Polight receives an 870 kNOK order for TWedgen technical samples. The direction is, as usual, an AR/MR product from a “top tier” manufacturer.

The press release doesn’t highlight it, but this is not a finished product; at this stage, it’s a product development concept whose exact specifications and features await the commitment of a “lead customer” to productization.

Despite this, product houses see the opportunities as so significant that they are ordering paid trial kits to see the technology’s potential and its impact on their roadmaps.

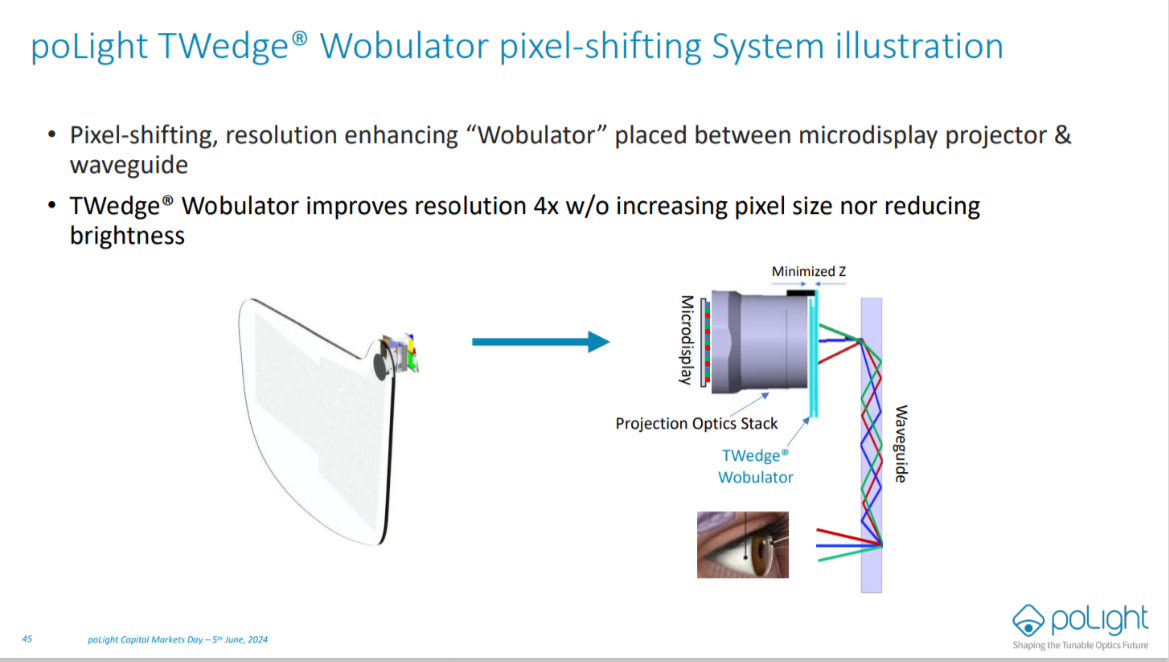

Promising, but as the press release also emphasizes, the technology is in its early stages. (Below is an image of TWedgen from last year’s CMD set.)

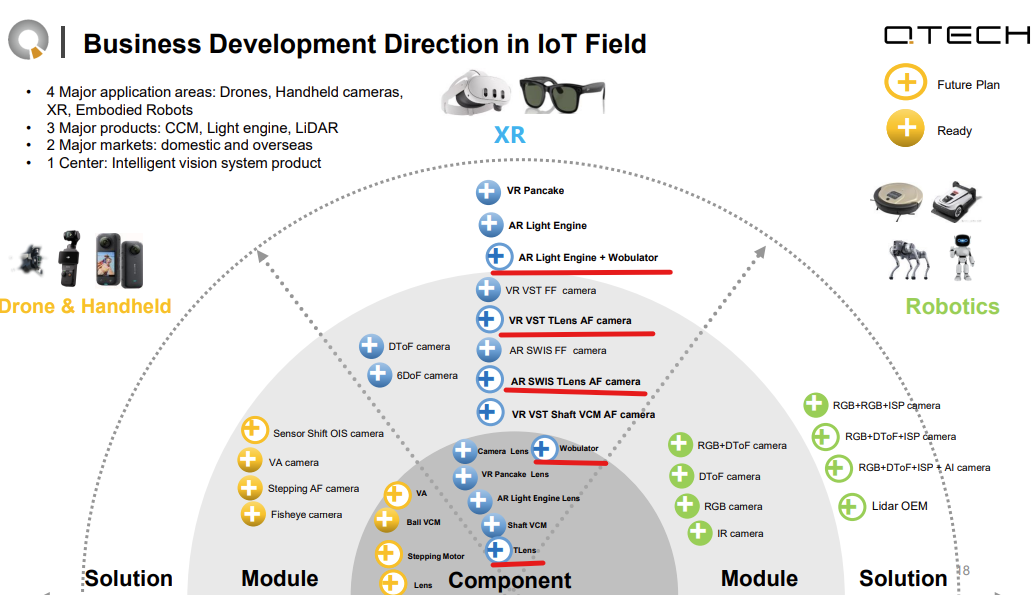

Polight’s largest owner, Chinese Q Technology Group, published its Q2 results a couple of days ago. Without going into the company’s results in detail, it is interesting to see how they, as a supplier of optical modules, perceive the larger strategic picture and market drivers.

For Tlens and Twedge, the application has so far been seen in the XR sector (AR/MR), and the status is “future plan,” which, based on a later slide in the same set, means 2026.

Component classification should not be seen as compartments, but rather as market drivers, where the component’s best “fit to market” and development needs are currently focused. In other words, the XR market does not exclude Tlens or Twedge from later AI robotics markets, but development is driven forward by the XR sector and its emphasized features.

In large robots, the current consumed by traditional VCMs is not a problem, and it is fundamentally a popular component because the mechanics required for physical movement inherently require power. The market is not binary; there is a place for both components.

Depending on Polight’s product development capability to drive down the module-specific price of Tlens, the market potential will either increase or decrease.

Follow the irresponsible dot-connecting in the form of speculation without any concrete evidence. I’m writing this here so that @In_Der_Esche or someone else can shoot it down.

I admit that even if such a connection can be made, it is still far-fetched, and I consider this more as one alternative among others. Perhaps Anduril’s expansion into Norway would have made the connection stronger. Based on what little I understand about the subject, poLight’s technology would nevertheless be a suitable piece for the applications developed by Anduril. Only the Chinese major owner is, at first glance, more difficult to reconcile with products developed for the US military.

As I understand it, this concerns a deal Microsoft received at one point, which Microsoft then sold to Anduril. Microsoft’s device was HoloLens-based, and at least versions 1 and 2 did not include Polight’s technology. This is not surprising, as TLens was not mature enough as a product to go through the NATO-level certification path, which I assume is thorough and demanding, for example, regarding drop resistance, vibration, and other measurement targets.

Meta and Anduril have entered into an XR device deal, and if Meta uses Polight components in its own future headset products (only circumstantial evidence like patents), the same components could end up in military use.

According to Anduril, different versions of the product will be made, so device-specific requirements will likely dictate which components are needed at any given time. TLens and TWedge (once completed) would offer the same benefits in military use as in civilian use, but does the proven functionality and supply reliability of VCM technology, for example, weigh more in the balance?

At the same time, it must be stated that Chinese Q Tech’s significant ownership in Polight is not beneficial for potential cooperation.

In typical American style, there is no shortage of hype, “best device ever,” and terms like sensor fusion and 360-degree situational awareness are abundant. The device’s price is stated as “over $10,000,” which is not surprising if one has looked at Varjo’s list prices, for example.

It feels like costs are scaling heavily with the growth in demand for the company’s products. I don’t really know at what point this could start making money. Is it then that giant order from a big manufacturer? I wonder if even such a thing can be done profitably.

Turning Polight profitable requires exactly that. The business model scales excellently, and if the company’s lens becomes the de facto standard for AR/MR glasses, the company’s strategic position will be strong.

The extremely high margin of the lens solution will quickly reflect in the operational profitability. Of course, it requires that there are no blunders in assembly, etc., the basic things that scaling a business to a new size demands.

As hopefully has become clear from the thread, the risk of a different outcome naturally exists. Without a strong position achieved in AR/MR glasses, the path to a profitable result is long.

This game is very binary in nature, and intermediate outcomes are unlikely. Currently, Mr. Market is optimistic.

Perhaps the most significant event of the coming week, from a PLT owner’s perspective, is Meta’s annual Connect event.

\u003e The theme of Zuckerberg’s keynote speech is tantalizingly “…the latest on AI glasses and Meta’s vision for artificial intelligence and the metaverse.”

I do not believe the product releases presented at the event will contain any Polight components. Attention is focused on Meta’s next-generation devices, where Tlens’s involvement is more likely. I expect Zuckerberg to present a more developed version of the prototype introduced last year.

Stay in the Shadow - oh, did I write that in caps - what a mysterious “high-end mixed reality” manufacturer it is. The “initial mass production purchase” leaves it to speculation how large the actual bigger order could be, but it probably wouldn’t exceed a million either. Currently, the order size was 0.4 MNOK.

Not many manufacturers produce expensive, enterprise-class MR glasses, so unit demand is measured at most in the thousands. Correspondingly, the per-lens margin is likely top-notch.

Pasila. Porilaisten marssi! (March of the Pori Regiment!)

Now the first larger order has come in. The same US company that has placed orders during the current year, on its way to a product launch.

EDIT: Let’s reserve the possibility that the customer is a DIFFERENT US company than before. The press release does not mention the order being a continuation of the previous one, and the sentence “We’re extremely excited to be a part of this AR camera design effort with a leading OEM” seems strange if it were a so-called old acquaintance. If so, it would further increase the significance of the press release!

This, in my opinion, is still an order preparing for mass production, and depending on the continuation of the product project and the size of the demand, 1-2 more orders will come next year. NOK 5 million is a large order in Polight’s history, but more significant is the demonstration of the product’s capabilities provided by the example of the order. Other good things will follow.

It has been a long road, but now the awaited breakthrough to become a significant component supplier in the AR field is a hell…very big step closer to reality.

…has received a purchase order to support a top tier U.S. consumer electronics OEM in designing a TLens®- based camera for AR applications. The purchase order, valued at approximately NOK 5m, involves efforts to design, build and execute aspects of TLens®-enabled future cameras that could be used in several AR head-worn devices. The TLens® Add-In lens and camera module samples are scheduled for delivery in Q1 2026

Well, what do you know, within a week, first a record-large order and today’s published lens order takes the #2 or #3 spot on the podium.

The purchase order is valued at NOK 2.6 million with a partial delivery worth NOK 1.3m by the end of 2025.

As has been noted repeatedly, Tlens is a versatile product. From camera lenses for AR glasses to microscope lenses.

The microscope lens stack was, if I recall correctly, triple (a device opened as open source by Norwegian Kavli), so a larger number of lenses goes into one sold end-product at once. The precision requirement is top-notch, because when stacked, optical errors would be severely exposed. That is reflected in the price of the lenses (and their finishing).

Updating the thread is starting to feel like work. Follow-on order for TWedge worth 1MNOK. These are still technical prototypes, meaning TWedge development is still ongoing. Therefore, the interest at this stage is very encouraging.

“As customers continue to evaluate our TWedge® wobulation technology, we are encouraged by their progress toward potential mass production supply for consumer devices”

Quarterly reporting is behind us, and the stock price, as usual, takes a dip. Well, there had already been such a significant rise that shares acquired in June are now twice as valuable.

Reflected by revenue, the valuation is indeed high – with annual revenue (~20 MNOK), the price/sales would be around 70-75. This wouldn’t make sense unless that cash cow was already a bit closer.

According to the very cheerful CEO’s projection, revenue will already increase more next year. I assume this means talking about 2-3 million Tlens orders (per large OEM’s AR glasses order) plus Twedge and design services on top of that.

The unit price of Tlens varies depending on the application, finish, and order volume, but if one estimates the average unit price for a large order to be 10-12 NOK per piece, we are at least in the right ballpark. The rest depends on timing.

Don’t expect [next year] yet super high volumes, but higher volumes

The most significant volume pull is expected from AR/MR glasses. Based on the CEO’s comment, it’s pointless to guess which of the big OEM players are involved – they are all involved, one way or another.

All major OEM’s work with both TLens and TWedge…AI/AR/MR glasses.

Some may only be doing benchmarking, and the final product will appear – if it appears – towards the end of the decade. Meta is likely to be the first, with others following, and Chinese companies close behind.

On the scanner side, the plugin lens compatible with the M12 interface is good for lowering the adoption threshold of the product. Based on the presentation, the Tlens component could also be connected to a Raspberry Pi, which opens up the market for hobbyist builders.

I won’t include the traditional pipeline image of design wins and ongoing PoC projects. The numbers are already so significant, especially in the AR/MR sector, that new order announcements will come sooner or later. There’s no need to guess if Tlens will break through in the market – it already has.

After the Q3 report, there was also an announcement about a design win for AR glasses in the medical sector. Based on a quick search, it doesn’t seem like a significant cherry on top of the cake, but rather a small startup for whom getting their name in a listed company’s press release is a reference in itself. Still, everything counts.

With good feelings towards next year. Watching the stock prices, there will be rallies and dips in both directions, but on average, I predict rising levels for next year as well!

Another new order in a row. 900 KNOK follow-on order for TWedger. A follow-on order is always a good sign - the potential has been noticed and the customer is continuing their projects.

Going forward, I will no longer link orders under one million to the thread, as otherwise, there might be too many chain bumps for some tastes. Even small orders are nice news, but their significance in the overall picture is already diminishing.

Everyone can get press releases in their mail if they wish, and apparently, Inderes also provides press releases from the Norwegian stock exchange:

A couple of smaller orders went unreported in the previous post for the reason mentioned, but it’s good to mention the opening of a new - in business language, a new vertical.

Already a few years ago, medical endoscopes were close to realization, but now access to optical inspection devices for internal surfaces came from the industrial applications side.

Based on the customer’s statements, this is not just any ordinary “temuskooppi” (temuscope). Stacking three TLens units sounds like the same application that has been used in the bio-side for imaging brain activity in so-called Kavli microscopes.

Apparently, the structure is not a “fixed focus” solution, but capable of some kind of adjustable zoom, which further increases the difficulty factor. For the same reason, I assume the unit price of the lenses is significantly higher than normal, so even though the initial delivery quantities are “would fit in a letter”, the per-unit margin is good.

TLens® is an excellent fit due to its small size and durability, and by stacking three TLens® units, we can achieve the required focusing range. Initial customer feedback has been promising.

…integration of TLens® into an industrial endoscope application. This marks the entry of TLens® into a new market segment. The first few hundred TLens® units have been ordered and will be delivered in Q4 2025.

Yesterday there was Raspberry news, and now an order for scanner lenses worth almost 2 MNOK came in. By gut feeling, this is the largest (or at least one of the largest) lens orders in the scanner sector in history.

As highlighted in the press release, the new M12-format lens component further increases order potential for 2026.

Some reflections on the possibility of a breakthrough for AI glasses (?) appeared on the Inderes front page. “AI glasses” is an unfamiliar category to me, so I assume it falls into the MR/AR (mixed/augmented reality) glasses category.

Be that as it may, rapid growth is expected for the industry, and there is no doubt about the importance of the role of optics. AI requires high-quality, well-focused images, and Polight’s products offer a solution for this.

Explosive growth on the horizon

Citi predicts that smart glasses shipments will grow by an average of 105% per year between 2024 and 2030. This would mean approximately 112 million units sold by the end of the period. Of note is the revenue side, where the market is estimated to grow at an annual rate of 112% to approximately 40 billion dollars.

I am not familiar with the Swedish firm Analyst Group, but the company has produced an analysis report on poLight. It’s a Buy recommendation, so it is no surprise that the target price (9 NOK) offers upside compared to the current share price. That’s how they tend to be across the bay, I guess.

The analysis itself is, however, a solid piece of work and provides basic info on poLight and its business opportunities and threats. The key driver for the share price will be orders from top-tier players related to AR glasses over the next couple of years.

The second part of the contract has been implemented. It is promising that the customer’s project is continuing. We are still in the early stages, so the project’s finish line is perhaps only visible within 1-2 years.

The final call was subject to project continuation and the total purchase order is worth approximately NOK 1.8 million. The final call announced today is worth approximately NOK 1 million.

Polight’s Q4 presentations watched and the Q&A listened to a couple of times.

Key points in brief:

record quarter in terms of revenue and full-year revenue approx. 20 MNOK, growth of approx. 100% from the previous year

AR/MR share of revenue 70% (!)

MLens component assembly from Polight is the first step up the value chain; in addition to just the lens and motorics, a more valuable “plug-in assembly” is produced. Ramp-up is a thing for 2026.

Locking in TWedge product specs is approaching: if customers can be committed, the goal is to produce components “en masse” in 18-24 months. Based on feedback, this should not be a problem.

Polight continues recruiting, hiring 10-15 more people per year if I heard correctly –> customer demand is strong and staff workload is high

CEO estimated the first volume-significant (AR/MR consumer device?) announcement to be ahead (in the autumn?), but in a conservative manner (and having learned lessons from the mobile phone side) left reservations for schedule changes

I won’t delve any deeper into the “project pipeline” situation from PoCs to design-in phase figures. The numbers are steady compared to the last quarter (new vs. ended), and maintaining additional projects will likely require the mentioned additional staff.

For the first time, I saw sector-specific order backlog in NOK in the interim report. Not big numbers, a few MNOK, but a step from an “R&D shop” to a company communicating with hard order numbers. Based on those alone, it looks like Polight will exceed the 2025 revenue level of 20 MNOK - even if the expected “big order” doesn’t come this year.

In the Q&A session, the understandable “when will Polight be cash flow positive” was asked. Internal figures are still not disclosed, but they noted with the CFO that if the roadmap hits the mark, Polight will be “very very profitable”. What the roadmap’s end year is was not stated. Somewhere in the 2030s, I guess.

To sum up - the company is doing what it should in this situation. More gas, so that the smoldering market demand doesn’t go looking for a better-oiled alternative.