What kind of effect do exchange rates have on business? The company now operates in several countries, but I guess the recent strengthening of the real can be seen as a positive sign.

1 Like

It is constantly moving more into hard currencies, and is already mostly in them.

However, for example, the strengthening of the USD will likely make Q1 challenging in terms of results, even if the business otherwise progresses as expected.

5 Likes

Real’s share is apparently so small that price changes don’t significantly affect the business anymore.

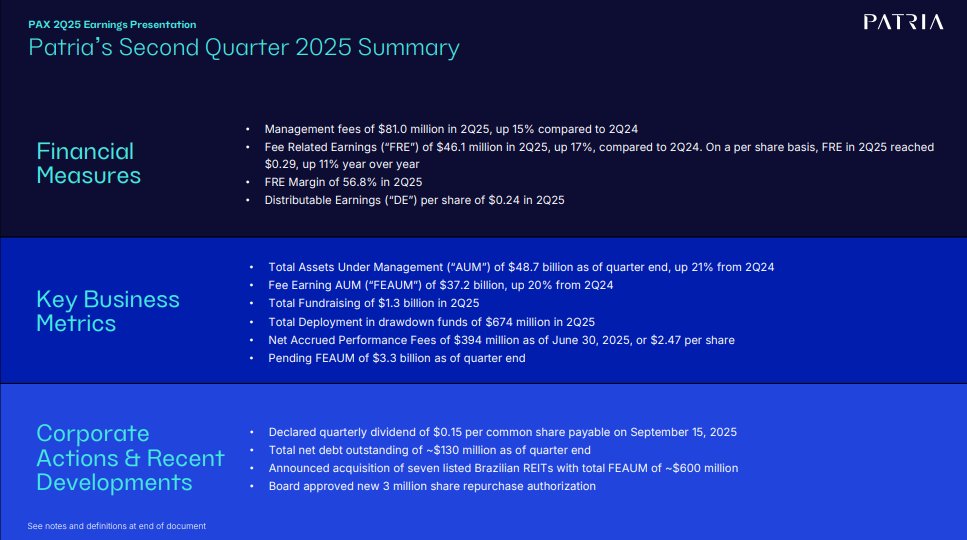

Alex Saigh, Patria’s CEO, said: “Patria is off to a very exciting start to 2025 as fundraising totaled a record $3.2 billion, highlighting the expanded reach of our investment platforms and distribution capabilities, and putting us in a strong position to achieve our $6 billion fundraising target for the year. We also reported 1Q25 FRE of $42.6 million, or $0.27 per share, representing year-over-year growth of 21% and 16%, respectively, despite the volatility in the region. Also, FEAUM grew 6% sequentially and 46% year-over-year, and we generated over $700 million of organic net inflows, reflecting an annualized organic growth rate of 9%. While a looming trade war and rising global economic concerns create potential headwinds, we believe we are well positioned to generate the $200 to $225 million of FRE we are targeting for 2025 as the increased diversification of our platform is paying off in terms of fundraising and profitable organic growth, enhancing our confidence in the three-year targets we introduced at our Investor Day back on December 9 th*.”*

Financial Highlights (reported in $ USD)

IFRS results included $13.6 million of net income attributable to Patria in Q1 2025. Patria generated Fee Related Earnings of $42.6 million in Q1 2025, up 21% from $35.1 million in Q1 2024, with an FRE margin of 55.1%. Distributable Earnings were $36.8 million for Q1 2025, or $0.23 per share.

Well, that doesn’t look too bad again. Good growth and the guidance for the current year was reiterated. The shares of these Latin American firms don’t really move anywhere. Usually down ![]()

10 Likes

Approximately 10% AUM increase in real estate management.

https://ir.patria.com/node/8281/html#dp229056_ex9901.htm

Patria Investments Signs Agreement Involving Six Real Estate Funds from Genial Investimentos

Transaction reinforces leadership in the Brazilian REIT market and enhances portfolio diversification. With this transaction, Patria’s Real Estate division in Brazil adds approximately R$ 2.5 billion in AUM, reaching a total of R$ 26 billion.

May 30, 2025 – Patria Investments, a leading alternative asset manager in Latin America, announces the signing of an agreement for the transfer of portfolio management of six real estate investment funds (FIIs) from Genial Investimentos. This transaction is part of Patria’s broader strategy to expand and diversify its Real Estate portfolio. Completion of the transaction is subject to approval by Brazilian’s antitrust authority (CADE) and the respective investors’ assembly of the FIIs.

While the financial terms of the transaction will not be disclosed, upon completion, approximately R$ 2.5 billion in assets under management will be added to Patria’s Real Estate portfolio, bringing the total to around R$ 26 billion. This further consolidates Patria’s leadership among independent REIT managers in Brazil, with three of the largest funds in their respective segments: HGLG (logistics), PVBI (offices), and HGRU (urban income), as well as some of the top-performing funds in the credit and securities segments (CVBI, HGCR, and RVBI).

Upon satisfaction of the closing conditions, Patria’s subsidiaries will assume management of the funds. The six funds involved, which collectively have nearly 190,000 unitholders, are: MALL11 (shopping centers), BPFF11 (fund of funds), PLCR11 (CRIs), SPTW11 (offices), GLOG11 (logistics), and PLCA11 (CRAs).

“This is an important step that further strengthens Patria’s REIT portfolio, which is already one of the largest and most diversified in the country—especially following the acquisitions of VBI’s and CSHG’s real estate businesses. This transaction consolidates Patria’s leadership and expands the range of attractive investment opportunities, while continuing to deliver consistent returns to our investors” said Rodrigo Abbud, Partner and Head of Real Estate at Patria Investments in Brazil.

Patria’s Real Estate portfolio currently includes 18 FIIs listed on B3 and 2 FIIs traded over-the-counter, operating across key market segments such as logistics, offices, urban income, credit, and securities. By strengthening its presence in strategic sectors and increasing portfolio diversification, Patria positions itself as a compelling platform for investors. At the same time, the ongoing consolidation of the REIT market contributes to the professionalization of the industry, raising management standards and benefiting both unitholders and tenants.

10 Likes

Patria is among the bidders for Banmedica, a LatAm region operator being sold by United Health ($UNH)

Banmedica’s EBITDA is around $200M, estimated transaction price $1Bn

The company has four non-binding bids for its Banmedica subsidiary, which operates in Colombia and Chile, for about $1 billion, according to both people, who asked not to be identified because the talks are private.

UnitedHealth’s shares tumbled 25.5% in May alone and year-to-date are down 40%. UnitedHealth left Brazil in 2023 and Peru in March. It is aiming to get around $1 billion for Banmedica’s operations in Colombia and Chile, the people said.

The two people said the company expects to set a deadline for binding proposals as soon as July.

UnitedHealth received bids from Washington, D.C.-based private equity firm Acon Investments; Sao Paulo-based private equity firm Patria Investments (PAX.O), opens new tab; Texas non-profit health firm Christus Health; and Lima-based healthcare and insurance provider Auna (GZ4.F), opens new tab, the people said. Auna is in talks with a financial partner, one of the sources added.

Patria, UnitedHealth Group and Christus Health declined to comment. Acon and Auna did not respond to requests for comment.

Additionally, the latest investor presentation has been published, so there’s more reading again ![]()

https://ir.patria.com/static-files/afe069aa-87ad-432c-82c6-278c909f554a

7 Likes

Q2 figures look good to my eye, and additionally, the fundraising target for the rest of the year was raised by 5-10% from the original 6 billion. Regarding FRE, the guidance was kept at 200-225 million for the year.

11 Likes

This still looks good ![]()

Financial Highlights (reported in $ USD)IFRS results included $22.5 million of net income attributable to Patria in Q3 2025. Patria generated Fee Related Earnings of $49.5 million in Q3 2025, up 22% from $40.6 million in Q3 2024, with an FRE margin of 58.5%. Distributable Earnings were $46.9 million for Q3 2025, or $0.30 per share, up 31% from $0.23 in Q3 2024.

Dividends

Patria declared a quarterly dividend of $0.15 per share to record holders of common stock at the close of business on November 14th, 2025. This dividend will be paid on December 12th, 2025.

and Q3 investor presentation:

https://ir.patria.com/static-files/36eb4673-6649-48c5-9b80-deb1a25905ae

12 Likes

And they also announced they would pay a dividend of 0.65 dollars per share next year, an 8.33% annual increase. I’ll take it.

5 Likes

There was some good information available in the investor call. The recent weakening of the dollar is seen as a positive, as investors have historically turned their attention to emerging markets. Of course, a lot of other things are happening in the markets now, so it remains to be seen which way things will go.

Fee earnings are expected to continue growing in 2026, reaching approximately $1.42 - $1.54 per share. This, of course, is in addition to potential performance-based fees and such, which should come in quite nicely.

It has risen somewhat, but the stock is not very expensive compared to its peers, at least if the share price is around a good 10X fee earnings.

10 Likes

Significantly more corporate loan market share ![]()

I couldn’t find any mention of the acquisition price ![]()

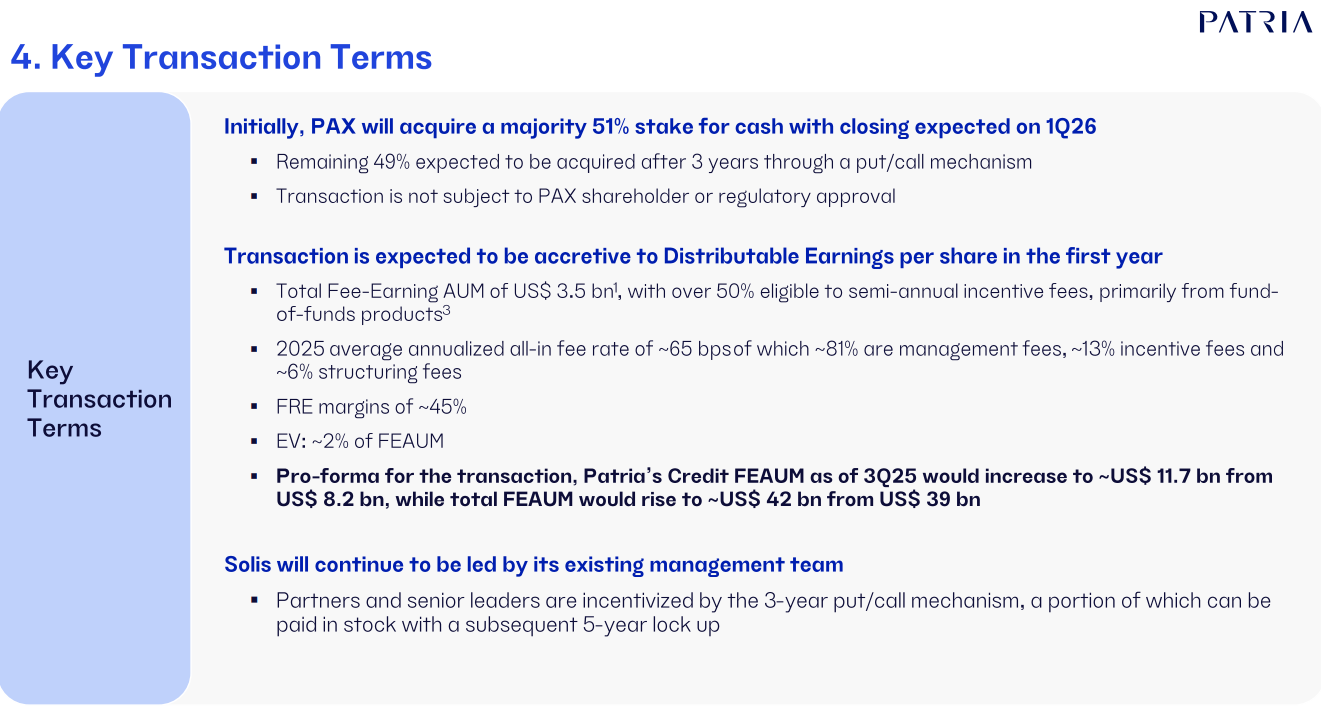

Patria Investments Limited (“Patria”) (NASDAQ: PAX), a global alternative asset manager, announced today the agreement to acquire 51% of Solis Investimentos, a Brazilian investment manager specializing in the structuring and management of CLOs. The CLO market in Brazil has been benefiting from a variety of structural and secular trends which have driven asset growth at a compound annual growth rate (“CAGR”) of 35% over the last 5 years.

Upon completion of the transaction, the addition of Solis’ approximate US$ 3.5 bn of Fee-Earning AUM (“FEAUM”) will increase Patria’s total Credit FEAUM by over 40% to more than US$ 11.7 bn pro-forma as of 3Q25, solidifying its position as a leading Credit platform in Latin America. Pro-forma for the transaction, Credit will account for over 25% of Patria’s total FEAUM.

10 Likes

And the next bigger deal ![]()

UnitedHealth sells Banmedica to Patria

UnitedHealth Group has agreed to sell its last South American business Banmedica to Brazilian private equity group Patria Investments for $1 billion, two sources with knowledge of the matter said on Sunday.

The final agreement was signed on Saturday and an announcement is expected on Monday, the sources added, asking for anonymity to disclose private talks.

UnitedHealth has been trying to exit Latin America since 2022 and had previously sold its businesses in Brazil and Peru.

The sale of Banmedica, which currently operates in Colombia and Chile, has been under discussion for almost a year.

Patria and UnitedHealth did not immediately reply to requests for comment on Sunday. Banmedica had 1.7 million health insurance plan members, seven hospitals and 47 medical centers as of June, after its divestment from Peru.

The exit from the region reduces one more distraction from the turnaround efforts led by CEO Stephen Hemsley. UnitedHealth, a member of the Dow Jones Industrial Average, raised its annual profit forecast in October and said it aims for a return to growth in 2026 that should accelerate in 2027.

Hemsley returned as CEO in May after leading the company from 2006 to 2017 and has been working to regain investor and consumer trust after a difficult period for UnitedHealth that included the murder of a top executive, an unexpected surge in medical costs and a federal probe.

He was brought in as a part of a management shakeup after the company’s first earnings miss in over a decade in April.

UnitedHealth booked an $8.3 billion loss last year related to the sale of its South American operations, $7.1 billion stemming from the Brazil exit and $1.2 billion from Banmedica.

6 Likes

Here are more details about the Solis acquisition and the CLO market

Those loan market figures are quite large ![]()

https://ir.patria.com/static-files/a94efafa-6b45-44bf-8005-703904aefa87

More detailed specs about the transaction

5 Likes

Patria has gotten its buying pants out of the closet for the end of the year.

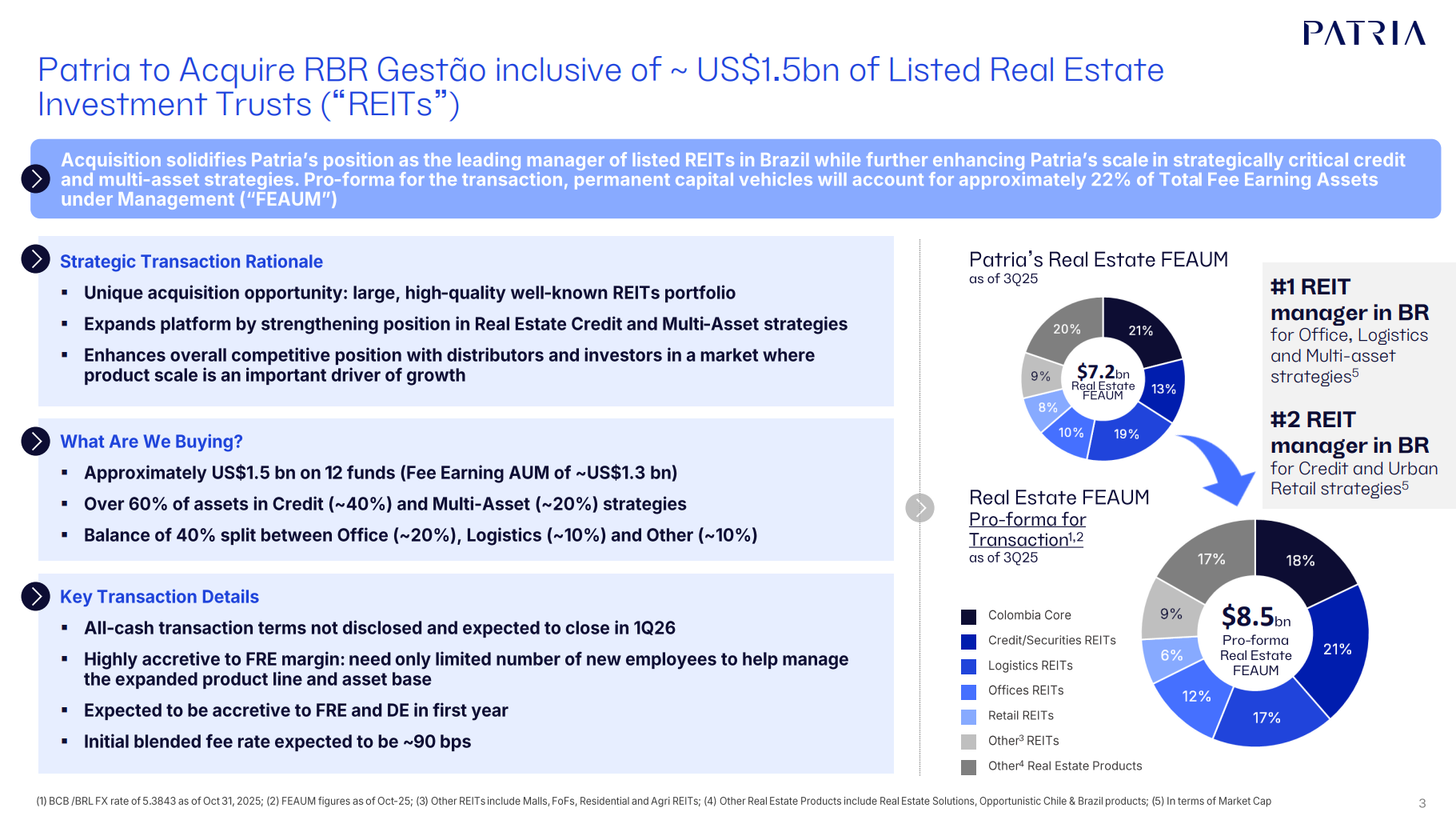

A new REIT player has taken the bait and moved into PAX’s control. Approximately 20% increase in real estate assets under management.

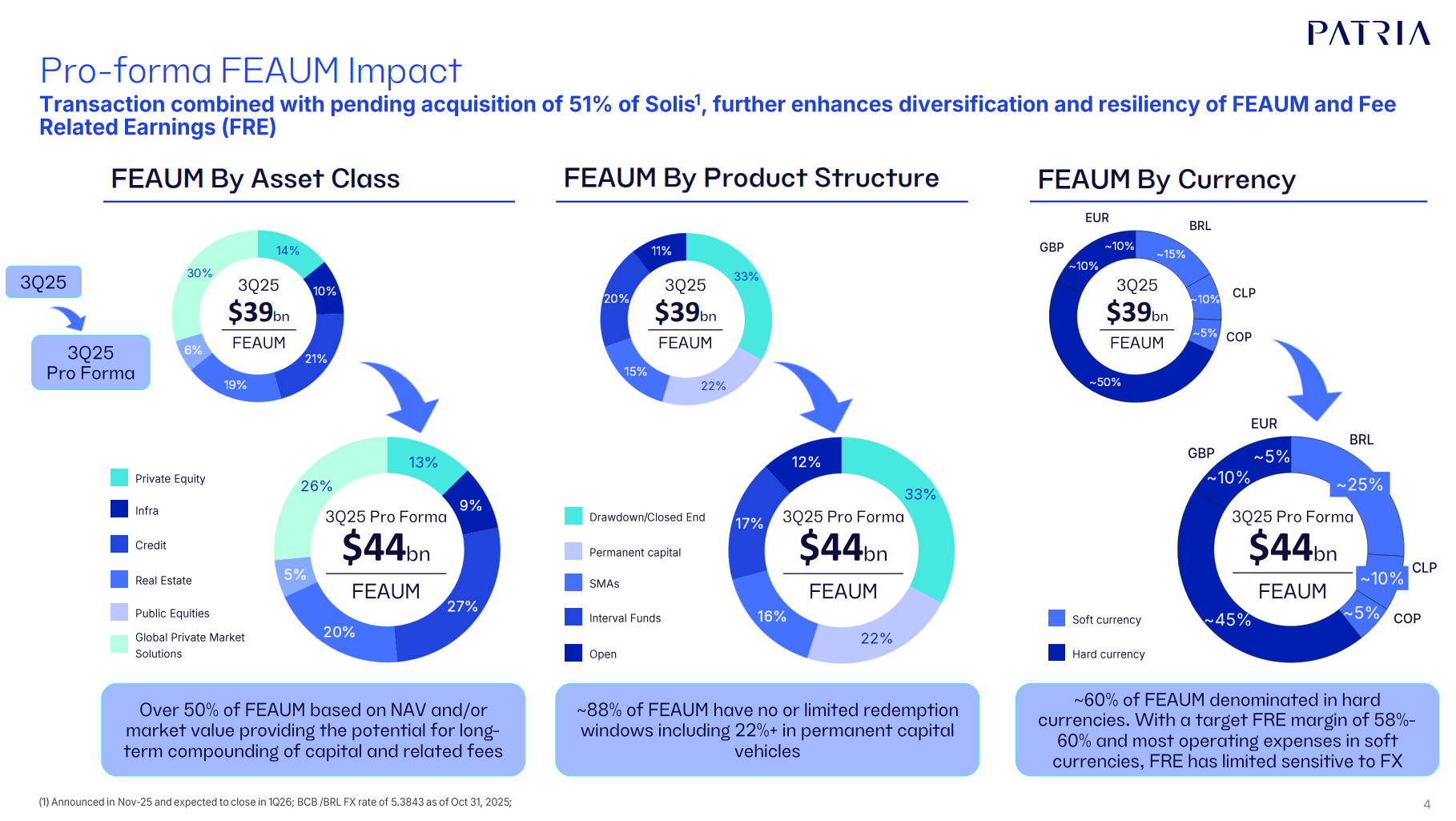

The Real’s ![]() weighting in currencies increases from 15% → 25%

weighting in currencies increases from 15% → 25%

Press release:

https://ir.patria.com/news-releases/news-release-details/patria-investments-announces-acquisition-rbr-gestao-adding-us-15

Patria Investments Limited (“Patria”) (NASDAQ: PAX), a global alternative asset manager, announced today the agreement to acquire RBR Gestão de Recursos Ltda. (“RBR Gestão”), which, after internal corporate reorganization, will hold approximately US$ 1.5 bn of listed Real Estate Investment Trusts (“REITs”). RBR Gestão is the current manager of 12 funds, of which 11 are listed REITs focused predominately on Credit and Multi-Asset strategies. Other assets that are not within the perimeter of the transaction will be carved out under the aforementioned internal corporate reorganization and will remain under the management of other RBR Group companies and their respective teams. Although not subject to shareholders nor antitrust approvals, the transaction remains subject to the satisfaction of conditions precedent customary for this type of transaction. Post acquisition, Patria will be the leading manager of listed REITs in Brazil with scale across a variety of strategies, including Office, Logistics, Credit, Multi-Asset and Urban Retail.

Upon closing of the transaction, the addition of approximately US$ 1.3 bn of Fee Earning Assets under Management (“FEAUM”) will increase Patria’s total Real Estate FEAUM to US$ 8.5 bn pro-forma as of 3Q25, representing a Compound Annual Growth Rate (“CAGR”) of over 65% since Patria’s IPO in early 2021. Patria’s high-margin Real Estate strategies, of which 90% is in permanent capital vehicles, will account for over 20% of Patria’s total FEAUM.

Rodrigo Abbud, Patria’s Head of Real Estate in Brazil, said: “It’s remarkable to see the evolution of Patria’s Real Estate platform. With the acquisition of RBR Gestão and the management of these 12 funds, Patria becomes the leading REIT manager in Brazil, positioning us for continued growth in a market where, in addition to investment performance, scale is key.”

6 Likes

Short report published a few days ago

- I didn’t find any particularly significant problem areas in it. Some holdings certainly perform better and others worse; that’s just part of doing business.

- In my view, transfers between funds are normal activity when old ones are being closed and some holdings are transferred to a new one.

- Exiting the funds is still ongoing, so comparing realized NAV is quite futile; it certainly looks nice on a graph, given the agenda.

I also bounced this off ChatGPT. A hidden summary of the report's main points, if you'd like to read.

1) Core Short Thesis — “Overstating performance & masking losses”

1) Core Short Thesis — “Overstating performance & masking losses”

Snowcap Claim:

Patria is allegedly masking losses in flagship funds by using aggressive valuations and off-balance-sheet loans, keeping cash-burning/distressed assets marked high despite poor fundamentals. Key funds supposedly hide weak performance and unrealized NAV is dominated by a few troubled positions.

Assessment:

- Mixed credibility — Private markets do rely on valuations, and differences between private valuations and public comps are common. However, Snowcap’s narrative is built on their interpretation of Brazilian filings and former employee quotes — not verified by independent auditors or regulators.

- Independent public information (e.g., analyst commentary) notes Patria has delivered mixed profitability and variable fundraising efficiency, but no public audit/regulator has found wrongdoing.

Verdict: Unverified and potentially biased hypothesis. Snowcap’s own disclosure states they hold a short position, signaling inherent bias.

2) Extreme Valuation Multiples on Key Holdings

2) Extreme Valuation Multiples on Key Holdings

Snowcap Claim:

Examples like Elfa Medicamentos valued at ~15x EV/EBITDA vs 4–6x for listed peers, and other portfolio companies at high multiples despite distress indicators.

Assessment:

- Possible, but context matters — Private company valuations are inherently less precise than public ones. High multiples may reflect growth, control premiums, illiquidity, or different EBITDA adjustments.

- Snowcap compares private valuations to public comps without always accounting for differences in business models or risk profiles.

- Snowcap’s view that “Elfa equity could be worthless” is speculative without audited asset-by-asset liquidation/valuation evidence.

Verdict: Claim requires deeper due diligence; not conclusive on its own.

3) Off-Balance Sheet Loans & Fund Guarantees

3) Off-Balance Sheet Loans & Fund Guarantees

Snowcap Claim:

Alleges Patria used off-balance sheet financing and fund guarantees to prop up troubled investments and delay loss recognition.

Assessment:

- This is a red-flag style allegation, but unproven in public domain.

- There’s no known regulatory or auditor finding that Patria has improperly hidden liabilities or used illicit structures to mislead investors.

- Recent news notes a delay in the Form 20-F filing — but this was explained as extended reviews due to business combinations, not fraud.

Verdict: Unverified; presented as speculation rather than documented fact.

4) Performance Fees & Asset Transfers Between Funds

4) Performance Fees & Asset Transfers Between Funds

Snowcap Claim:

Most performance fees in FY2024 came from a transfer of assets between Patria funds instead of real portfolio exits.

Assessment:

- It’s possible funds engage in cross-fund transactions; this occurs in private markets, but whether this was done to artificially inflate fees is not independently confirmed.

- Public filings do not highlight irregularities in fee reporting or banned practices.

Verdict: Allegation of questionable behavior requires substantiation beyond short-seller analysis.

5) AUM Roll-off & Duration Risk

5) AUM Roll-off & Duration Risk

Snowcap Claim:

Claims up to 40% of AUM could mature/roll off within 3 years, potentially pressuring earnings.

Assessment:

- This is plausible as a private markets feature — many funds have finite lives and will either realize exits or roll into new vehicles.

- Patria’s disclosures on AUM mix and duration aren’t as granular publicly, so the exact roll-off percentage is hard to verify independently.

Verdict: Possible risk factor, not necessarily misconduct.

6) Blackstone Exit / Auditor Change / CFO Resignation

6) Blackstone Exit / Auditor Change / CFO Resignation

Snowcap Points:

- Blackstone sold down its stake.

- Patria changed auditors in 2025 without full public explanation.

- CFO resignation observed.

Assessment:

- Blackstone selling down: Confirmed — Blackstone reduced its stake over time. That doesn’t necessarily imply performance issues; strategic de-risking is common.

- Auditor change & CFO departure: Patria’s filings do show changes in leadership and auditors, but absence of detailed comment doesn’t prove wrongdoing.

- Changes in management and service providers do happen normally in companies of this size.

Verdict: Relevant context but not proof of systemic fraud.

What Snowcap is not proving with public evidence

| Major Snowcap Claim | Verified Independently? |

|---|---|

| Patria is inflating NAVs fraudulently | |

| Assets are worthless despite valuations | |

| Off-balance sheet guarantees misused | |

| Management lacked transparency |

Looking at it from another perspective:

- The USD/BRL (Real) exchange rate is favorable, and even though the impact of currency exchange rates has diminished, this has a potentially profit-boosting effect, at least in the short term.

- Emerging markets are now attracting more capital, as the US market shows similar traits and risk levels there are on the rise.

6 Likes

The company mentioned in its earnings release that they are planning to target the US (and Mexican) markets (at least in real estate & credit).

We’ll see if the more volatile situation in the US affects these plans. However, interesting opportunities might open up there while there’s some turbulence ongoing.

In general, regarding the CEO’s responses, I have to say they are at least thorough and extensive in the Q&A sessions. Of course, something essential could still be hidden, but it seems like they would rather answer too much than too little.

3 Likes

The Q4 earnings release is being moved forward by a week, meaning it will be tomorrow, February 3, 2026:

And shopping in the US:

https://ir.patria.com/static-files/53b375d7-a3c4-47e0-aa15-332605eb2f6c

5 Likes

Q1/2026

https://ir.patria.com/static-files/9954afad-96e4-4a06-8056-5ed18917e3f0

“We delivered a strong start to 2026, driven by continued fundraising momentum, meaningful growth in Fee-Earning AUM, and consistent investment performance across our platform,” said Alex Saigh, Chief Executive Officer of Patria. “We raised $2.1 billion in the quarter, grew Fee-Earning AUM to nearly $46 billion, and delivered 19% year-over-year growth in Fee Related Earnings, keeping us firmly on track to achieve our full year objectives. With increasing global and local investor engagement, a strengthened balance sheet following our inaugural bond issuance, and a highly diversified, long duration asset base, we believe Patria is exceptionally well positioned to capture the opportunities ahead.”

Financial Highlights (reported in $ USD)

IFRS results included $2.3 million of net income attributable to Patria in Q1 2026. Patria generated Fee Related Earnings of $50.5 million in Q1 2026, up 19% from $42.6 million in Q1 2025, with an FRE margin of 54.6%. Distributable Earnings were $42.4 million for Q1 2026, or $0.27 per share.

And another dividend increase from 0.15 → 0.1625

Dividends

Patria declared a quarterly dividend of $0.1625 per share to record holders of common stock at the close of business on May 18th, 2026. This dividend will be paid on June 11th, 2026.

7 Likes

Solid performance indeed, the metrics are still pointing in the right direction. In the current uncertain global situation, it’s a pleasure to hold this stock even just from a geographical diversification perspective (of course, good growth and a decent dividend need to be there as a foundation). I would add at these levels, but my position is already such a good size that I’m content with just happily holding.

That dividend increase was likely a “technical announcement,” as they previously stated they would pay a total of 0.65 dollars in dividends this year. The first installment of the year was 0.15, and now presumably there will be two quarters at 0.1625, followed by one similar increase announcement (0.175) towards the end of the year, bringing the annual total to that 0.65 figure.

4 Likes

Patria’s fundraising for the new fund has exceeded expectations

Patria SOF V exceeds its initial USD 500m target, building on the success of its predecessor secondary funds

GRAND CAYMAN, Cayman Islands, July 02, 2026 (GLOBE NEWSWIRE) – Patria Investments, a global alternative asset manager and industry leader in Latin America and Europe, has successfully closed Patria Secondary Opportunities Fund V (“SOF V”), securing over USD 670m in total commitments.

SOF V closed more than a third above its initial target size of USD 500m and is a significant increase on the size of its predecessor fund Patria Secondary Opportunities Fund IV. SOF V attracted commitments from a diverse global investor base spanning institutional investors, family offices and private wealth channels. Re-ups and existing Patria clients accounted for approximately 55% of SOF V commitments, with the remaining 45% of commitments coming from new investors.

The Fund attracted capital from five regions with North America representing over 50% of total commitments, followed by Europe at approximately 40%, with additional commitments from investors in Latin America, the Middle East and Asia-Pacific.

7 Likes