In this thread, we can discuss fossil and fissile fuels, metals and forestry, fishing and agriculture, as well as all other primary production and related topics.

I’m moving a few messages:

3 Likes

I don’t know if it would fit in this thread, but in my opinion, some good tweeting from Tankerdata’s Calvin:

Edit. I’ll put it here now as this tweet apparently sparked discussion about Oroco, which is familiar to many Inderes users:

9 Likes

Predicting the future is very difficult ![]() GS, on the other hand, predicts that after years of commodity suffering, a new supercycle would finally begin.

GS, on the other hand, predicts that after years of commodity suffering, a new supercycle would finally begin.

https://www.reuters.com/article/us-metals-supercycle-ahome-idUSKBN29A1QM

It would be quite unfortunate for commodity investors if, after the dry spell that began in 2013-2014, the current price peak would last only a year and the next 10 years would also be nothing but suffering. In fact, that would sound very strange to me, because adjusted for inflation, we are still very far from the peaks, and investments in commodities have been very moderate in recent years.

6 Likes

That last sentence you wrote was, in my opinion, the most important. Humanity must move away from fossil fuels in the future, but an investor’s job is to make money ![]()

The transition from oil use to renewables is a monumental project that will take decades. Just building the production chains needed for electric cars will take about ten years, so oil consumption will not end anytime soon, no matter how much we in the West want it to. At the moment, it’s hard not to be an oil bull, when all signs point to a significant price increase within a year.

7 Likes

I’m moving @Musta_leijona here

That response was for you, user @kelkka.

3 Likes

More on oil. A really strange situation is unfolding in America, where oil companies are going bankrupt even though oil prices are already at a quite tolerable level. Shale oil production declines really quickly if continuous maintenance investments are not made, and a one-year break in investments can mean that your company’s production drops by 50%. Many smaller players therefore cannot withstand even a one-year disruption in oil prices, and many oil companies in the United States are facing balance sheet clean-up, which means production cannot be increased immediately.

4 Likes

I’ve also been looking at Exxon with interest ever since a friend of mine mentioned a couple of months ago that he bought it last autumn for forty dollars. He mentioned many of the same reasons you’ve talked about: oil will be needed for surprisingly long, and if production isn’t invested in due to unfashionableness, it will support the price. From a shareholder’s perspective, it makes sense for Exxon to pump oil until, sometime in the distant future, the industry truly begins to wither.

I also agree that there are two completely different things: what I wish the world were like, and what it actually is. I consider climate change to be humanity’s greatest threat, and I wish it were fought more aggressively. But even if I don’t like Exxon’s business, if it’s clearly undervalued, I’m interested. (On the other hand, I do have my limits; I probably wouldn’t invest in a tobacco company at any price.) The reason I haven’t bought yet is my biggest weakness as an investor: it’s psychologically difficult for me to buy a company that has risen significantly in the recent past.

I’d still be interested to hear your summary of Exxon’s outlook for the next 20-30 years. Is the current dividend sustainable?

6 Likes

Regarding banks (e.g., GS) and oil, do you know why the bank sector’s stock price seems to be tied to the energy sector’s performance - is it that their money is tied up in these, or what kind of situation might be behind it (if not a coincidence)?

3 Likes

Making borrowing more difficult plays directly into the hands of rogue states. Iran, the Saudis, and Putin are laughing all the way to the bank.

Furthermore, preventing investments by shutting off funding is likely to increase price pressures. I wouldn’t rule out a new oil crisis, with these bandits bringing the whole world to its knees again. The explosive growth of US production has been instrumental in keeping the world economy afloat. Now Biden and other virtue-signaling useful idiots are blocking gas pipeline projects in their own country, while giving the green light to Putin’s rogue pipeline.

@Musta_leijona So the best way to rein in those rogue states is precisely by drying up the demand for oil and gas. The EU, as far as I know, is also striving for independence from Russian gas by supporting renewables. Getting rid of oil and gas could be surprisingly quick if enough funds are poured into scientific research. In populist-controlled states, however, science-based decision-making tends to be stifled, and scientific funding is constantly cut. This is going off-topic again, so no more on this.

4 Likes

One always has to balance with rogue states. Putin is unpredictable and understands that the people should be kept somewhat content, at least to some extent, to avoid the worst unrest. Politics can become unpredictable if an angry dog is cornered too much.

I can say that the raw materials sector does not interest me in the slightest. At a low enough price, these might even work, but from an investor’s perspective, there are far too many negative factors. Too many investments, too cyclical, susceptible to political maneuvering, no pricing power, etc.

4 Likes

Yeah, this wave of bankruptcies has come as a bit of a surprise to me. On the other hand, this is a bullish thing in the short term. Now assets are available at bargain prices for those who survive.

In addition, many have already announced that they will be selective with investments as the debt mountain brought by the coronavirus is dismantled. As demand is expected to continue its good growth, production cannot keep up at the same pace, which again puts pressure on prices.

3 Likes

Demand for Russian gas is being dried up nicely right now with the Nord Stream 2 pipeline :D. Europeans are good at virtue signaling because citizens swallow it without complaint. The truth is different, because corrupt Europeans, including Finns, accept money from rogue states (Esko Aho, Lipponen, and Germany’s former president are examples).

Finland’s electricity production is in such a poor state that it imports an insane amount from Russia in winters. And how does Russia produce that electricity ![]() ? But this doesn’t bother an environmentally conscious person from Helsinki.

? But this doesn’t bother an environmentally conscious person from Helsinki.

Some of this renewable hype is just politicians scoring easy points, trying to convince their citizens of their strong actions against climate change. However, the Green Deal funds and such mostly go elsewhere than to developing renewables.

Furthermore, Europe’s “greening” doesn’t help much when China and India are massively increasing their use of oil and other fossil fuels. Of course, they are so far away, so we can close our eyes to that reality.

I personally see the future of oil as very bullish in the medium-short term. Of course, there are risks, but I think they are exaggerated. Generally speaking, when a sector is really hated, it can present a good buying opportunity.

4 Likes

Seems like a coincidence.

Uh, well, I’m not even sure Finland will exist in 20-30 years, let alone some listed company ![]() Even forecasting ‘just’ 12 months ahead is incredibly difficult.

Even forecasting ‘just’ 12 months ahead is incredibly difficult.

The things you mentioned are also reasons to invest in the raw materials sector. Large investment needs make it difficult to enter the industry and increase the value of successful companies, as establishing new companies is challenging. Cycles and political maneuvering create irresistibly good opportunities when stocks are completely mispriced. A lack of pricing power means that your product will always sell, and competitors cannot threaten the position of a superior company.

Now that @Seinakadun_Keisari has sparked interest in mining stocks, and especially copper, on the Inderes forum after the OROCO thread, new threads about mining companies have started appearing weekly. The industry is incredibly difficult and risky, so there’s plenty to learn. Conveniently, MiningStockEducation just released a quality hour-long video on how to value mining exploration companies. As stated earlier, this sector is challenging and has significant risk, but of course, the reward is commensurate:

8 Likes

It should be noted here that I have a very high threshold for investing in any other mining company, although the uranium side is tickling me once again.

In mining companies, you take on company risk and raw material risk in the same package, but of course, in favorable circumstances, you also get the benefits with a multiplier.

4 Likes

If you’re interested in the sector, it’s worth remembering royalty companies as one option for participation.

Most people probably know their idea, but in short, they finance mining companies and in return get a fixed share of the company’s profits → diversified risk, but naturally lower potential returns.

Royalty companies have traditionally focused mainly on gold and silver, but there are some new and smaller firms whose main focus is elsewhere.

If you’re interested in learning more, for example, the following might be interesting. Roughly sorted by market capitalization (and from memory):

- Franco-Nevada; precious metals, oil, and gas

- Wheaton Precious Metals; gold and silver roughly 50/50

- Sandstorm; primarily gold

- Maverix Metals; primarily gold

- EMX Royalties; also battery metals and copper. Medium-sized, but only a few operational mines in its portfolio → value in future earnings expectations. Focus on the Nordics.

- Altius Minerals; main focus elsewhere than precious metals

- Vox Royalties; a small growth company

- Nova Royalties; focus on copper and nickel. Only projects in development and exploration phases → no cash flow.

(I own some of these, but not all; not a buy recommendation)

7 Likes

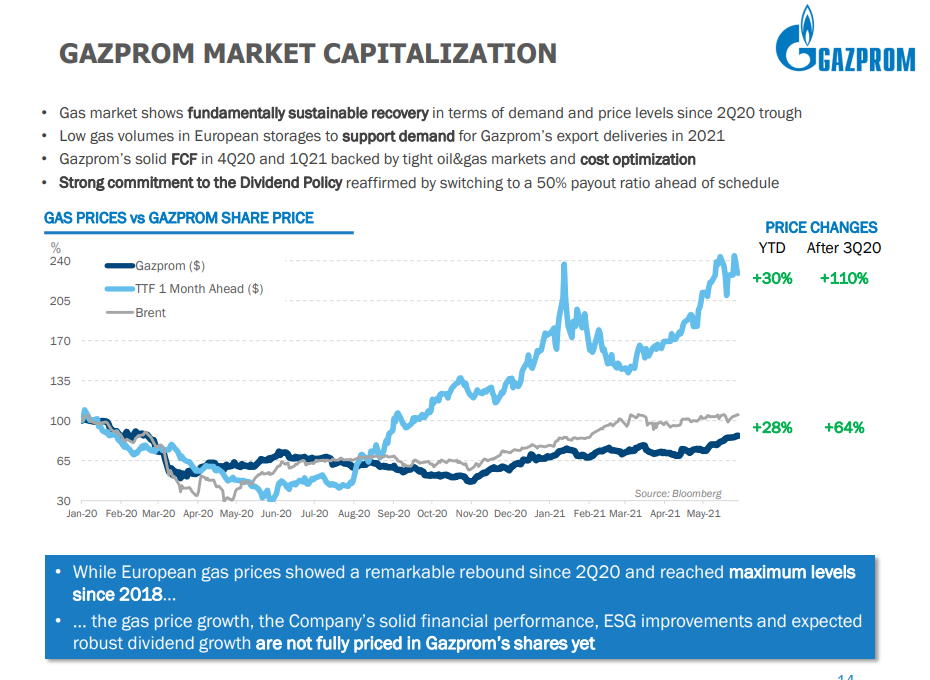

Are there any Gazprom investors on the forum? I have about a 1% slice of my portfolio in it, but I’ve been shamefully bad at following it. I’ve mostly just been collecting dividends for some years, and the stock price has been fluctuating. Now Q1/2021 results have been published, and the presentation has some quite interesting slides.

https://www.gazprom.com/f/posts/57/982072/gazprom-ifrs-3mnth2021-presentation.pdf

5 Likes

There was a good session at Cambridge House’s Copper Summit yesterday, especially Rick Rule’s talks on country risk, among other things.

2 Likes

Yes, of course, accurately predicting the future earnings prospects of companies is more or less difficult, but many entities do buy entire companies for very long-term ownership with no thoughts of “ever” selling, in which case they need to make scenarios over decades. I try to adopt this attitude to investing to some extent. After all, Exxon’s share is fundamentally a security that entitles one to one four-billionth of all the money the company will generate for its owners in the future. It’s like a bond with probably over a 50-year maturity, and you have to try to estimate the “interest” yourself.

In general, it seems like an interesting case: a shunned industry that many believe will die out in the coming years (it won’t die for a very long time), many institutions can’t even invest in Exxon, depressing share price development for a long time which further increases the shunning and thus pressures valuation multiples. And oh yes, it offers good inflation protection. But I need to delve deeper into the numbers.

2 Likes

I’m not, but if you’re interested in Russian raw material companies, their leaders, and their decision-making, I highly recommend this read. It talks a lot about Gazprom, among others.

5 Likes