I have been looking for a new suitable investment target with a focus on Latin and South America. Funds or ETFs would have been an easy option, but now we’re not taking the easy way out – in my familiar style ![]()

I started exploring an asset management company that focuses on alternative investments, real estate, credit, and infrastructure. Patria Investments Ltd is not related to our domestic defense industry namesake in any way, but rather follows in the footsteps of Blackstone, which serves as a major global comparable for its operating model. The target market is just slightly different.

Fortunately, @Verneri_Pulkkinen had already made a suitable summary of Patria, which is well-suited for starting this thread.

I’m boldly quoting the message here as is:

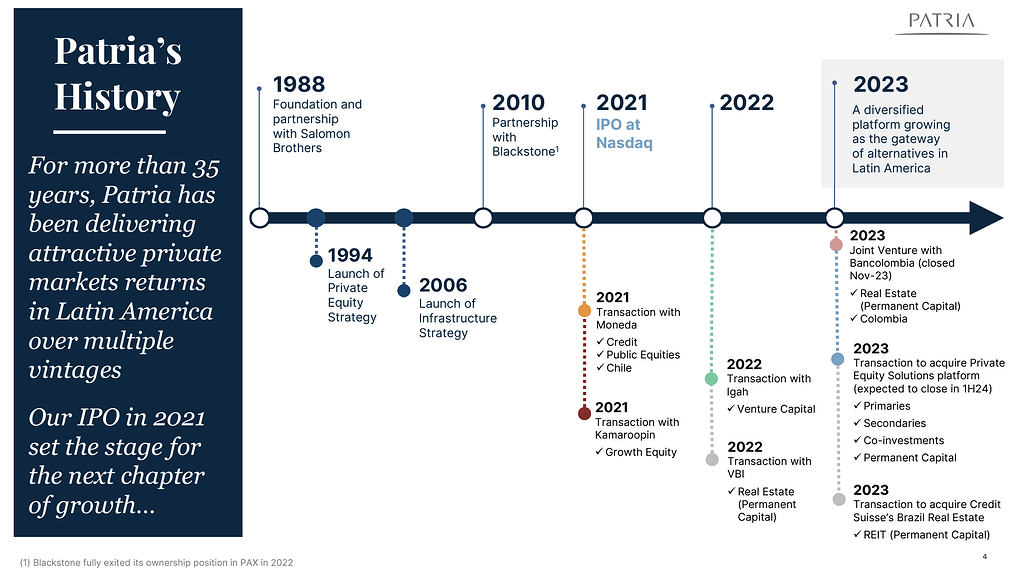

This is indeed a fast-growing asset manager registered in the Cayman Islands, focusing its investments on Latin America. The core team has been working together since the 80s. The company was listed on the stock exchange in 2021. Companies in the Cayman Islands have their own quirky features, such as the total powerlessness of shareholders, a criminally low tax rate, and numbingly long SEC reports. The company has two share classes, so it’s completely pointless for a retail investor to complain to management about anything.

The market capitalization is a good couple of billion. Quickly judged, it seems highly unlikely that this particular company would be among the world’s largest asset managers with a market capitalization of 200 billion. Could this be a 20-billion company someday if strong growth continues? Perhaps.

The company focuses particularly on private equity (entire companies are bought into a fund and developed until they are sold or listed), infrastructure (e.g., hydropower plants are bought), and credit (money is lent to companies).

The company claims to be one of the leading Latin America-focused alternative asset managers, but I’m so numb to the word “leading” that it doesn’t really mean anything.

Asset managers make money by collecting money from investors, charging a percentage of assets under management, and performance fees, simplified. The larger the assets under management (AUM), the better.

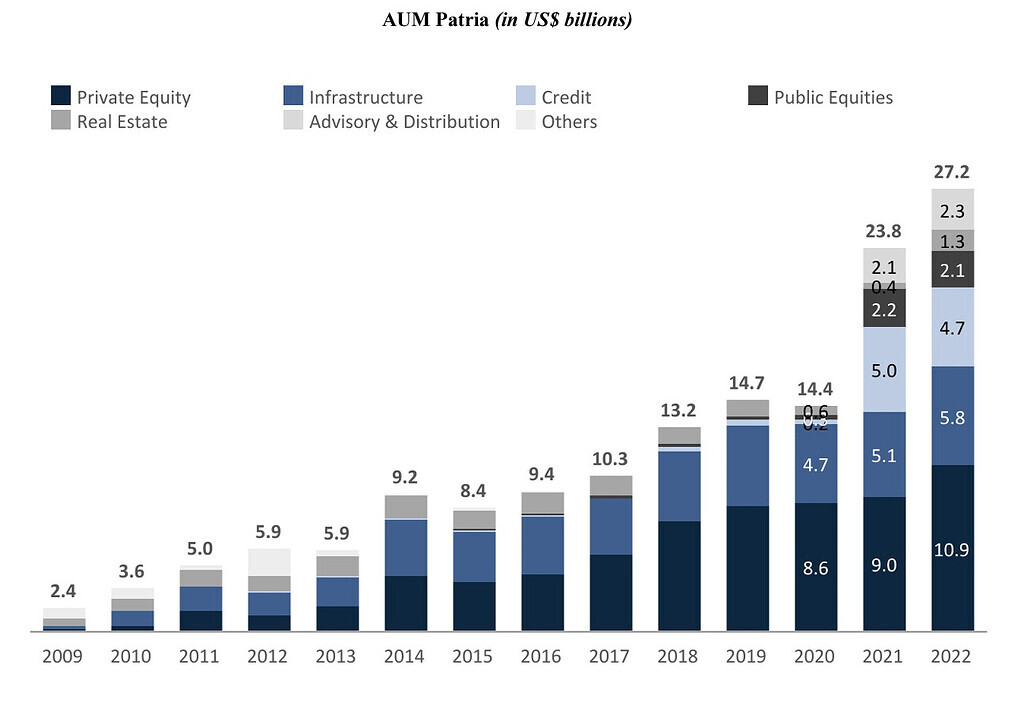

The company’s AUM has grown impressively both organically and through acquisitions, although I haven’t had time or necessarily the skill to assess how profitable the acquisitions have been.

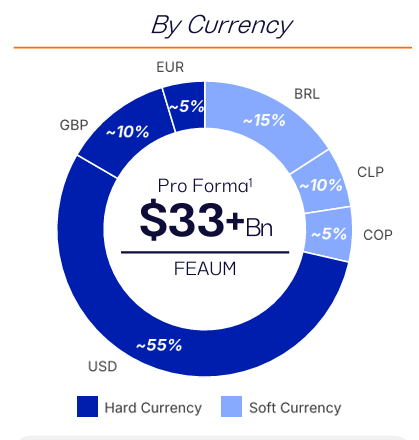

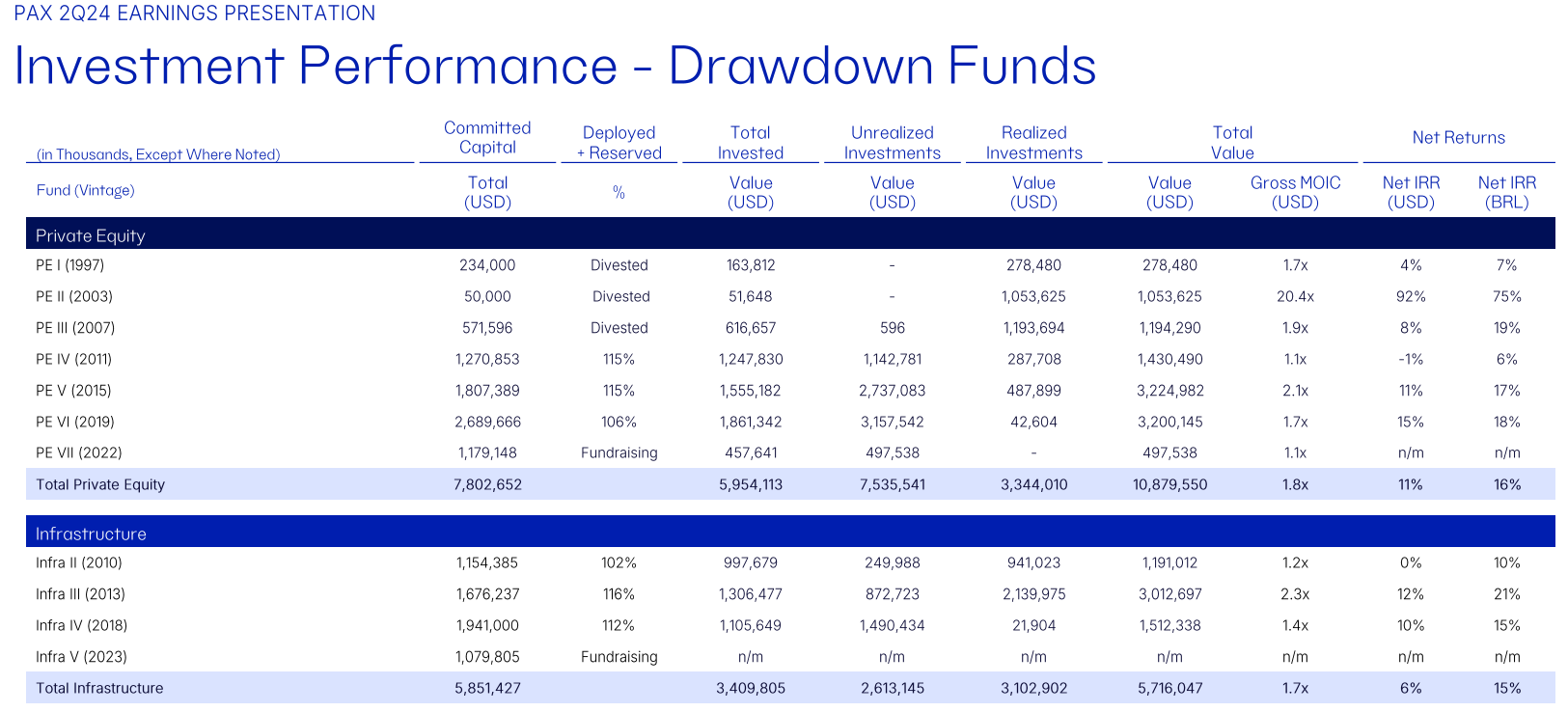

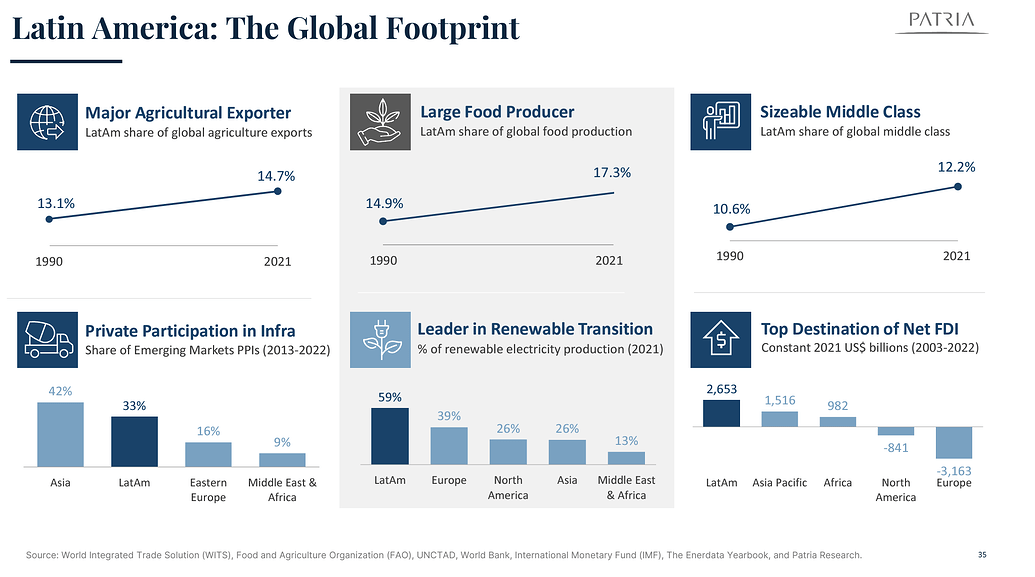

Since investments focus on South America, the continent’s economy plays some kind of role in PAX’s attractiveness. The continent is large and growing, although politically unstable in places. PAX has succeeded in achieving excellent returns there, even when measured in dollars (local currencies are “soft” currencies), but these are no guarantee of future performance.

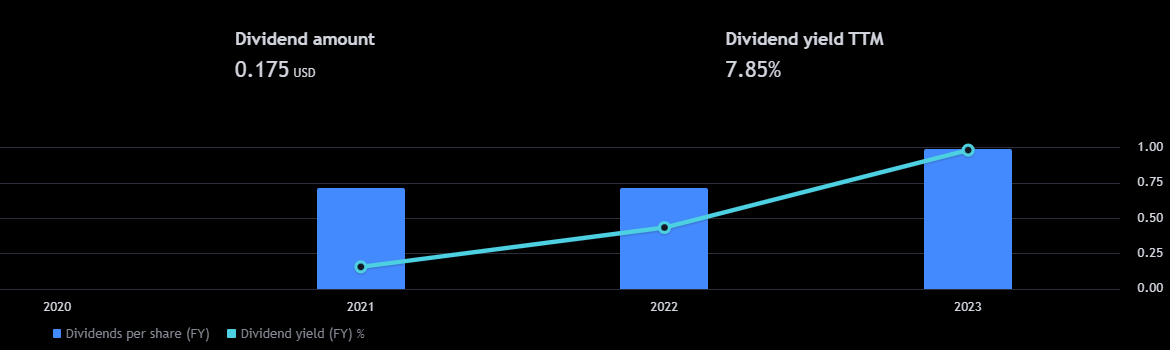

The business model is capital-light when managing others’ assets. Dividend payout ratio 85% of earnings, paid quarterly. Varies significantly, but the upward trend over a few years is pleasing. ![]()

Growth is also sought through inorganic means

A significant real estate portfolio was just acquired in Colombia in July -24

https://ir.patria.com/news-releases/news-release-details/patria-investments-completes-acquisition-nexus-capital-further

PE solutions and management from Aberdeen in April -24

https://ir.patria.com/news-releases/news-release-details/patria-investments-completes-acquisition-private-equity

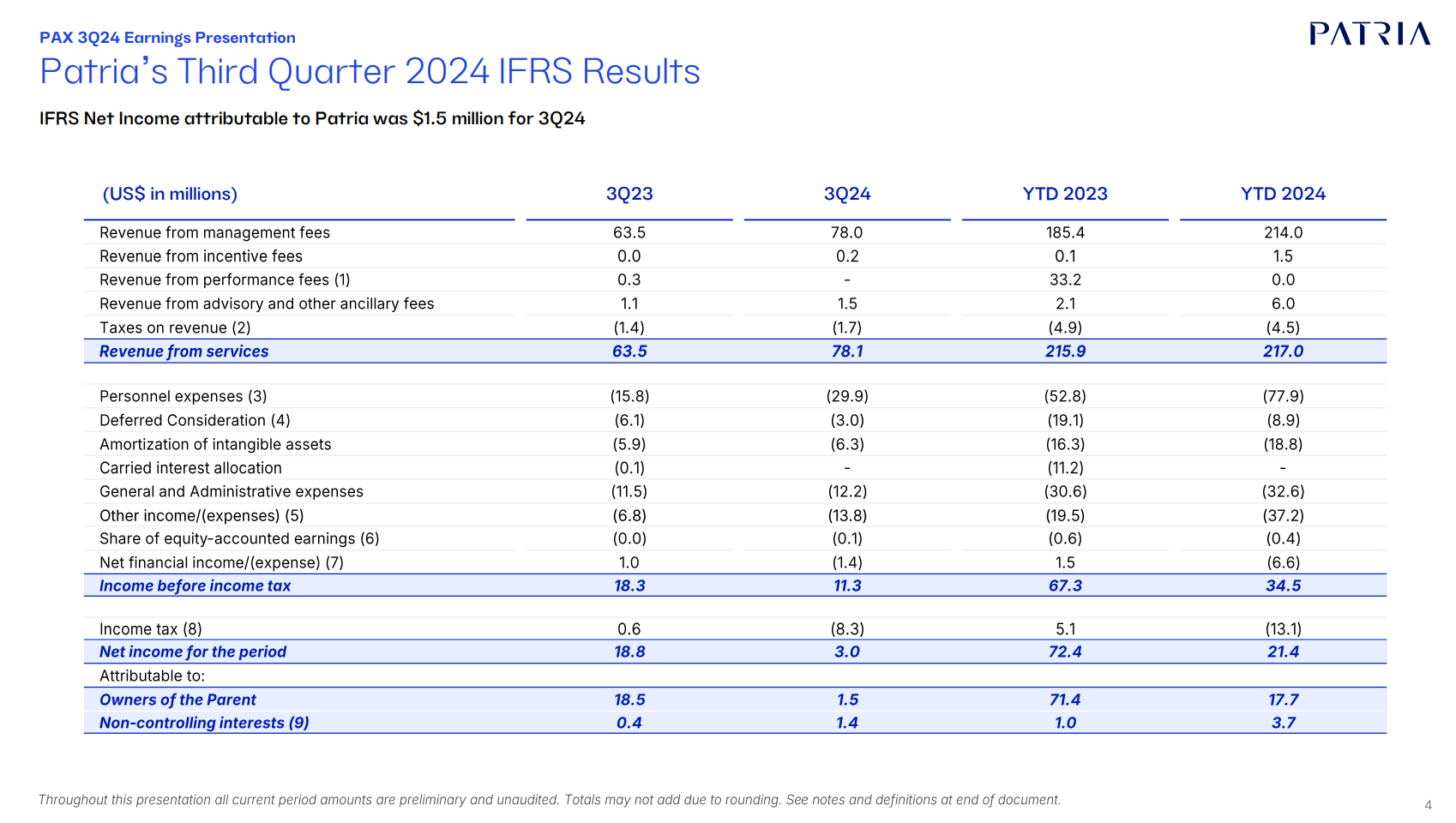

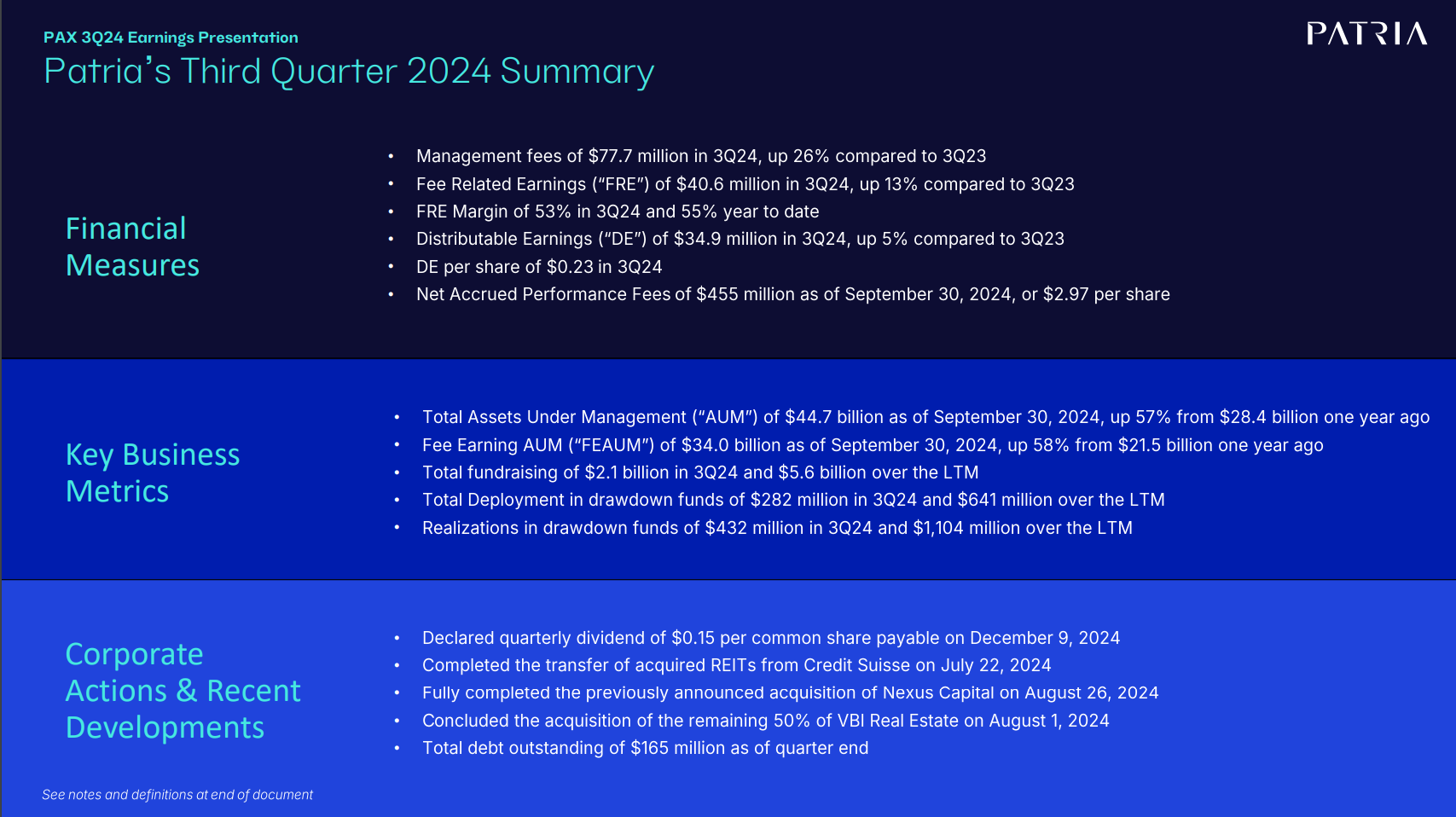

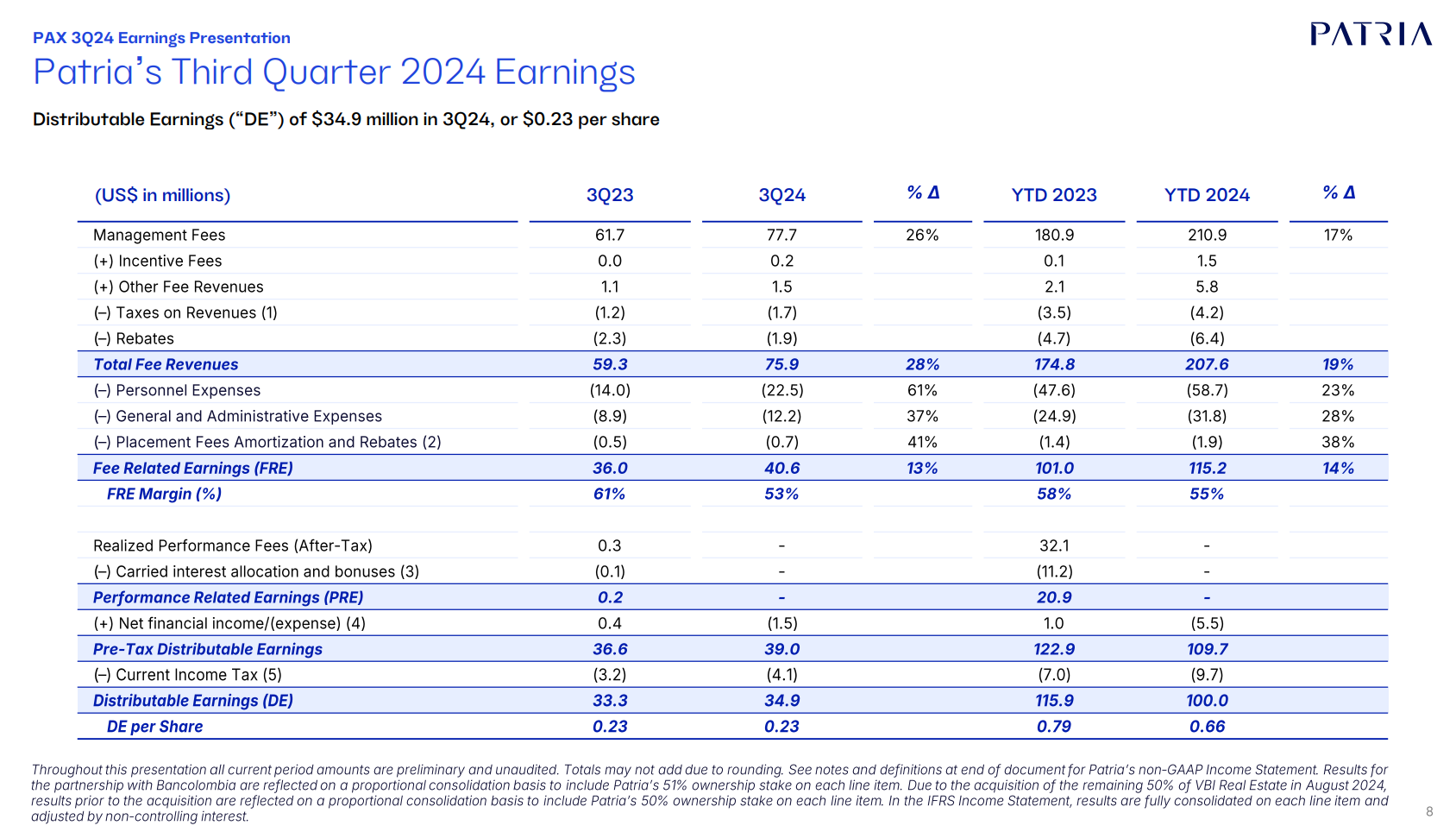

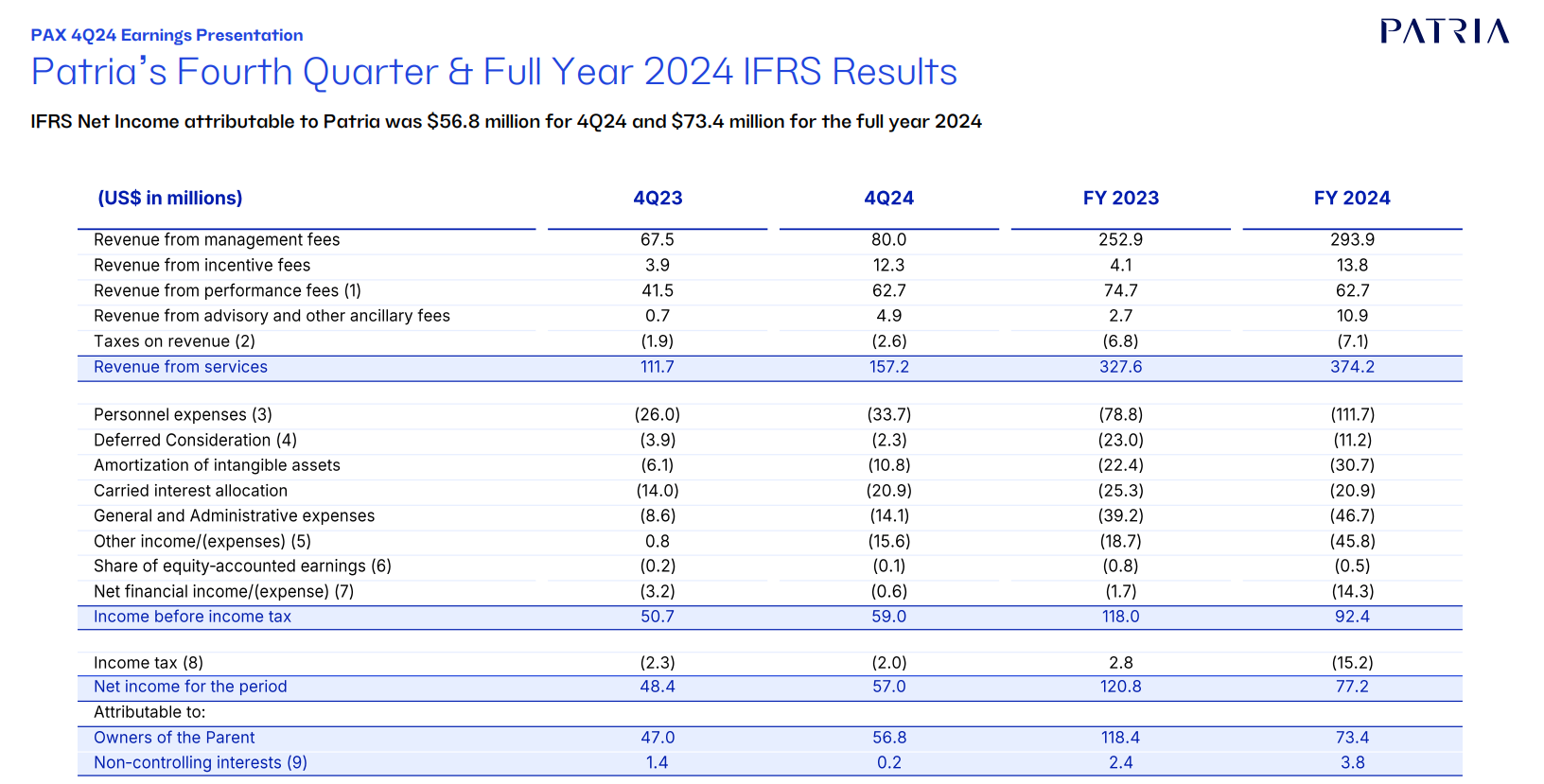

Figures

Q1/2024 investor presentation

https://ir.patria.com/static-files/2e74dc99-329c-4dfe-b3d4-542a0f4a2bb0

and results

https://ir.patria.com/news-releases/news-release-details/patria-reports-first-quarter-2024-earnings-results

And last year’s 2023 results

https://ir.patria.com/news-releases/news-release-details/patria-reports-fourth-quarter-full-year-2023-earnings-results

At least @Nurre and @VasynytKonsulentti seem to have found the company earlier. Welcome to share your views ![]()