Text quoted from February. The share issue was carried out as a directed issue, contrary to my own expectations. The issue price, NOK 110/share, was significantly below the share price at the time of publication (approx. NOK 140), which naturally raises questions. A dilution effect would make a 10%-15% discount understandable, but such a large drop raises eyebrows. As an open issue, the price per share would have been higher.

On the other hand, the share of costs related to the issue remained smaller, because costs related to an open share issue (brochures, etc.) do not have to be incurred. The total sum, EUR 12.5 million, is significant in any case. If the company reaches the targeted break-even and profitability in 2-3 years, it would be logical to seek further financing from the loan market.

In any case, the timing and method of the issue raise questions regarding the Q3 report.

–

In addition, an additional order was announced this week for a previous, unnamed surgical device. An official design win confirmation has (to my knowledge) not yet been made, but signals seem to support its arrival in the coming months. At the same time, it will become clear whether it is a disposable device or part of a device.

And even if no one is interested, I increased my own shareholding by 2.5 times when the expected issue was finally completed and the share price dipped significantly.

Polight’s company presentation material, updated a couple of weeks ago. Good basic information about the company and its current status.

To my eyes, a new opening was the strategy point “become a solutions provider rather than a supplier of components”. An understandable goal - defending margins as merely a component supplier is arduous.

The year 2021 has already provided a good number of design wins and orders, but 2022 is shaping up to be a real double-or-nothing year. I’ve said it before, but Polight is a very binary company. Success accumulates, and additional sales boost margins almost like a software company. The risk of hovering around zero is evident.

Apparently, in response to criticism from small investors and to ensure equal treatment, Polight is, after all, organizing a public share offering. The price of the subscribed shares is the same, 110 NOK, but the ratio of approximately 3 shares per 100 owned shares indicates how small the offering is.

///

Science has utilized Tlens technology to image the brains of laboratory mice while they run in a test area. The trick was done by first tuning 4 Tlens lenses to be smaller and stacking them on top of each other. The result is a microscope at the end of a flexible cable, weighing only 3 grams!

This implementation will not have any commercial impact in the coming years, but one could imagine the prototype eventually leading to a commercial product and opening up new application possibilities.

To decrease the overall weight while maintaining the large z-scanning range, we developed a new type of miniature z-focusing device based on a nanotech micro-tunable lens (Tlens®,

Polight, Horten, Norway) and named it μTlens. We assembled a quartet μTlens (4 flat lenses stacked together, which weighed only 0.06 g.

PoLight’s latest report is out. It’s a rather bland report at first glance, and the share price, which had risen somewhat in anticipation of the earnings day surprise, might face a setback today. No new design wins, although the material mentioned a few design-in products.

The AR carrot is still dangling in the same spot, a couple of quarters away, but compared to previous reports, the language used was, in my opinion, more cautious. The chip shortage might also affect AR glasses’ specifications and development in the short term, so caution is warranted.

A more detailed analysis of the information will be made when there is more time. Scratching the surface revealed more positives than the presentation alone suggested. The identified need for testing and correction was related to the camera module level, not Tlens, as I initially understood and was concerned about. But moving on.

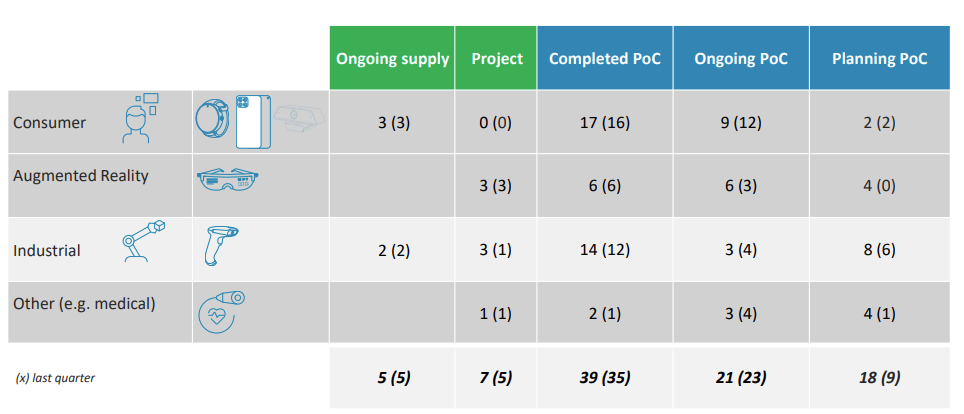

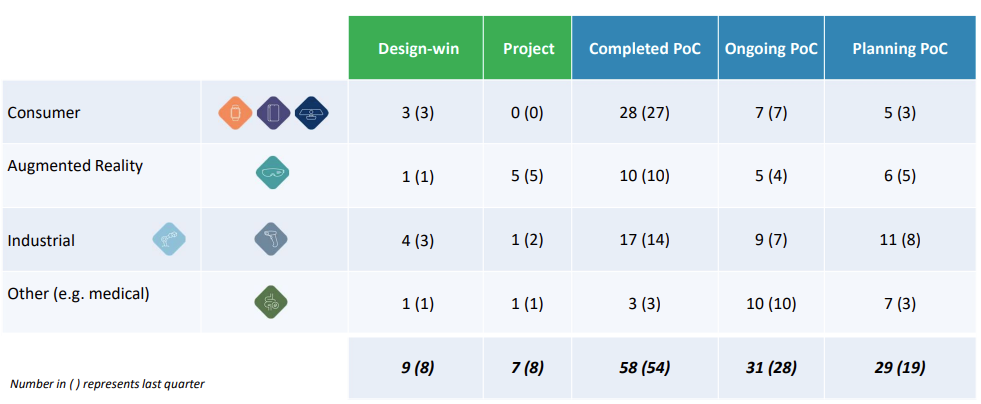

Let’s start with the pipeline image. Compared to before, the Augmented reality segment is reported as a separate entity. The Q2 figures do not completely match the previous image (quarterly comparison), but this is mainly a personal observation.

The biggest change in the pipeline is in the planning PoC column, which doubled from the previous quarter. Let’s go through these in more detail with the information from the quarterly release.

In the Consumer segment, the main focus remains on cellphone selfie cameras, as I have stated in previous messages. The target for a design win is still H1/2022, and deliveries would begin in Q2/2022. As I noted at the beginning, adjustments are still being made, but at the camera module level, so that the pieces work better together. No actor is yet in the project phase, so nothing is certain here either. The number of actors is large, so if none of these progresses to delivery, I would be really surprised.

In the Industrial segment, increased interest in barcode readers. Currently, only 1 (Honeywell) is in delivery, but 3 in design-in phase and 3 PoC candidates is a good balance and at least one design-win assumption in 1H/2022 is realistic. It’s hard to say anything about the others (1 PoC, 5 in design phase). The revenue brought by these will be the bread and butter of the company’s revenue in the long run. Unsexy but important.

The pleasant surprise in the AR segment was the strong progress of consumer AR glasses (3 projects) already to the PoC phase. Polight has estimated that consumer AR will only bring revenue in 2025, but the PoCs already underway suggest that the estimate is pessimistic. Facebook’s metaverse project is certainly not a hindrance on this path. AR glasses aimed at professional use will still bring the estimated design wins in 1H/2022, so there’s no need to rush things any further.

In the Medical segment, one design-in that has already led to deliveries is also awaiting a design win announcement. Presumably a Q1 matter, although in this segment, obtaining the necessary official approvals and certifications can take a long time. A potential DW would be high-margin, as Polight would handle part of the assembly work. The “packaging” of the standard Tlens needs to be modified, I confirmed this with Polight’s IR team.

The increased use of disposable endoscopic instruments can significantly expand demand in this segment, but as mentioned, the journey from proto to product is not the shortest possible in this area. But the margins are all the better!

Summary of next year’s design win expectations, timing, and revenue estimate on a scale of €-€€€:

It is clear that even with a slightly worse strike, production and revenue will jump to a new size class next year. This has been noted in advance in the preparation of production capacity:

By mid-2022, assembly partners are expected to have a planned monthly capacity of around 1,500,000. Material flow (e.g. wafers) and final test capacity is planned accordingly.

Polight pleasantly surprised by delivering a professional AR design win within the current year. The order value is on the scale of a large company’s Christmas party budget (NOK 360,000), but this is expected due to the market size (see the € estimate in the previous post). The press release mentions that this is the first purchase commitment, so order confirmations can be expected once the OEM (whose name has not been disclosed) gets up to speed with production.

The value of the first purchase order is approximately NOK 360.000 and is expected to be delivered within early second quarter 2022. Customer’s AR product launch is planned to be in the first half year of 2022.

And as I have mentioned in the thread, direction is more important at this stage. This is, however, Polight’s first design win in the field of AR glasses and a significant confirmation of the story the company has communicated. While waiting for the next, now more likely, wins…

…and also for industrial scanners, a new design win made it into Santa’s sack. As usual, the OEM remains anonymous. Still an expected win in an expected category.

The announcement is sparse and leaves open the size of future lens orders, but in previous cases, the volume has been 750,000 - 1.25M NOK. If the purchase order is larger, the exact size will likely become clear in the coming months. As long-lasting products, scanners are like SaaS sales; after a design win, relatively steady volume is expected for years to come, accumulating nicely with new wins.

The year 2021 was wrapped up for Polight, also in terms of figures. Revenue grew from 3 MNOK to 10 MNOK year-on-year, but EBITDA was still around -40 MNOK, so value investors are still not keen on this case!

Polight continues its familiar path, trying to gain a foothold for its Tlens lenses in various industries. It has become customary to show a diagram from PoC to design win (see below). The top of the funnel is still crowded, and Polight’s CEO stated in the investor call that their hands are full with PoCs and projects. There are curious customers, but the transformation from experimentation to regular customer takes time. The number of ongoing or completed cases has already exceeded 110.

The greatest interest was directed at selfie cameras in mobile phones. Expectations for a design win and the start of deliveries are still within H1. Details related to components are still being refined, and the supply chain is being built for operations many times larger than before. I would still consider one or more design wins likely for this year.

Regarding AR, the focus remains on achieving a strategic position. The product development related to mobile phone cameras and the credibility gained from testing is, in my opinion, a valuable validation on the path to becoming a standard component for AR devices. The pipeline looks good, and significant AR players are reported to be involved in PoCs and projects, so a foot has been put in the right door. However, a significant revenue stream is still years away.

In the industrial segment, the number of scanner projects and PoCs increased slightly. Not a sexy “wow” business like the previous one, but according to the CEO, it offers high-margin sales compared to the consumer segment.

In the medical sector, margins would also be good, but even the investor call confirmed my skepticism about a rapid breakthrough. Obtaining permits and completing tests takes time. I don’t doubt that projects will eventually materialize into revenue, but in a rigid industry, significant sales volumes are likely to be seen only from next year onwards.

In summary – no revolutionary new news from Horten, good or bad. I still see Polight breaking into AR glasses and front-facing phone cameras within a few years. Adding the wins from the industrial and medical segments, the snowball is still rolling in the right direction. The consistency between the told story and its realization is admirable.

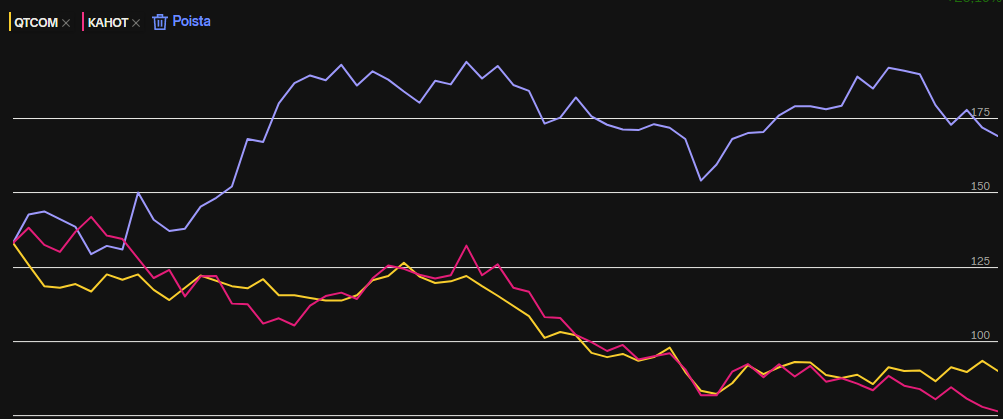

Investor sentiment, however, has changed, and it remains to be seen how investors, nervous about the decline in tech stocks, will be able to wait for Polight’s potential to materialize into results. Comparing stock prices between companies is dangerous, and I have tried to keep stock price chatter to a minimum, but as background (image below), Polight’s stock has risen (!) by 25 percent in the last 3 months, while its peers Kahoot and QT have retreated firmly into negative territory.

The current stock price, in my opinion, cannot withstand even small setbacks – in the big picture, quarters here or there, of course, mean nothing if and when the product is relevant.

Polight’s Q1 results can only be described with one word - disappointment. The situation in China is affecting phone model releases as feared, and the anticipated breakthrough in selfie cameras for this year will not happen, shifting to next year at the earliest.

The share price deflated (approx. -20%) and returned close to the autumn 2021 offering price. I got back on board with half a load.

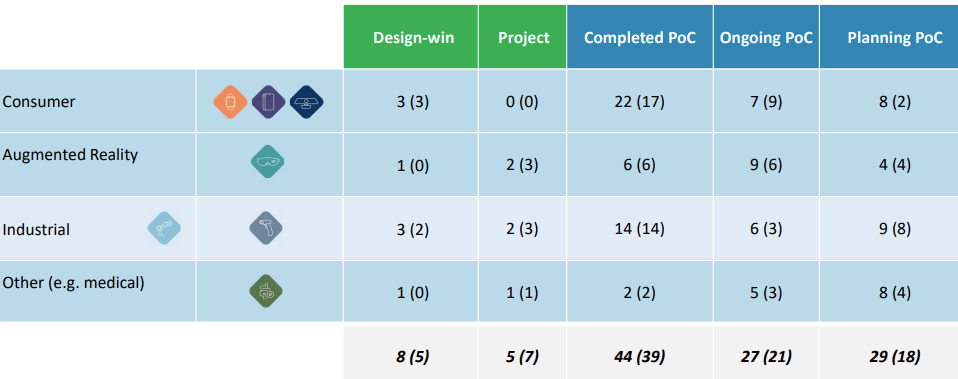

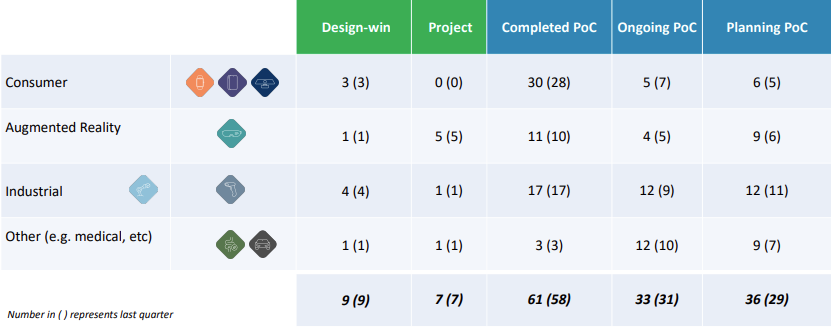

Here’s the traditional pipeline image. The PoC (Proof of Concept) department is likely near its maximum, meaning Polight’s resources cannot handle a larger group at once. The earnings material detailed the content of each segment more closely. As with selfie cameras, the situation in China may delay design wins in other segments as well. The pipeline still looks good for the rest of the year.

In the investor call, the CEO stated that the work currently being done for mobile phone lenses would be beneficial for the AR side. This includes image quality, drop tests, and commercially optimizing production. However, the wait is still long, and global turmoil is disrupting business.

Yesterday, Polight announced it would hold a Capital Markets Day in June. This is an interesting timing and a sign of the company’s maturation.

Polight held its first Capital Markets Day, as I understand it, on June 1st, and a link to the presentation material in PDF format is below. Perhaps the most interesting part was the list of competing technologies and their performance in various optical areas. Naturally, Polight listed itself as being ahead of others in several categories.

A good summary of the company, products, and their applications and targets. Plus a product development roadmap with rough target times. Recommended quick read for those getting to know the company.

Today, Polight announced another design win and order from the scanner front. 0.6 million NOK is not a huge order in euros, but as I have stated to the point of exhaustion, these are long-lasting recurring orders and generate revenue “steadily” year after year.

Superlead, which manufactures scanners, appears to be a Chinese company, and unlike Honeywell, which is Polight’s reference in scanners, it is difficult for an amateur to assess how significant Superlead’s scanners are.

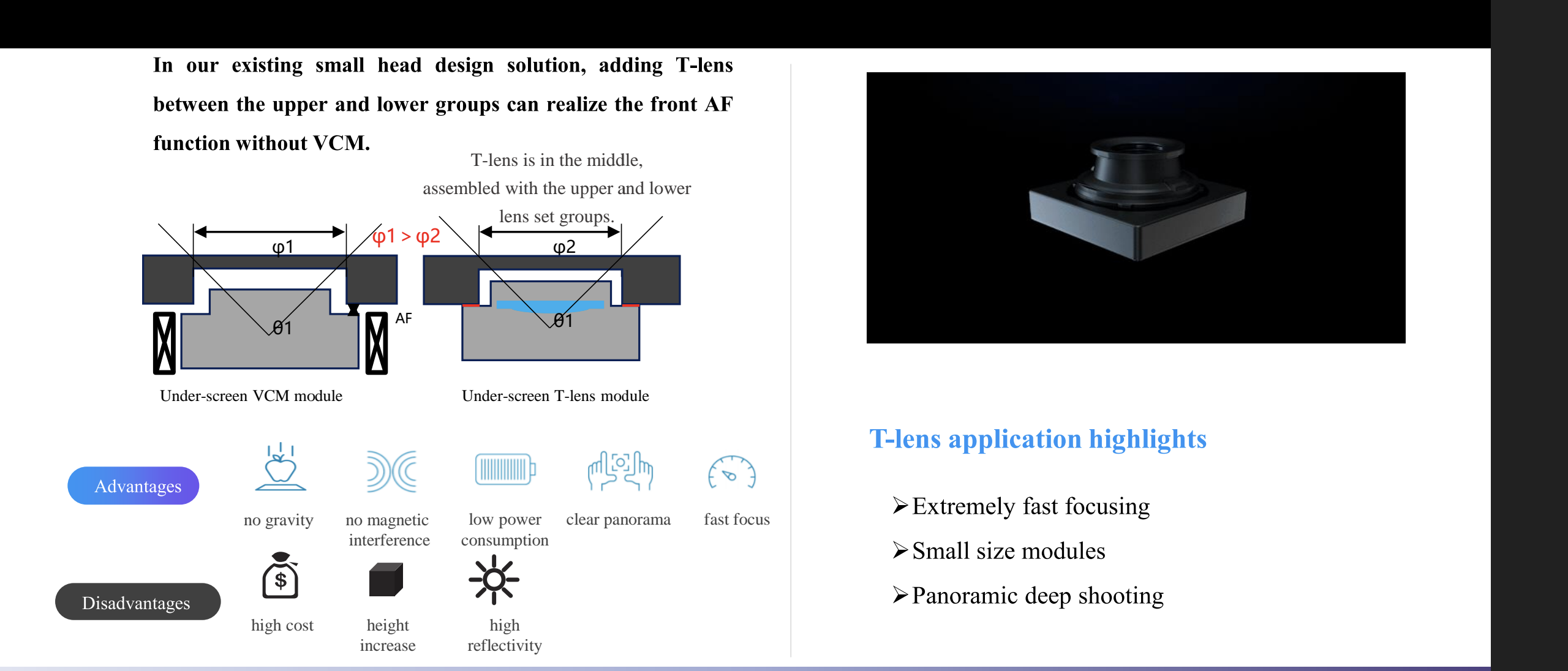

T-lens got its own slide in Chinese Sunny Optical’s investor presentation. The lens is part of the front camera module (aka selfie camera) and the solution is placed under the screen, according to the caption.

The pros and cons of the solution are listed next to the image. Among the negative aspects, high cost (cf. VCM legacy solution) is probably the most significant.

The reasons for the highlight are not clear from the material. OnePlus is estimated to be one of the first customers, but the potential design win remains for next year? I need to dig deeper to see if there’s a webcast related to the material that would explain the reason for the highlight.

Later in the presentation material, there is an estimate of the development of MR/AR/VR device sales. This year’s estimate is 15 million devices, and 50 million by 2025. The number of AR devices is still relatively small, but is growing strongly in percentage terms.

Today, a PoC agreement worth NOK 1.7 million was published, with end-use in endoscopy devices.

Still small fish, but PoC phase agreements have not been announced before, and in this case, the reason is probably the project’s size for a PoC phase deal and an apparently prominent player (not disclosed). Polight already has another project underway in a more advanced development pipeline (design-in), so the industry, initially thought to be a side stream, seems to be bringing significant revenue for a long time if the development projects are successfully implemented.

Of course, I have no idea how significant a segment a potential product would cover, but I assume that the profit margin pressure for medical devices is lower than, for example, consumer electronics. In addition, the small size of the product would likely prevent the use of a standard T-lens module, requiring customization of the solution, in which case Polight operates at a higher level in the food chain. The potential margin per lens would thus be larger.

An unnamed AR glasses manufacturer has renewed its mass production order, acquiring lenses worth 1.2 MNOK. The market launch of the glasses will take place this year. In December 2001, the first batch ordered by the same manufacturer was modest, only about 400,000 NOK. At a steady pace, the next, larger order should come in about six months?

The Q2 interim report will be published on Thursday. No fireworks are expected, but perhaps the most interesting content will be the outlook for the Medical side’s endoscopes and the status of the more mature end of the project pipeline.

In the Medical sector, a supply related to endoscopes seems almost certain. If the product were to hit the market possibly as early as this year, there wouldn’t be much time to finalize the deal. I estimate the potential contract to be Polight’s largest ever. The sector’s rise from insignificance to a potential pillar of revenue has happened in about a year.

One or more AR (Augmented Reality) players were estimated to choose T-lens for their final product by the end of the year. Although no names were mentioned, at least one player is located in North America. In the Q&A, the CEO (Chief Executive Officer) let slip that a potential customer had conducted production facility inspections “as far as Asia,” which would hardly be said about Chinese manufacturers. Polight has had a recruitment open in the Silicon Valley area, so potential customers are likely familiar global names to all of us.

Smartphone selfie lenses remain the most attractive high-volume product for the coming years, but order expectations related to them will fall into next year, as was already reported in May.

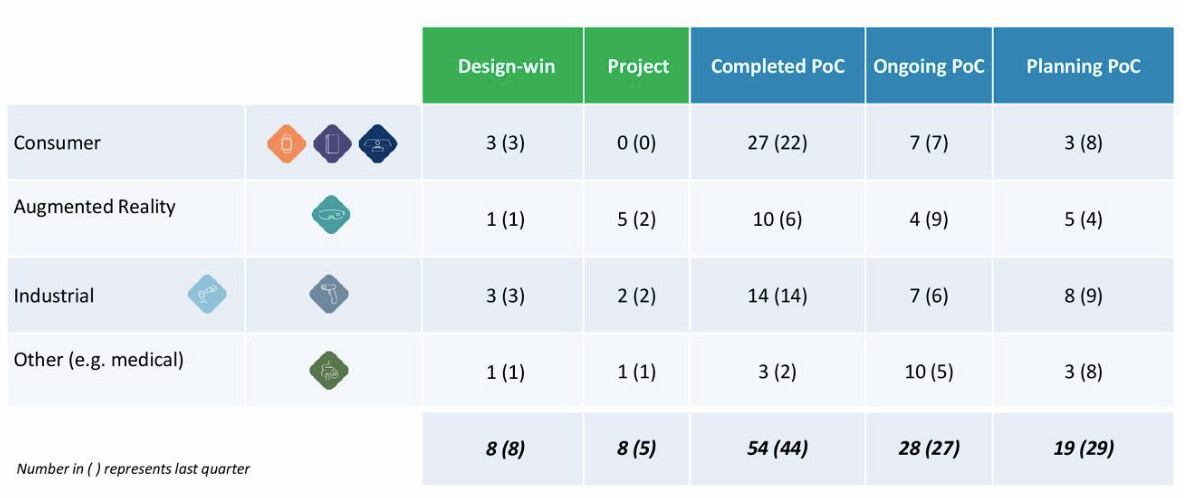

There are no major changes in the project pipeline image. In my opinion, the PoC (Proof of Concept) phase or those planning it are at a record volume.

The warehouse has been stocked full of raw materials, and more product testing equipment has been purchased, so we will follow whether the rocket lifts off the ground or fizzles on its launch pad.

Although the device manufacturer has not yet been disclosed, it is likely a Xenocor product. If I understood correctly, the imaging head of the endoscope, with its lenses, is disposable. The device received FDA approval, and the optical specifications match the properties of Polight’s lenses.

I cannot say how competitive the device is compared to conventional endoscopes. In American marketing, products tend to be more or less revolutionary.

Q3 earnings review is behind us, and it was without surprises. The increased headcount is reflected in record numbers for the PoC (Proof of Concept) department. The industrial and medical sectors accumulate the largest volumes numerically. The earnings review highlighted that these verticals are more recession-resistant than consumer electronics.

Regarding mobile phones, the honey pot of selfie cameras did not open this year either (as already reported in the spring), and attention is already on next year’s phones with a new release cycle. The pace of innovation in the industry has slowed down to incremental improvements. The economic downturn does not help development one bit.

For AR (Augmented Reality) glasses, there’s one checkmark on the wall, and based on the project status, more can be expected next year. It was important for Polight to get a reference site and to get into designers’ portfolios, even though it’s notoriously difficult, almost impossible, for other lens solutions to achieve the same performance without compromising, for example, power consumption.

The Xenocor case was now publicly confirmed in connection with the Q3 earnings review. Officially, the project is in the “qualification stage,” and the final seal is missing, but in my opinion, the cancellation of the lens order would require Xenocor’s bankruptcy or some other revolutionary event. Another endoscope device (unnamed operator), as per the summer announcement, is in the PoC (Proof of Concept) phase, and the customer-funded product development will extend into next year.

From the industrial side, scanner manufacturers’ interest has jumped significantly all at once. A total of 20 barcode projects are either in the PoC phase or are about to start. There is still a way to go before orders, but it seems that one Chinese manufacturer’s initial move related to TLens brought along a host of other competitors.

In summary: the big breakthrough is still missing. Revenue will grow to a new record this year (10-13 MNOK), but the growth leap is not as significant as I anticipated even a year ago. Shifting orders in the mobile sector are the main reason for this. Conversely, the medical segment has brought joy surprisingly soon.

I will stay involved with a smaller share than last year, at least for now, keeping an eye out for buying opportunities. The share price has remained surprisingly high, close to the prices of the share issue made a year ago (split-adjusted), even though small tech stocks have otherwise been dumped from portfolios.

The Nature article discusses the Mini2P microscope, which was mentioned earlier in the thread, where Tlens (4 units per microscope) plays a key role:

In Trondheim, Zong discovered an alternative tunable lens called the TLens, made by optics technology company poLight in Skoppum, Norway.

Designed for mobile-phone and smartwatch cameras, the TLens seemed ideal for the two-photon miniscope, Zong says. It is tiny and fast, and thanks to a fundamentally different mechanism for tuning the lens’s optical power, has better thermal stability

To reiterate, Mini2P microscopes were “implanted” in the heads of laboratory mice, and due to their lightness, the mice’s brains could be imaged live.

It was new information to me that the microscope assembly instructions have been made open source and freely available. (I still can’t assemble it; it’s not a simple DIY kit.) Opening up and publishing the design will certainly generate more use cases and modifications, as is common in the open-source world.

Again, this is not a large market in terms of unit volume, and the total addressable market (TAM) for minimicroscopes is not sky-high. The per-unit lens price is certainly high compared to the volume deliveries of mobile orders. The approval given by scientific circles and the added credibility brought by the Nature journal is a quality seal that cannot be bought with money.

The stock has been rising for the past week and especially today, as the details of the AR/VR expertise presented by the Japanese company Sharp at CES 2023 were revealed in a press release.

Head-Mounted Display (HMD) [prototype; exhibited for the first time]

Sharp will exhibit advanced devices such as an ultra-high-resolution display, an ultra-high-speed autofocus camera module (using a polymer lens), and an ultra-lightweight HMD prototype for VR equipped with an ultra-compact proximity sensor.

Ultra-fast autofocus, polymer lens… those familiar with PoLight’s technology know how to tick the right boxes.

The stock market might be giving these demo devices too much weight, as it is widely known that PoLight’s lens technology is on the desks and in the portfolios of the biggest players as one of the options. However, advanced, compact, and lightweight devices like Sharp’s demo device won’t be seen on the market for another 2-3 years.

Tech companies’ cost-cutting is reshaping Polight’s potential markets. Experimental projects that burn cash are, after all, the easiest to prune first. It remains to be seen whether Meta and Apple will put their own projects on ice; Microsoft seems to have already done so—at least partially.

Therefore, a breakthrough in Polight’s VR/AR vertical in the form of design wins won’t be enough if the market workhorse has “ceased to exist,” as Monty Python would put it.

My own view on the breakthrough of AR devices has become more pessimistic, especially regarding consumer devices. For devices aimed at enterprise and military use, 2024/25 look better, but for the mass market, the “hockey stick” curve will only start pointing up towards the end of the decade.

Polight’s cash flow hockey stick for the coming years thus relies on a tripod of endoscopes, scanners, and smartphone cameras. Of these, the latter would be the most critical to achieve, preferably already this year.

In any case, the company will need to raise more cash, either through a share issue (likely) or through debt. If the first half of the year doesn’t provide encouraging news regarding design wins for volume products, the market may begin pricing a 30-40% “issue haircut” into the share price, similar to what happened with another Norwegian tech firm, Nordic Unmanned.

Not a volume product, but heading in that direction. If you guess that OnePlus is behind the smartphone project, you’re likely not far off. More importantly, the technology is starting to make its way into mobile phones too.