…

10 Likes

https://twitter.com/getbenchmarkco/status/1355221782677094402?s=21

Seems like a good bit of the worst steam has been let out… this will be fine

39 Likes

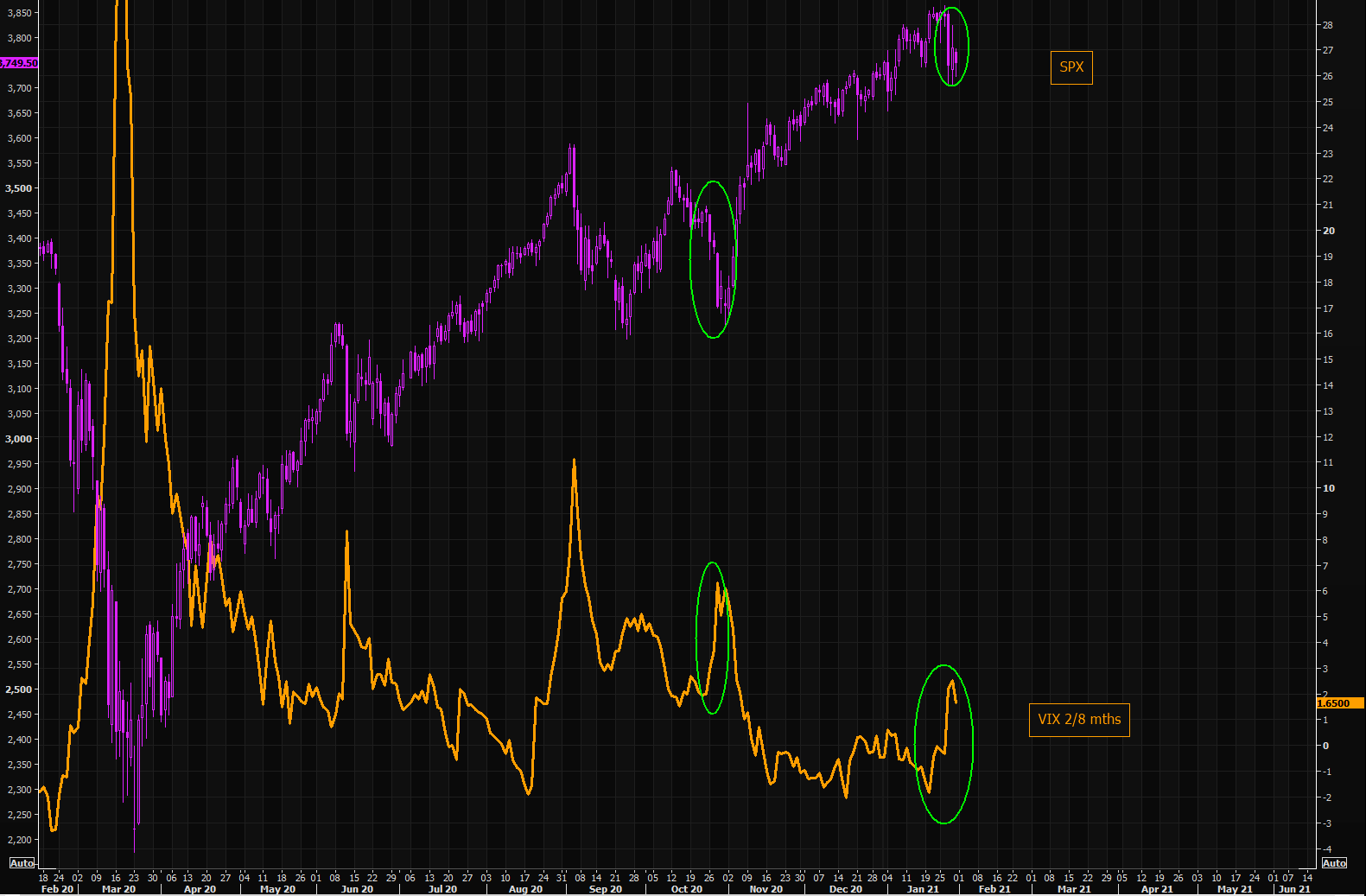

The Volatility Index VIX is interesting to follow again. (Ihre Datenschutzeinstellungen).

It has been fluctuating quite strongly this past week.

On Wednesday, January 27, the VIX index saw a strong 62% increase. The previous strong increase was in October, before the presidential elections.

On January 28, the VIX fell below 30, from which it rose again today. Towards the end of the last day of the month, it rose above 37. Now it is falling again more…

https://twitter.com/jsblokland/status/1355030418643431424

A picture from The Market Ear website shows the VIX increase in October, when the S&P 500 also began a larger decline.

4 Likes

Most of us here are probably “non-professional”. ![]() We just try to keep this thread as substantial as possible because it easily gets sidetracked.

We just try to keep this thread as substantial as possible because it easily gets sidetracked.

You can chat freely in the Coffee Room.

26 Likes

Tesla’s and Nokia’s valuations are on completely different planets. Nokia’s stock price hovers at a relatively reasonable level, but paying Tesla’s stock price is closer to leaving a legacy for the sixth generation to potentially get a ticket to the moon.

In the long run, stocks are bought for no other reason than to make money. Tesla has been bought as if it were an admission ticket to some gang that doesn’t exist. It’s a bit like a pin on your chest showing you’re part of it. I’ve met people like this. This kind of valuation is certainly present in other hype stocks and many brands.

The trend is downwards, but it can be very volatile. Eventually, we’ll get to those unpleasant key figures, EPS, and dividend yield, and when people finally start looking at their own portfolios, each person’s own guidance counselor is the most significant factor of all, not so much analysis and vision.

7 Likes

That’s a pretty good comparison; I myself think of Tesla as a religious movement. By this, I mean that no economic performance metrics support the stock price. The prophet or god Musk steps before his followers and presents his “divine” visions of future miracles, and the followers, in ecstasy, rush to buy stocks based on these visions. It doesn’t matter that most of the prophecies related to products and production have not happened or have at least been postponed indefinitely.

5 Likes

So, if the only reason for the sales is that someone is covering their losses, then this is actually a really good dip to buy. If only they would say when they plan to stop selling off their longs… there’s no guarantee that everything’s over yet.

4 Likes

Norway is starting to ease coronavirus restrictions. Hopefully, this will boost Norwegian stocks.

Norway to ease COVID-19 restrictions next week

Norway is set to ease strict coronavirus restrictions in the capital Oslo and its surrounding areas starting on Wednesday, announced the country’s Minister of Health, Bent Höie.

Very strict COVID-19 restrictions were introduced in the Oslo region due to new, more contagious virus variants. For instance, all non-essential shops were closed.

“The number of infections in Norway is constantly decreasing, and we now have a better understanding of the epidemic and its spread,” the minister explained.

On Wednesday, among other things, all shops not located in shopping centers can reopen. The same applies to restaurants, although they will not be allowed to serve alcohol.

Schools in the area will also gradually return to in-person teaching.

STT

12 Likes

Will Vaccine Optimism Boost the Markets? OP Macro Overview 29.1.2021

10 Likes

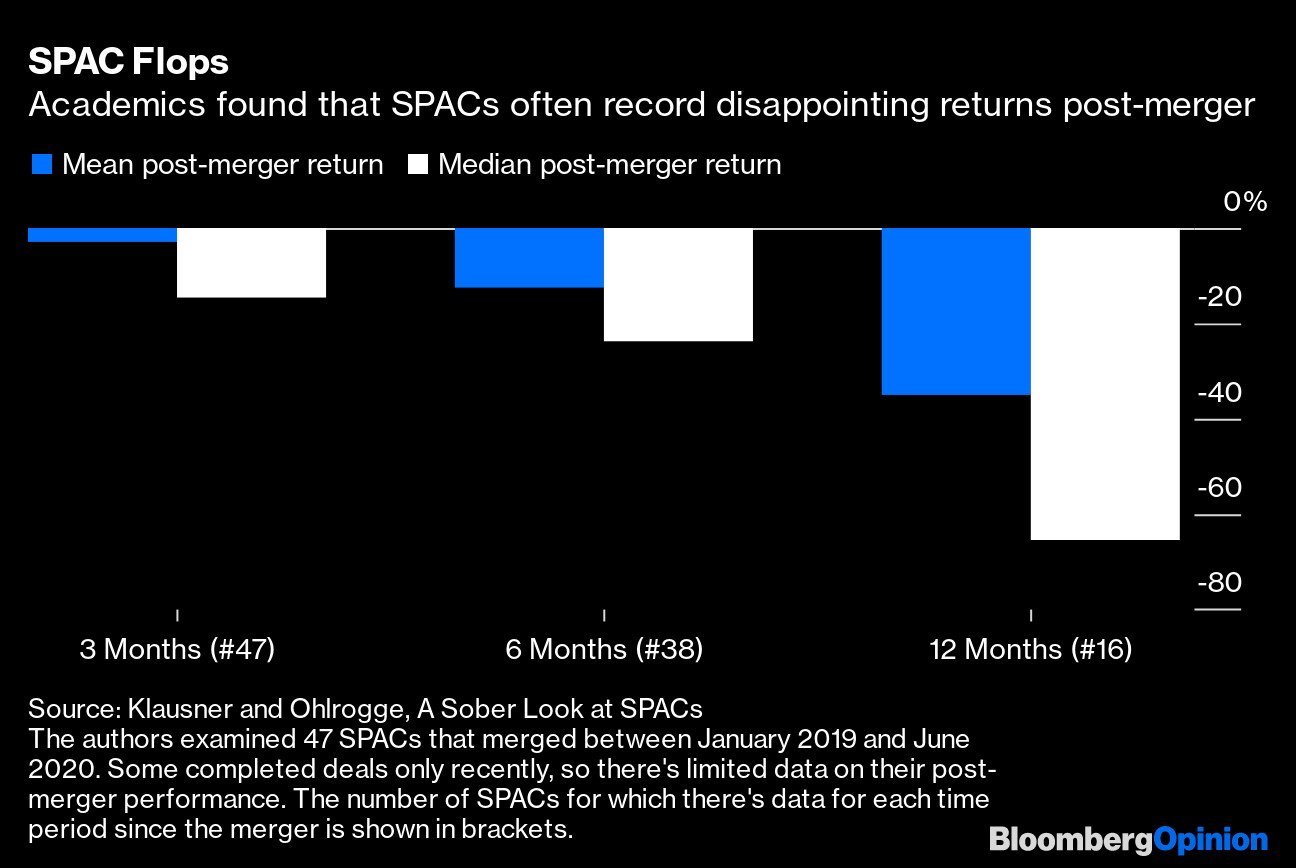

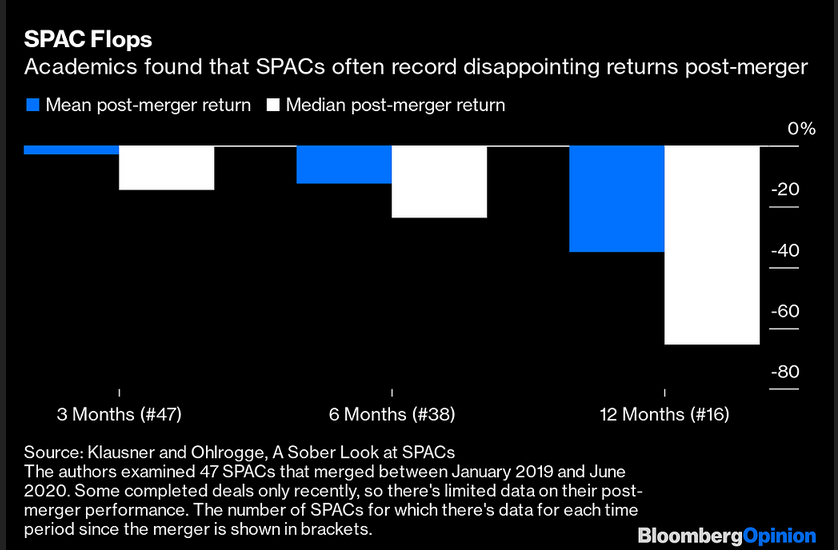

Here are a bunch of graphs for forum members to enjoy from this morning’s video. The main topic is SPACs, with a somewhat critical tone despite their great popularity (or rather, because of their great popularity ;D).

I understand why SPACs are appealing: their shares are priced at ten, which is a nice round number. As long as they don’t buy anything, their value also stays around that ten-mark. So, they have a nice lottery ticket feel to them. Many also argue that through SPACs, individual investors can access companies that only private equity investors could access before. I’m not sure, considering SPAC incentives among other things, whether the companies that investors get access to are, on average, very good investments. I know this is pointless nagging, but most SPACs go down the drain and big time when they eventually buy something:

I read on Bloomberg that even a chunk of a company like WeWork has been approached by several SPACs ![]() WeWork tried to go public a couple of years ago, when Softbank and investment banks inflated its value with hot air until the entire IPO collapsed under its own impossibility and chaos within the company. Now WeWork is trying to turn a profit.

WeWork tried to go public a couple of years ago, when Softbank and investment banks inflated its value with hot air until the entire IPO collapsed under its own impossibility and chaos within the company. Now WeWork is trying to turn a profit.

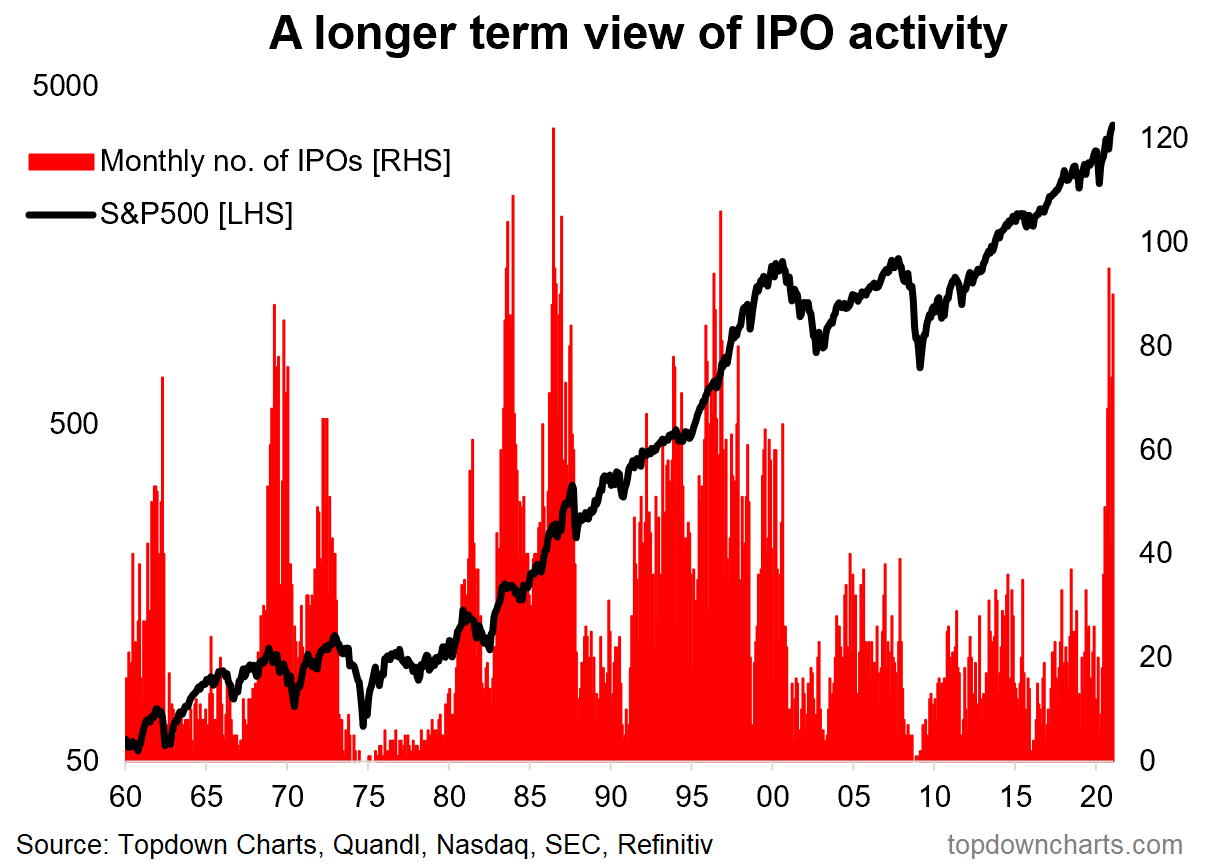

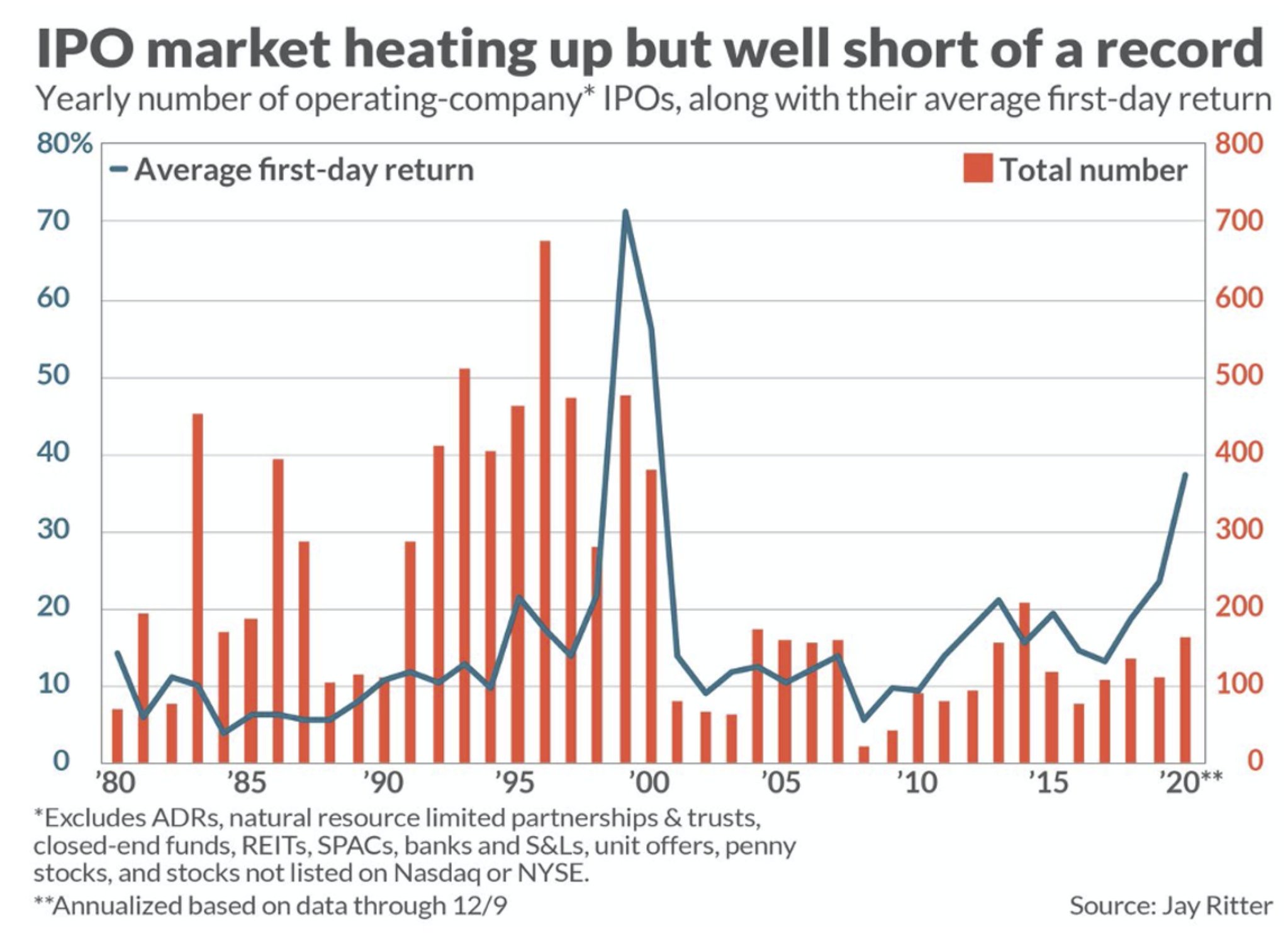

Anyway. With SPACs, the number of IPOs is approaching late 90s levels. Note that IPOs come throughout the stock market cycle, but often such IPO clusters occur at or near peaks.

Without SPACs, the number of IPOs isn’t much, although the stock reactions on the first trading day are.

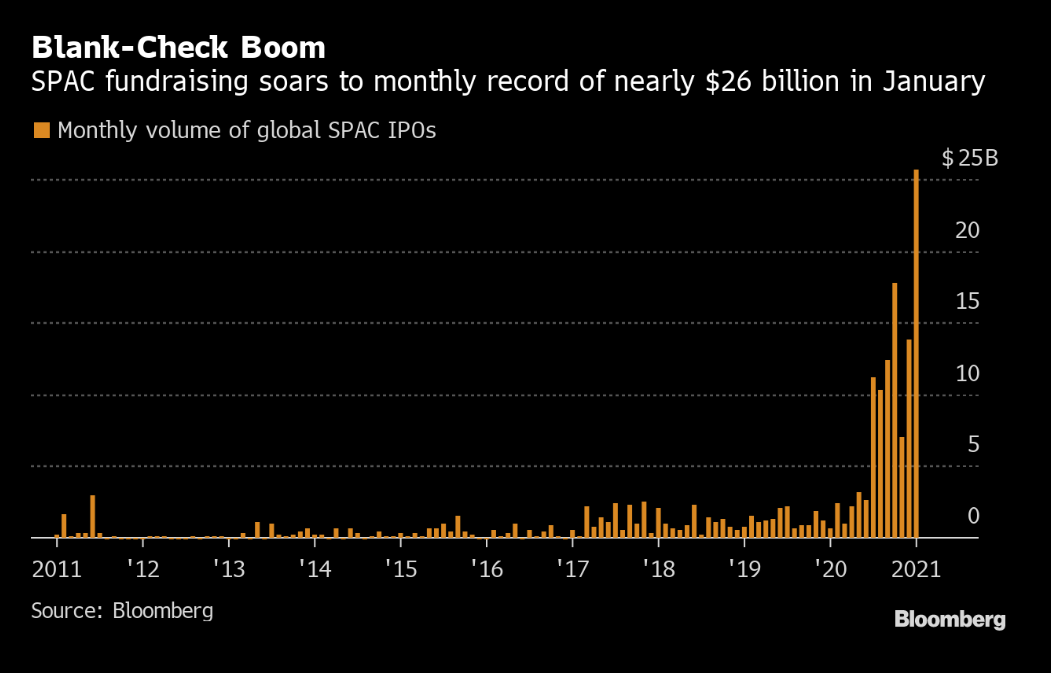

Record amounts of money are flowing into SPACs, yay

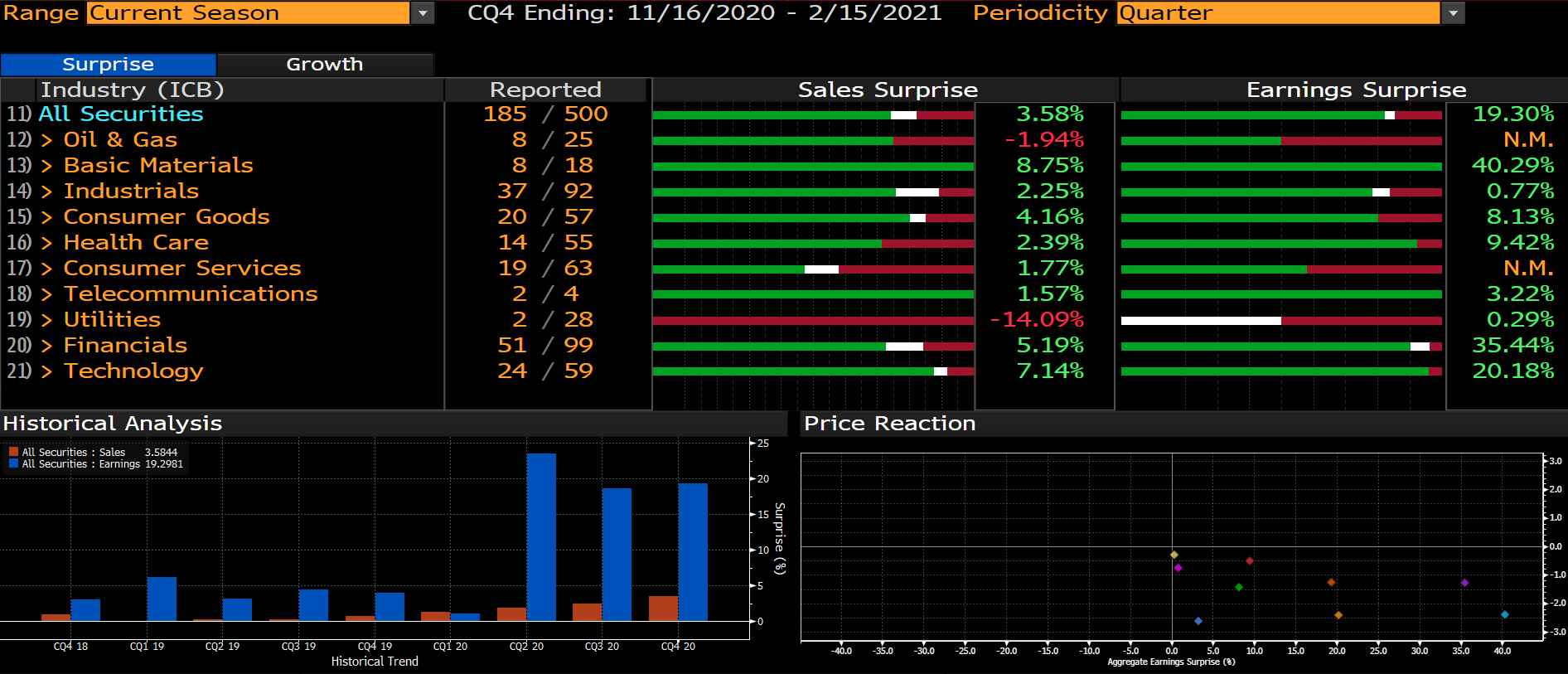

A quick look at the earnings season for S&P 500 companies. 80% exceeded expectations. Earnings are even growing slightly, in fact, exceeding expectations by about 20%. Still, stock reactions have been mostly negative.

25 Likes

When I look at these, I sometimes wonder if these returns were calculated according to the “around ten euros” share price or only after the ticker has changed/the vote has been successfully passed?

4 Likes

That’s post-merger, so not necessarily from that “ten”.

Note: that sample is already half a year old. Now, if someone could go through hundreds of SPACs and recalculate…

3 Likes

From the IMF report:

No Global Financial Crisis to Date: Don’t Turn It into One!

Delayed access to comprehensive health care

solutions could mean an incomplete global

recovery and endanger the global financial

system. With emerging market economies

accounting for about 65 percent of global growth

(about 40 percent excluding China) over 2017–19,

delays in tackling the pandemic in such countries

may bode ill for the global economy. Supply chain

disruptions could affect corporate profitability even

in regions where the pandemic is under control.

And because growth is a crucial ingredient for

financial stability, an uneven and partial recovery

risks jeopardizing the health of the financial system.

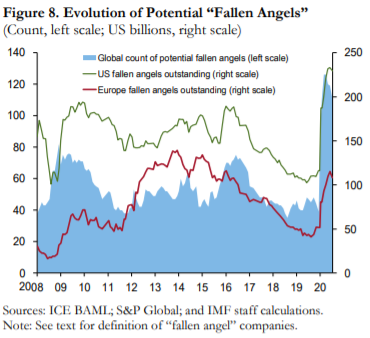

While solvency pressures have been limited so far, risks in the nonfinancial corporate sector remain.…

Default rates at large

firms have remained well below previous peaks,

and bankruptcies among smaller firms have stayed

low or even declined in some cases. However,

challenges remain. For example, the number of

potential “fallen angels” (that is, firms with a BBB

minus rating and negative outlook) has tripled

globally since the beginning of the pandemic, and

in some jurisdictions (for example, the European

Union and the United States) the potential for

further downgrades is elevated (Figure 8).

Here are those fallen angels in a graph:

How to summarize this? Risks have been under control so far, but are elevated. My feeling is that many things need to go smoothly for us to emerge from this crisis as if nothing happened. Additionally, several investors were probably interested in the following from the end of the report:

However, policymakers should also be

cognizant of the risks of a market correction

should investors suddenly reassess growth

prospects or the policy outlook.

Asset valuations appear to be stretched

in several markets. A sense of complacency

permeating financial markets as investors seem to

bet on a persistent policy backstop and uniform

market views raise the risk of a price correction

7 Likes

That has undeniably been the case. However, here’s the return of SPACs that merged in 2020:

https://twitter.com/DJohnson_CPA/status/1345757643755937796?s=20

The number of SPACs on the market and in the pipeline is likely well over 400 at the moment, so you don’t need to be a fortune teller to see that a lot of bad deals and target companies are coming in 2021. However, I would see SPACs as here to stay and with a better reputation than before. When you look at the names behind/leading some SPACs, it’s hard to see them wanting to just flip SPACs for quick profits.

As @jaska1 pointed out, there’s a difference between calculating return from the merger or from the $10 redemption price. I first got involved with SPACs last summer, and it’s still hard to see where you can get a better return with such low risk than by buying a SPAC at or even below that $10 fund value. I don’t fundamentally want to hold these long-term; I generally sell them before the merger.

13 Likes

I didn’t manage to interpret this this way, but apparently the last time there were such tired reactions to earnings overruns was during the IT bubble.

https://twitter.com/hemingwayz/status/1356230906042867719?s=21

When everything starts to be priced in…

44 Likes

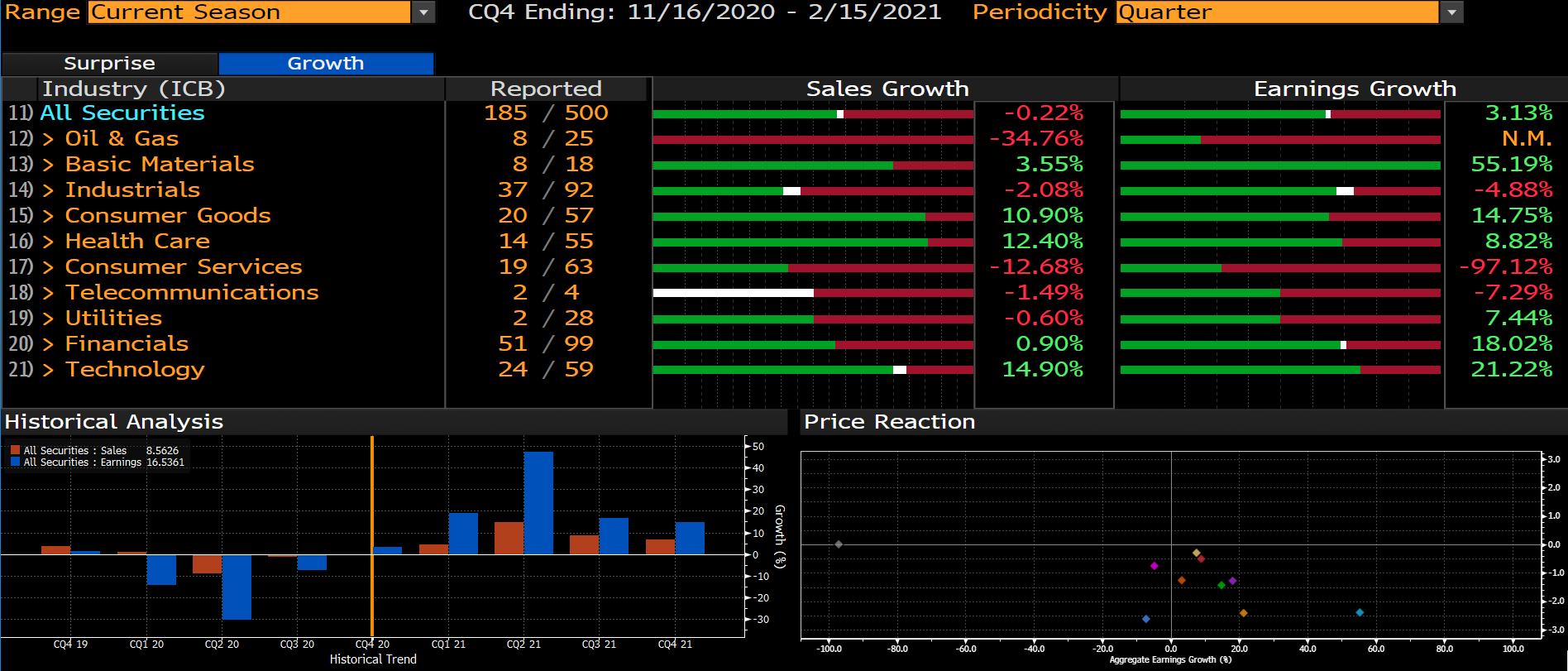

How should this be interpreted? Can we approach this by saying that the rising valuation levels are cooling down if the results catch up with the runaway stock prices, and the situation is quite healthy? Sometimes during the rise in the summer of the pandemic, some financial person seemed to ponder a theory where so-called excessively rising prices might cool down at some point, and the results would start to close this gap. I didn’t go through the companies in the message, but apart from the correction and concern due to wsb, stable big companies don’t seem to have crashed, although they didn’t rise from the reports either.

As an owner, I’m interested in China, especially Baba, from Tuesday. Its valuation has gone the other way; compared to its peers, the valuation is downright cheap, but then political risks have caused the price to tumble, and it will be nice to see if the good earnings I’m expecting will make people forget these risks. Of course, it depends on what is said in the press about the future and even the Ant IPO.

12 Likes

Yes, that’s one way to interpret it.

On the other hand, it could be due to weaker outlooks, for example, as corona isn’t being crushed as quickly with vaccine struggles. It’s hard to say what’s truly behind it all. But that chart is impressive in the sense that previously, stock prices haven’t on average fallen when there’s a clear beat (in revenue and operating profit).

Addition: as I commented in the coffee room, it’s good to note that only a third have reported their results so far. So it could still change as earnings season progresses.

8 Likes

An absolutely interesting phenomenon. I’ve mostly followed FAANG out of interest, even though I don’t directly own them, but since talking about the tech bubble is such a sexy topic, I somehow see it as healthy that it’s not always pushed northeast, even if expectations are met, and instead, a little bit of a handicap is given regarding those valuations.

Perhaps investors are now genuinely looking 6 months ahead to the autumn, and with everything being so foggy in the crystal ball, they’re taking a moment to relax and see what appears for the next half a year.

I mainly commented on this because the tweet mentions the situation being like this at the peak of the IT bubble, which raises everyone’s stress levels, and I personally approach the situation a bit more calmly and even see it as a good cooldown.

13 Likes

I also have the impression that earnings announcements will almost invariably cause the share prices of these highly-risen stocks to fall. The biggest gains seem to happen with stocks that are 1) genuinely rising for the first time ever and have not yet experienced the unpleasant feeling of a decline, and 2) the company may not be profitable, and the P/E ratio cannot be calculated, so the price increase is based on unrealistic dreams and imagination (more elegantly put, expectations of the future).

When the earnings announcement comes, the dreaming ends as the limitations of the real world are presented in the form of financial results.

2 Likes