That new 100-baggers thread is attracting a lot of interest, and many of us regular guys would surely like to participate in a lighter discussion related to the topic. However, since it’s a thread where the quality is expected to be kept exceptionally high, let’s see if there’s a need for this kind of lighter-level discussion around the subject.

For example, there are surely many kinds of profit-taking strategies, and as was already well-noted in that thread, a sensible approach depends a lot not only on the investor’s personal situation but also on the company’s outlook and valuation multiples.

Proposing this kind of lighter thread around such an interesting topic.

I don’t have the time to delve deeper and write a longer review, but I have Viafin as a candidate. The market is growing at least 5% per year, EV/EBIT is about 6, the track record for growth is excellent, ROIC ~60%, and there are plenty of growth opportunities in Finland as well. Additionally, the company operates in a boring industry and doesn’t interest anyone. If I recall correctly, the company’s revenue is now ~€80M and the target market size is €2,000M.

Great opening! I’m adding this thread to my watchlist. I hope discussion on the topic is also permitted for those of us who don’t have the time to write long essays on the internet.

What are your thoughts on a company’s market cap when hunting for 100-baggers? Literature on the subject has suggested that a company needs to be small enough so that it has room to grow big. Then again, I wonder if it has been statistically studied whether companies with a market cap of, say, 500 million euros have a higher probability of growing 100-fold than those with a 5 billion market cap?

I had to add Patria to my own watchlist as well, although I still prefer BAM. In terms of size, Patria is at a suitable level for growth, and the continent certainly offers good growth, though also risk.

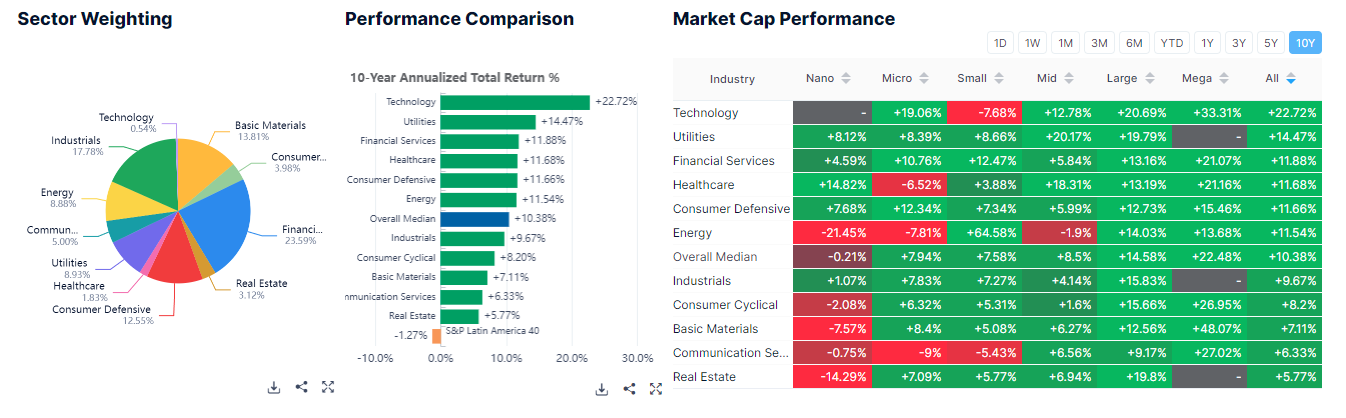

For example, Infra (which I think might partially fall under Utilities?) has performed significantly better over at least the last 10 years compared to, say, the US.

LatAm. performance by sector:

Of course, the past is no guarantee of the future, and stagnant real estate could be the next winners, which Patria also has a small exposure to.

I think in that other thread, the constraint was that the company already has to be listed?

Personally, I think the best chance of hitting a 100-bagger is in unlisted companies that eventually go public and continue to perform well—or are acquired with a significant premium before an IPO. This is where the initial valuation is at its lowest.

You could realistically get into something like this through an early-stage angel investment, for example, or by being one of the first employees at a startup that eventually becomes a huge success.

Of course, the opportunity for this kind of investment (or “investment”) is limited for many and the risks are massive, but then again, the probability of finding a listed stock like that isn’t very high either

Throwing this one out there, in case some more experienced investor than myself has looked into it or would be interested in researching it so we can get some opinions on this company. My own research is still in the early stages and, as is well known, my track record in everything I touch is heavily loss-making, so I don’t dare make any huge claims about the future. However, the revenue growth percentages mentioned in webinars (+60% per year until the end of the decade) got me interested. A small position has been opened and I’m trying to research more to see if there’s reason for systematic additions over time. Comments from more experienced folks would be very welcome.

If some +60% annual growth were to materialize for 10 years, wouldn’t this be pushing for a 100-bagger, at least in theory? Is there, however, some reason why management wouldn’t be able to keep the high growth rates going beyond the end of the decade, and that’s why they only talk about the end of the decade? Or is it just thought that it’s not worth shouting too much about 10 years out or beyond? Or how should these be interpreted? Revenue growth doesn’t end up in the stock price as rising valuations for some reason x?

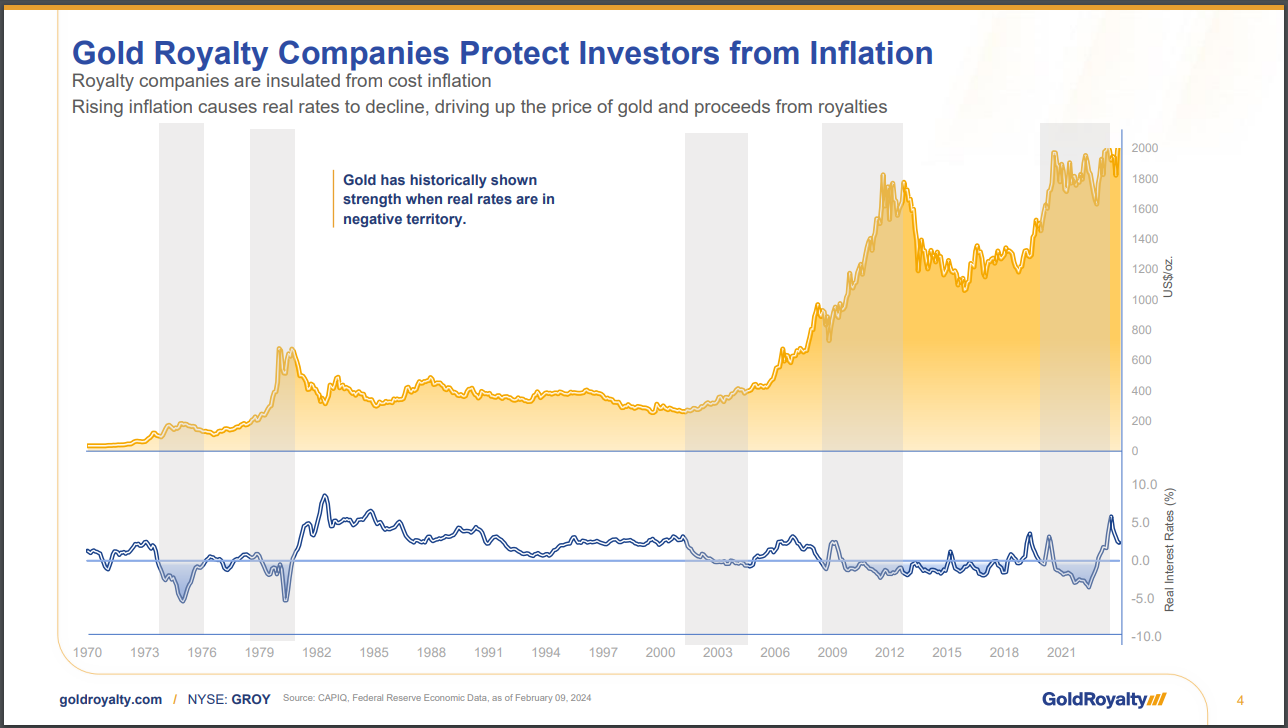

-Gold price near nominal peaks; will future economic turbulence and geopolitical friction drive the price of gold up further? Gold as a safe haven if there is a flight from the dollar?

-How will future moves with interest rates affect the gold price?

-Central banks have been on the buy side regarding gold?

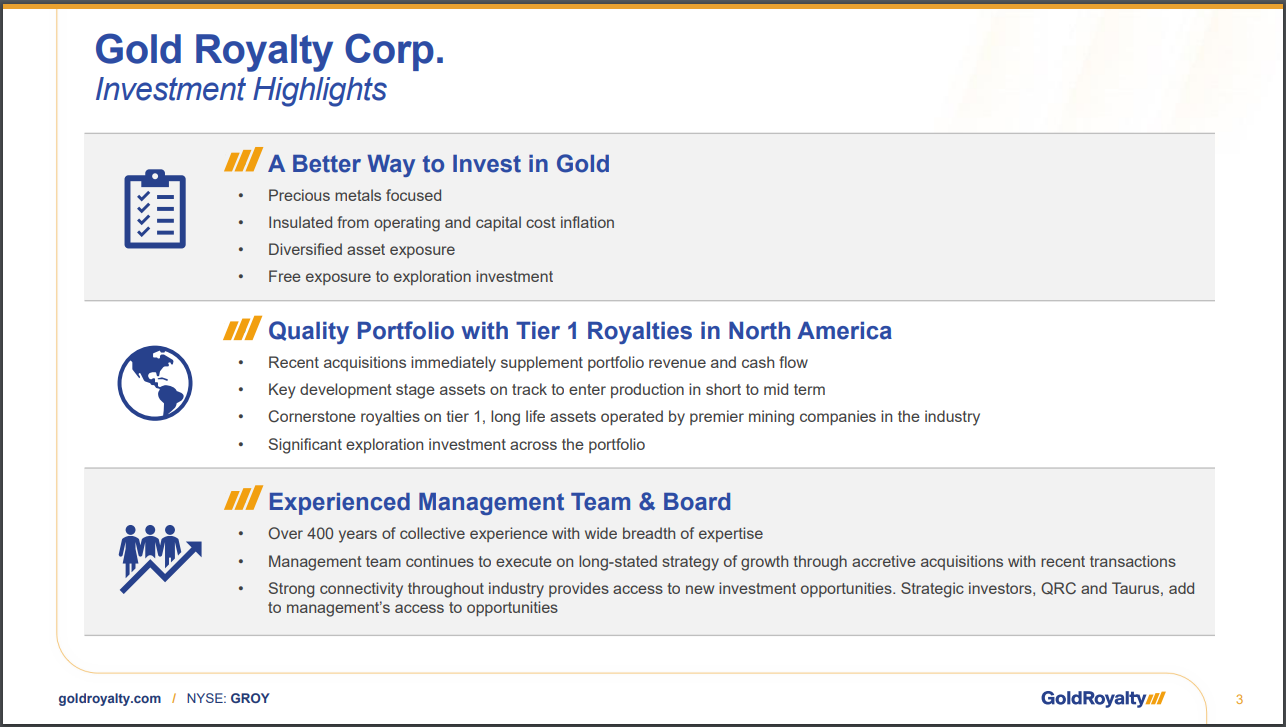

-Management team has a total of over 400 years of experience in the industry

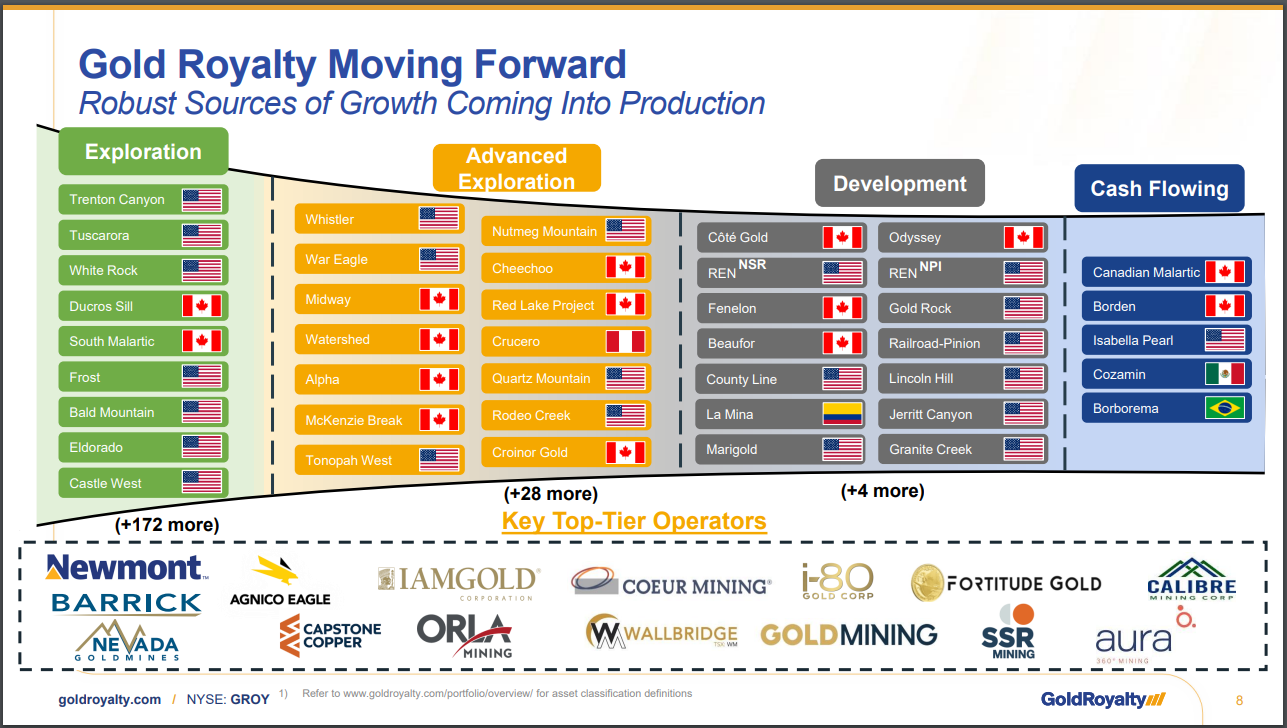

-Gold Royalty is still a small player, plenty of runway left?

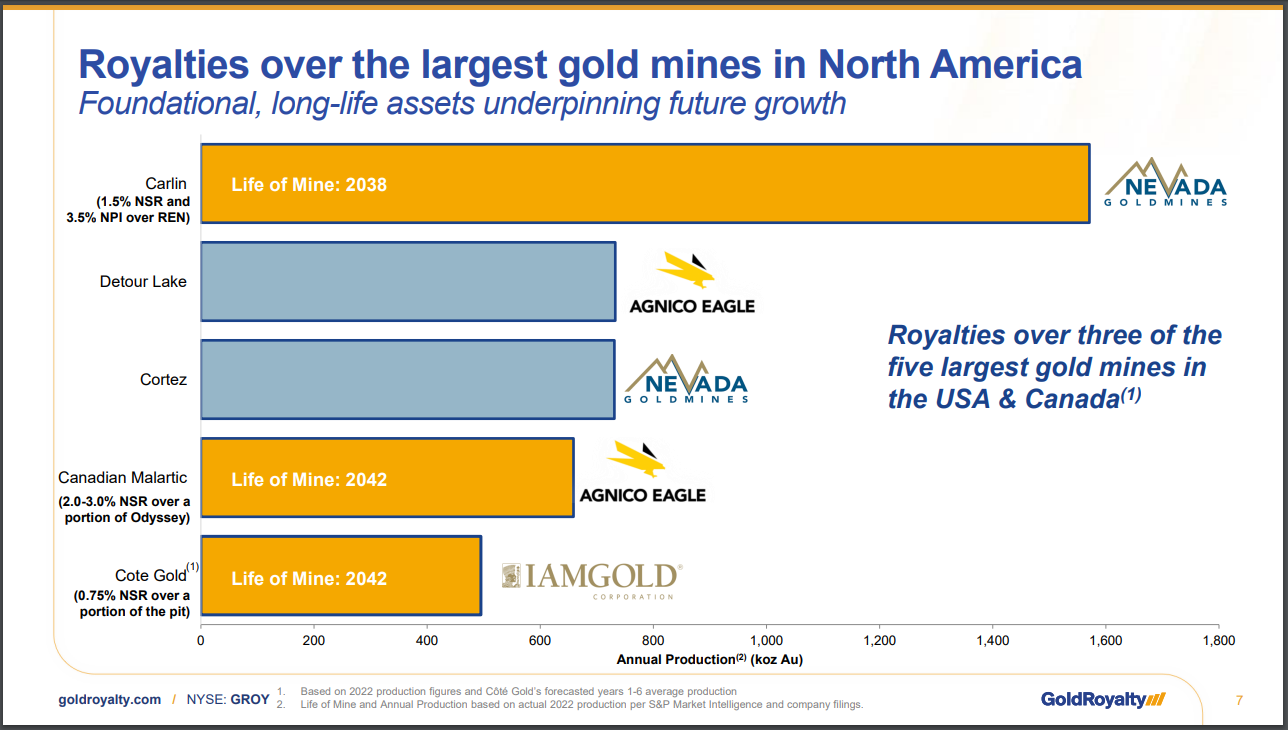

-Royalties in three of Canada’s five largest gold mines, long mine lifespans

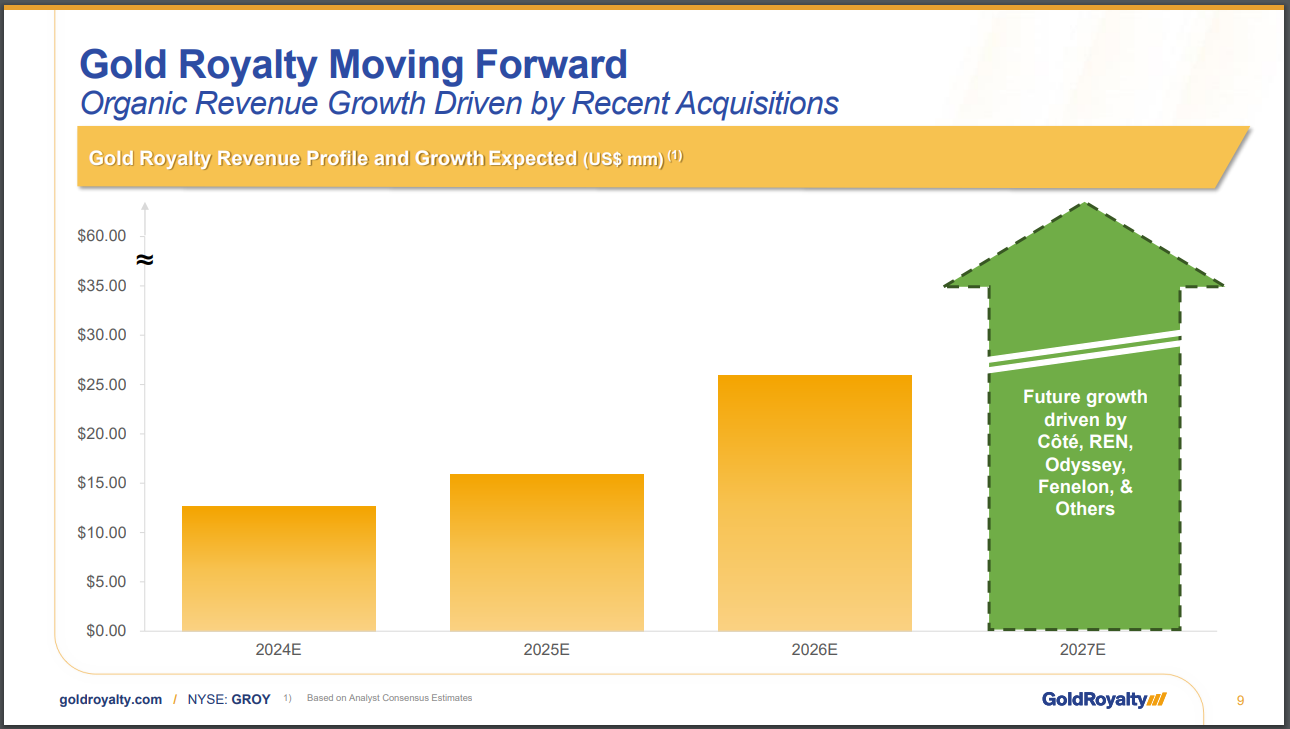

-Mines going into production in the short & medium term, cash flow turning positive

-Once a royalty is acquired, no need to pump more money in

-Risks for a royalty firm are small, as the mines carry the risks. Diversifying risks is easy when spread across multiple sites

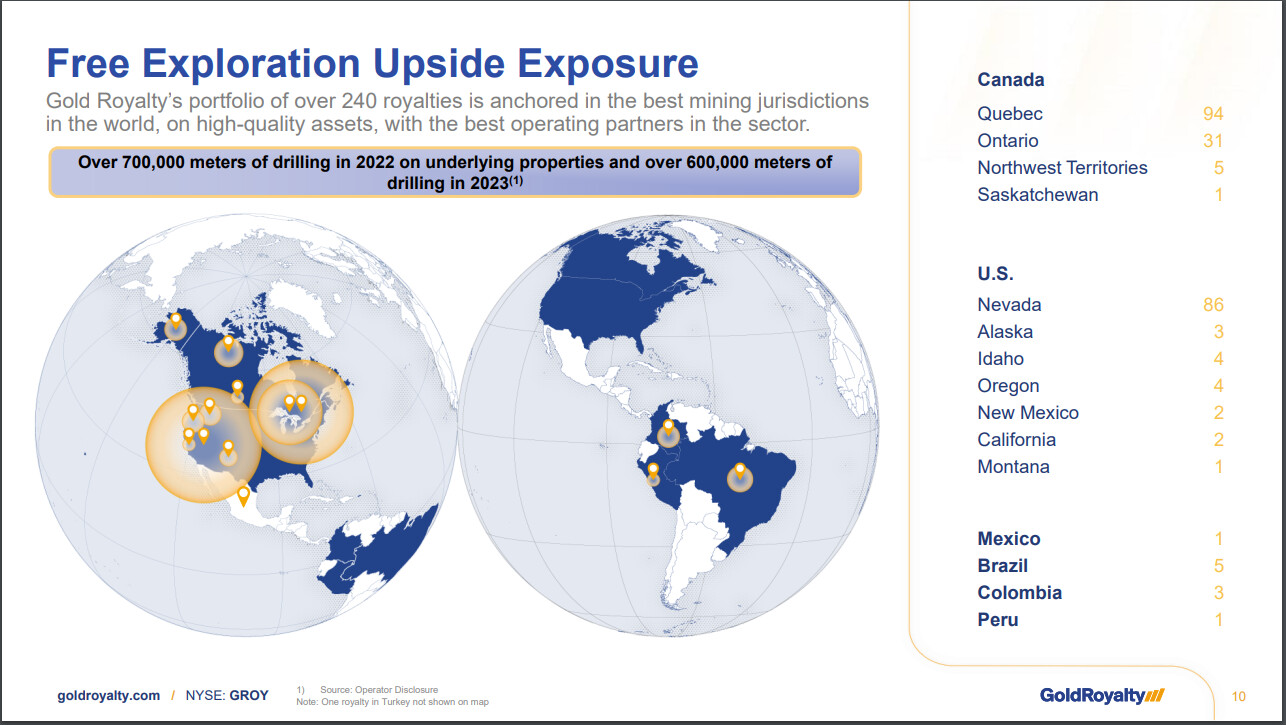

-Gold Royalty currently has about 240 assets in its portfolio. Adding assets (according to the CEO, the number of assets could be e.g. 10x the current amount) wouldn’t increase personnel costs, strong scalability possible?

-Exploration upside without having to invest more yourself

-In the royalty model, there is surely a massive amount of everything I don’t understand. What possible risks should one understand to take into account?

So far, everything is just beautiful and wonderful: others carry all the operational and inflation risk and we investors mostly have to stress about where all the big money coming in can be smartly allocated?

My own expertise is very limited, but if some more experienced person has looked into this or is interested in researching it, I look forward to comments with great interest. What kind of development do you think could be expected from this over a roughly 10-year time frame?

Thank you!

In my own post, my breakdown of the royalty business was a bit lacking, and as it happens, I was tipped off in the Coffee Room this morning that Jackfin had recently explained this well in another thread.

Many mines seem to be located on the Canada/USA axis, but how do royalties flow geographically?

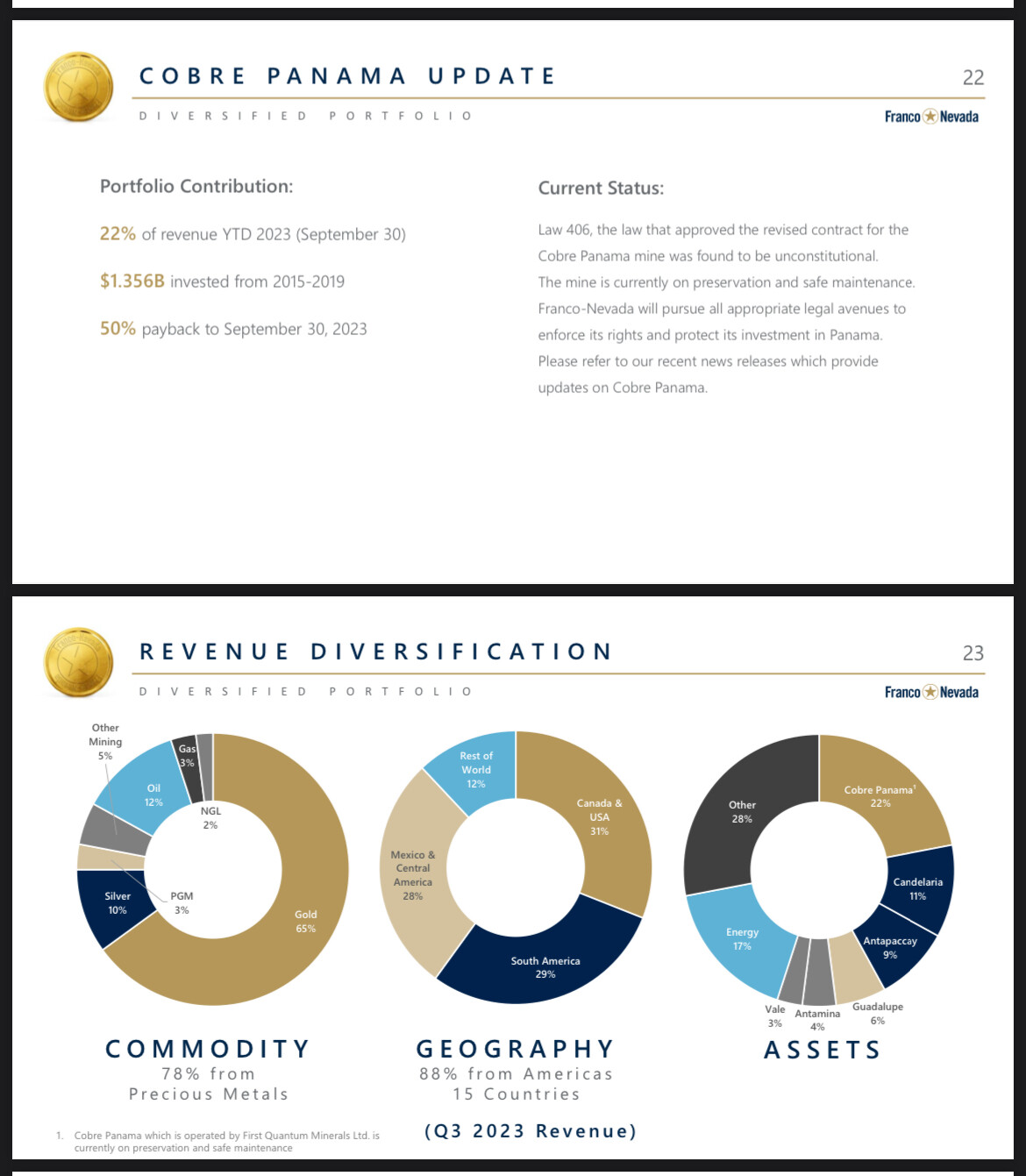

The king of royalty companies, Franco-Nevada, softened nicely on the stock market when a fifth of its assets were apparently frozen in Panama.

One risk with these is also that despite the investments, the mines do not achieve a sensible production volume (from which royalties/streams are derived) and they have to be funded more and more continuously.

The business idea in these is ingenious and at its best really cash-flow rich, as a small office staff can indeed manage hundreds of investments in different mines. On the other hand, they also have to pump that cash flow into developing the mines.

There are five projects currently marked in the “Cash flowing” category. Of these, two are in Canada, one in the USA, one in Brazil, and one in Mexico. So, at this stage, the diversification is still relatively okay, but looking further ahead at the projects, the weight of the USA and Canada is indeed heavy—there’s no getting around it. There’s probably some degree of political risk in all of these. Even though mining company salesmen always advertise that they are in the best possible area regarding permitting etc., difficulties can arise everywhere.

As some wise person once said, “it doesn’t matter if someone steals my money with the strike of a gavel in Canada or with an AK-47 in the jungle.”

That’s exactly what sparked my interest, but unfortunately, my competence isn’t sufficient yet to evaluate these well enough. You learn by doing, but I’m afraid the company will reach the end of its lifecycle before I’ve learned enough. So, getting in “early” with a small stake so I don’t miss the train entirely if it’s a good case, and meanwhile continuing to research and learn to see if there would be reason for those additions.

As I understand it, there wouldn’t be an actual obligation for additional funding; rather, it’s the mining company’s job to figure it out. Of course, one could probably negotiate more money for an extra slice of royalties. A running mine would certainly be in the interest of all parties.

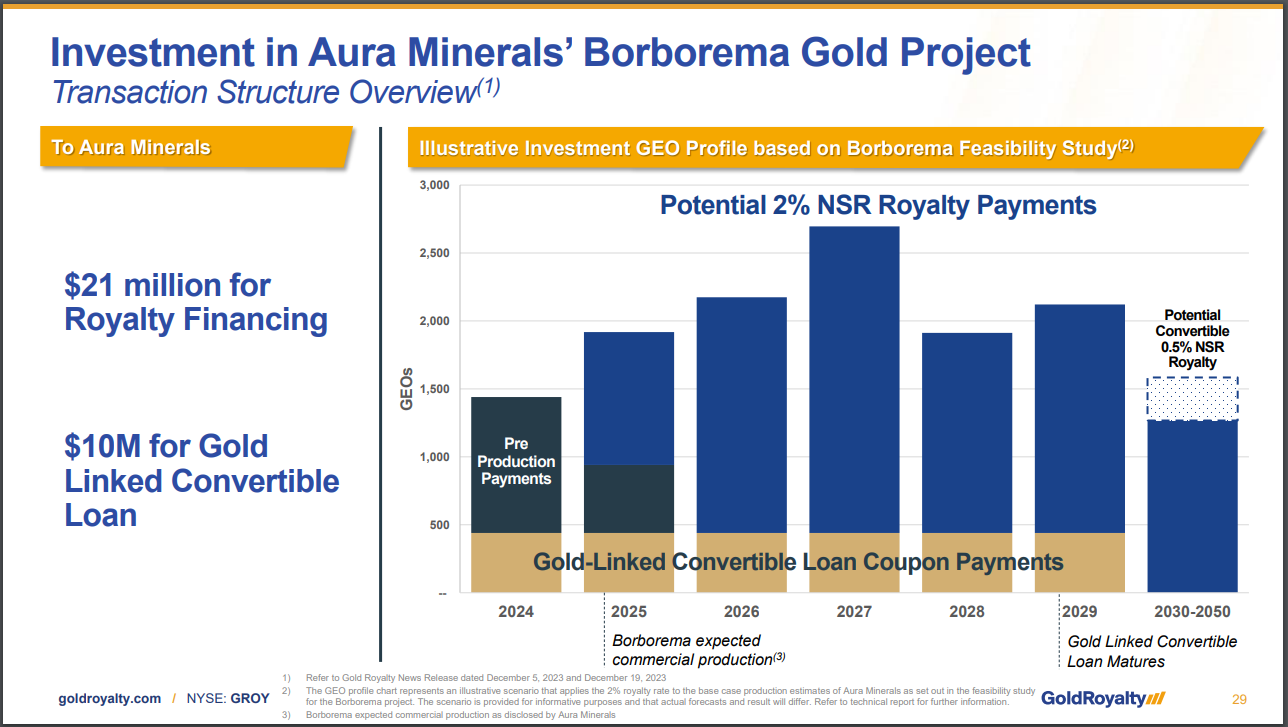

At least in the case of the Borborema mine (Brazil, apparently entering production in early 2025), there was a contract for pre-production payments, which apparently roll in while waiting for production to start. From other projects, I didn’t find similar ones with a quick glance, but hopefully they’ll realize to include those in future projects as well.

This is still a small shop and the current revenues are peanuts, but I’m following with interest how the story starts to progress.

I’m completely the wrong person to discuss this in more detail, as I’m still figuring out the basics, but hopefully some more experienced person will get excited enough to participate and help me understand these better.

Here is the table of contents with timestamps so you can pick out the highlights:

I tried to look into whether any negative characteristics of the business would immediately come to mind or crop up. None did, so it likely requires and deserves a deeper look. As one essential factor, I would perhaps see what is done with the available funds when there are cash-flow-generating mines (current + potential future ones). In other words, are the cash flows returned to shareholders or are they constantly reinvested into new projects (which some might consider a good thing, but it’s well known that the success rate of mining projects isn’t staggering, as there are many ways things can go south, especially with small companies). At least upon a quick glance, I didn’t spot any mention of the capital return policy in the presentation? So the idea is to compound investor funds in the spirit of this thread? A potentially challenging industry for that, or at least you need to have quite a bit of trust in the management

Thanks! I’ll have to give that a listen this evening.

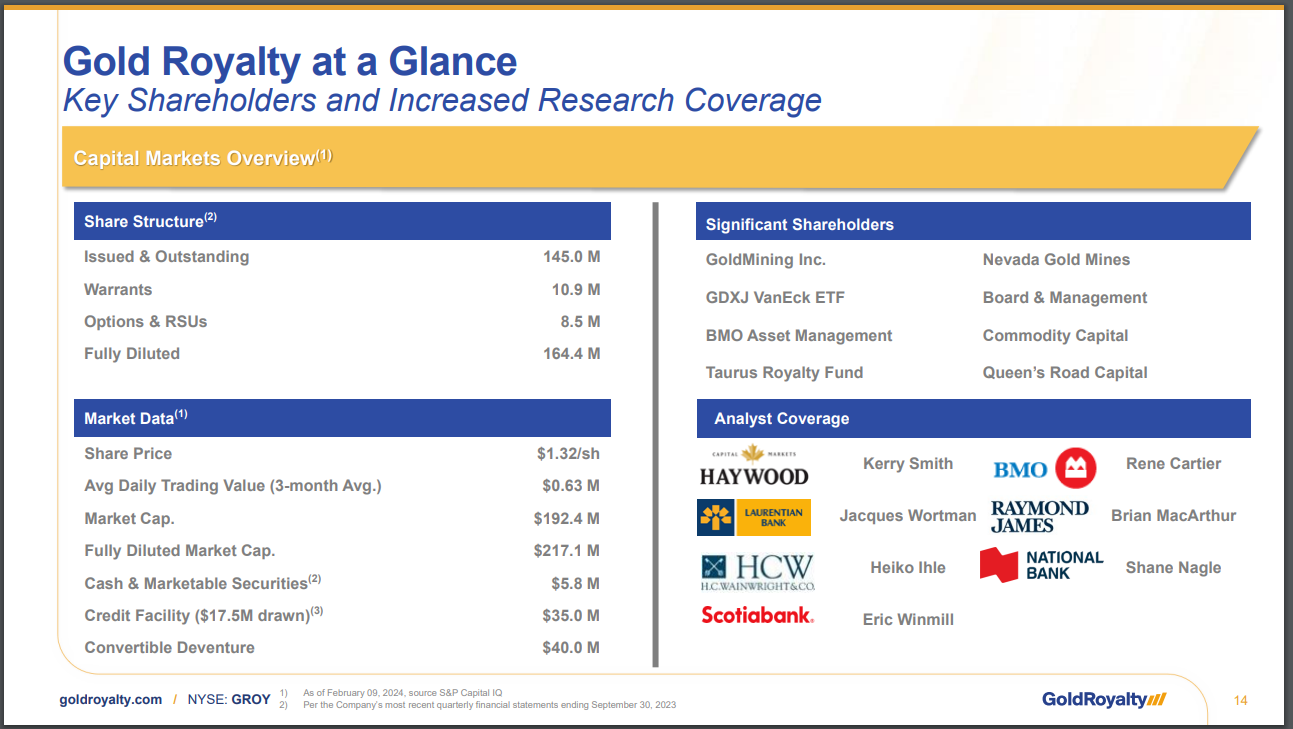

Currently, it seems to be paying a dividend of around 2%, which I see as a bit unnecessary during this hopefully aggressive growth phase, as capital is constantly needed for further growth.

I don’t recall any good questions on the topic being asked in the webinars yet, but then again, I’m in the middle of a cycle of illnesses with the kids, recovering myself as well, and in such a constant state of sleep deprivation that I have to listen to everything 2-4 times for anything to stick.

Let’s throw this out there since NCI.V operates in the boring IT sector. It is making about 2.5m in net profit this year and the market cap is currently 8m. If we wanted this to 100x with the same share count, then the profit would need to be 28m and the P/E would be around 30 => mc 840m / 205 = 4.09 CAD; the price has currently been hovering around $0.04-$0.05.

So, it is not an impossible task for the stock to 100x in the future. Especially since profit growth has been 62% in 2023 vs 2022.

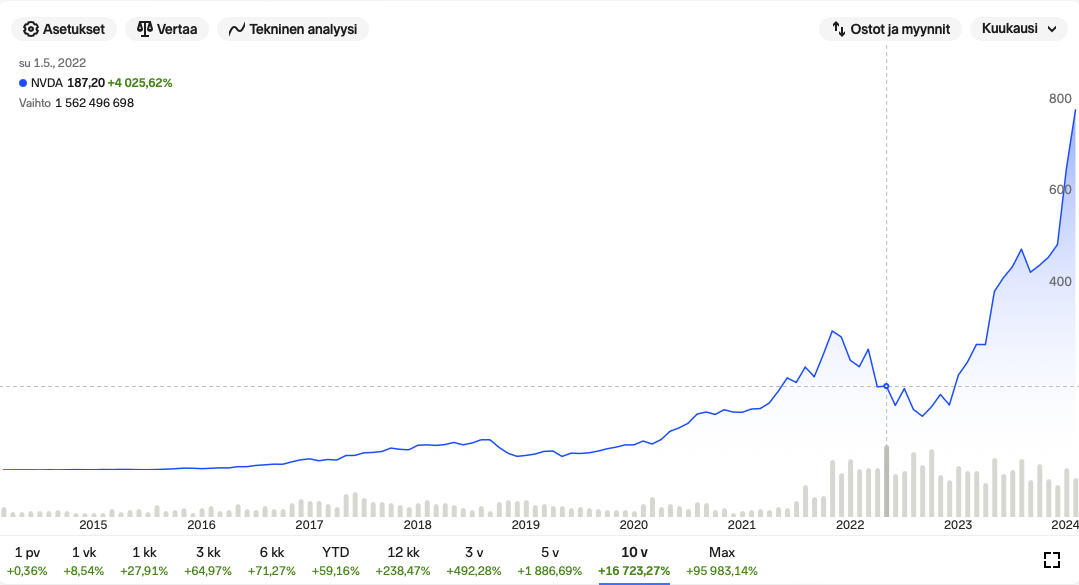

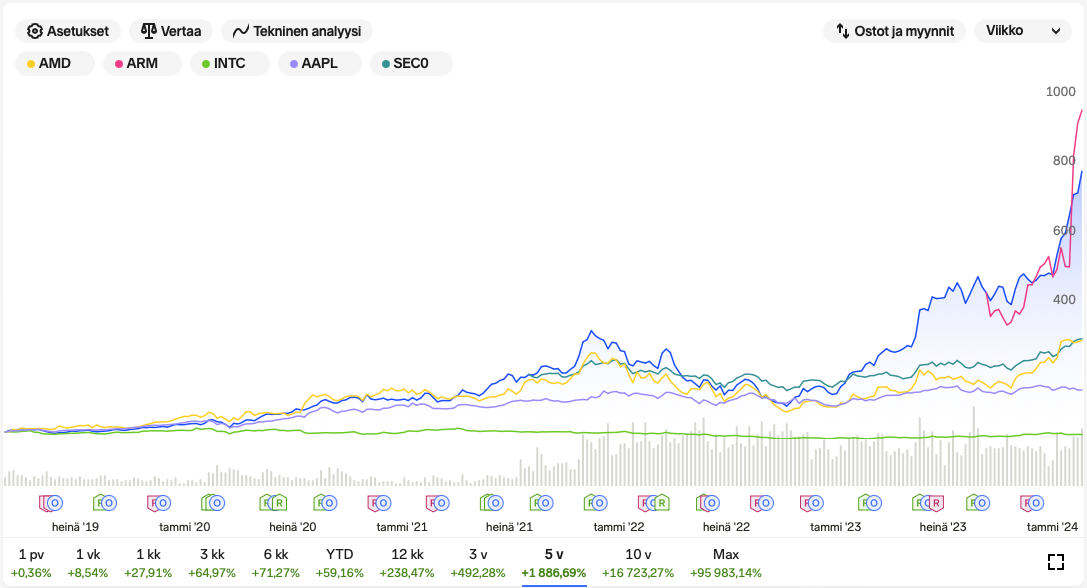

Since I don’t feel this belongs in the main thread, I’ll leave it here. It seems the most recent 10-year 100-bagger is Nvidia. A 167-fold increase over 10 years, and a 19-fold increase over 5 years.

But is Nvidia low risk? Well, there hasn’t been a risk of losing all invested capital since 1997, but instead, over the last 10 years, there have been two periods where a poorly timed investment and weak nerves could have halved the invested capital in a very short time.

But even more importantly, all three of Nvidia’s surges (2016–2018, 2019–2021, and 2022–present) have been largely the result of external factors and luck, not just the company’s own actions. Of course, the products have been good and R&D has worked, but the company likely didn’t predict that Bitcoin mining would rip all GPUs off the market, and even though they already had a strong position in the world of machine learning computation, the AI hype caused by ChatGPT has been a windfall for them in a way that only ARM is comparable to (and there isn’t much of a track record to show for that).

If an investment strategy is based on timing factors external to the target company, it’s quite hard to call it risk-free.