A few takeaways from this morning’s video.

In recent days, with GameStop, Nokia, and WSB sucking up all investor attention from many directions, many have commented that the market is crazy or in a bubble. Naturally, such sharp and rapid overshoots are characteristic of bubbles.

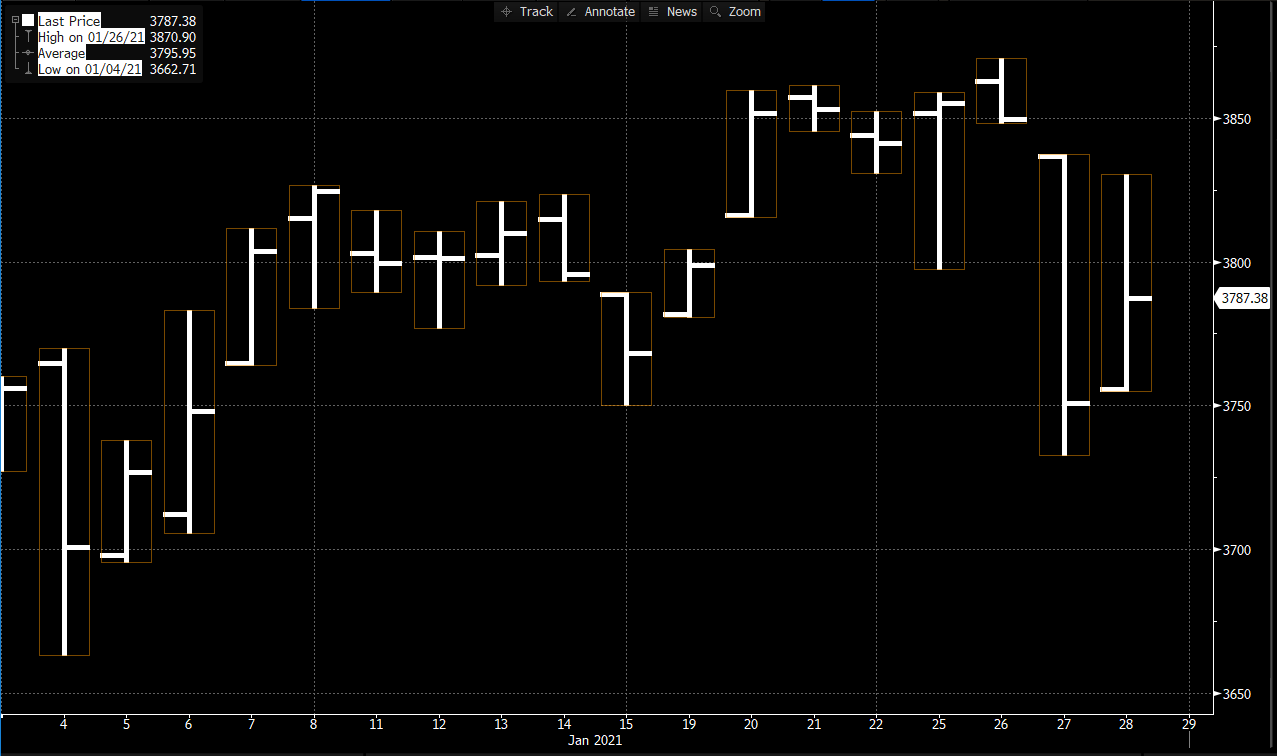

However, I would venture to point out that most of the market is just plodding along normally. Look at the S&P 500, for example. It hasn’t really moved anywhere in January:

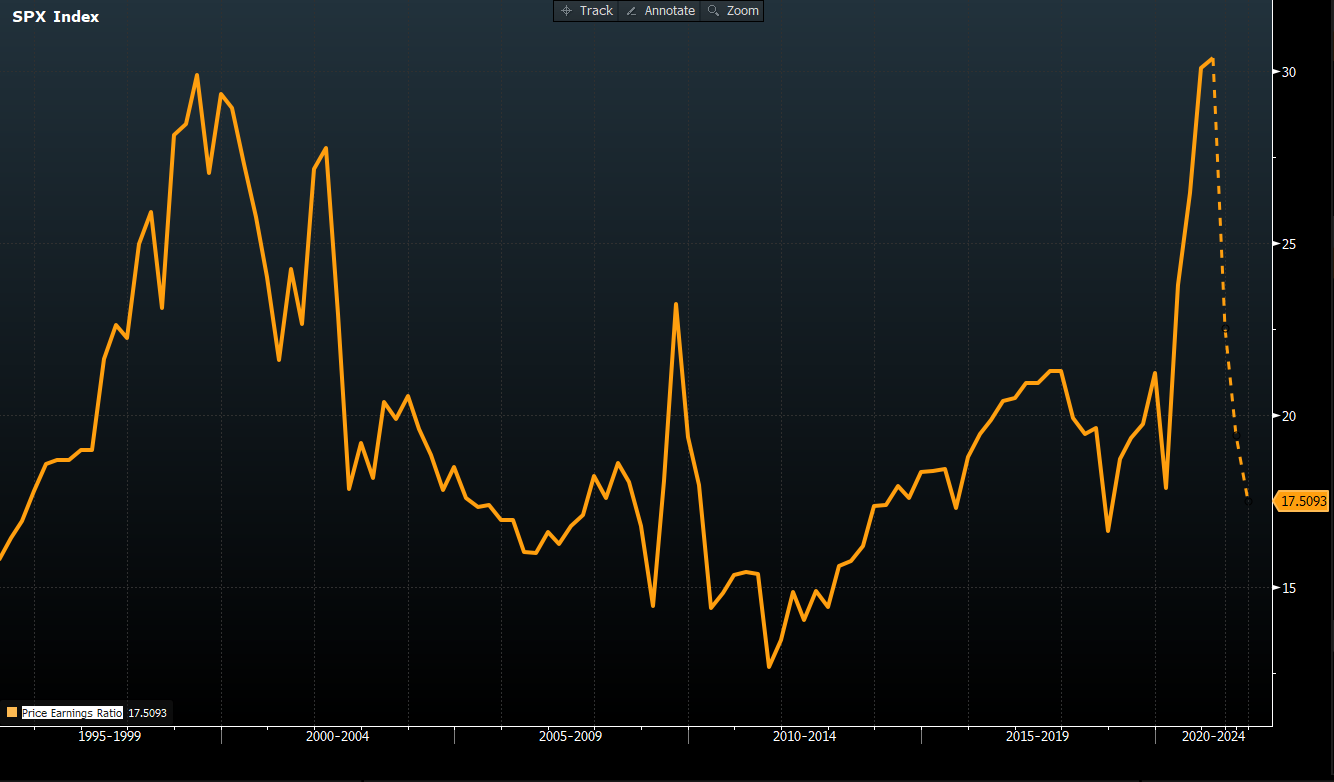

Okay, the stock market is expensive now. In fact, talk of a bubble gains traction from this, as the P/E ratio is at the same level as during the dot-com bubble. However, earnings are expected to recover after the coronavirus, and then the P/E would normalize quite a bit, as seen from the dashed line in the chart.

The stock market is by no means cheap, but it’s not hopelessly expensive either, generally speaking, if one can look a little further ahead (something that certainly seems difficult for many :D).

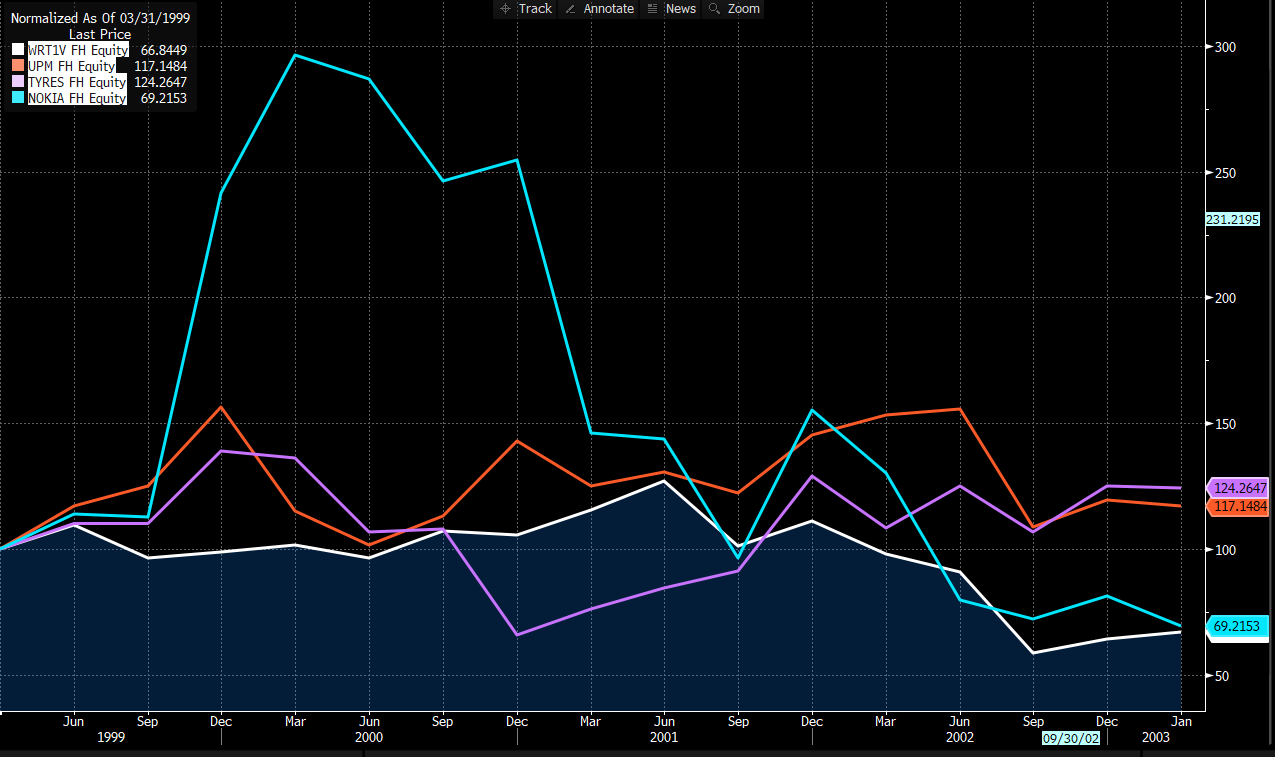

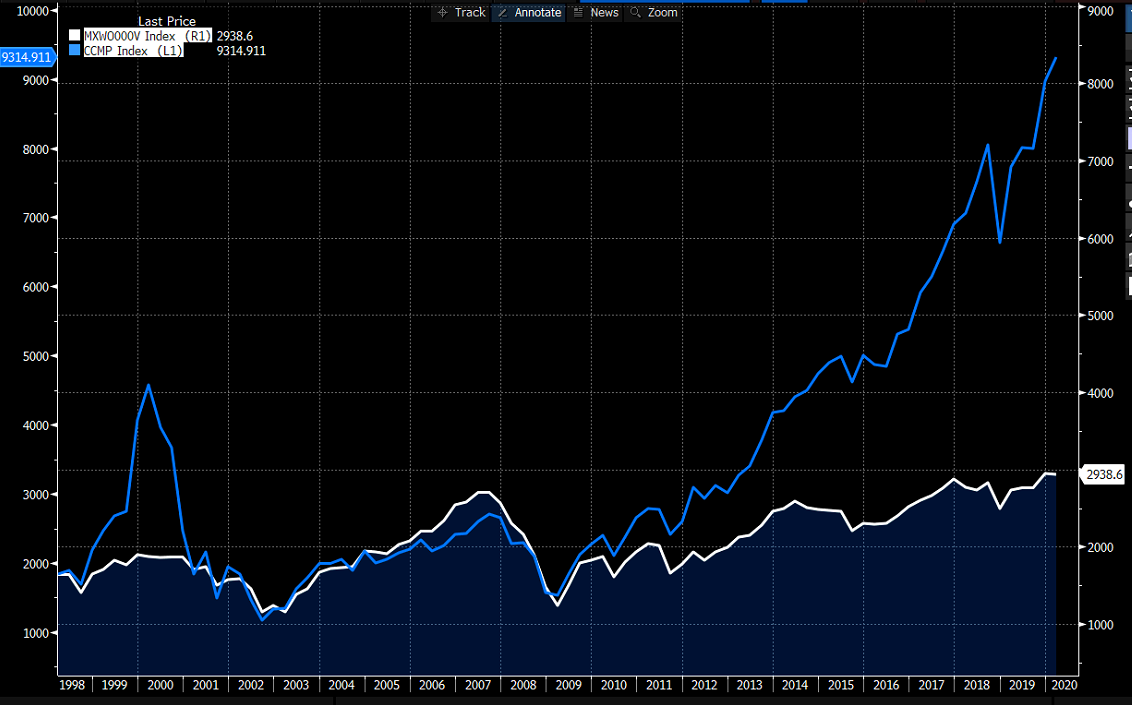

The stock market is also not homogeneous. Here’s a bit of a recap from yesterday on how some value stocks developed during the dot-com bubble. This is just an example, but the 90s dot-com bubble was a pretty total full-body bubble, yet even then one could make good stock picks during the bubble.

For example, Berkshire Hathaway practically countered Nasdaq. It halved as Nasdaq rose, but also bottomed out at exactly the same time Nasdaq began its three-year, -80% bear market.

In the Helsinki stock exchange, experienced investors always talk about how they loaded up on cheap KONE, Sampo, etc. when the IT sector was boiling. Unfortunately, I couldn’t get a KONE graph from Bloomberg for that period, but here’s Nokia vs. UPM, Wärtsilä, and Nokian Renkaat. Indeed, money rested quite well in UPM, for example. Sampo, Nokian Renkaat, etc. multiplied tenfold in the bull cycle that followed the dot-com bubble. KONE has been one of the best stocks of the 2000s, so there are always opportunities, even in a boiling market.

Here’s one more observation. From 1995 to 2000, the S&P 500 rose +300%, or about +25% per year. Now, from 2016 to 2021, the stock market has risen about +100%, or 14% per year. This also speaks volumes about the fact that even at the index level, we haven’t risen at a classic bubble-like pace.

So, it’s always a stock picker’s market, even if times aren’t the best right now. Read analysis and make good stock picks.