In 2021, Smartcraft, a leading SaaS company in the Nordic construction sector, was listed in Norway. Its goal is to increase the use of digital tools, particularly in small and medium-sized companies. The company has operations in Norway, Sweden, and Finland.

The company targets 15-20% organic growth annually, plus growth from acquisitions. Between 2017 and 2022, as many as 8 acquisitions have been made, all of which have been highly successful.

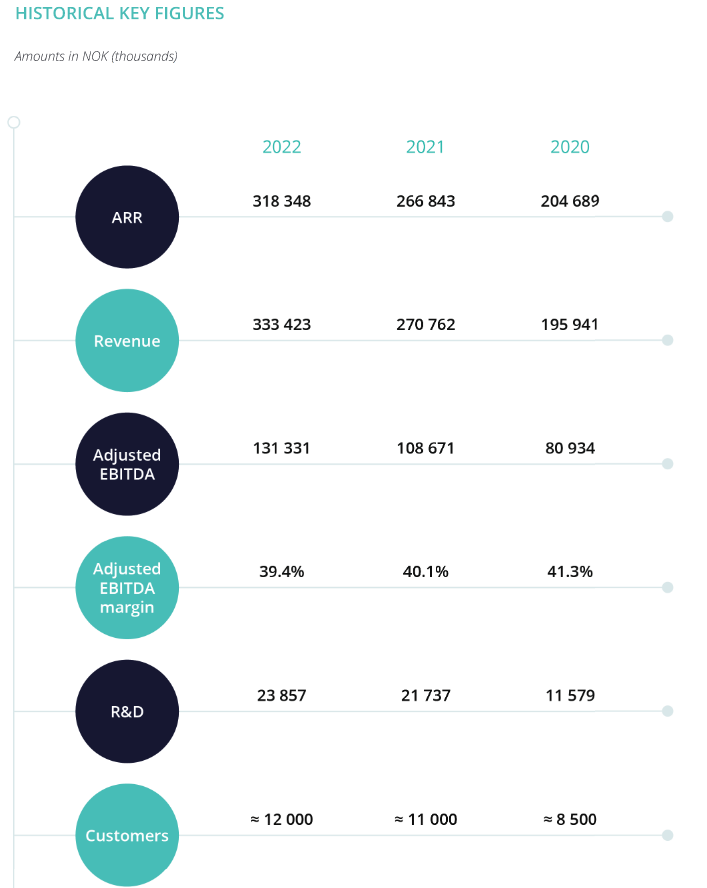

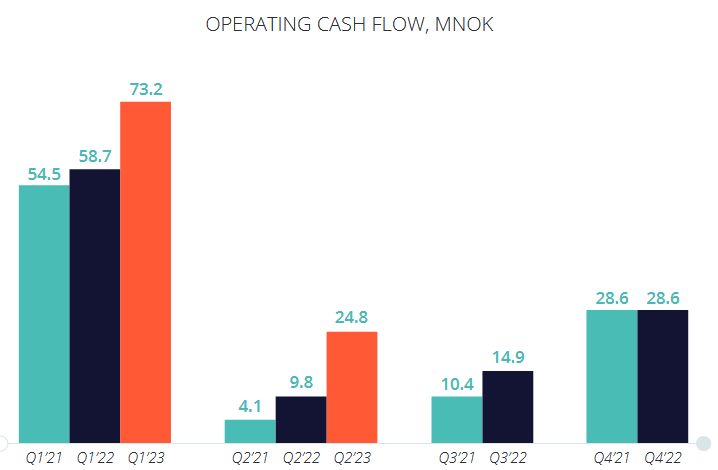

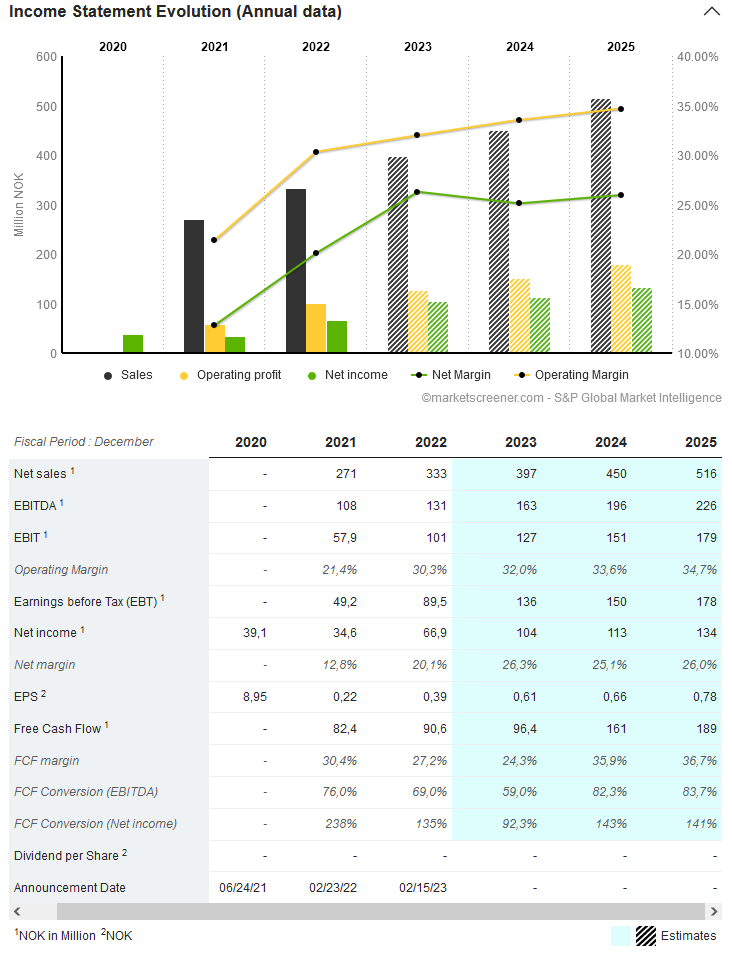

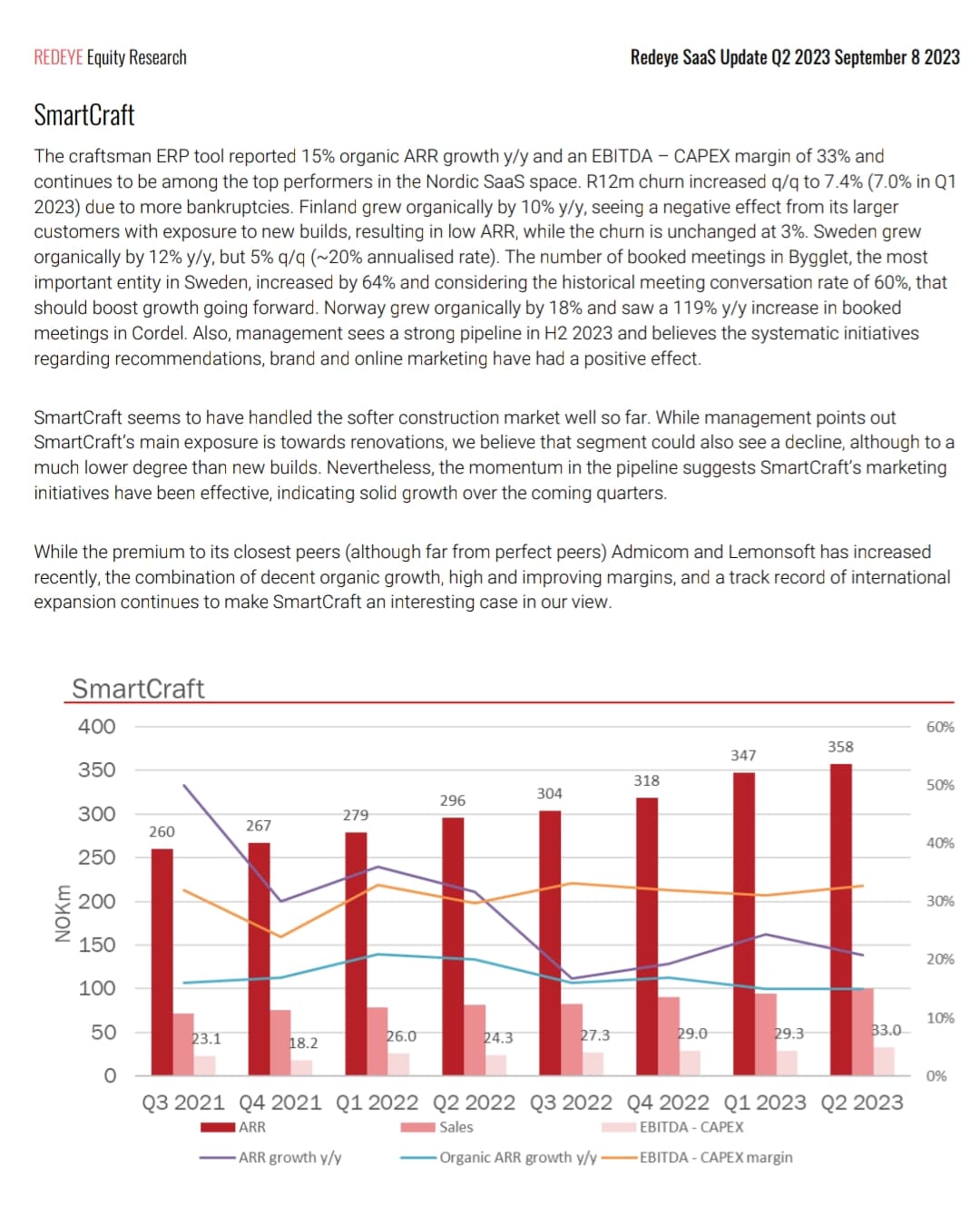

Attached are historical key figures. ARR (Annual Recurring Revenue) is a common metric for SaaS companies, used to measure recurring revenue for the next 12 months.

With this growth, I think the valuation is quite reasonable, but unfortunately, organic growth has slowed down to around 15%, and I believe Q3 will fall below that. I also believe the market will punish the share price a bit for it. Especially in Finland, growth is reportedly slowing down very sharply.

On the other hand, if growth is this fast and profitable even during bad years, this value creation train is hard to stop, and there’s plenty of market share to be taken for decades, as the digitalization of the construction industry is only just beginning

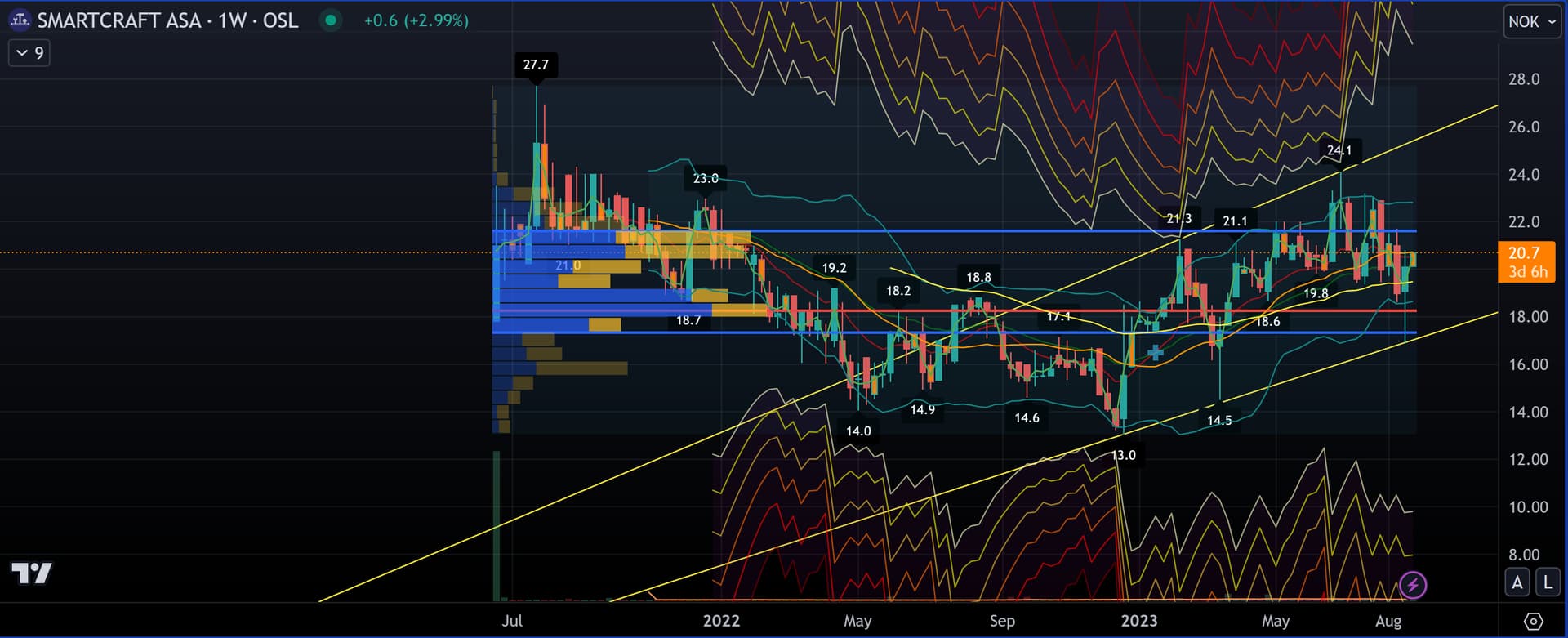

The share price has been treading water, which is very rare for a 2021 IPO company:

Here is my quick take - the megaphone pattern indicates a major price movement this year. It can help visualize the potential range going forward. POC is 18.25, value area low 17.35, and value area high 21.6.

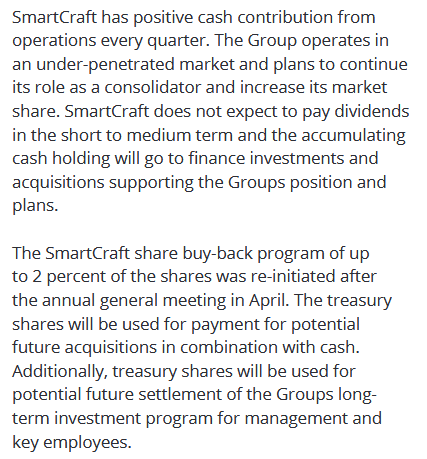

Once the jump in free cash flow materializes in 2024 → the multiples won’t look so bad anymore. Of course, it would be nice if the share price also dropped by, say, -20% at the same time

As policy rates start to decline and the Nordic construction sectors begin to recover, multiples will presumably start to expand again.

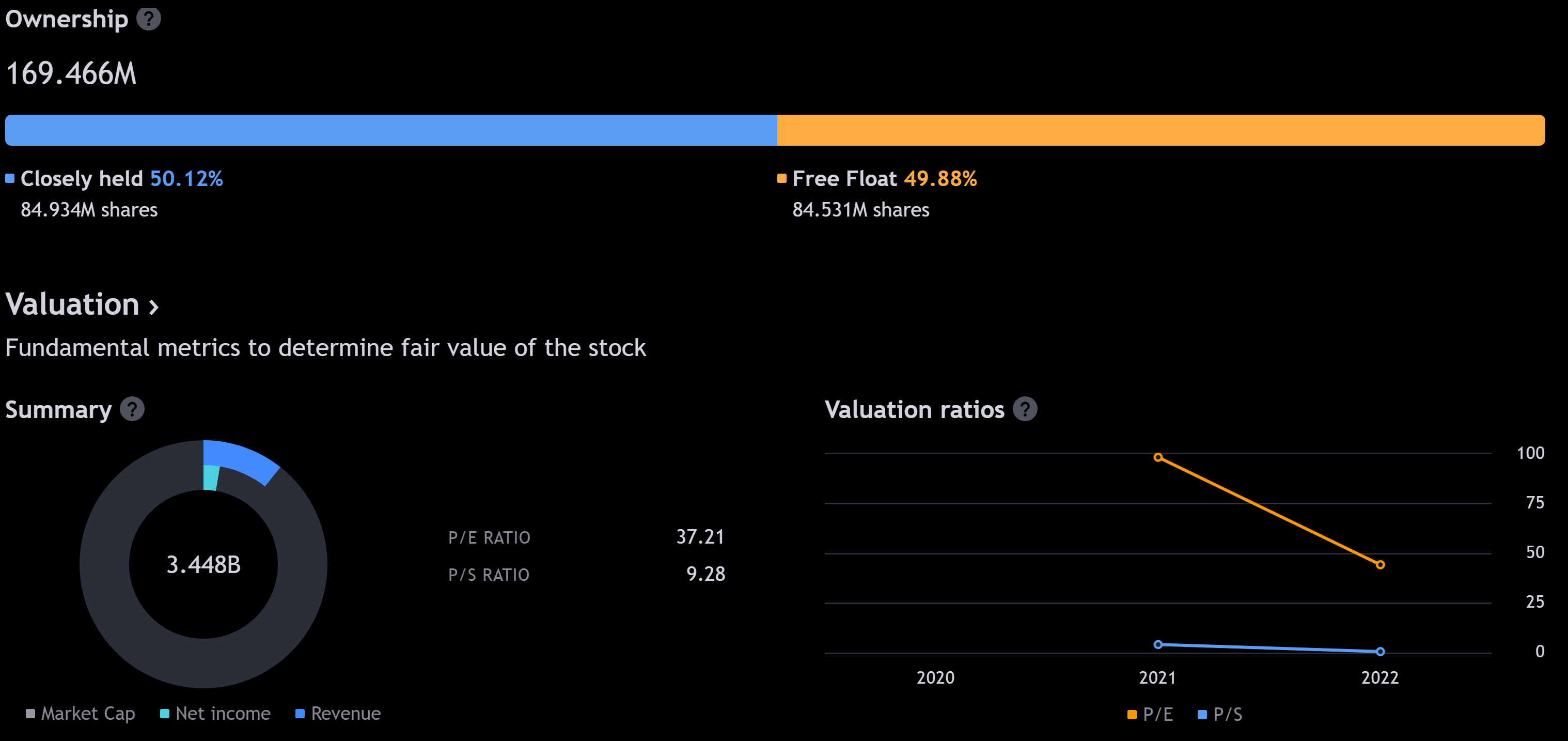

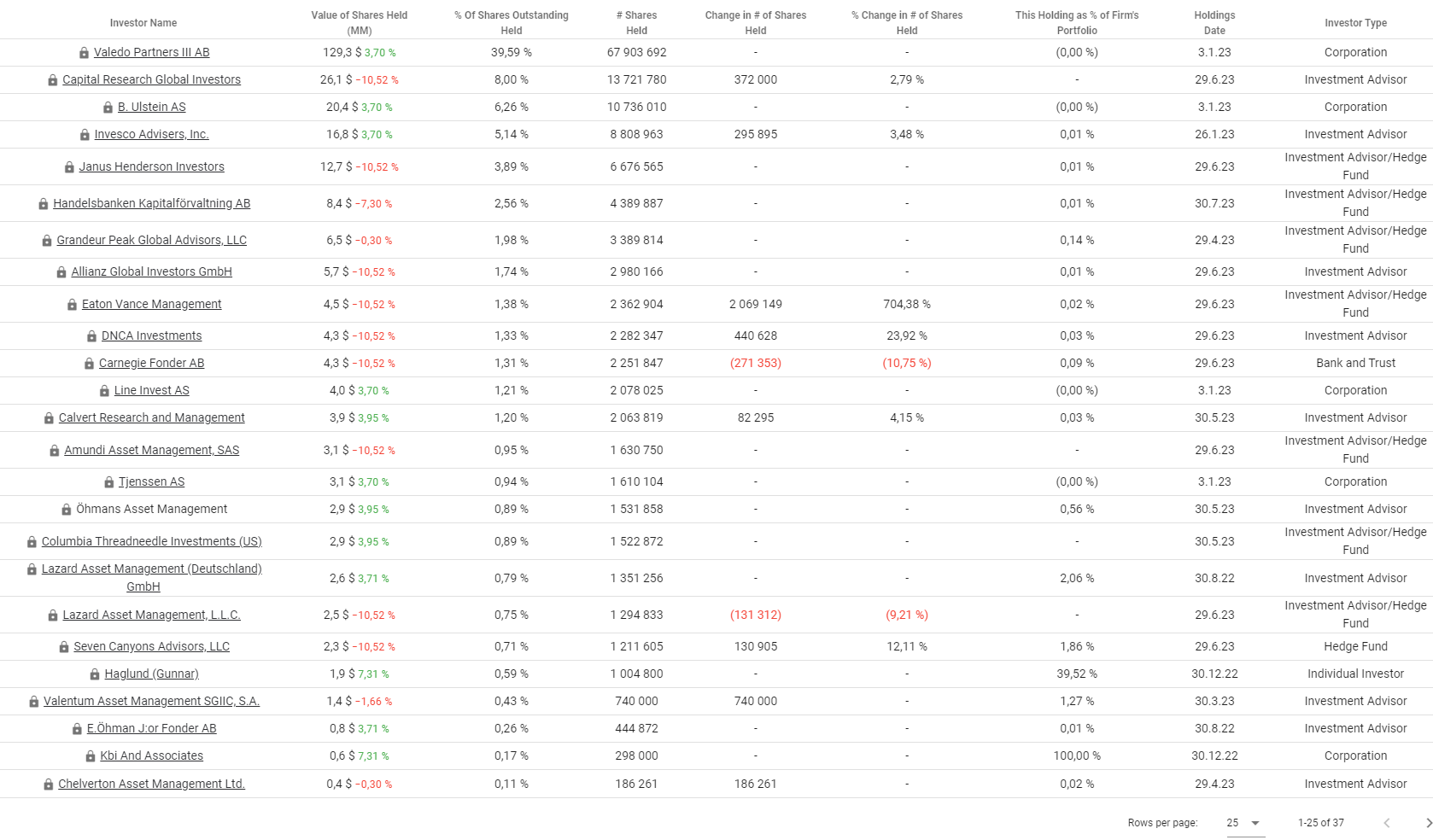

Here are the top 25 owners and ownership changes over the past few months. With the exception of Carnegie, the largest owners have made small additions.

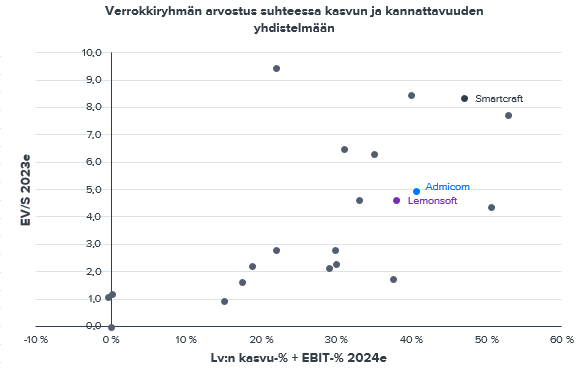

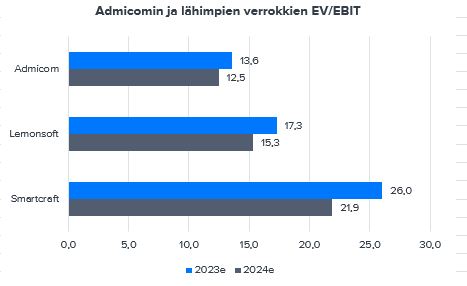

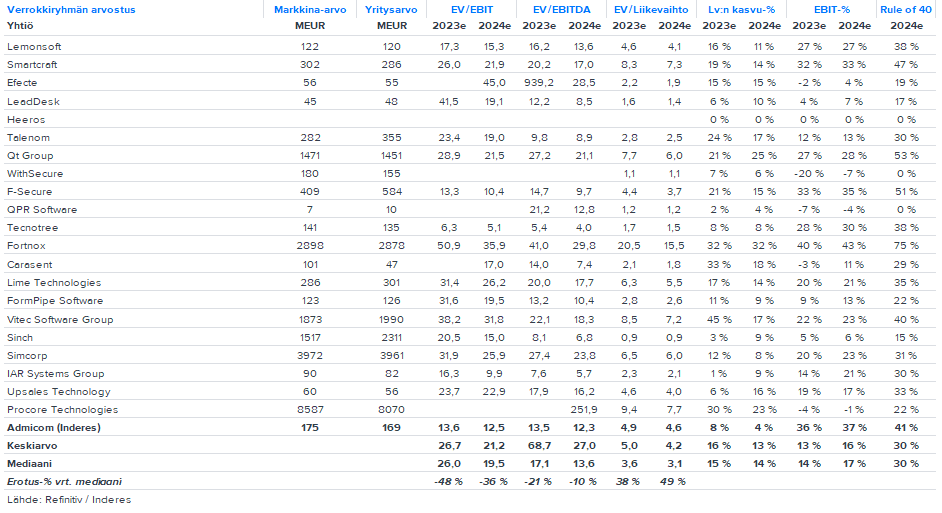

If comparing the valuation to Admicom using the EV/EBITDA multiple, it’s worth noting that Smartcraft capitalizes R&D expenses quite heavily on the balance sheet (this year’s estimate is 10-11% of revenue). Admicom does not capitalize development expenses, so comparing valuations with the EV/EBIT multiple is more consistent.

Can anyone say if Autodesk is a competitor to these construction digitalization companies (Smartcraft, Admicom)? For instance, does the “Autodesk Build” app have similar functionalities related to construction projects?

Here is an analysis of the company. The document has been translated from the other official language into English using Google Translate. Therefore, the document has some strange fonts and minor translation errors. The message comes across clearly, though.

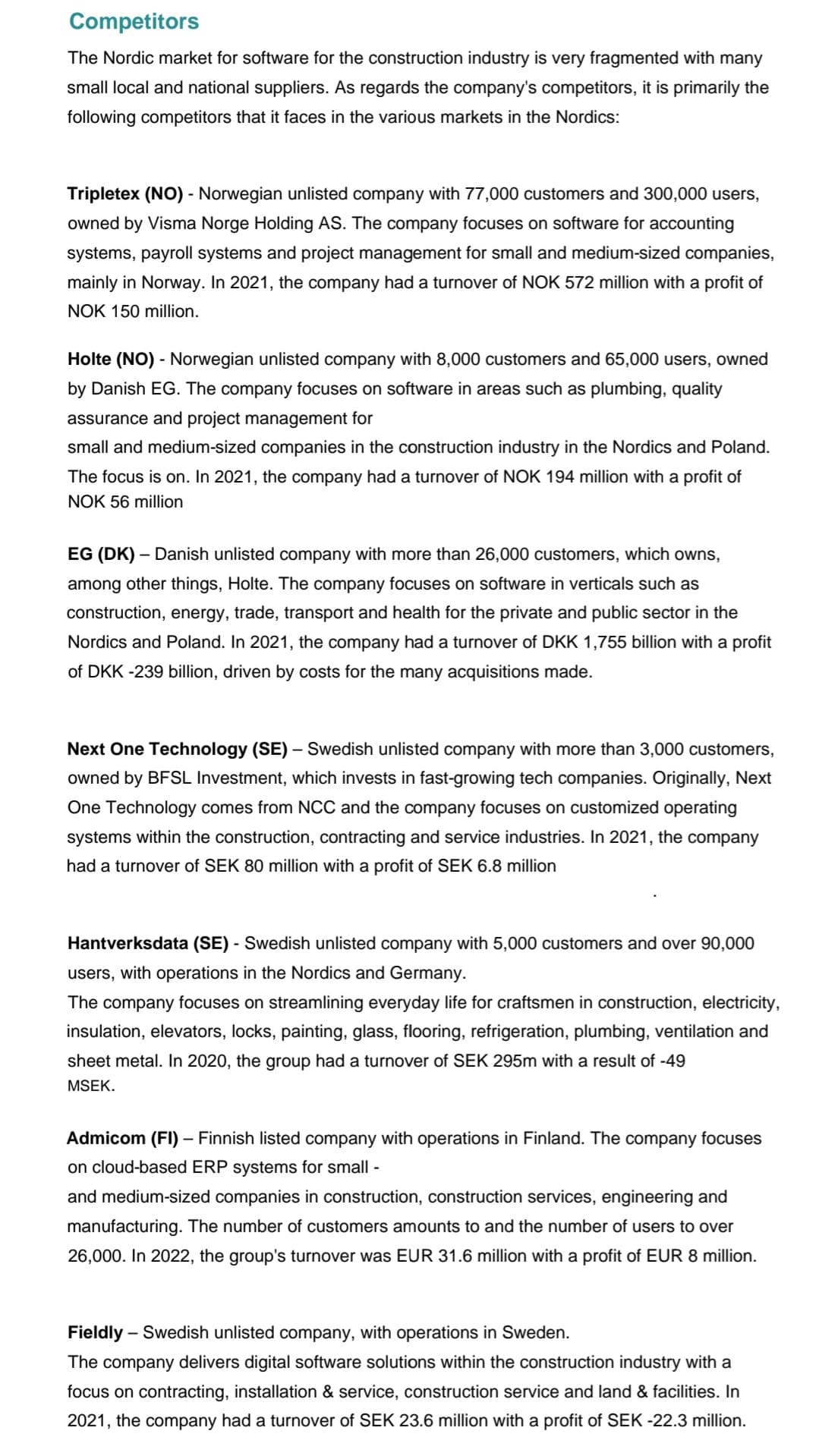

At least in the analysis I linked, Autodesk is not identified as a direct competitor. However, here are other competitors highlighted in the analysis, with Admicom mentioned.

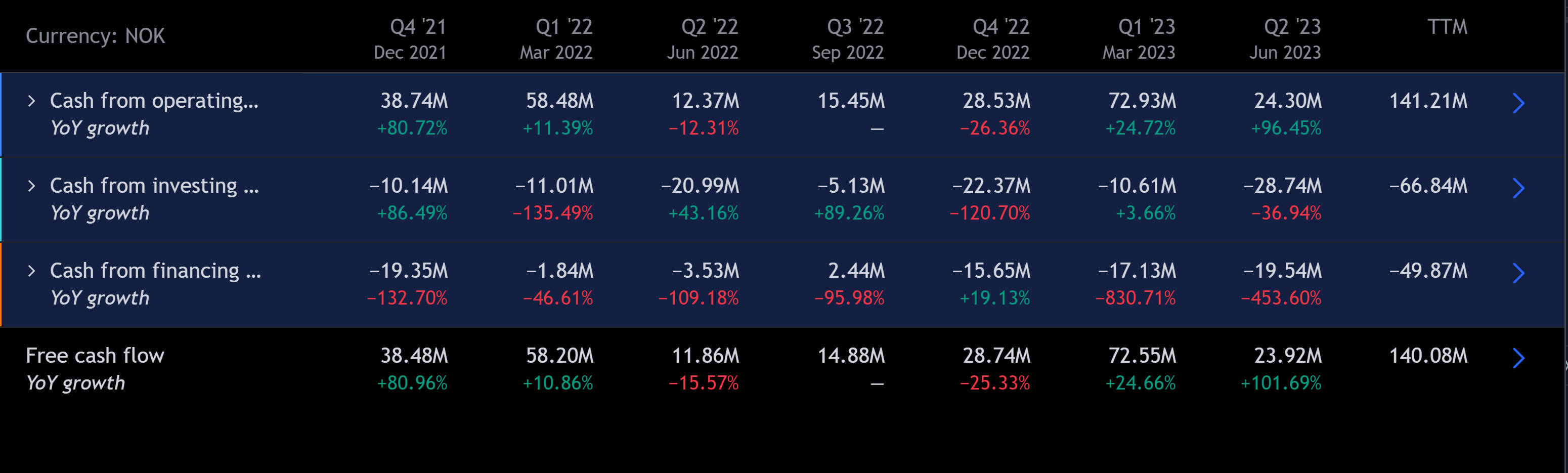

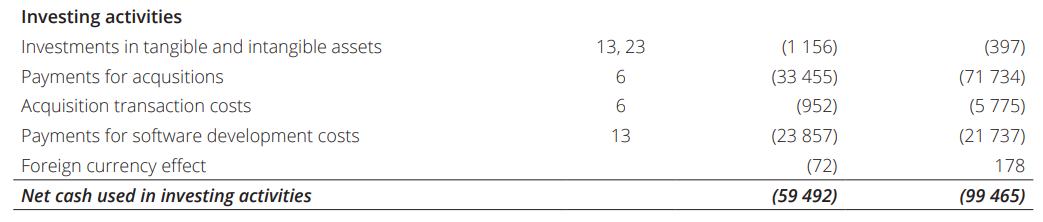

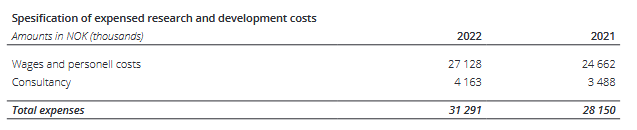

I’m going through the 2022 annual report and under investing activities in the cash flow statement, I found ‘Payments for software development costs’. Can someone smarter (literally anyone) explain in what cases that might end up there?

When software development is capitalized on the balance sheet, it is an investment in intangible assets, which is amortized annually and naturally comes out of investing cash flow rather than operating cash flow

Here is a blog post that explains that logic a bit better:

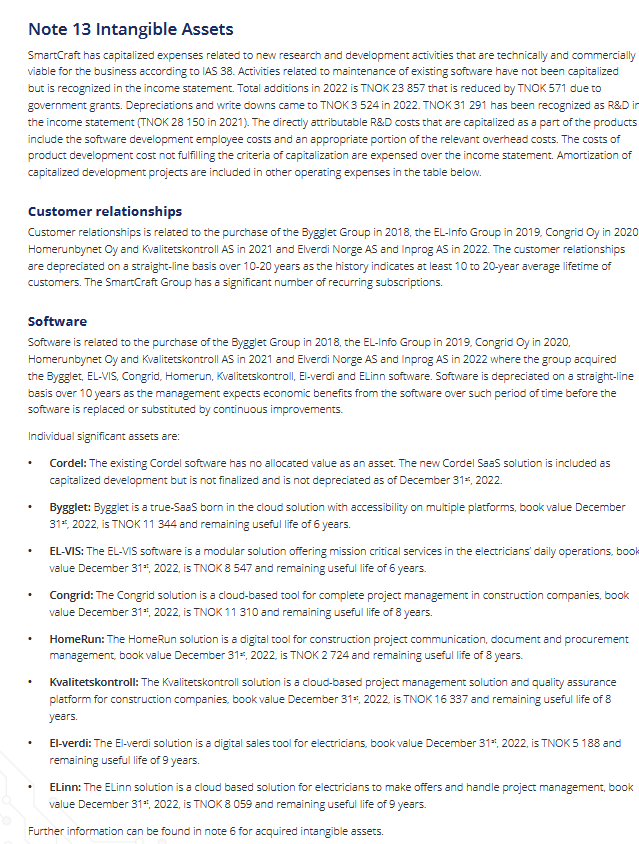

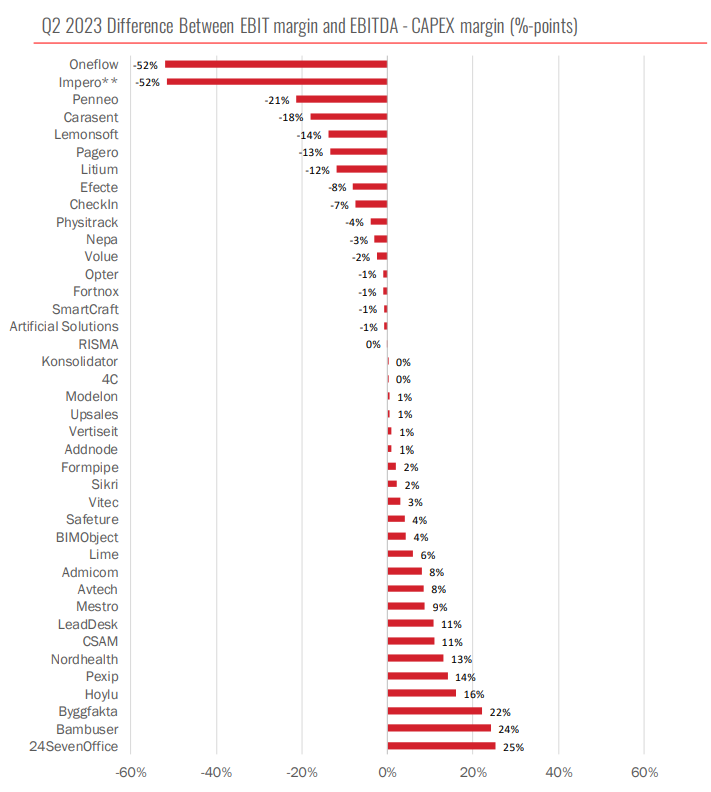

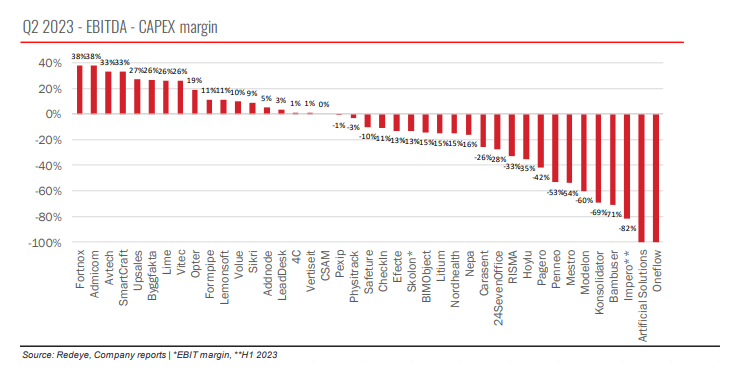

Related to this, Redeye’s recent SaaS report featured a good metric (EBITDA-CAPEX), which makes it easier to compare the profitability of different software companies. This is because some companies capitalize R&D costs heavily on the balance sheet, while others may not at all.

Sometimes, a company showing good profitability at the EBIT level, for example, can in reality generate significantly negative cash flow from its operations. Investors need to be careful with these and evaluate each situation on a case-by-case basis!

Without taking a stand on the effectiveness of that ratio, this part seemed like it was written by some Master of Business Administration who has never set foot in a factory in their life

Selling a modern factory line specialized in a few gadgets isn’t usually a fast process (nor does it sell for anywhere near its book value), and you constantly have to be investing more and replacing capital wear.

In comparing financial ratios, the greatest benefit is that they speed up various calculations. I wonder if EBITDA - CAPEX becomes too complex of an adjustment compared to just using cash flow figures directly?

I wasn’t quite at the level yet where I read the attachments, but I guess I have to

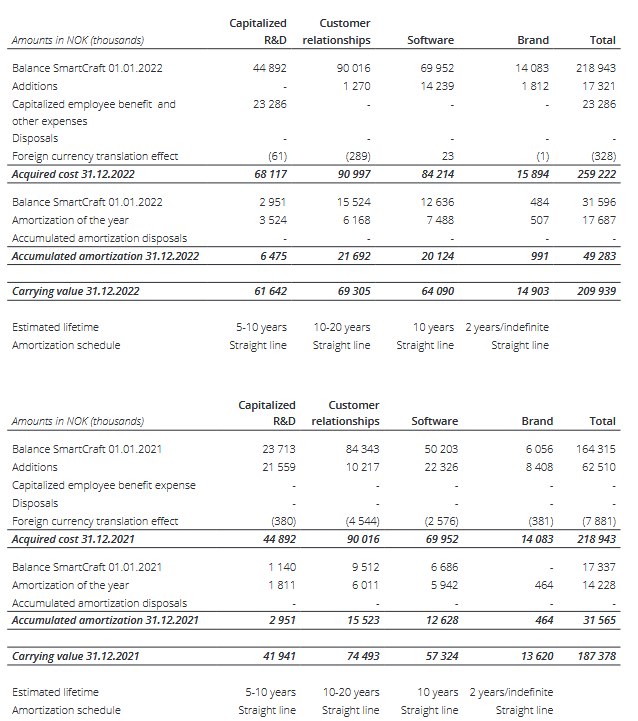

I went through the attachment now and yeah, this looks like ‘we decided to define this part of the work as an investment because we’re allowed to’.

Okay, fair enough, but it’s hard for me to imagine that a software firm’s development costs would fluctuate in a way that they couldn’t be on the payroll. I suppose they are in both now.

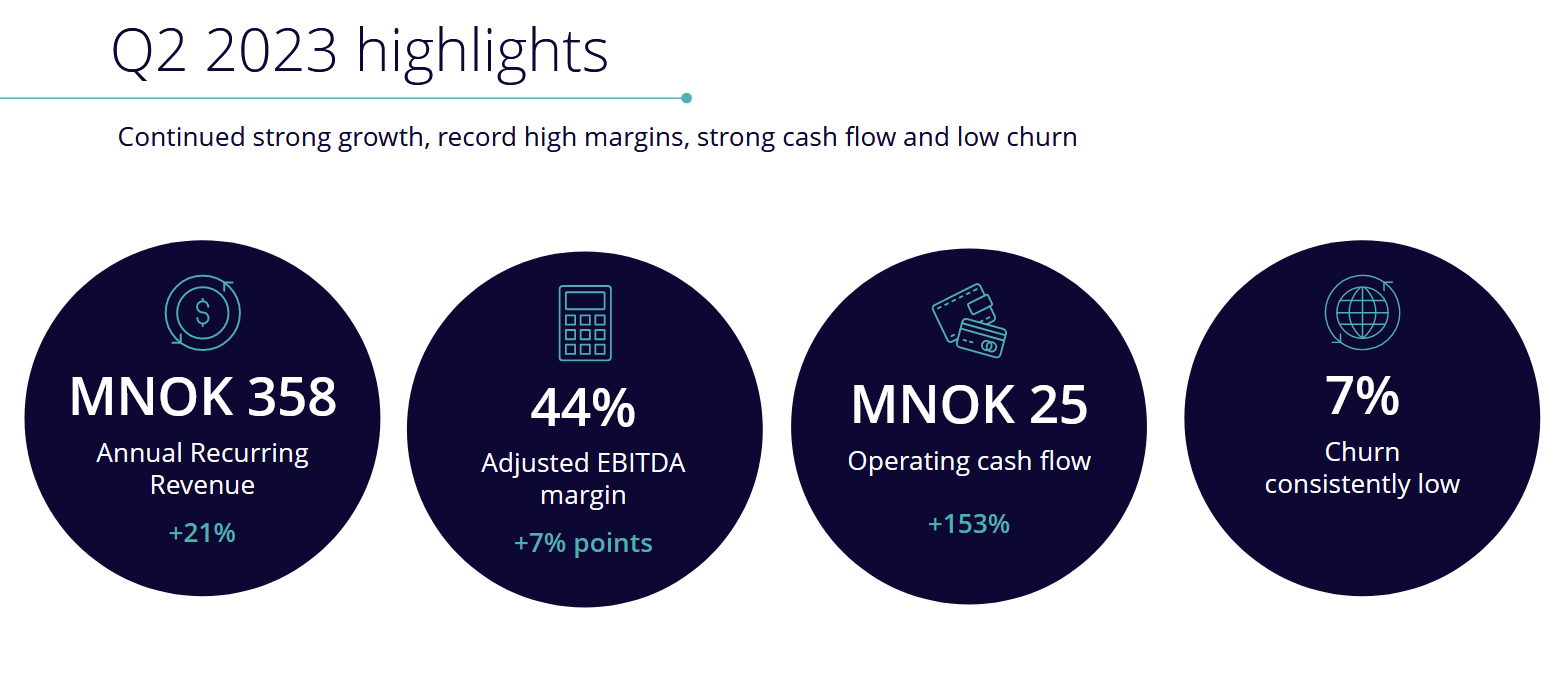

It seems the slump in Finnish construction has dampened the discussion, but SmartCraft just keeps powering through. The Q3 figures released today were typically strong. ARR rose by 21 percent, with organic growth accounting for 14 percent. The growth drivers were, of course, Sweden and Norway, but even in Finland, ARR grew organically by 4 percent.

The reported EBITDA margin increased by 3 percentage points to 42 percent. Cash flow was good. There was a slight increase in churn, but even this was showing signs of improvement towards the end of Q3. The outlook is positive, and confidence in profitable growth remains strong.