The stock market’s utilities sector includes companies providing power generation and distribution, gas distribution, and water supply. (To clarify, waste management belongs to the industrials sector and natural gas producers to the energy sector along with oil companies.)

North American companies in this field don’t have a thread yet, so let’s start one here. This first post focuses on US electric companies, but Canadian and why not Mexican companies in the field, as well as gas and water companies, are also suitable for the thread.

Who wouldn’t want to own beauties like these?? ![]()

![]()

(Photo by Jakub Hałun / Wikimedia Commons)

There are currently 31 sector companies in the S&P 500 index, in addition to smaller companies in the field on the stock exchange. The entire industry accounts for ~5% of US GDP.

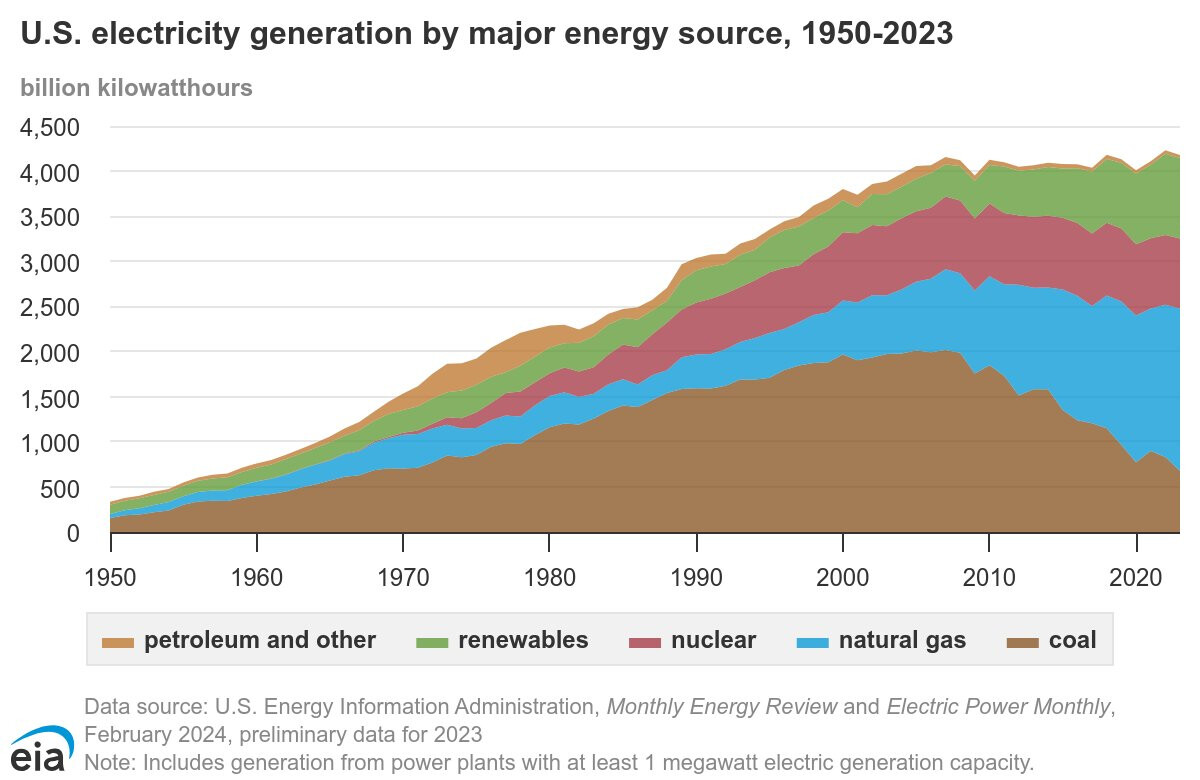

In power generation, the trend in the United States has also been towards reducing CO2, especially by reducing the use of coal.

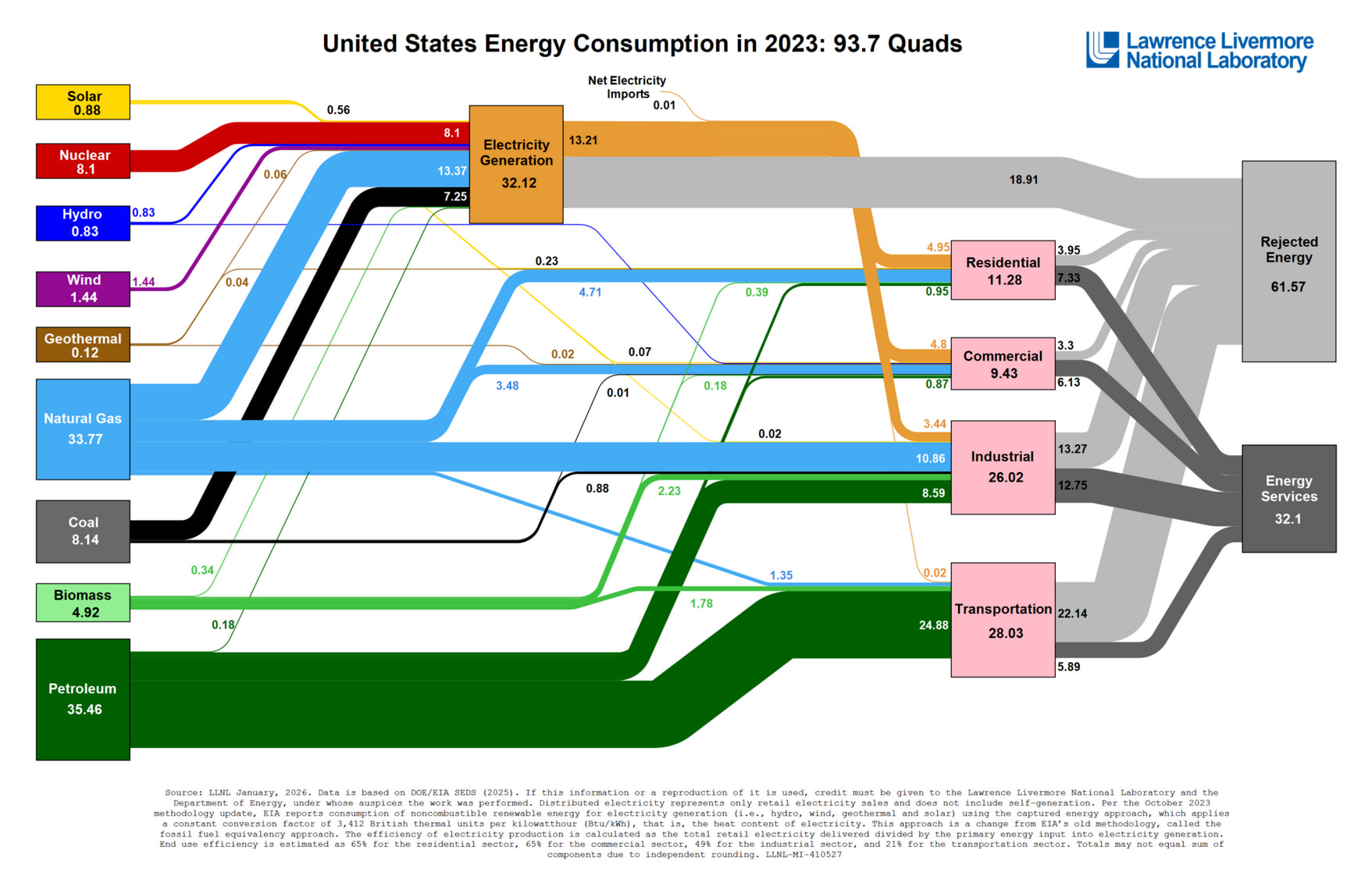

Some companies focus only on electricity or gas, and some have both in their portfolio. Gas is used much more there than in Finland; for example, 47% of residential heating is done with gas.

In terms of distribution, the companies are local monopolies, so they are also regulated; they cannot charge whatever they want. In the wholesale power generation markets, where customers are industrial, regulation is looser. The market includes pure regulated monopolies (e.g., Consolidated Edison, Eversource Energy, and Exelon), electricity wholesalers (e.g., Constellation Energy and Vistra), and companies whose business is a combination of both (e.g., NextEra Energy and Duke Energy).

Investment Profile of the Sector:

In principle, the companies are regulated, capital-intensive defensive companies and stable dividend payers, often being long-term dividend growers. Companies with greater exposure to the wholesale market are more growth-oriented or, on the other hand, more cyclical.

Industry Trends:

The electrification of the economy (heat pumps, electric vehicles) and especially the growing energy demand of data centers are the prevailing trends driving growth in electricity demand. Renewables such as solar and wind, as well as battery storage, are also on the rise. There are major investment needs in power grids and production.

Specific Risks:

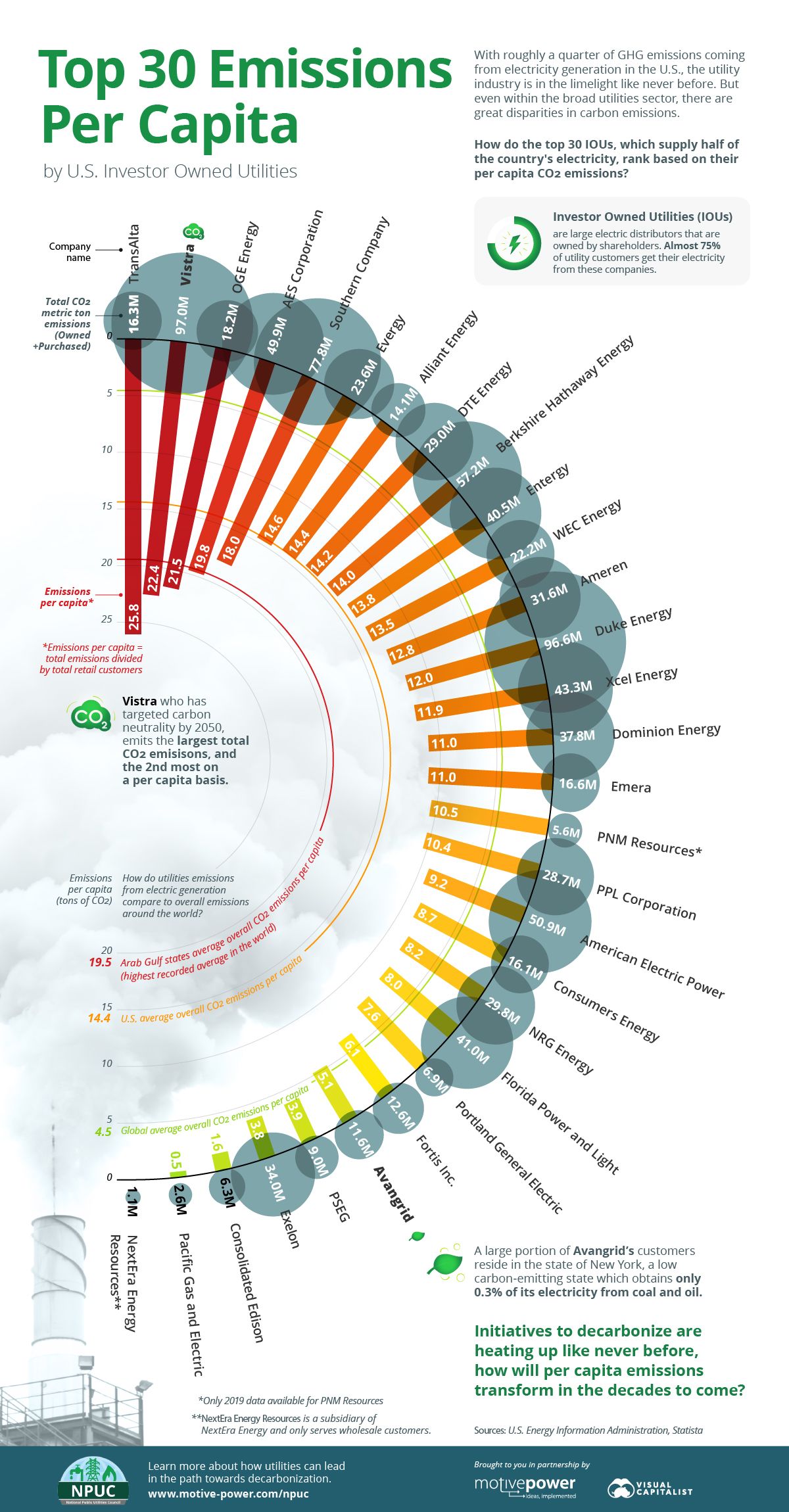

Natural disasters, especially wildfires, are a significant risk for many companies; for example, California-based PG&E has nearly gone bankrupt twice this millennium because it was ordered to pay compensation for damages caused by various wildfires. Similarly, Hawaii-based Hawaiian Electric had to pay $2 billion in compensation for the fire that destroyed the town of Lahaina – nearly half of the company’s pre-fire market value. Edison International, the parent company of Southern California Edison operating in the Los Angeles area, seems to have survived LA’s latest wildfires with just a scare regarding liability, but it also carries risk.

Graphics to Understand the Big Picture:

US Energy Flows:

State-specific charts can be found here: Energy Flow Charts | Flowcharts

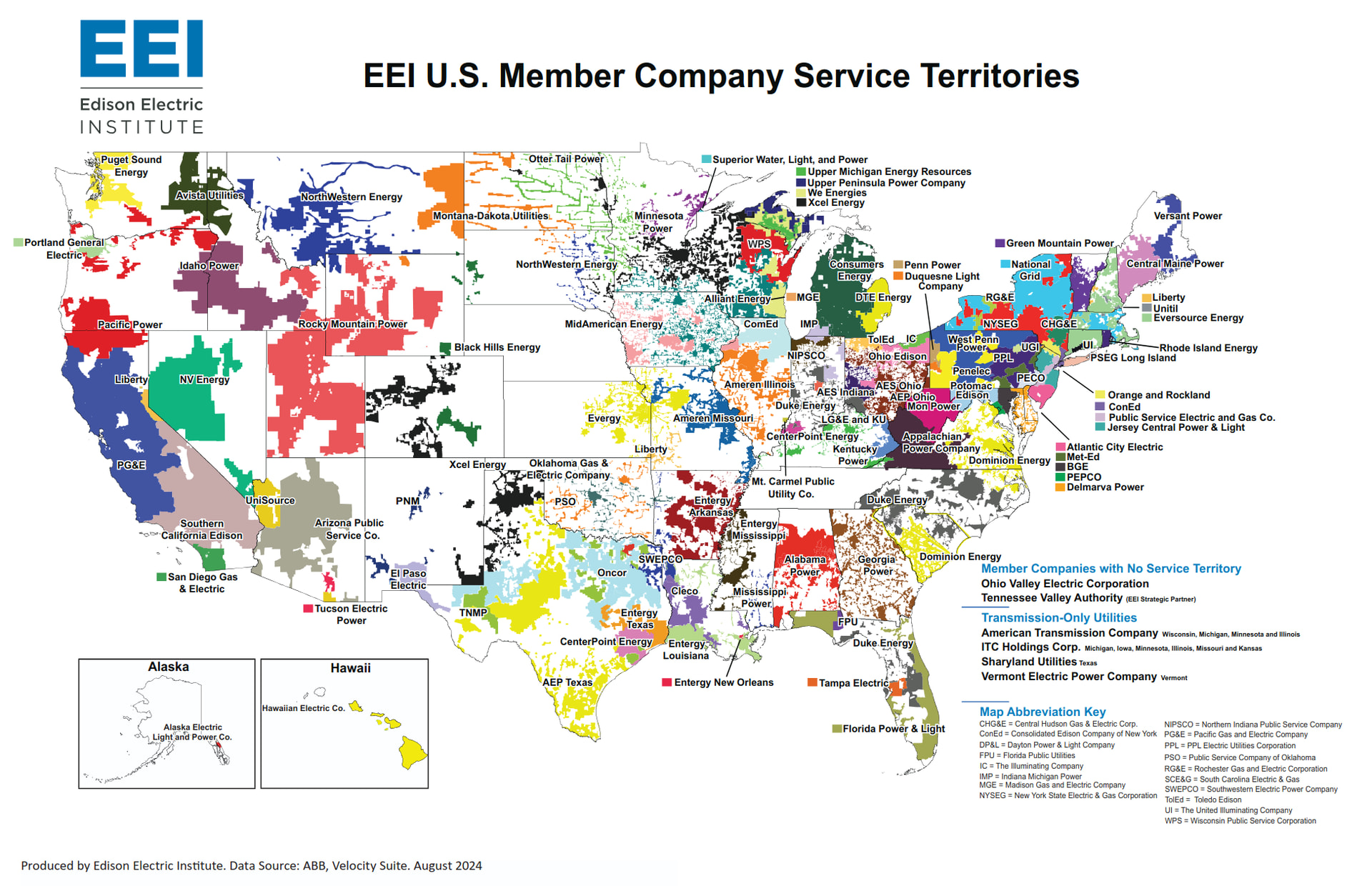

A map where you can see the operating areas of many different companies in the sector (not all are publicly traded, but many that are not directly listed are subsidiaries owned by a listed company):

A graph of CO2 emissions from different electric companies both in total and per customer – there are large differences between companies in terms of climate impact:

The easiest way to invest in the entire sector is through ETFs or other sector funds; e.g., with the iShares S&P 500 Utilities Sector UCITS ETF, but of course, a seasoned stock picker will take a view and select individual companies. My own portfolio currently includes Consolidated Edison and NextEra Energy.

I will post company-specific posts and industry news when I have time, but hopefully others will too!