This thread is a continuation of the comment: Kurssien ja niiden muutosten kyselyt, kauhistelut ja hehkuttelut - ketju (Osa 1) - 10431 - Sijoittaminen - Inderes forum.

Previous thread:

This thread is a continuation of the comment: Kurssien ja niiden muutosten kyselyt, kauhistelut ja hehkuttelut - ketju (Osa 1) - 10431 - Sijoittaminen - Inderes forum.

Previous thread:

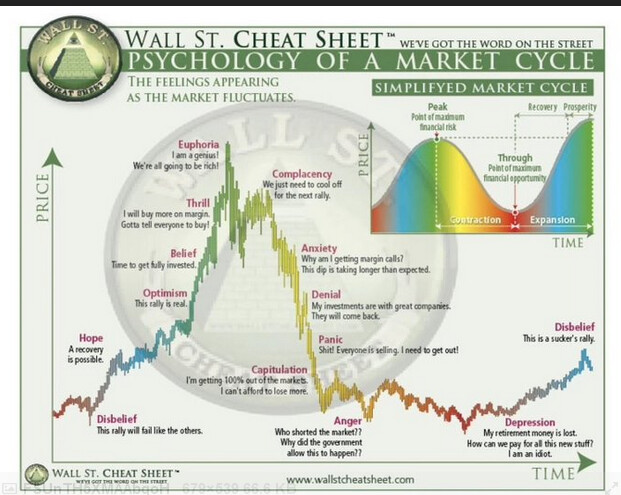

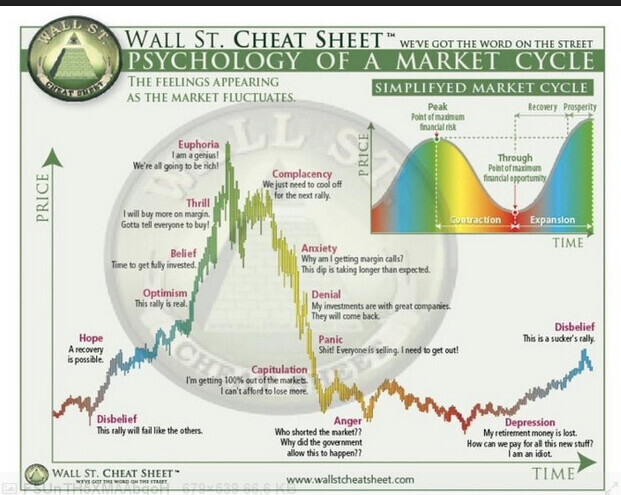

It’s not panic yet, we are at the “Denial” stage. ![]() When we see -10% daily drops, then we’ll be in a panic and it will be buying season.

When we see -10% daily drops, then we’ll be in a panic and it will be buying season.

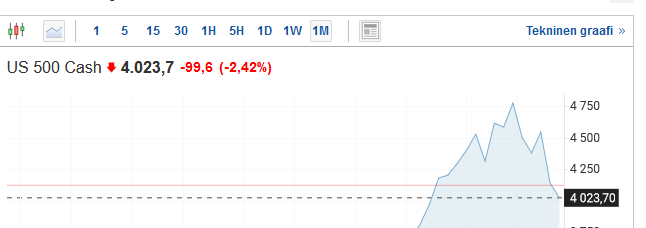

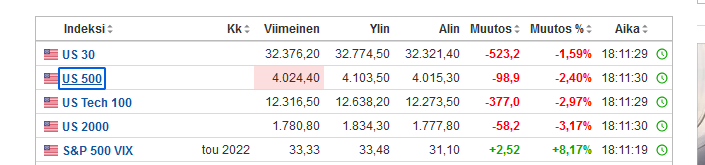

The S&P 500 isn’t even in a bear market yet.

Though, it’s not a long way off.

Looking at the Sepä curve from its peak and comparing it to the WS psychology image and the current volume, I would say that panic is at least starting, if not already in full swing.

Daily changes in my foreign portfolio holdings today…

Edit: situation added at the end of the day at 23:02

That picture with its texts is somewhat simplistic in the sense that usually the true euphoria climax of a bubble is experienced months before the index reaches its final peak. For example, the climax of what is perhaps the biggest stock market bubble in US history, in my opinion, was in February 2021, when measured by the number and quality of SPACs, Goldman’s Non-profitable Tech Index, ARK Invest, hydrogen and electric cars, crypto, general optimism, and the amount of irrational behavior. After that, these elements started to cool down. At the index level, it went up until the end of the year due to a strong rally in blue chips, but at the same time, speculative assets had already fallen chillingly by tens of percentages. Bubbles always seem to have a final phase where blue chips wipe the floor with small growth companies, and the index goes up even though the sentiment is secretly already souring. In 1929, this phase lasted 8 months, in 1973-1974 just under a year, in 2000 about half a year, and in 2021 about 10 months.

So now it’s starting to become clear that the termites of doubt reached the great and mighty Sepe (S&P 500) slightly before the turn of the year. (At that time, it was impossible to see, no one can identify in real-time when the peak is reached.) This year, Sepe is -16%, which is actually a historically really muddy spring season. It is still expensive, with a P/E of 20 on earnings forged with incredibly large margins. It does not attract classic value investors due to its expensiveness, nor momentum investors due to its downtrend. Violent rebounds indicate distress. The extremely expensive housing market adds systemic risk.

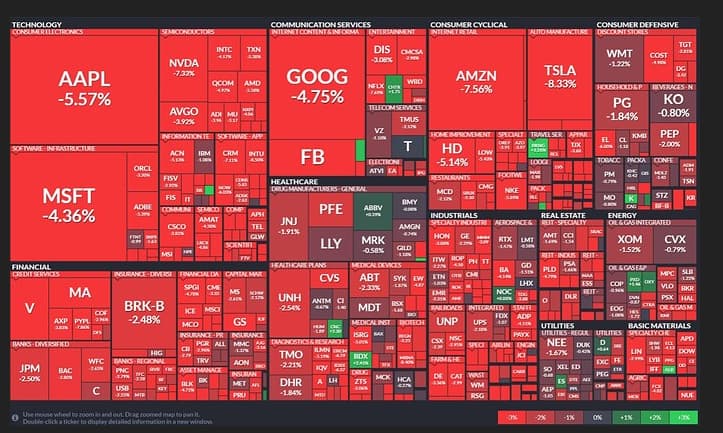

Well, growth stocks have pulled several days over -10%. Several are down -30% in 3 days. Oatly, for example, is down -90% from its peaks and -86% from its IPO.

My daily watch looks like this, and I’ve already bought some

I personally like to follow private investors’ sentiment on Jodel (Jodel). Based on what I’ve seen, we are definitely no longer in the complacency phase. On Jodel, no one is bullish anymore; everyone is neutral or despairing about the future. Many are genuinely panicking, asking in distress why their stocks are plummeting. This forum gives a rather rosy picture of how investors are enduring the bear market. I would say we are already in the denial phase. It’s worth remembering that not every bear market ends with every other investor’s portfolio being liquidated, just as not every bull market ends in euphoria.

Could we get a little profit for this Victory Day? The portfolio looks like it’s been hit by Ukrainian artillery fire… ![]()

Is this capitulation now that absolutely everything is going overboard in the market?

Well, luckily my own horizon is still decades away and there’s no leverage, so I can calmly plod through this shitstorm too.

Oh boy, looking at DoorDash’s drop, I can almost feel the level of frustration the Wolt guys are experiencing. Doesn’t Wolt’s final sale price depend on Dash’s H1/2022 share price? ![]()

You can even with leverage. Or at least that’s what I want to believe. However, a moderate 20-30% leverage requires a roughly 50-60% drop for a margin call to activate. You can always buy more shares with your salary, and the capital/loan ratio improves, and you don’t even have to liquidate the entire portfolio in a margin call situation.

Of course, I only leverage large indexes; I’m too much of a scaredy-cat for direct stock investments with a large weighting. The worst weather vane of the century looks back at me from the mirror =D

Then again, Wolt’s owners probably understood that they sold their shit at an absolutely exorbitant price. 7 billion dollars for a company that made 150 million in revenue and absolutely massive losses. Furthermore, I don’t believe that these Wolts and DoorDashes will ever make much money, because anyone can buy a car and deliver food. These companies have minimal moats.

A student loan is the best kind of loan, because a margin call will never ring me up ![]()

You speak the truth. I mean, I follow FANGMAN (Facebook, Apple, Netflix, Google, Microsoft, Amazon, Nvidia) companies more, and their movements are already at -3%. Nvidia is even more. When these companies also experience -10% drops, then we’ll be in panic territory, in my books ![]()

I won’t take a separate stance on Wolt here, but it has become clear over the last year how toxic the current market is for companies that have not proven their ability to generate cash flow for shareholders. A drop in stock price is one thing when a company’s cash flows are still far in the future, but it’s an entirely different case when the pricing implies they will never materialize.

The worst cases are those where companies simultaneously try to achieve growth with IPO funds, dilute existing shareholders with absurd stock-based compensation, and still don’t turn a profit. At the same time, investor sentiment is a complete dumpster fire, with investors doubting the veracity of these growth stories, which will raise the cost of financing in the future. And when the business doesn’t generate the necessary money, a vicious cycle is complete. Even if the business develops well, financing costs and dilution will affect the investor’s final outcome for a very long time.

Me: “Sometimes I’ve even invested in quality so that not all investments’ stock charts are complete bum-booms.”

Quality: “Today was just one of those days. Good work on my end.”

In response to the question referencing this image:

I’d say we’re in the denial phase. I haven’t yet considered whether I should sell something to avoid worse outcomes. Nor has there been a major selling wave on this investment forum. The financial media or evening news hasn’t yet warned that owning stocks is now truly risky.

However, I’ve at least gotten past the anxiety phase in my own head. A small dip used to bother me, but now I’m more in a “who cares” mood.

What bothers me most is that I was quite well prepared for a bear market with a 50% cash allocation, but now all of that has already been reinvested. So, for my part, the capitulation phase could already be underway. Unfortunately, I don’t think it is…

This depends a lot on what’s in the portfolio. I myself would now be most concerned about these “value stocks” that many people bought after selling off growth companies. There’s nothing wrong with that, it was a good move back then. But there are companies out there making good profits and strong growth at quite low valuations. It could be that the value investor is actually in euphoria when growth tech is, at least in some places, close to the end of panic ![]()

Hopefully, no one actually takes that sentiment graph as factual. Of course, it’s a fun pastime, so no harm in that. In that spirit, I’d say I’m in the Denial phase and don’t really ever go below that, except for individual stocks – meaning for some stocks, I’ve admitted I no longer understand their story and have exited.