@Olli_Vilppo commented; in short, it went well, but let’s move on.

Puuilo’s Q2’25 performance was again very strong in terms of both revenue and profit and in line with consensus expectations, but fell slightly short of our own expectations, which had already soared to the upper end of the guidance.

If the new ambitious targets for 2030 are met, there is still upside potential in the stock. However, the Swedish market will by no means be an easy nut to crack, even though, in our understanding, the company has already learned something about the market through its long-standing online store there. In Finland, on the other hand, the concept has dominated market share, and in that regard, the targets are easier to believe. So far, Puuilo has always met its targets in Finland, which adds weight to management’s statements.

However, they are going to Sweden moderately and realistically, following Puuilo’s model – this is how I interpret the announced opening of 10 stores by 2030. Saarela’s writing contained no chest-thumping or vague promises, but clear figures regarding stores, revenue, EBITA, and indebtedness.

Saarela has always kept his word, even though many things have happened around him, so I don’t doubt now either that the goals will be achieved.

My initial feeling about Puuilo’s new strategy is goodbye to the sector’s best profitability. I was already pondering this in March, and brutally, in light of the numbers compared to Tokmanni, the profitability difference comes from other operating expenses and last year also from personnel costs relative to revenue. When breaking that down further, Puuilo’s profitability was formed by higher revenue per store and lower real estate and store location costs relative to revenue.

One doesn’t need to be a great clairvoyant to see challenges in the future in achieving similar revenues per store when stores start opening in increasingly less attractive locations. If revenue per store drops, then a natural consequence is an increase in personnel costs and store location costs relative to revenue (because in these calculations, the dividend grows faster than the divisor).

Hopefully, Puuilo proves me wrong. In Sweden, the path is open for the company to expand its store network in good locations, if they can only gain a foothold there. There, the challenges are less fundamental, but not necessarily any easier to overcome.

Where did you dig up those figures? As far as I know, Biltema and Jula are private limited companies, so they don’t report figures for everyone to see in the same way as public ones.

Could an Inderes analyst get more information from Puuilo’s management on how expertise in Swedish culture is acquired or if it has already been acquired? That is, how will Puuilo be made to operate in Swedish culture if stores are opened in Sweden.

Somehow, I’ve been left with the impression that quite often a lack of cultural understanding leads to failure and losses when expanding into Sweden, when it’s assumed that the Finnish way of operating is valid abroad, which is apparently a big mistake as an assumption.

This is truly an amazing company, and it has been a pleasure to follow this story from an owner’s perspective since the IPO. There has been patience for sensible growth, and it still seems to be the case!

Having read the comments above, and especially @Sambadi makes a relevant reflection on how the current good profitability level follows store openings in the short term (Finland) and long term (Sweden). I have also pondered this perspective myself while owning Puuilo: what stage in Puuilo’s growth story is it when/if profitability starts to suffer? It is certainly clear that it is easier to extract profitability through, for example, 50 stores compared to Tokmann’s ~200 stores (Finland), when considering the entire cost structure (okay, purchase volumes support profitability, but in any case)? If this is not the case, then these comments and justifications are interesting and help to understand this story even more deeply from a so-called shareholder’s perspective → also ping analyst @Olli_Vilppo

But today, let’s enjoy – all Puuilo owners and also those just following this great story – a proper possumunkki and coffee or just coffee/tea in a diet mood

Specifically in the neighboring country. The profitability of Swedes has suffered when they have gone to the Finnish side, and the same the other way around.

Hi! I hadn’t noticed this message yet when I was speaking with management. But this is a good question for the next interview. Operations in Sweden haven’t been fully launched yet; instead, investors were informed of the strategic guidelines to improve visibility regarding what has been decided for 2026-30.

I used the midpoint of the guidance for full-year 2025 revenue and EBITA. Sales should proceed at the same pace in the latter half of the year as in the first half, but the EBITA guidance seems quite low.

Why would EBITA% decrease in the latter half of the year, when it has continuously improved and, according to the CEO’s review, it should continue to improve as the share of private label products grows?

Probably not much new for current investors, but let’s go through the concept and the company a bit for future investors, for example.

In the article, Saarela tours the store and also highlights some niche departments, such as ropes sold by the meter, equestrian supplies, and welding masks:

\u003e In the small ironware section, Saarela gets excited: now a good shelf space has been found. The reason is the ropes, which can be bought by the meter from Puuilo. Especially in summer, boaters need rope material, and Puuilo offers them in the desired length instead of pre-packaged bundles.

\u003e

\u003e “We sell ropes by the meter, which not many do. Such a selection of ropes and cords cannot be found in many places,” Saarela advertises.

\u003e “The impact of Temu and similar online stores on us is, according to our current estimate, small.”

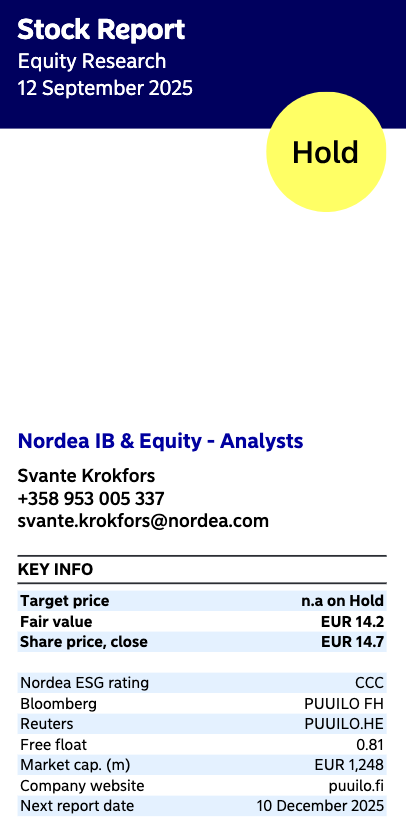

OP raises target price to 14.50 euros and keeps recommendation unchanged - reduce.

We maintain our REDUCE recommendation for Puuilo and raise the target price to 14.50 euros (previously 13.50). No significant changes occur in our earnings forecasts for 2025 and 2026, but we have raised our longer-term forecasts based on updated financial targets (especially the increased targets for Finland).

I am equally concerned about the possibility of a ‘wasted investment’ as I am about a success story. The reasoning is the certain similarity of products and concepts in discount stores. How to stand out from the crowd? This, in my opinion, is the alpha and omega here. The Swedish consumer has undoubtedly chosen their routes over the years. Does a somewhat ‘rustic’ ‘finn-devil’ store bring ANYTHING new? Can Puuilo go with the same branding, or is a new beginning needed? Where does the money come from, and what’s the return on it? Starting from scratch is not cheap. In the north, it might even work as an original concept with Finland’s good and honest reputation, but I would think carefully about going to southern Sweden.

I worked for 3 months in Sweden and asked customers about the price level and consumer purchasing power in Sweden. They said that purchasing power has weakened significantly and everything is expensive. – I noticed this myself too. Apparently, salaries haven’t kept pace. I don’t know if that’s true.

If Puuilo could maintain Finland’s affordable prices in Sweden, which people aren’t necessarily used to nowadays, that could be the biggest key factor for a breakthrough(?)

P.S. I was managing a fairly large construction site near Örnsköldsvik, and construction materials were needed there almost daily. Actually, the only option was Jula. A bit shabby and a very small supplies section for tools and construction chemicals. In my opinion, Jula was at least 30% more expensive than similar purchases in Finland. I really missed a proper store. Finally, I did find Ahlsell, but you can’t get anything there without a company account. My colleagues also described it as difficult to get supplies for construction sites in Sweden.

Here’s an article about Motonet’s trip to Sweden. In my opinion, opening 1-3 stores as a trial, as told by Saarela, is a good strategy; let’s see how it goes, and if necessary, adjustments can be made. With Puuilo’s concept, not so much money is burned that the trial wouldn’t be worth it, in my opinion.

They state that the concept is 90% the same as in Finland, so they are proceeding with fine-tuning.

After a year of operation, they opened/are opening 5 stores in 2025 and have gained over 50,000 loyal customers.