www.argeo.no

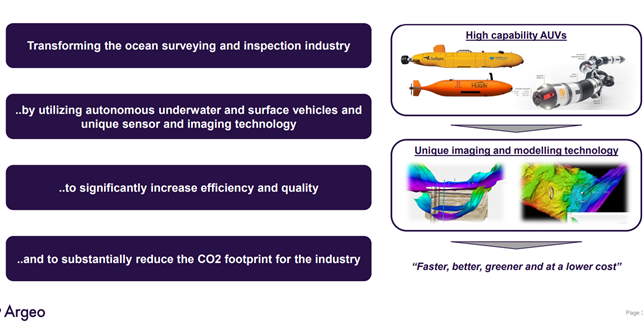

Argeo focuses on seafloor imaging and digitalization (mapping) using smart, lightweight robotic technology (AUV, robotics). The company was listed on Euronext Growth at the end of March with the ticker ARGEO. The company’s strengths include technological advancement compared to “traditional imaging” and a strong pipeline.

Argeo’s specialty is providing survey and inspection services to industries installing, constructing or maintaining infrastructure or equipment in the oceans. Argeo provide these services primarily by acquiring data using advanced AUVs, and resident robotics systems for then to apply advanced integrated processing and interpretation creating a high resolution digital representation of the seafloor and the sub-seafloor.

The Group also provide exploration services using the same robots, but with specialized sensors to characterize the deep ocean space seafloor for high value DSMs (deep sea minerals) used in the electronics and renewables industry

The company’s history dates back to 2014 in Norway.

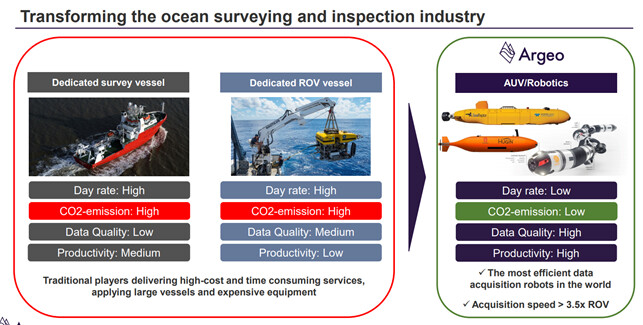

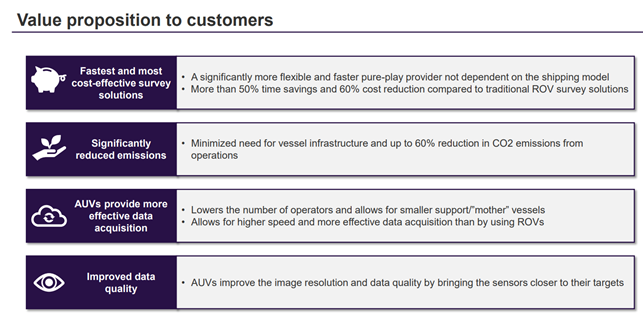

Thanks to its technology, the company can significantly reduce the environmental impact of seafloor imaging. The company purchases lightweight robots (AUVs) externally but develops sensors itself (a technological competitive advantage combined with AUV use). As far as I understand, the sensor side is a key factor in forming a competitive advantage in its peer group, as anyone can buy an AUV. In addition, the use of AUVs, which can often be deployed as a container solution on smaller vessels than actual ROVs (remotely operated vehicles) where people are directly involved in controlling them, should also provide a competitive advantage.

Argeo has gone to great length in qualifying the Group’s processing and integrated 3D

modelling tools and services developed by the group since 2018 aiming to provide customers with significant value uplift for ocean space construction and installation projects

AUVs allows the Company to get closer to the area of examination which enable a higher resolution imaging as compared to surface survey vessels and ROVs. Especially in deep waters, data acquired from surface survey vessels are from management’s experience at too low resolution to discover or image the seafloor, objects or commodities sought after in the DSM vertical.

The general presentation I used can be found here:

The company states that its business provides added value, e.g., in terms of cost savings, reduced environmental impact, and better data quality.

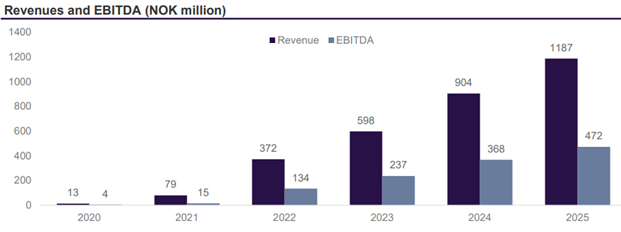

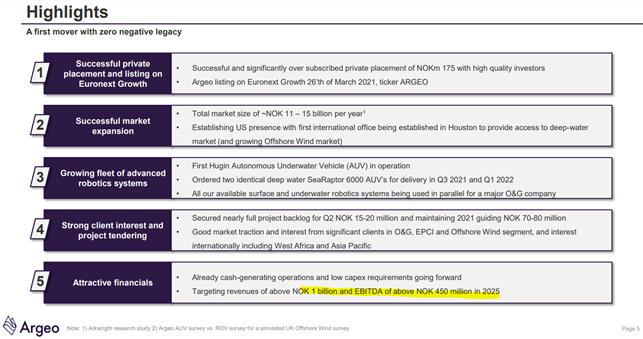

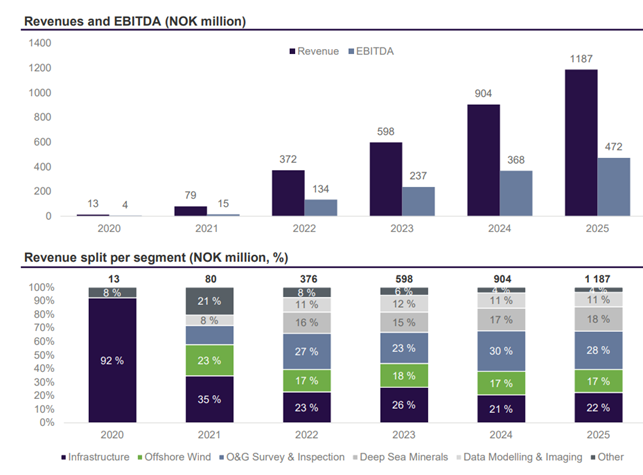

Highlights and company guidance for 2025:

- The goal is 1 billion NOK in revenue and 450 million NOK in EBITDA.

The company’s revenue comes from four different segments:

-

EPCI is imaging related to marine construction

-

offshore wind is imaging related to wind turbines (TAM NOK 950m annually)

-

Oil & Gas is imaging for the needs of the oil and energy industry (Norway TAM NOK 1.5-2.0 bn / Global TAM NOK 15-20bn)

-

Deep Sea Minerals focuses on the exploration of deep sea minerals

Argeo can offer its products and services to the following markets:

Infrastructure

o Data acquisition, imaging and underground modelling for large infrastructure projects and aquaculture

o High accuracy imaging needed to reduce project risk and construction costs combining services from

the Group and Multiconsult expertise in geotechnical and construction engineering.

o Digital construction grade integrated 3D geological models used for detailed input to building and

installation design.

o Life-cycle sub-surface Digital Twin solution for future inspection, monitoring and maintenance

Offshore wind

o Input to wind farm design, including design and location of foundations, substations which include

environmental impact analysis before installation.

o Investigation of routes for power cable and assessment of environmental impact

o Inspection of existing infrastructure

o Digital construction grade integrated 3D geological models used for detailed input to building and

installation design.

o Life-cycle sub-surface Digital Twin solution from installation including future inspection, monitoring

and maintenance to end-of-life decommissioning

Oil and gas

o Input to offshore field design, including design and location of platform and subsea infrastructure

o Seabed habitat and environmental impact and assessment analysis

o Investigation of routes for pipelines and environmental impact assessment.

o Detection damage/erosion on existing installations

o Life-cycle sub-surface Digital Twin solution for future inspection, monitoring and maintenance to endof-life decommissioning

DSM

o Exploration and characterization of DSMs using specialized deep sea autonomous robots

o Wide use of sensors and in-house Mineral Hunter-system under development by Argeo Robotics

o Significant upside in future multi-client data library developed

o Strong in-house competence in multi-sensor data processing, Digital Twin modelling for exploration

service

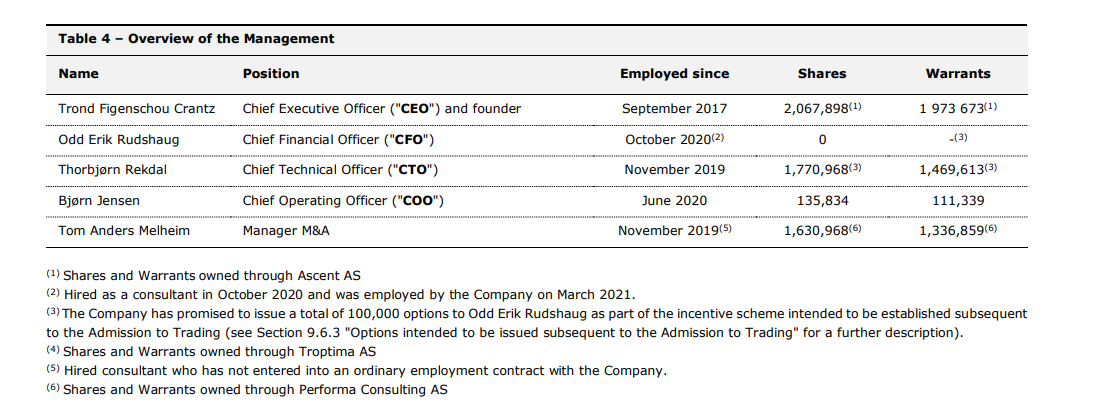

Management has extensive experience and a vested interest

and the board of directors:

Lock-up:

As part of the Private Placement, the Company, certain shareholders owning 1% or more of the Company and members of the Company’s board of directors and management entered into customary lock-up arrangements with the Managers for a duration of 12 months, respectively, following the admission to trading on Euronext Growth Oslo

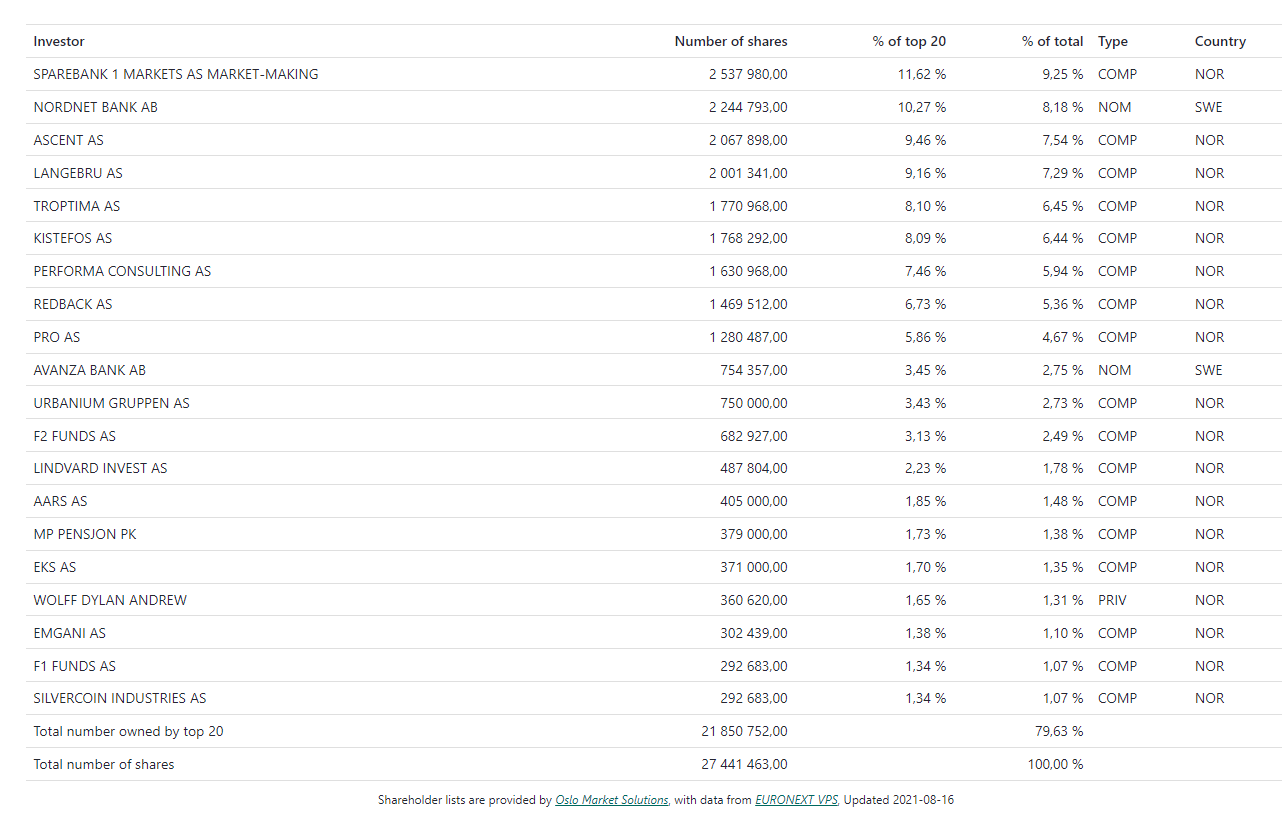

TOP Shareholders

https://argeo.no/investor-relations/largest-shareholders/

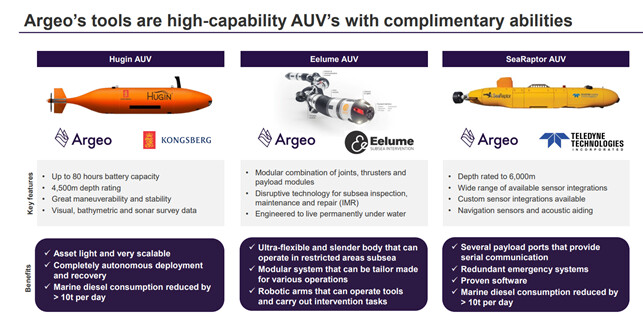

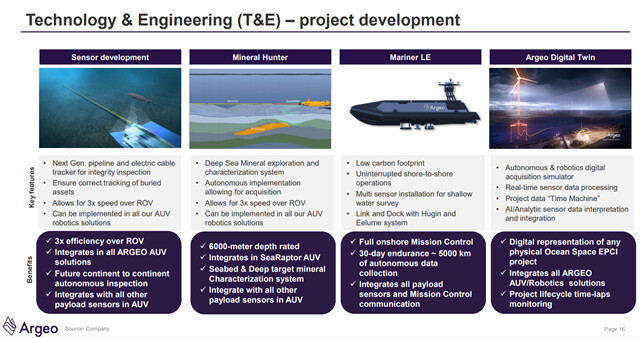

Technology (briefly)

More detailed information on the technology can be found in the company’s slide decks.

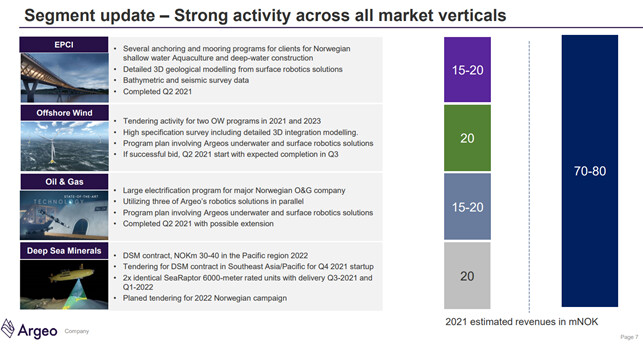

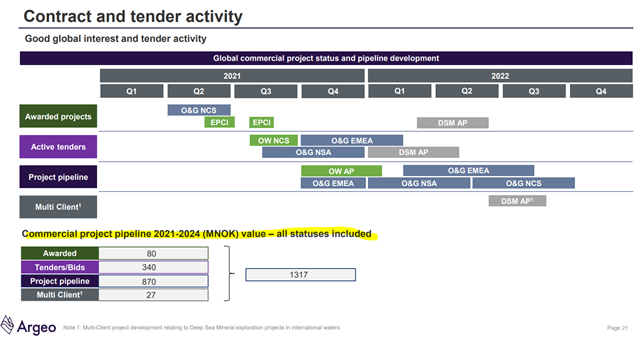

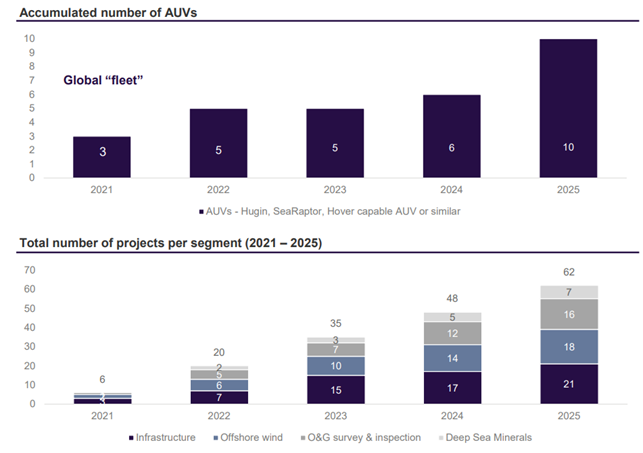

Pipeline

The potential current pipeline is approximately 1.3 billion NOK (not all of it is “in the bag” yet).

On the numbers:

The company’s 2022 guidance aims for an approximate 40% utilization rate. About 20% would be sufficient for break-even.

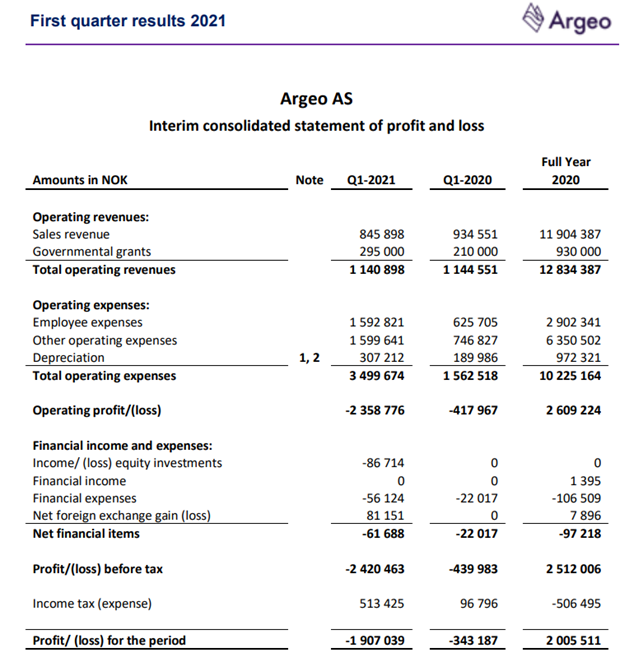

Q1 report

Guidance:

The company maintain its initial 2021 revenue guiding of 70-80 million NOK and expect revenues between 15 to 20 million NOK for Q2-2021

Q2 update (interim report due on 25.8.)

IPO Admission:

Risks are certainly:

-

The author of this text does not have deep knowledge of the substance of seafloor mapping.

-

Cyclicality of the industry (?)

-

Break-even expected in 2022?

-

Technology, i.e., why couldn’t others set up a similar company by developing and acquiring similar technology?

-

The pipeline’s visibility is not necessarily “years ahead,” as indicated by the guidance?

-

Not a risk, but the stock has had relatively weak liquidity.

-

The young age of the industry, legislation, key personnel- No patents (Argeo does not currently hold any patents. However, Argeo has engaged a patent lawyer firm in a process for writing a patent application related to inspecting an object near or at the seafloor and are in the process of writing two additional patent application relating to inspection and exploration for DSMs, including applications relating to inhouse “Mineral Hunter” which is based on a Company invention providing important information on DSMs.")

-

Competitive landscape

Other:

Sparebank 1 16.8.2021:

We initiate coverage of Argeo with a Buy recommendation and NOK 18 target price. Argeo targets to transform the ocean survey and inspection industry with Autonomous Underwater Vehicles (AUVs), which are faster, cheaper and greener than conventional ROVs. The AUV market is expected to double by 2025 and surpass the ROV market in size by 2030. Argeo is the only pure-play provider of AUVs in the market, and has an asset light and flexible setup with low required utilization for break-even. We see revenues increasing from NOK 66m in 2021e to NOK 506m in 2024e, driven by ramp-up of the AUV fleet and increased utilization, with EBIT margin increasing from 5% to 27% in the period. Note that Argeo’s own revenue estimates are 46-79% above our estimates for 2022-24, meaning there could be upside to our estimates. We calculate EV / EBIT or 4.2x / 1. 8x in 2022-23e and P / E at 6.3x / 3.1x, which is very low both on an absolute basis and vs peers. If Argeo delivers on estimates, we see vast upside beyond our NOK 18 target price.

Disclaimer: This writing is not an investment recommendation. I encourage everyone to do their own due diligence. ![]()