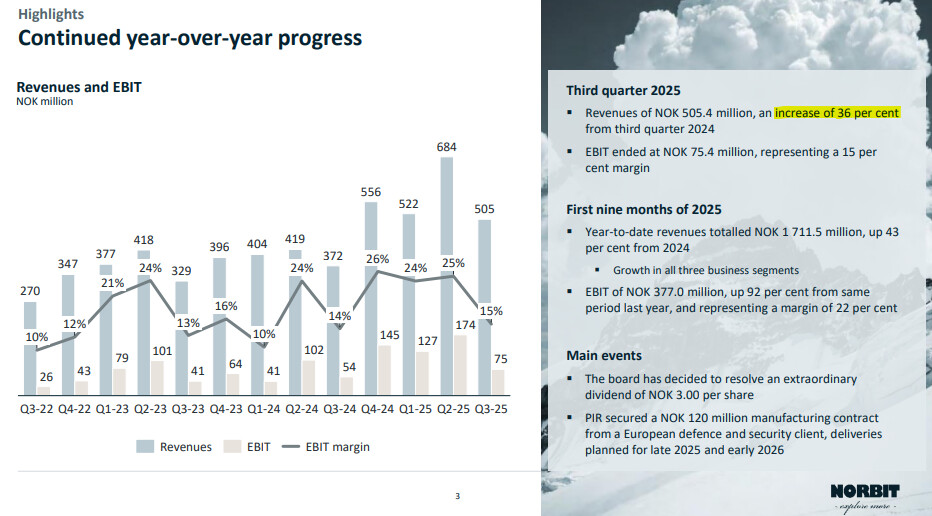

Q3 2025

Let’s write a clean message, as the previous one was already getting a bit overflowing.

Most important first:

Additional dividend (3.0 NOK/share). The last day entitling to the dividend is 17.11. Ex-dividend date 18.11. Payment date approx. 26.11.

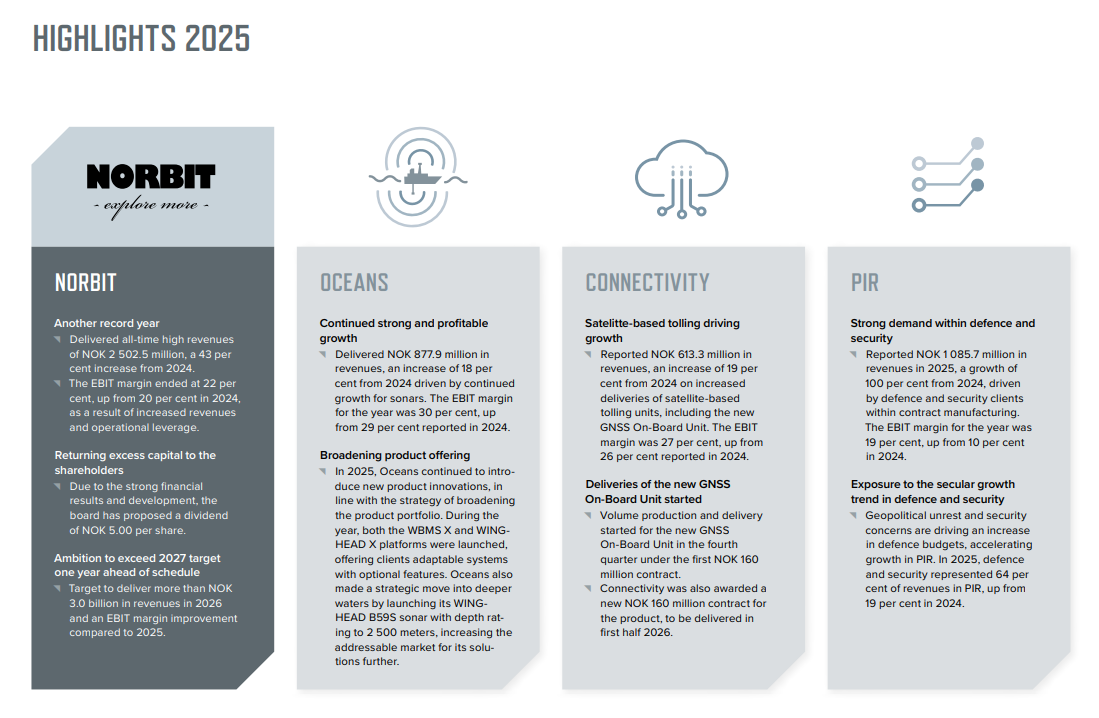

All in all, a very successful quarter. Tremendous growth, even though Q3 is usually a somewhat quiet quarter. It’s nice to see that this is also developing into a truly significant part of the year in terms of results.

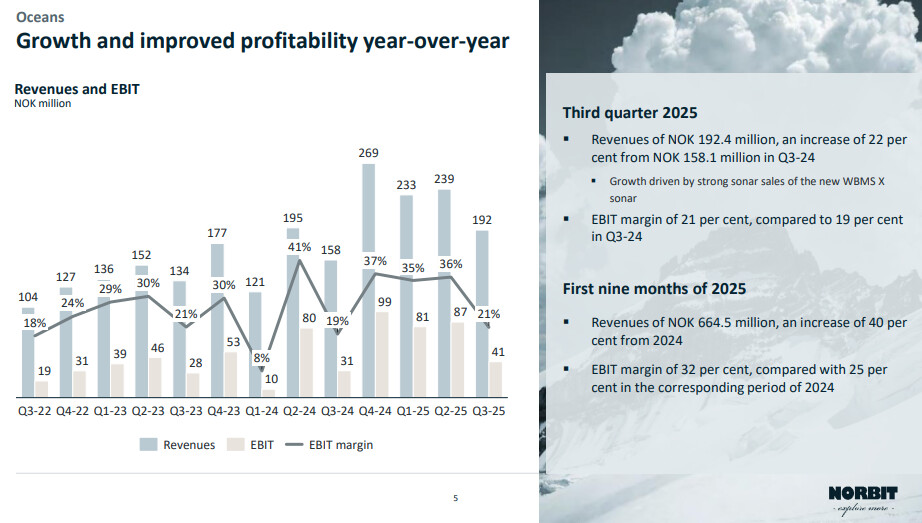

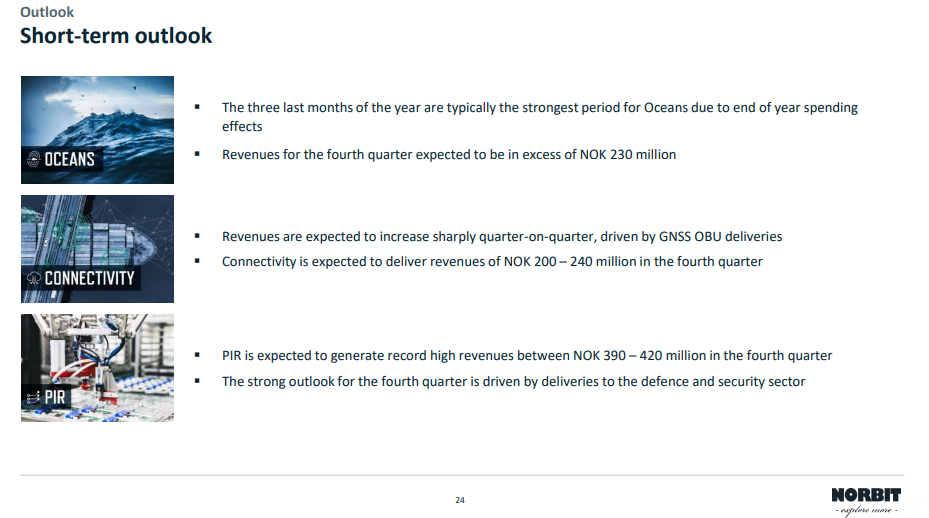

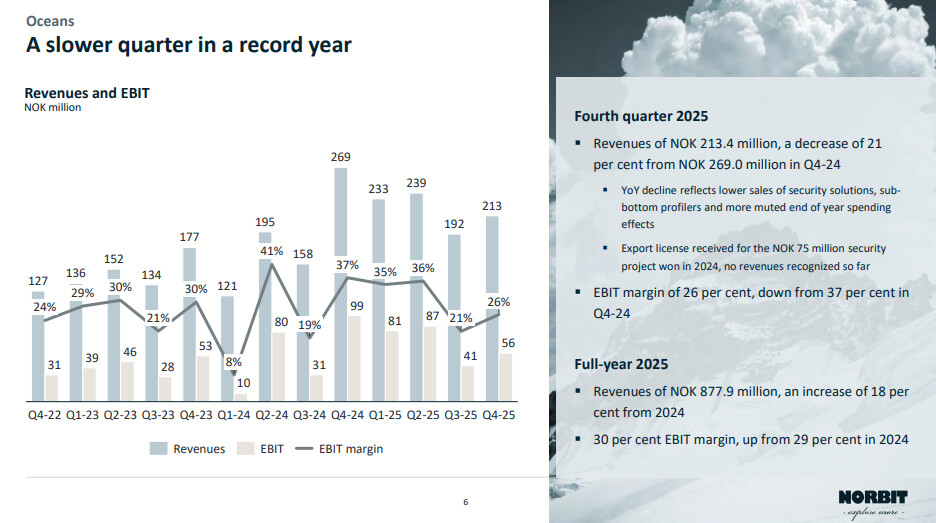

Oceans

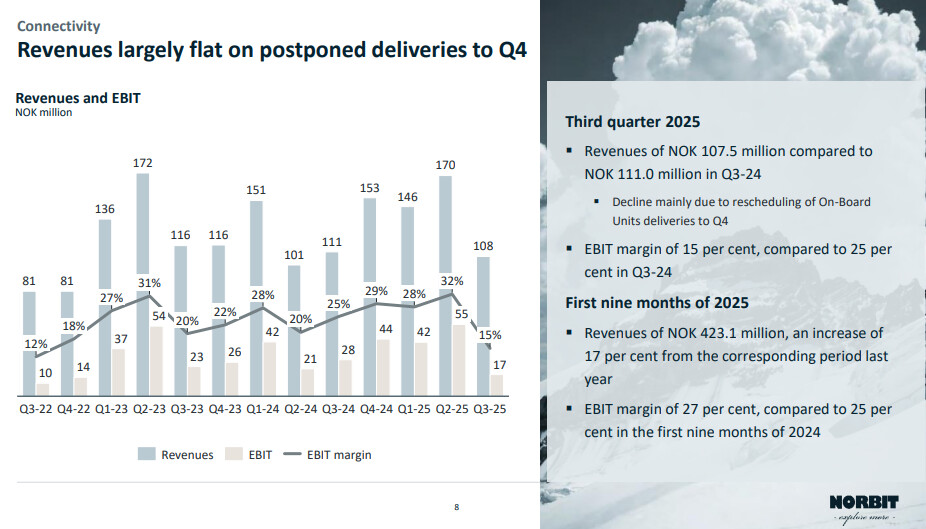

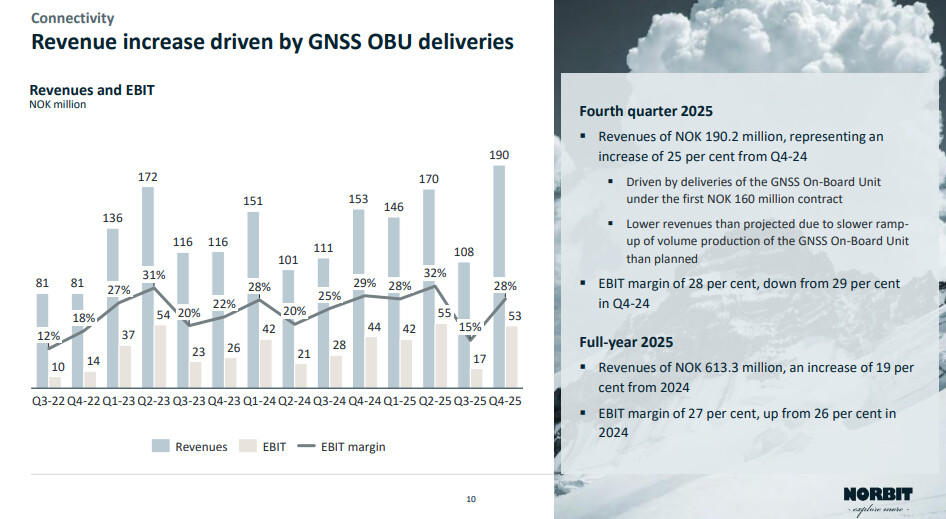

Connectivity

This segment was a clear disappointment for me this quarter. Of course, there was a logical reason for the decrease in revenue, as the delivery of goods had to be postponed to the next quarter. This involved challenges in material procurement, as well as capacity shortages.

GNSS OBUs (On-Board Units) are emerging as Connectivity’s new spearhead, which began to be delivered to Toll4Europe (more about the deal earlier in the thread).

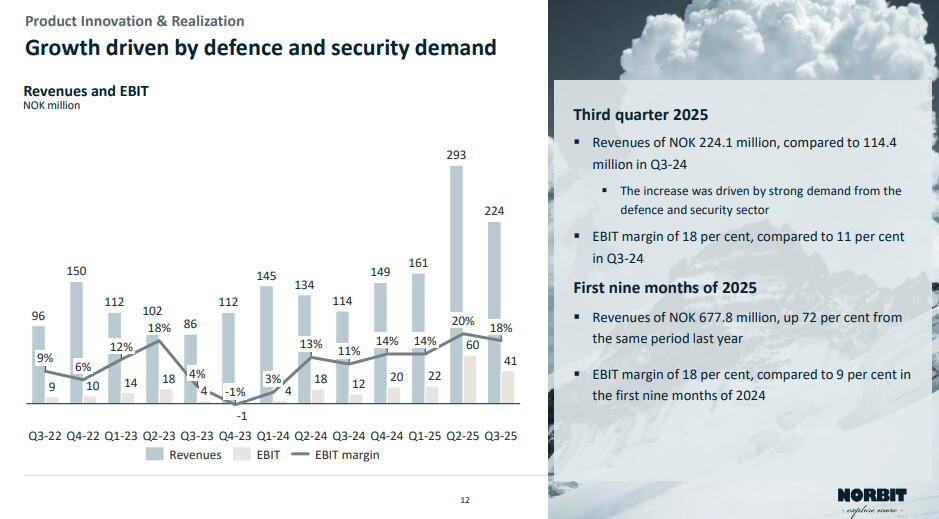

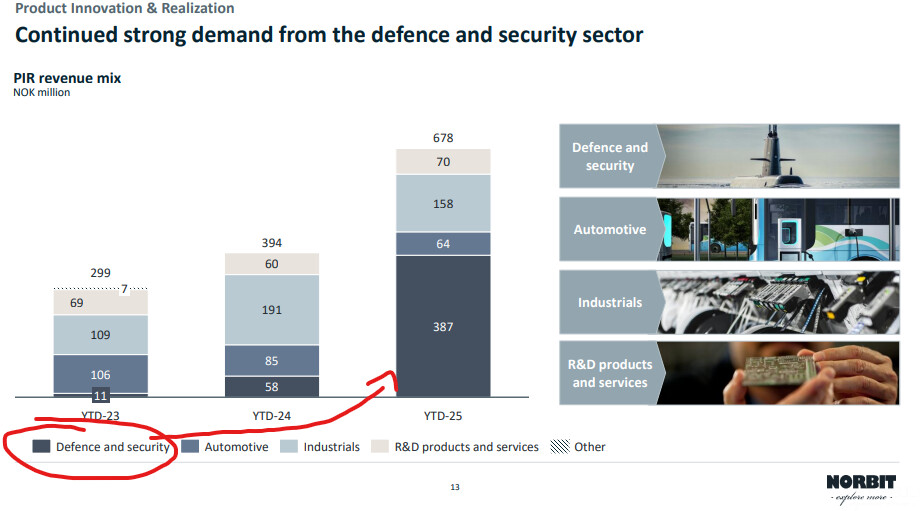

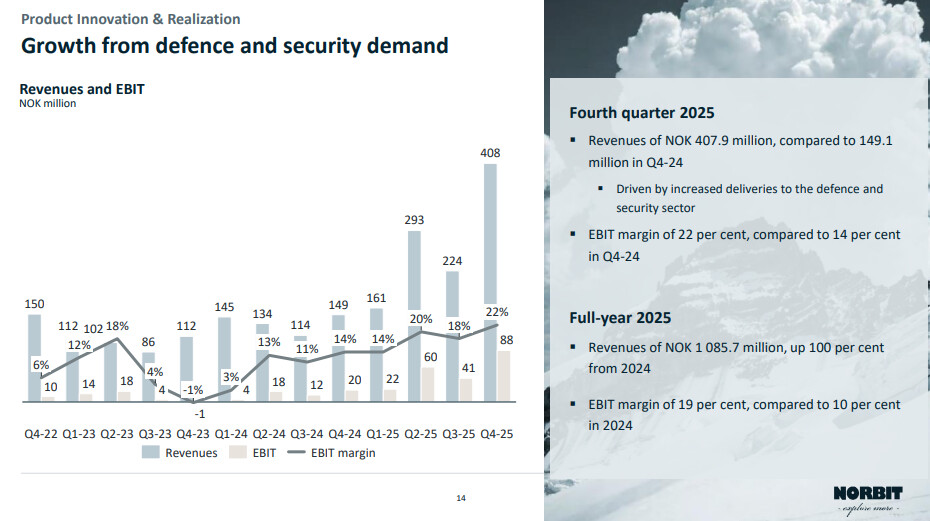

PIR

With the defense and security sector as its main driver, PIR already delivered its second consecutive top quarter.

Overall

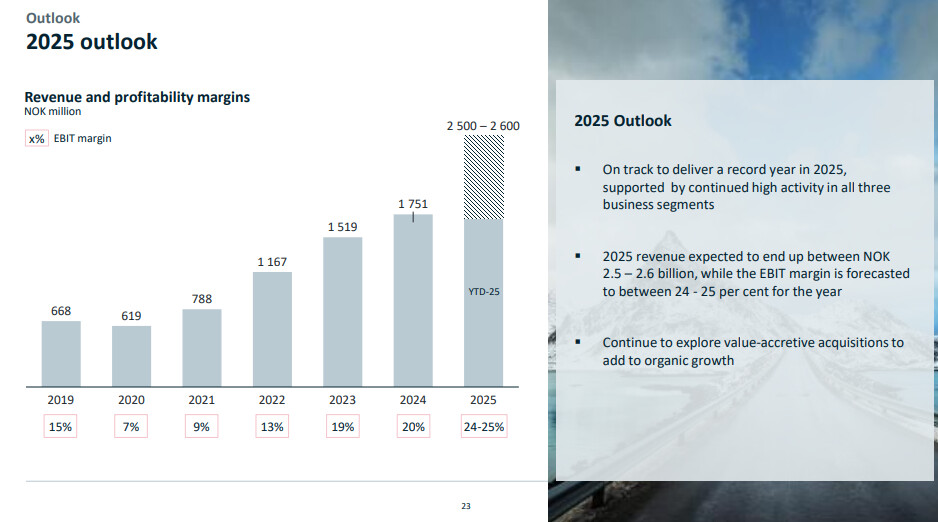

Outlook for the rest of the year

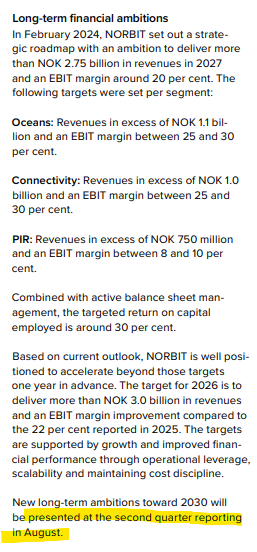

Guidance reiterated, and in the conference call, management was confident that the guidance would be met. The fourth quarter is always quite busy and there’s a lot to do. The biggest variable, once again, is the Oceans segment, whose forward visibility is very limited. However, the company has been a very precise guide, so in my opinion, there’s no reason for major concern. I am perhaps most looking forward to whether new guidance will be given in connection with the Q4 review, and whether the company’s 2027 targets (which will be achieved already next year) will be raised.

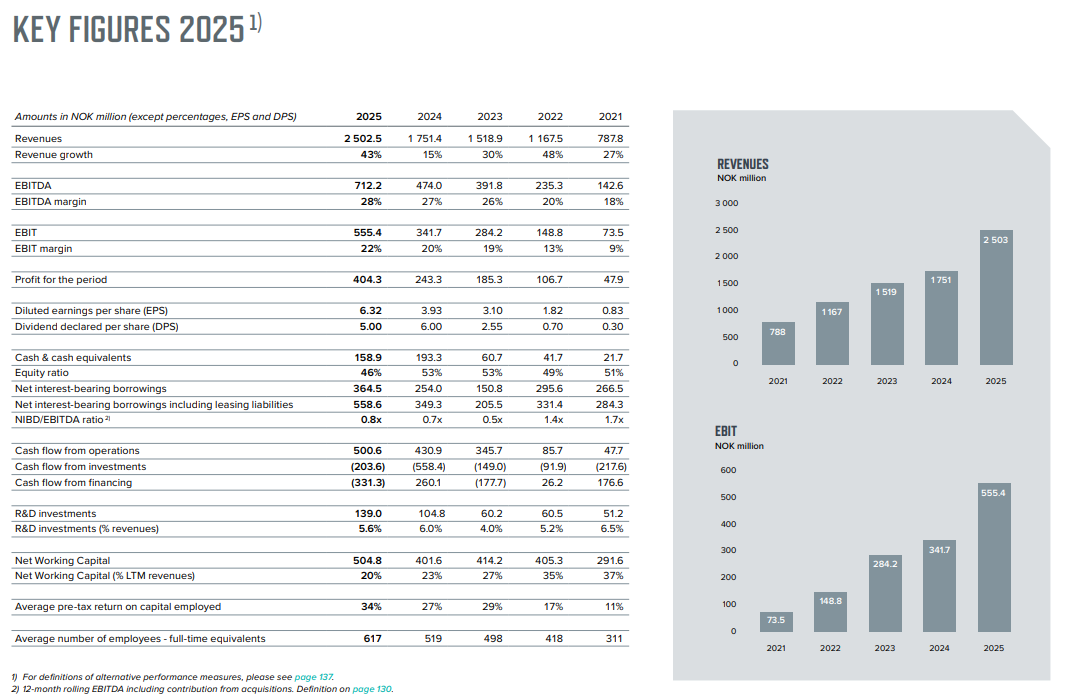

These figures estimated by the company itself total 820 -890MNOK (for Q4). Q1-Q3 revenue now stands at 1711MNOK. Thus, the range with current information would be 2530-2600MNOK for the full year 2025. This would be quite a comfortable range, as it would still leave a bit of leeway to the lower end of the guidance. EBIT-% has been 22% for the first 9 months.

All in all, a tremendous quarter and year so far. The market had slightly higher expectations, but I used this as a buying opportunity.

Valuation

The year is almost over, and one can already outline the conclusion of the current year. If the company reaches its guidance, the EV/EBIT would be 19.1-20.7x (upper end/lower end of guidance).