En ole vakuuttunut että Panostaja kykenee luomaan arvoa sijoittajille. CoreHW on ainut joka voi melkeinpä pelastaa tilanteen, mutta on myös mahdollista, että siitä tulee myös perus mörnijä. 2020-luvulla Panostaja on ollut umpisurkea. Nettotulosta on tullut viiteen vuoteen -8,6M€ yhteensä. Aikamoista arvon tuhoamista ja tällekin vuodelle ennustetaan tappiota. Ei siis ihme että kurssi on alhaalla. Vaikka arvoa on nähtävissä osien summassa niin lopulta jos ei tule rahaa viivan alle, yritykset on kutakuinkin arvottomia. Edes pieni positiivinen nettotulos ei riitä kun halutaan saada ainakin 7% vuosituotto. Panostaja saisi maksaa enemmän osinkoja ulos. Väitän että meistä lähes jokainen saisi ne rahat paremmin tuottamaan kuin Panostaja itse.

Konsernikuluja voisi myös karsia. Jos Muut kategorian kulut -1,6M€ 9kk aikana on tätä. Summa vastaa Granon, Hyggan, CoreHW:n ja Lenion yhteenlaskettua liikevoittoa samalta ajalta. Onko liian kalliit toimistot hyvillä paikoilla ja kaikki kivat edut vai mistä moinen? Pitäisi sopeuttaa kuluja.

CoreHW on se ainoa syy miksi tämä kuitenkin vähän kiinnostaa. Mikäli siellä onnistutaan jatkossa paremmin niin ehkä kannattaakin Panostajaa omistaa. Vielä ei vakuuta.

@Blackparta Määritätkö ”omistaja-arvon tuhoamisen” kirjanpidollisen kikkailun seurauksena saadun nettotuloksen perusteella? Vai olisiko mahdollisesti parempi määritystapa katsoa yrityksen tuottamaa operatiivista kassavirtaa tai kenties vapaata kassavirtaa? Nuo luvut ovat viimeisen esimerkiksi 5 vuoden ajalta oikein mallikkaat ja itselleni sijoittajana hyvin paljon tärkeämmät kuin nettotulos tai EPS. Panostaja on vuoden 2018 jälkeen jokaisena vuonna tehnyt erinomaisesti vapaata kassavirtaa, joka näyttää unohtuvan hyvin monelta sijoittajalta jotka tuijottavat vain kirjanpidollisen kikkailun tuottamaa alinta riviä. Ja kyllä, vähemmistöt toki vaikuttavat lukuihin eikä kassavirtaa/vapaata kassavirtaa voi suoraan katsoa sellaisenaan.

Ehkä olet oikeassa, mutta ei tässä kyllä mielestäni ihan kauheasti ole arvoa luotu kun 31.10.2019 oli omaa pääomaa 79,552M€ ja se nyt oli 30.4.2025 48,544M€. Hienosti on kikkailtu omistaja-arvoa kirjanpidolla. Toki hieman osinkoja tullut myös matkan aikana. Aika paljon paremmin olisi mennyt jos olisi sijoittanut OMXH25:een. Voihan se olla että seuraavat 5v Panostaja voittaa indeksin, mutta täytyy kuitenkin vähän olla skeptinen.

Juha ja Tomi juttelivat Panostajasta yli 40 minuuttia.

Aiheet:

00:00 Aloitus

00:36 Arvonluontia aktiivisena omistajana ja kehittäjänä

02:52 Pääoman tuotot jääneet laihoiksi ja kauas tavoitteista

05:35 Granosta olisi pitänyt irtaantua jo 5 vuotta sitten

10:33 Grano jauhaa vahvaa rahavirtaa

12:23 Oscar Software potentiaalinen arvoajuri Panostajalle

15:17 CoreHW:n läpimurto voisi räjäyttää pankin

21:58 Lenio portfolion tuorein kasvuaihio

27:28 Murheenkryyni Hyggan arvo nollissa

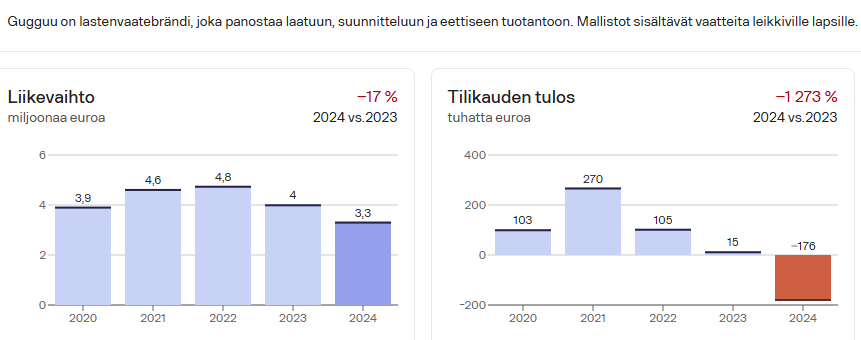

30:36 Gugguun hyvä kehitys katkesi koronavuosiin

33:11 Kassa saatava töihin

36:24 Osake on halpa konservatiivisillakin odotuksilla

39:50 Positiivinen skenaario

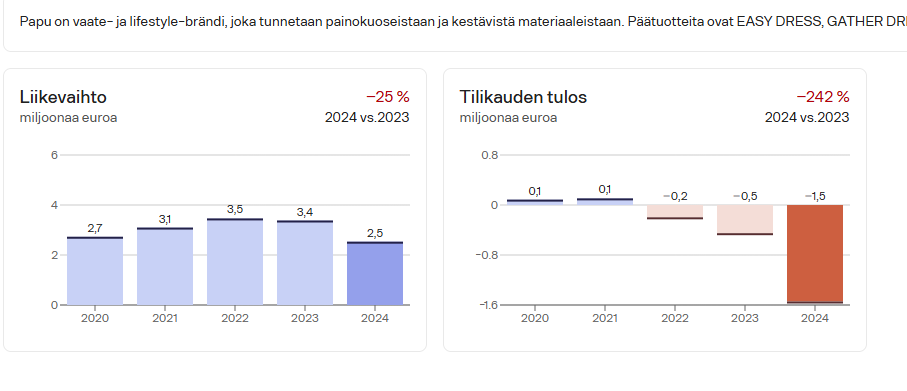

Puhutaan Panostajan kannalta hieman sivuseikoista. Panostajan vähemmistöomistaman (43% omistusosuus) Gugguun kotimainen kilpailija, Papu Design, hakeutui konkurssiin. Tulee mieleen, että joutuukohan Panostaja kirjaamaan Gugguun omistustaan alas jollain aikavälillä, koska Gugguu on myös taapertanut tässä kysyntätilanteessa jo pitkään.

Viimeisimmässä analyysissa Kinnunen toteaa, että Inderes ei ole tehnyt Gugguulle arvonmääritystä, vaan Panostajan kirjaaman tasearvon 1,55 MEUR mukaisesti tuo vähemmistöosuus on huomioitu myös Inderesin arvonmäärityksessä.

Mielenkiintoista seurata tätä sivuraidettakin, että mitähän ihmettä Panostaja aikoo osuudelleen tehdä ja varsinkin, mitä ihmettä Panostajan konttorilla luultiin tiedettävä lastenvaatebisneksestä ylipäänsä?

Eipä tuo gugguu taida ihan samassa tilanteessa olla kun tehnyt suurinpiirtein nolla tulosta. Varmaan tässäkin pitää kulut pitää tiukasti hanskassa kun suhdanne on mitä on. Tämä vuosi on vielä heikompi kuin edellinen ja myynti on jäljessä ja tappio on samaa luokkaa kuin edellinen vuosi.

Tietty jos tappiot onnistuu pitämään minimissä niin on tämä monelle tällaiselle pienemmälle firmalle ollut selvitymistaistelua. Toisaalta niitä kaatumisiakin tulee ja yleensä sitten myynti saattaa siirtyä heiltä kilpailijoille..

Yleinen talouden vire on suomessa aneeminen ja se heijastuu moneen sektoriin kun ihmiset eivät kuluta. Vähän noidankehä kun porukka pelkää inflaatiota, oman työpaikan säilymistä, energian hintoja, bensanhintaa jne.. ja säästää sukan varteen… samalla sitten kaivetaan omaa kuoppaansa kun täällä ei kuluteta niin monen työpaikka loppuu sitten siihen että kuluttajat säästää liikaa ja yhä useampi firma on nurin tai yt parissa. Liikevaihto ja liikevoitto oli vielä suht hyvin hanskassa vuosina 2016-2021. Liikevoitto oli parhaimillaan noin miljoonan. Saa nähdä koska kauppa piristyy ja miten luvut kehittyvät jatkossa.

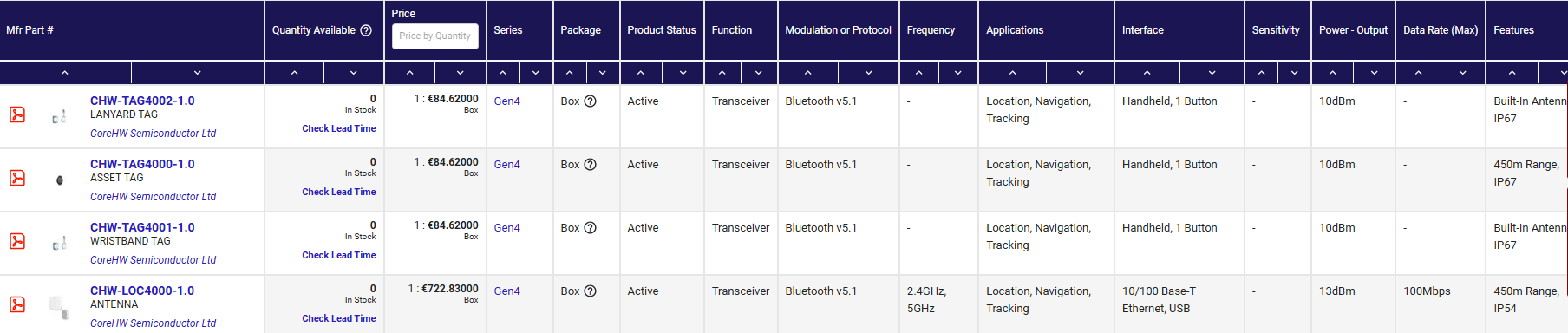

Corehw:n lokaattorit tulleet näköjään myyntiin (digikey). Saldot tosin nollissa vielä, mutta eiköhän tuo ylösajo kohta ala. En tiedä onko näitä nyt sitten alettu pistää painoon kun sertifioinnit saatu ja testaukset käynnissä. Aika näyttää..

Tässä on Kinnusen kommentit, kun Hyggan klinikkaliiketoiminnan myynnistä.

Panostaja tiedotti eilen myyvänsä tytäryhtiönsä Hyggan klinikkaliiketoiminnan PlusTerveys Hammasklinikat Oy:lle. Liiketoiminnan kauppahinta 2,8 MEUR on mielestämme olosuhteisiin nähden hyvä, mutta korollisia velkoja Hyggalla on merkittävästi enemmän. Hygga Flow -ohjelmistoliiketoiminta jää toistaiseksi Panostajalle, mutta sitäkin todennäköisesti pyritään myymään. Olemme arvioineet Panostajan koko Hygga-omistuksen arvon nollaksi jo aiemmin, eikä kauppa anna aihetta muuttaa arviota arvon jäädessä oletettavasti nettovelkojen alle. Positiivisena näemme sen, että Hyggasta irtaantuminen selkeyttää Panostajan fokusta ja pysäyttää tappiot epäonnistuneessa sijoituskohteessa.

Ehkäpä tämä kohta lähtee ja toivottavasti isosti: alla pari nostoa..

Itse olen edelleen sitä mieltä että jos ja toivottavasti kun nämä lähtevät skaalaukseen, niin Panostajan nykyarvo on muisto vain.

“The certification of our Tags and Locator validates years of R&D and comprehensive testing,” said Mika Jäsberg, VP of RTLS and Devices Business at CoreHW. “We’re thrilled that several customers are now entering production with these solutions – demonstrating that the technology is not only proven but ready for real-world, large-scale deployment.”

With the certification now in place, CoreHW has begun fulfilling commercial orders for Tag and Locator units. Early customers – including partners in industrial automation, logistics, and healthcare – are now launching production systems that rely on CoreHW’s high-accuracy Bluetooth AoA technology platform.

Granossa on tehty yhden liiketoiminnon myynti. Granon tytäryhtiö, Grano Diesel, on myyty tytäryhtiön toimitusjohtajalle. Kauppahinnasta ei ole mainintaa eikä tämä ilmeisimmin ollut Panostajan mittakaavassa tiedotteen arvoinen juttu. Asiakastiedosta selviää, että Diesel on ollut Granon kannattavimpia osia: Nousevalla trendillä oleva liikevaihto ja liikevoiton kehitys erityisesti vuonna 2024 oli huikean hyvä.

Tämän myötä Granon liikevaihto tippunee 8-10% ja jäljelle jäävän Granon suhteellinen kannattavuus taitaa laskea myös hieman? Toisaalta, markkinointiviestinnän liiketoiminnan myynti antaa hiukan toivoa sille, että jäljelle jäävä Grano on nyt fokusoidumpi (ja pienempi) paketti ostokohteeksi jollekin. Ehkä tällä saadaan myös Granon nettovelkaa nopeammin alas?

Vaikka kyseessä lienee ns. katsauskauden jälkeinen tapahtuma, niin @Juha_Kinnunen olisi kiva saada muutama CEO:n kommentti tästä joulukuun haastattelussa.

Tiedote 12.11.2025

Edit: Toteaisin vielä, että Hyggan klinikan ja Granon markkinointiviestinnän myyntien jälkeen Panostaja on on kutistunut entisestään, jota Lenion osto ei kompensoi. Näillä kahdella myynnillä liikevaihtoa lähti noin 12 MEUR ja positiivista liikevoittoa useta satoja tuhansia euroja. Ainakin lyhyellä tähtäimellä kehitys menee edelleen väärään suuntaan ja Panostajan kiinteiden kulujen suhteellinen osuus kokonaisuudesta taisi kasvaa entisestään.

Se on nykyään @Olli_Vilppo ruorissa Panostajassa, joten otetaampa hänet tähän mukaan. Minä olen varmaan 15 vuoden Panostaja -taipaleen jälkeen siirtynyt sivummalle, ja Olli saa katsoa yhtiötä tuoreemmin silmin

Heikkoa ollut kyllä Panostajan suoriutuminen Kotisun rahapotin jälkeen. Juuri mitään järkevää käyttöä rahalle ei keksitä. Samaan aikaan Relais group tekee 5 yrityskauppaa vuodessa ja kasvaa. Roinisen investors house on takonut miljoonia vaikka asuntomarkkinat on surkeat. Jopa Arvo osuuskunta tehnyt rahaa exiteillä ja on lupaavia omistuksia kuten Lapwall palanen. Kompetenssia tarvitaan. Olisi ostettu vaikka bitcoineja tai edes Nasdaq indeksiä jos ei muuta keksitä.

Sitten toisena liian suuri osa omistuksesta on huonolla toimialalla. Panostaja on vähän jäänyt Granon vangiksi. Kun on junassa joka menee väärään suuntaan, niin hyvälläkään suorittamisella on vaikeaa saada hyvää tulosta.

Teknologia yritykset joilla on omia tuotteita arvostetaan usein hyvin kalliisti. Esim. Optomed ja Nexstim 100 Miljoonan pinnassa, vaikka hädin tuskin nenä pinnalla vasta. Jo tuolla hinnalla Panostajan omistus oli 50me arvoinen. Kun koko panostaja P on vain 25me + velat, niin olisihan siinä mannerlaattojen liikettä. Nyt Optomed liikevaihto on 15me ja Nexstim 9me. Corehw prototyypit 1me ja Inderes podissa arvattiin alkuvaiheen liikevaihdoksi 3me kaupalliselle toiminnalle.

Itse uskon että noissa kolmessa pilotissa on kyse kymmenestä miljoonasta ylöspäin koostuvasta liikevaihdosta. Se miten se skaalaus tehdään ja jakautuuko kuinka monelle vuodelle, saadaanko yksittäinen kauppa läpi vai kenties useampi.

Itse uskon että noilla 3 pilotilla puhutaan toteutuessaan kymmenistä miljoonista, miljoonien sijaan.

Näitä tuotteitahan ei tehdä mihinkään pk-yrityksiin vaan todennäköisesti jättimäisiin yrityksiin jotka hakevat tehokkuutta, jäljitettävyyttä toimintoihin.

Uskon että 5-vuoden potentiaali liikevaihdollisesti liikkuu 10-70M estimaatissa. Riippuen siitä kuinka suuria toimijoita tämä jenkkien sairaanhoitoasiakas ja japanilaiset logistiikka/teollisuusasiakkaat ovat.

Kyllähän skaalaus piloteista täyteen tuotantoon täytyy olla 10x ylöspäin.

Paljon ratkaisee se saadaanko nämä asiakkaat skaalaamaan ylipäätänsä ja kuinka suuria toimijoita ne todellisuudessa ovat. Jos esim. Jenkkien toimija on joku iso sairaalaverkoston omaava yritys niin potentiaali on huikea..

Eiköhän se pian selviä että tuleeko kauppaa ja minkälaisille toimijoille. Potentiaali on huikea ja näistä olisi tärkeä saada preferenssiasiakkuudet. Omilla tuotteilla, ip:t, suunnittelu/osaaminen kate% on varmasti kelvollinen ja sopimusvalmistaja on sen kokoinen että pystyy reagoimaan suuriinkin volyymeihin.

Itselleni oli yllätys että pilottiasiakkaat olivat näinkin suuria.. Tuntuu että tämä yritys menee nyt aikalailla seurannan ulkopuolella ja porukalla ei ole oikein käsitystä minkälainen arvoa nostattava tekijä tämä on jos nuo pilotit johtavat seuraavaan steppiin. Ainakaan tämä ei ole näkynyt kurssissa mitenkään🙂

Tuo skaalauskin pitäisi sopimusvalmistajan kautta tapahtua kivuttomasti koska jos en nyt väärin muista niin taiwan semiconductor toimii sopimusvalmistajana.?

CorewHW:llä on muutama merkittävä etu tyypillisiin startt-uppeihin nähden:

Vakiintunut kannattava liikevaihto, rullaava 12 kk liikevaihto yli 10 Me ja EBIT 1,6. Tämä mahdollistaa kasvun ilman osakkeiden laimennusta osakeantien kautta.

Investoinnit tuotteeseen pitkälti tehty, jolloin kasvu käytännössä monistamista

CoreHW on fabless, eli ei omaa tehdasta ja sitä kautta pääomaa sitovaa kasvua

Kaikki on tietenkin kiinni tuotteen haluttavuudesta, jota on vaikea alaa tuntemattoman arvioida. Mutta jos se on alan huippua kuten väitetään, on tässä kaikki palikat paikalllaan Panostajan kannalta käänteentekevään menestystarinaan.

Mikään ei tietenkään ole varmaa, mutta itselläni on hyvä fiilis tämän suhteen, varsinkin kun tämän arvan saa Panostajan mukana käytännössä ilmaiseksi.

Hyvät kolme pointtia. Potentiaali ei valitettavasti näy osakekurssissa, koska CoreHW on Panostajan alla. Harva tietää CoreHW:sta mitään ja viimeistään nimi Panostaja karkoittaa oman 15v track recordinsa vuoksi osan potentiaalisista sijoittajista. Toivon, että tämä muuttuisi Granon, lopun Hyggan ja Gugguun myynneillä. Ja uskoisin tämän myötä Panostajan johtoon strategian mukaisen alan osaajan.

Nvidia taas yllätti iloisesti markkinat eilen illalla. Luulisi, että Suomen pörssin ainoa langattoman teknologian mikrosiruja ja antenneja suunnitteleva ja tuotteistava yhtiö saisi tässä ajassa kiinnostusta ja nostetta, mutta ei.

Positiivista on kuitenkin se, että 12.12.2025 saamme kuulla pidennetyn kvartaalin “välituloksen” (30.10.2025 saakka) ja maaliskuussa 2026 taas koko 14 kk tuloksen. Mielenkiintoisia hetkiä JOS tässä syntyy käänteentekevä menestystarina.