This is a Norwegian company founded in 2005 and listed on the Oslo Stock Exchange in 2018, which develops and manufactures bendable thin lenses based on the piezoelectric effect for industrial, medical, and consumer electronics needs. Those seeking a more detailed technical description can find it here.

Market capitalization approx. 60 million euros. (Note, I am converting Norwegian kroner to euros for clarity, using the formula 1 EUR = 10 NOK.)

PoLight appeared on my radar from an interview with Juha Alakarhu, known from Nokia’s former camera unit. He currently serves on the company’s board (albeit without share ownership). Tampere is home to one of the company’s offices, and some former Nokia/Microsoft “camera gurus” have been hired there.

Products and Product Development

Why should one be interested in the company? The “piezoelectric lens” has advantages over traditional lens solutions: power consumption and space requirements are smaller, and the focus delay caused by the “pumping effect” of the motor moving the lens is absent, as the lens is bent to the desired position with electric current.

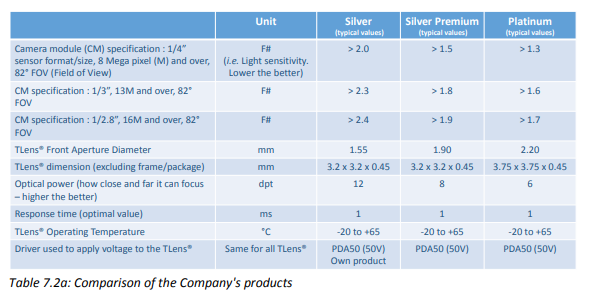

PoLight uses the name TLens for its product. The image below details the different product versions (source: IPO material), of which the Silver and Silver Premium versions are on the market.

The most advanced version, Platinum, which produces the best image quality, is currently on hold as the company cuts its development costs. In the IPO material, the Platinum version was described as being ready this year. The differences between the products relate to, among other things, the required space, image quality, and thus naturally the final price of the element. (Source: IPO prospectus, section “Products” and annual report 2019)

The product’s cash-burning development phase is still ongoing. Freezing the Platinum product version for now reduced R&D costs, but at the same time, it excludes PoLight from high-quality rear cameras that bring better margins, to which consumers are already accustomed in their mobile phones.

According to the company, development and commercialization will continue once current products have established their place in the market. A small reservation must be made that this may never happen.

Use Cases

The number of potential use cases for PoLight’s technology is large, but the company sees AR (Augmented Reality) glasses as the most significant opportunity. Since the entire market is nascent, there is no need to displace previously proven technology and win markets from others.

\u003e ”This includes consumer market devices, such as smartphones, wearables and augmented reality, as well as a wide range of industrial applications, such as barcode readers and machine vision/sensor application…TLens is currently being considered for use in next generation augmented reality (AR) glasses by several market participants. While the AR market is still at an early stage, with low volumes, it could potentially be the next ‘big thing’ in the consumer mass market after the smartphone. ” (Source: 2020/Q2 report)

A “design win” is an important milestone for the company, where a proof of concept demo materializes into product and TLens orders. TLens is currently used in two children’s smartwatches (Chinese market, as a front camera and a shooting camera) and the first industrial product using the lens is a handheld scanner, which will be launched by an OEM manufacturer during the autumn.

In addition, in the Chinese market, the product has already ended up in a Xiaomi mobile phone, as a front camera, as I understand it. Potentially, a mobile phone could have several TLens lenses, but as mentioned, without a high-quality rear camera enabled by the Platinum version and further software development, there is no access to higher-priced devices.

Note: A month ago, a press release was published stating that development of a Platinum-type TLens would resume with the support of an unnamed camera module supplier, but this was only an MoU-type preliminary commitment.

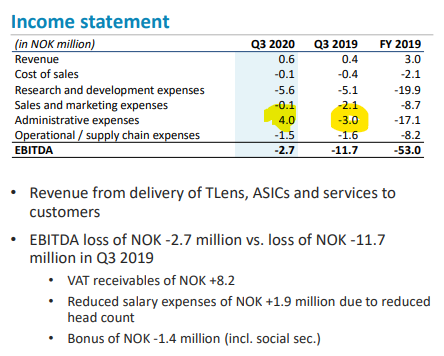

Financials

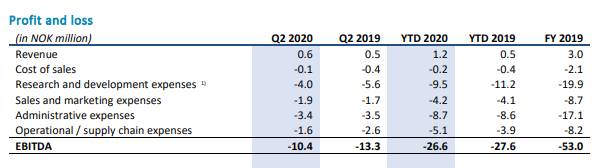

(Images from 2020/Q2 presentation.)

In 2019, the company incurred a loss of approximately 8 million euros, and cash flow was approximately -5.4 million euros. The company arranged an offering in the summer (5 million euros), with which it secured its financing until 2022, according to its own words.

For 2020/Q2, the cash burn rate has slowed down, thanks to personnel (read: R&D) cuts compared to the previous year. After Q2, the company has approximately 9 million euros in cash, so the company’s estimate of cash sufficiency until 2022 is realistic.

According to the company, the “pure” product development phase is ending, so the cash burn rate will slow down and revenue growth will begin. On the other hand, customer projects and production support activities require resources and increasingly tie up capital. PoLight uses a subcontractor for product manufacturing. In my understanding, scaling up capacity is not an issue.

The first Proof of concept projects are now converting into orders, although we are not yet talking about large sums. In 2019, the company’s total sales were only 300,000 euros, consisting not only of lenses but also of development kits and ASIC driver chips controlling the lens.

The company does not provide euro-denominated guidance for the current year. No delivery volume target for this or the coming year has been published either. So far, the company is ahead of last year’s revenue, so revenue growth compared to last year is possible. It does not appear to be a major growth leap.

In the long term, the company believes it will be profitable if it becomes the chosen solution in smartphones and barcode readers (Source: IPO material). The breakeven point has not been described in more detail than this. Unofficial online sources estimate the selling price of a TLens unit at 2-3 USD, but this is not the company’s own factual information and should therefore be taken as an approximation.

\u003e If the Company is able to achieve design-wins within both the smartphone and barcode segment, the Company expects to become profitable. If it is successful in reaching all of the milestones listed above, it has an ambition of reaching annual revenues of USD 150 million at a targeted EBIT-margin in the midtwenties. (Source: IPO prospectus, EBIT margin not disclosed.)

Currently, achieving the original revenue target would require revenue to approximately double every year.

Strategy, its Implementation, and Risks

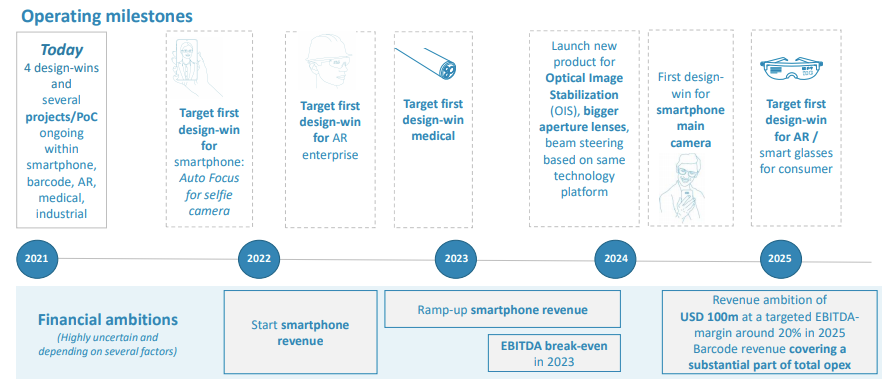

In its strategy, the company has first sought to gain a foothold in the barcode reader and mobile phone/smartwatch markets. So far, the strategy has been implemented as planned, although achieving design wins has taken slightly longer than initially estimated.

Barcode readers have a relatively long “shelf life” compared to consumer electronics (several years vs. one year). Therefore, more significant than individual design wins in the mobile phone/wearables sector would be repeat orders from the same players. This would signify a genuine breakthrough into lucrative markets and continuous cash flow.

“Selling” a new solution to various market players is a challenging task and can take longer than initially imagined, especially in established markets, despite TLens’ obvious advantages. According to the company, COVID has already affected the launch of smartphone PoC projects and slowed progress. This should be kept in mind when drawing rosy growth curves.

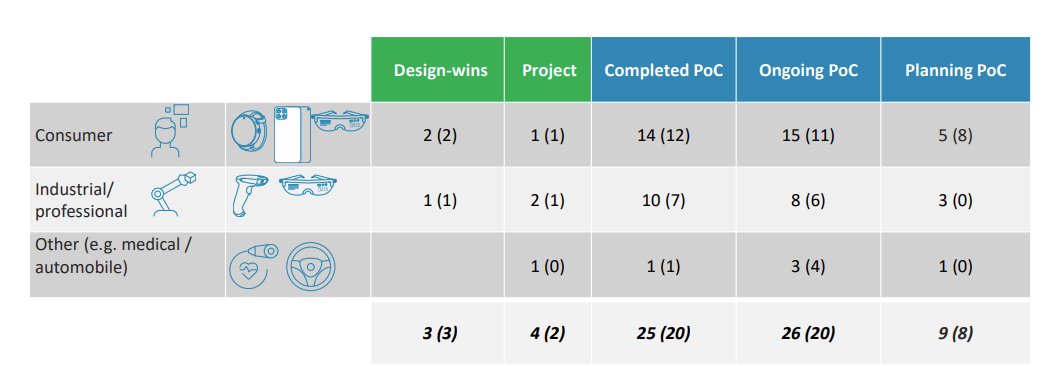

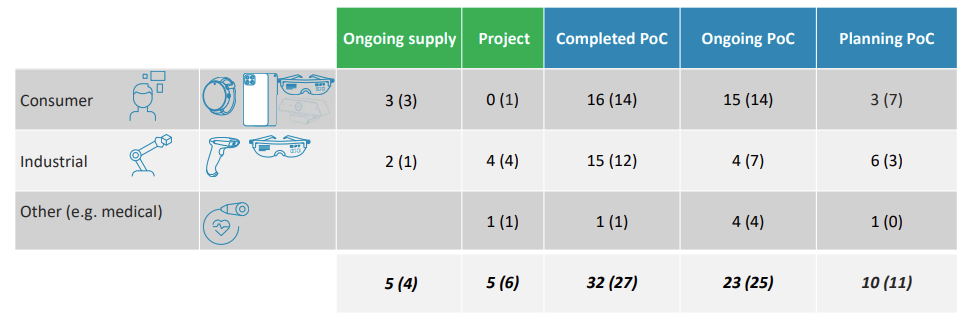

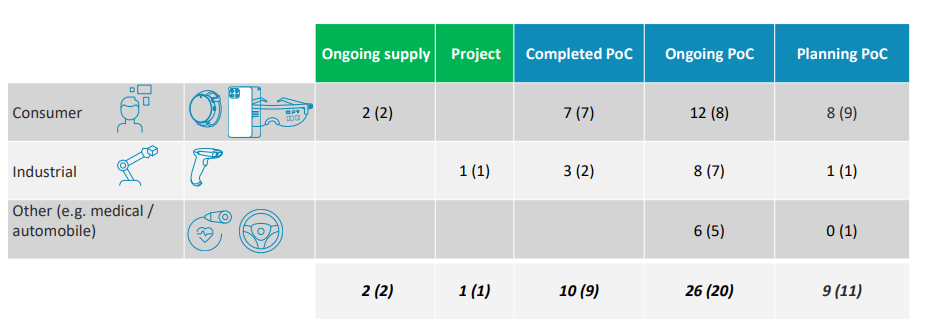

In the Q2 quarter, the project situation is described in the image below: the number in parentheses describes the situation in the previous quarter. The concentration of numbers on the right side of the image excellently demonstrates how early the product’s commercialization phase is!

There is a decrease in the “Planning PoC” column compared to the previous quarter, and I believe this is explained by delays caused by the COVID shock. Although the size and significance of each PoC project for the company are not equal, the “Planning/Ongoing PoC” columns are one indicator of the realization of TLens’ potential.

Despite delays, the pace of progress and the future across all different segments were described as good in management’s speeches in the Q2/2020 presentation material.

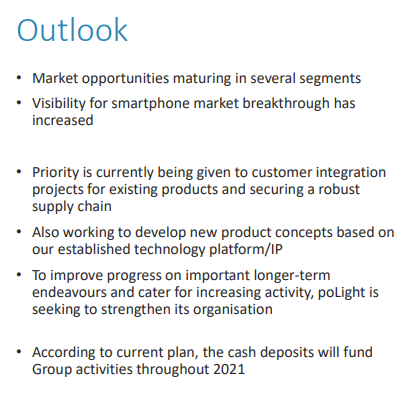

Market focus on

- securing the first design-win for barcode

- position poLight for the first AR case

- follow-up orders/new design-win for smartwatch cases and bring poLight existing products, and longer-term potential new products, into the smartphone market

Expect good progress on all the above activities the next twelve months

Expectations have been set high for the next 12 months!

Verdict

The stock price, like other small tech stocks, has surged ahead, and the current price level (~65 NOK) is not cheap, even though the recent price drop - thanks to sales by the seed fund (Viking Fund III) - has unwound the worst overshoot. It is illustrative how about a month ago, a single “letter of intent”-type news caused the stock price to rocket 25% to around 100 kroner.

On the other side of the scale weighs the realization of potential: a breakthrough in barcode scanners would secure cash flow and reduce the risk of a new share issue diluting owners. Design wins related to AR glasses would be a significant factor in terms of market value, even if the impact on revenue would be minor.

Disclaimer

Today I opened a Polight position at a price of 62.5 NOK. I am adding the article towards the weekend, after Oslo closed recently, so that there is no impression of “pump and dump” and interested parties have time to calmly familiarize themselves with the writing. The Q3 results will be published next week.