Known in the forestry sector as a quality company and a good partner in timber trade. A good reputation and local brand resonate well with the public.

But going public with growth targets and dividend payments at the forefront? I’m not so sure…

As a rule of thumb, the profitability for sawyers with A-grade logs is 5%. B-grade logs break even (+/-0%), and C-grade logs lose 5%. Yet, sawmills pay the same price for all log grades, even though it’s only profitable to saw large-diameter logs. Due to MTK’s (The Central Union of Agricultural Producers and Forest Owners) advocacy and competition, landowners are paid log prices even for small wood that isn’t profitable to saw. You can’t survive the competition in wood procurement if you only start buying logs with a top diameter of 20cm or more. There’s always some debt-driven firm or entrepreneur in the market who will buy wood even at a loss.

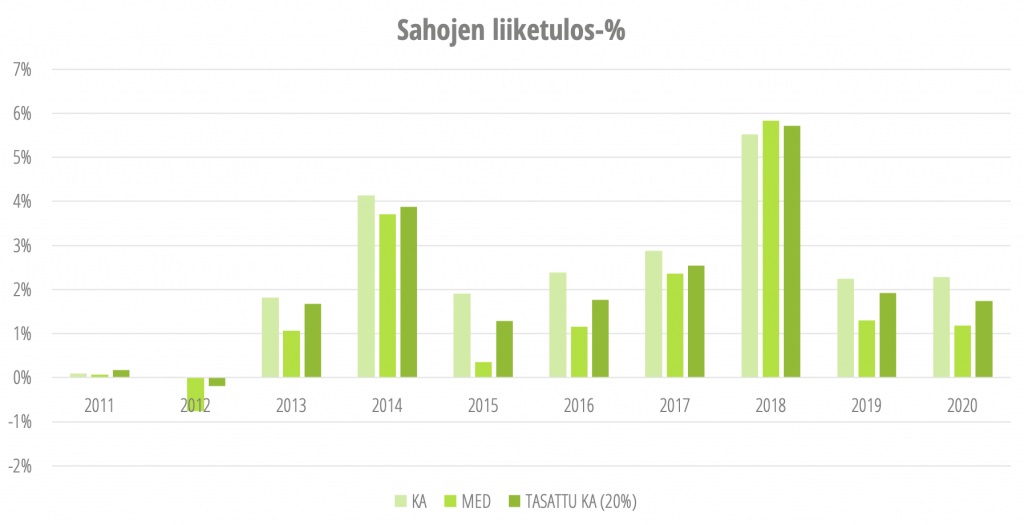

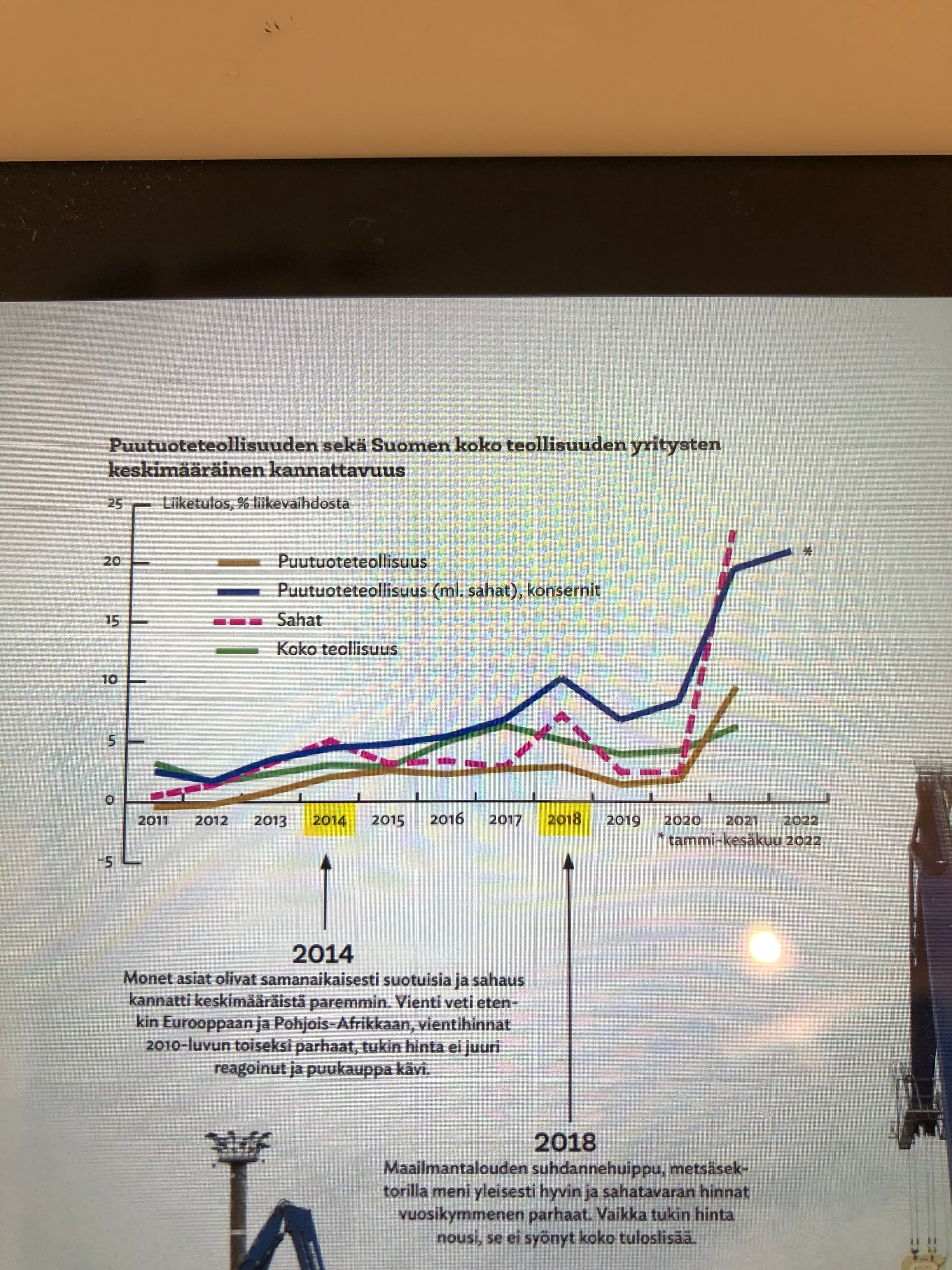

During a downturn, sawmills just barely break even or post a loss. As noted in the article linked earlier in the thread, the sawmill industry traditionally follows seven-year cycles. Seven lean years followed by seven fat months…

So, maybe one profitable year and six years of zero profit, with one year perhaps being loss-making. In the old days, sawmills used to burn down at regular intervals, which improved the profitability of the remaining mills in the area. That was then, but not much has actually changed. One thing that has changed is that the probability of a sawmill burning down is no longer 100%. Nowadays, side streams like shavings and chips are used for energy, which provides profitability for the sawmill. Every stage from wood procurement through sawing to export delivery requires a significant amount of labor. Automation has improved efficiency, but labor is still heavily required at many stages. Then, the profits made during a peak cycle are poured into new investments when the sawmill line and such are updated.

The margin between the price paid to landowners, procurement costs, and the final sawing result is slim. Figuratively speaking, there is very little room between the wood and the bark. You can operate on a small scale within that space.

The business is entirely export-driven, and the cards are not in one’s own hands. The worst-case scenario is when the price of wood in the procurement area in Finland rises while global exports falter.

Furthermore, the general public and those outside the forestry sector don’t fully realize that Finland is running out of large-diameter trees suitable for sawing. Many get an unrealistic perception of logging potential because members of the Center Party (Kepu) and MTK lobby so hard for the forest industry. Finland does not have “more forest than ever before.” It is not possible to increase logging volumes. In some places, they are practically scouring the woods for log timber. Forests have become younger, and trees are no longer left to grow large enough to become proper logs. Conservation obligations are an additional factor, but I don’t consider them significant or a real threat to the forest industry.