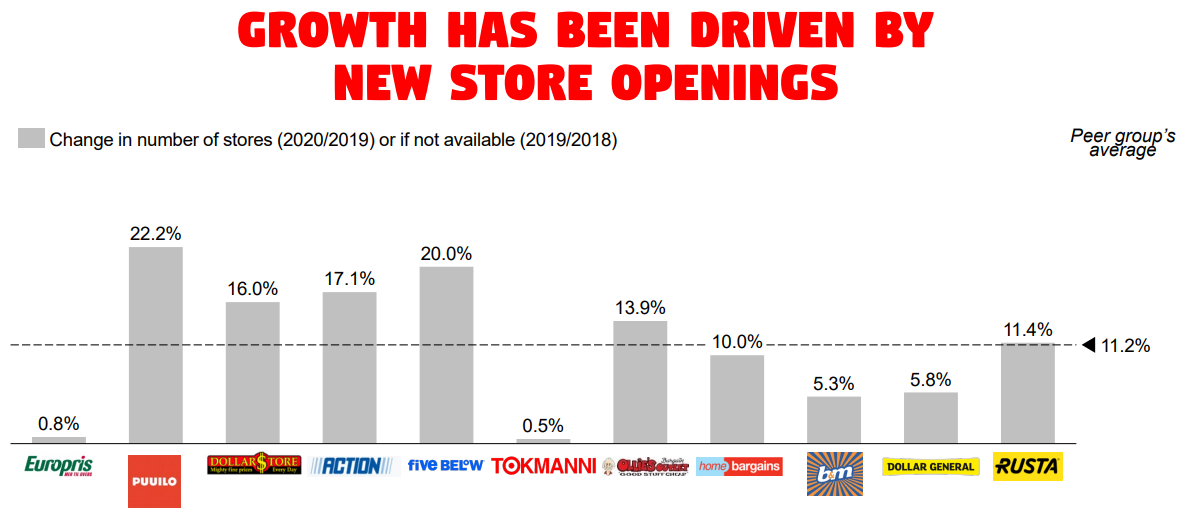

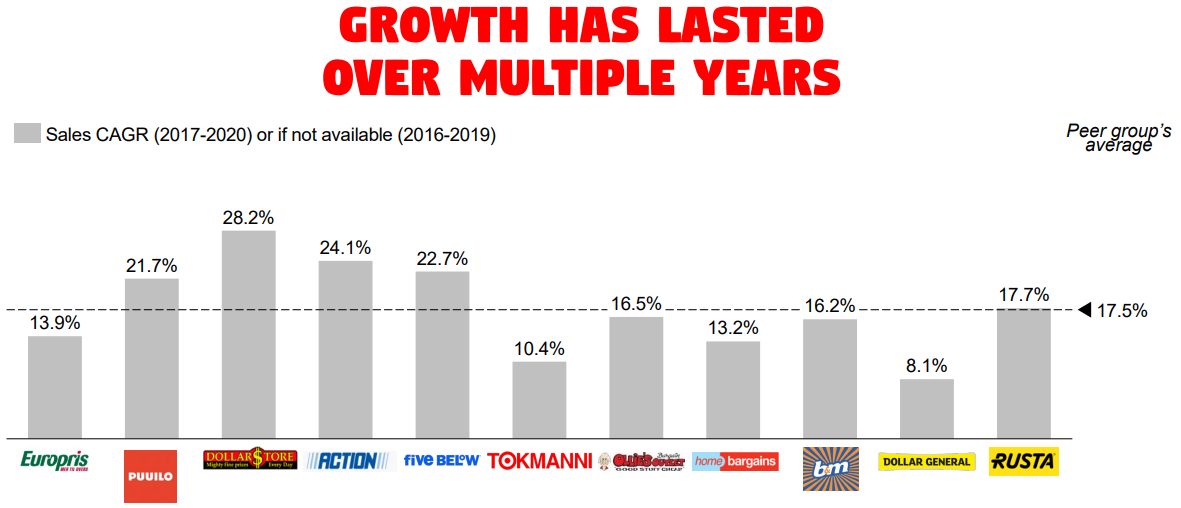

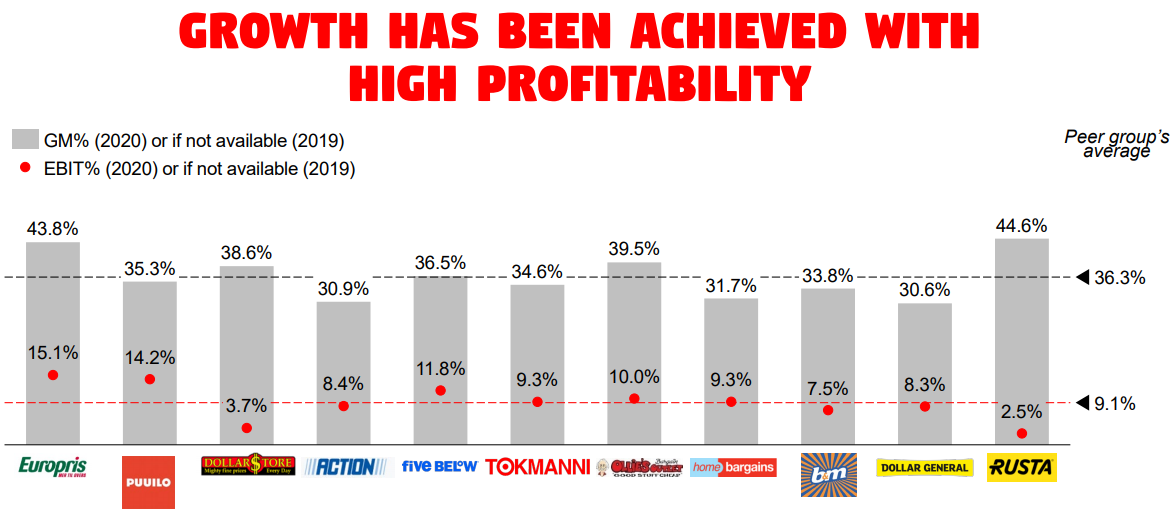

A few images of Puuilo’s (and competitors’) growth from Tokmanni’s presentation: