Let’s open a thread for a growing Canadian company manufacturing fiber optic sensors. Recent growth has been tremendous, and the company is small enough that it is still unknown to the general public. Late last year, a significant distribution agreement was signed with South Korea. The company is almost debt-free, and the P/E ratio is moderate. Here is their website:

https://www.photoncontrol.com/

13 Likes

Yahoo Finance data:

3 Likes

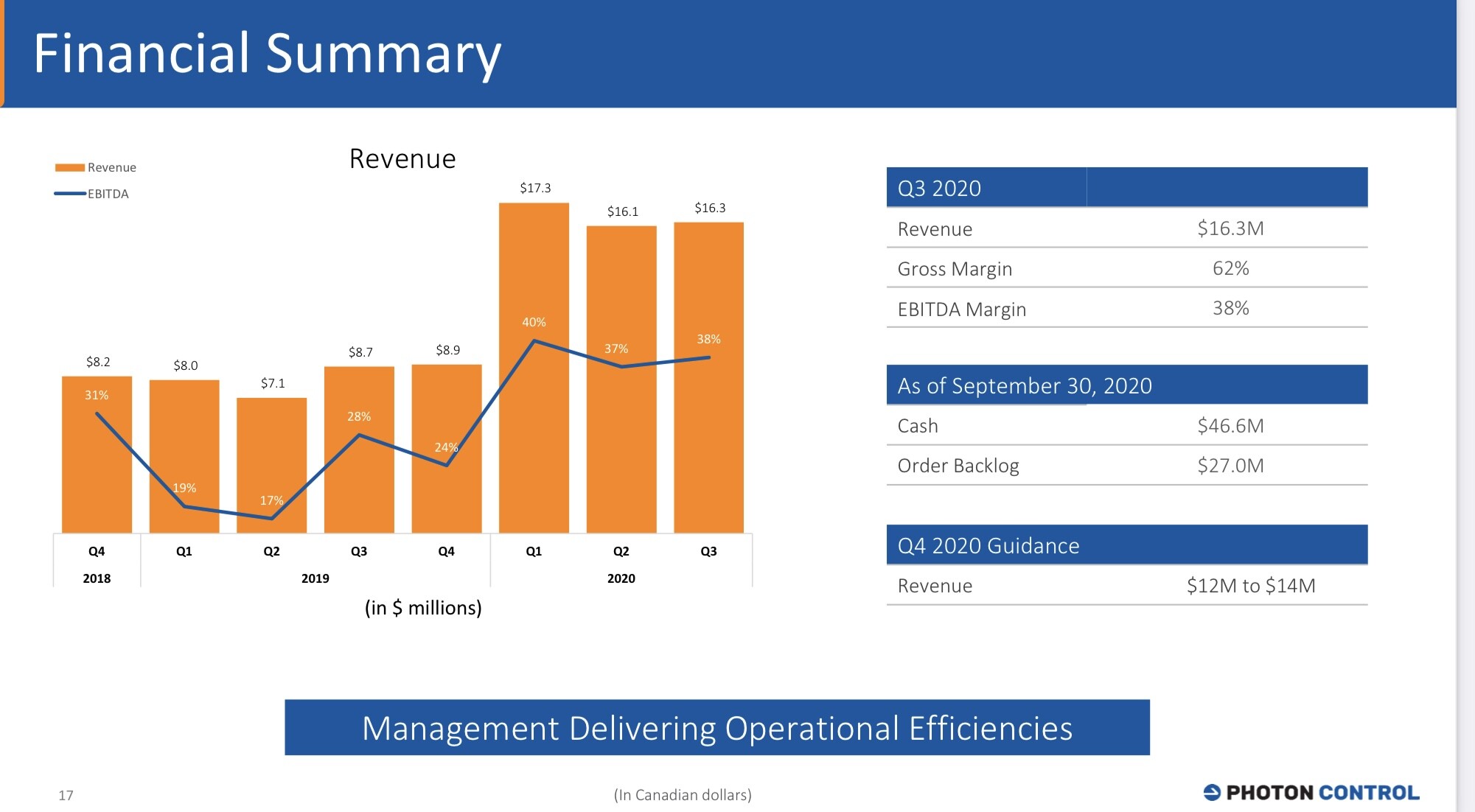

Here’s the Q3 2020 earnings report, with impressive growth. If this continues, it’s possible for the stock to skyrocket. Note the significance of Korea, which isn’t yet reflected in these figures. Highlights for the third quarter 2020 were as follows:

- Revenue of $16.3 million (Q319: $8.7m) and record year-to-date revenue of $49.7 million (2019: $23.9m);

- EBITDA[1] of $6.2 million (Q319: $2.4m) or 38% (Q319: 28%) of revenue and record year-to-date EBITDA of $19.1 million (2019: $5.1m);

- Net income of $3.6 million (Q319: $1.5m) and record year-to-date net income of $12.9 million (2019: $1.7m);

- Basic earnings per share of $0.03 (Q319: $0.01) and year-to-date basic earnings per share of $0.12 (2019: $0.02);

- Gross margins of 62% (Q319: 55%) and year-to-date gross margin of 61% (2019: 54%);

- Cash and cash equivalents of $46.6 million at September 30, 2020, increased $13.2 million from December 2019.

1 Like

Let’s throw in a question here: what happened in the summer of 2018 (if you know)?

The same could be asked about last summer, but that can probably be attributed to general market euphoria and the popularity of penny stocks.

1 Like

According to the company, the decrease was due to an increase in inventory for outstanding orders. This is believable, as the growth since then has been significant. The company is still the size of a hot dog stand, so this could have such a large impact.

I was into this one when I found it around 1.80 and sold it for around 2.30, thinking I had something better. Today I’m jumping back on the wagon.

Good find! What about Q4, guidance that revenue will be below Q3? Also, not much Q2Q growth this year.

1 Like

I don’t have more specific information on the reasons for this. I do have a suspicion, though - the business gas segment is currently a little stuck. The products are widely used in process industry and consumer electronics. I don’t know the exact proportions, but demand for the company’s products has certainly decreased as Covid has prolonged. On the other hand, Q4 would be a record for them. Korea will surely break through once the market recovers from the Covid storm.

1 Like

Yeah, hey, at least the website is from another planet compared to ILA ![]()

Cyclical business. I personally wouldn’t buy now at the presumed peak of the cycle, but rather wait for a downturn. However, the markets will punish when customers freeze investments at some point, and sales/profits decline.

2 Likes

Add a more positive view:

Bottom line: We are reiterating our Top Pick recommendation on BC-based Photon Control (“Photon” or the “Company”) following blockbuster results by Lam Research (LRCX-US, NR) and a bullish conference call earlier this evening. LRCX’s call pointed to an increasingly constructive outlook with its sales guidance for the next quarter coming in a whopping +11.2% ahead of pre-reporting Street estimates. We raised our estimates and target price earlier this month (see our note here) following a set of bullish earnings reports downstream. Namely, TSMC’s (2330-TSEC, NR) results surprised with a large capex boost for 2021 (US$25-28B, up from US$17.2B in 2020). As well, Samsung Electronics (A005930-KOSE, NR) pre-reported constructive results on the back of the Company’s semiconductor business. Photon exposes investors to best-in-class ROIC and FCF/share growth metrics at compelling valuation levels (~9% FCF yield / 11.5x 2021 earnings): Despite the remarkable recent stock performance (+64.1% in the last year), we believe Photon shares currently present exceptional risk-reward characteristics. On a more macro level, we continue to be constructive on industry dynamics. Drivers such as, e-commerce, gaming, video streaming, AI, cloud computing, IoT, and the deployment of 5G networks are tailwinds that will drive additional data center capacity requirements benefiting Photon. Our price target of $3.50/shr implies 62.8% return from current levels.

LRCX blockbuster results should benefit PHO: Top line for the December quarter came in +4.7% ahead of mid-point guidance and +3.6% ahead of Street estimates at a record $3.5B (+33.8% y/y, +8.8% sequentially). The Company’s CQ121 guidance came in 11.2% ahead of Street at $3.7B +/- $0.2M. Guidance implies a +47.8% jump y/y and +7.1% sequentially. On 2021 the management provided ample bullish commentary on the conference call, pointing that they expect 2021 Wafer Fabrication Equipment (“WFE”) in the high $60B to $70B range, up from the high $50B range in 2020. Management noted: “While today’s absolute levels of Wafer Fabrication Equipment [spending] are significantly higher than a few years ago, we believe the rapid digitization of the global economy combined with rising capital intensity due to greater process complexity supports robust multiyear WFE spending. In fact, if there’s a common theme that underpins our outlook for the next several years, it is that sustainable growth throughout the semiconductor value chain will be driven by the proliferation of artificial intelligence, high-performance computing, IoT, 5G and, the incredible societal advances and user experiences these technologies enable.”

TSMC 2021 capex budget not a one-off blip: Earlier this month, TSMC released capex budget for 2021 of US$25-28B, up from US$17.2B in 2020. The company pointed that ~80% of the capital budget will be allocated for advanced process technologies, including 3-, 5-, and 7- nanometer. During the conference call, TSMC spoke at length to a period of higher capital intensity going forward: “As we have said previously, our long-term capital intensity is in the mid-30s percentage range. However, when we enter a period of higher growth, our CapEx needs to be spent ahead of the revenue growth that will follow, so our capital intensity will be higher. […] Today, as we enter another period of higher growth, we believe a higher level of capacity – of capital intensity is appropriate to capture the future growth opportunities. We now expect a higher growth CAGR in the next few years driven by the industry megatrends of 5G and HPC-related applications, which C.C. will discuss in more detail.”

Contextualizing Photon’s current valuation: We believe Photon’s balance sheet strength together with its leverage to an economic upcycle constitute attractive risk-reward characteristics. Despite the strong stock performance since our late 2015 initiation, valuation remains exceptionally attractive with earnings growth keeping pace with stock performance.

Namely:

We expect the Company to generate $0.15/shr and $0.16/shr of free cash flow in 2020 and 2021, respectively, versus a stock price of $2.15/shr ($1.71/shr, ex-cash), implying FCF yields of 8.8/9.1% for 2020/2021. Photon currently trades at 6.7x/6.1x our 2021/2022 EBITDA estimates and 11.5x/10.3x our 2021/2022 earnings estimates. We believe these to be exceptional valuation metrics by any standard. For reference, Tokyo based Hamamatsu Photonics trades at a whopping 23.3x EBITDA.

1 Like

Allow me a little boast, as I’m just chatting here anyway. Analysts believe that the low valuation levels started to break down at 52W high 2.48 CAD

2 Likes

Investointipäivillä hehkutusta:

Earlier today, I watched Peter Hodson’s presentation at the Virtual Money Show. Spent most of his presentation on hedging techniques but then finished up with some of his lists of favoured stocks. PHO was one of four Canadian stocks on his “Small Cap Fun” list. GLTA

1 Like

Others also noticed the company’s quality: https://www.photoncontrol.com/press_releases/photon-control-agrees-to-be-acquired-by-mks-instruments-and-reports-first-quarter-2021-financial-results/

1 Like

Yeah, that’s what happened, too bad I wasn’t involved anymore. I ended up selling mine for a little under 3 CAD. A nice profit, though. Too bad the thread didn’t really pick up steam. A lot of people missed out on making money.

Thanks for bringing this up anyway. This short thread was enough for me at the beginning of the year, even though I now have to fish for new information again.

1 Like