Cambi has been discussed a few times in different places, so I decided to create its own thread for it. Perhaps this way we can gather even the little discussion in one place.

The introduction is largely the same as this pitching competition entry. Of course, I made some additions and updates.

What the company does

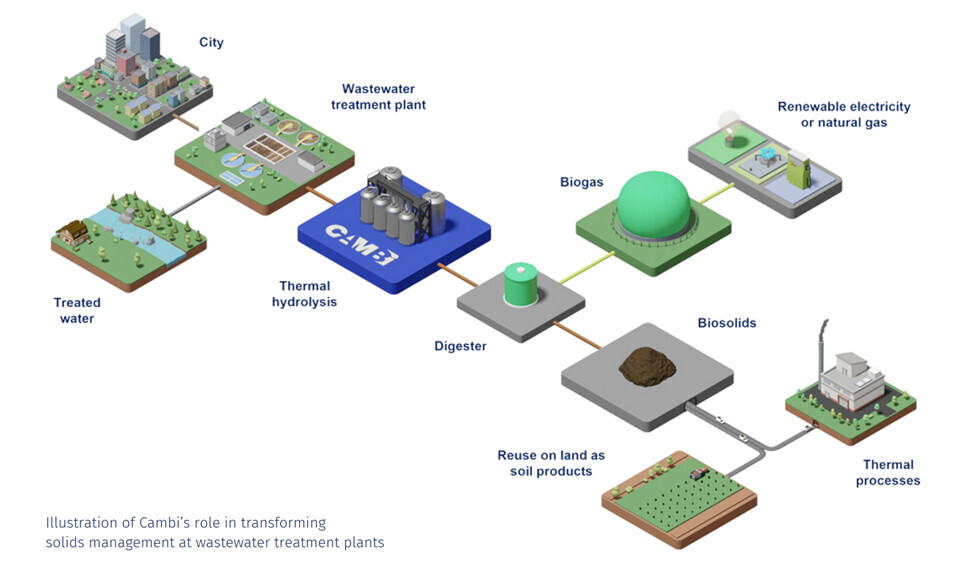

Cambi ASA is a Norwegian company and the world’s leading provider of Thermal Hydrolysis Process (THP) solutions for the treatment of wastewater sludge and organic waste. The company developed the thermal hydrolysis process in the early 1990s and has since become a well-known and reliable technology supplier in advanced anaerobic digestion and biogas solutions. Due to its long history, the company should have a good number of patents protecting it.

Video of the process:

https://vimeo.com/870276237

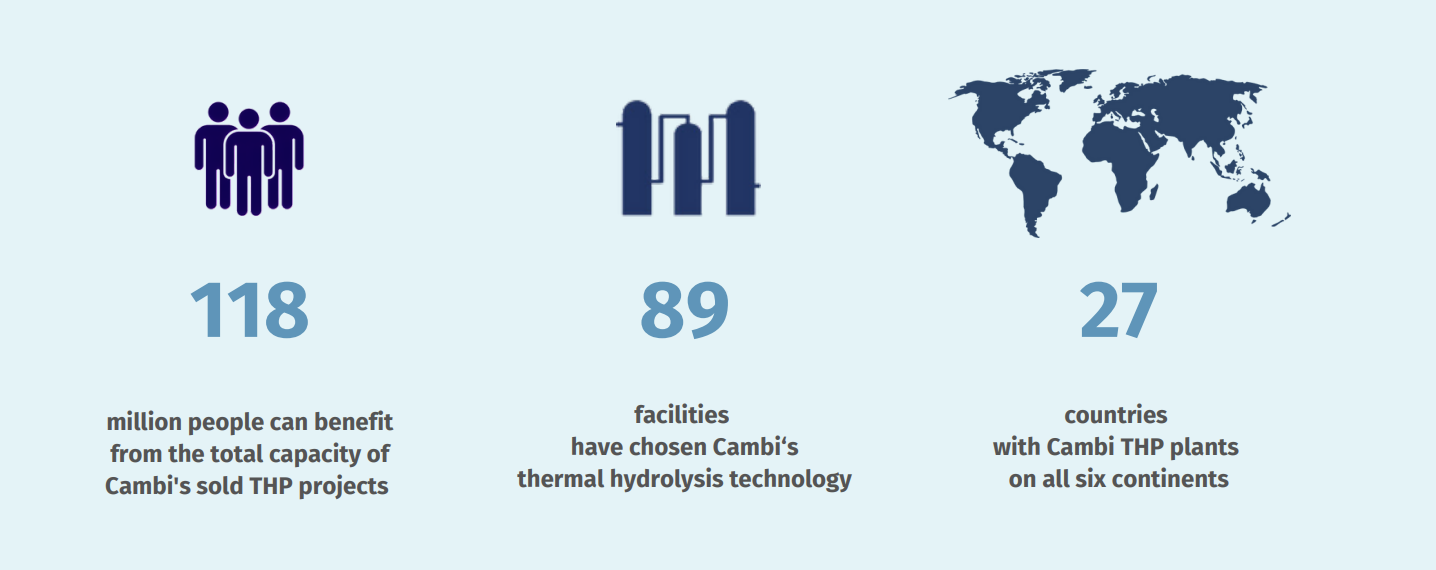

The company itself has stated that it is the market leader in its technological niche with up to 90% global market share. There are currently 89 facilities in 27 different countries, processing the waste of 118 million people.

Thermal Hydrolysis

How it works

- Heating and pressurization: Sludge is heated to high temperatures (approx. 150-170°C) and subjected to high pressure (approx. 7 bar) using steam.

- Cell disintegration: This combination of heat and pressure breaks down the cell walls of microorganisms in the sludge, releasing water and organic matter.

- Rapid depressurization: The sludge is rapidly depressurized, causing further breakdown of organic matter.

- Resulting product: The end product is a more liquid sludge that is easier to handle and further process.

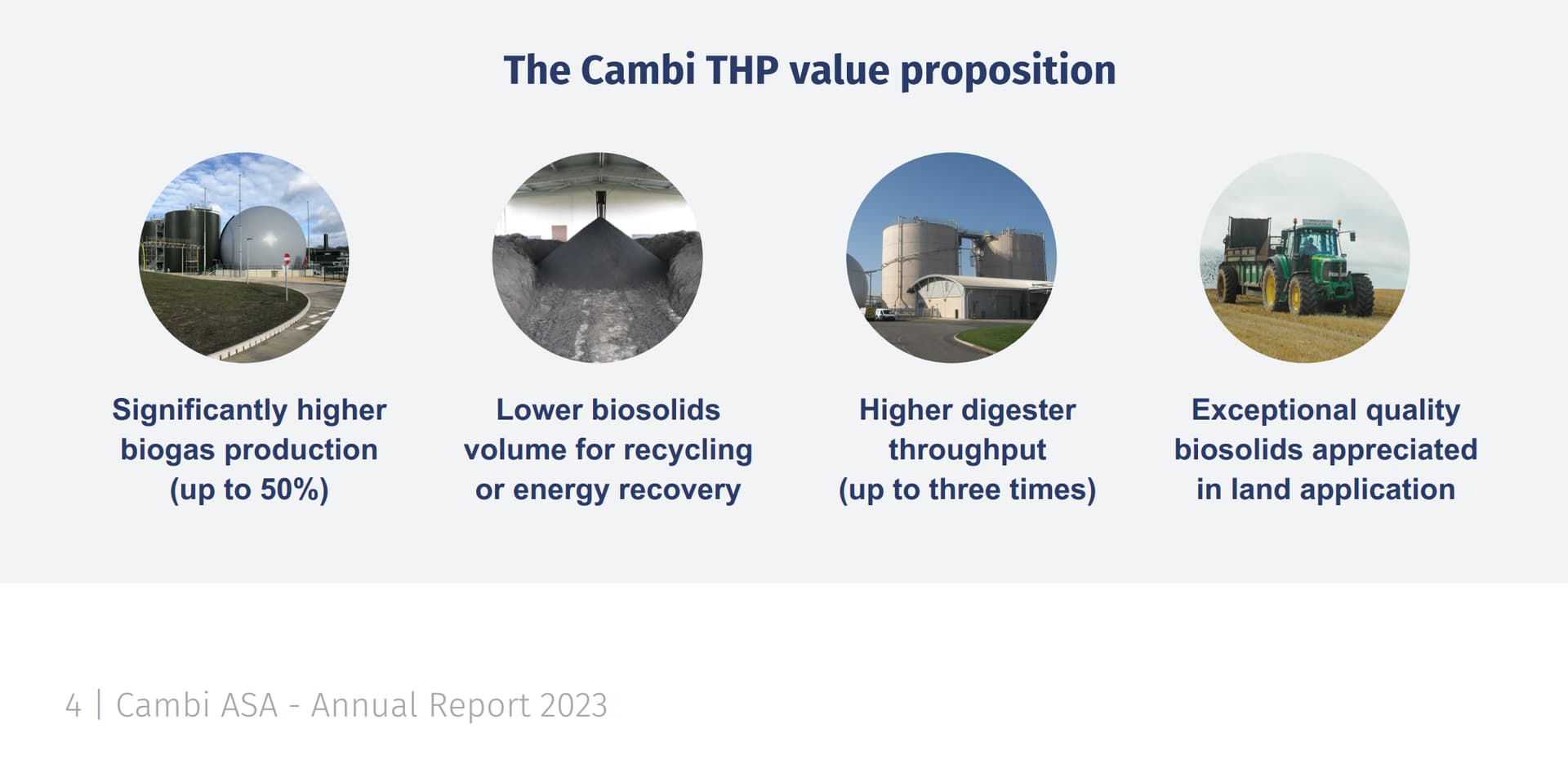

Benefits

- Improved biodegradability: The process makes sludge more biodegradable, which improves the efficiency of subsequent treatment processes, such as anaerobic digestion.

- Pathogen reduction: It sterilizes the sludge, destroying pathogens and making it safer for agricultural use.

- Volume reduction: With the breakdown of organic matter, the volume of waste is significantly reduced.

- Energy production: The process produces biogas, which can be used as a renewable energy source.

- Improved dewaterability: Treated sludge is easier to dewater, reducing disposal costs.

This process is widely used in wastewater treatment plants to improve the overall efficiency and sustainability of waste management.

Considerations

- Costs: Thermal hydrolysis systems can be expensive to install and operate.

- Complexity: The process requires advanced equipment and skilled operators.

- Energy consumption: It consumes a significant amount of energy, although this can be offset by the biogas produced.

Alternatives

- Anaerobic digestion: Effective in biogas production and sludge volume reduction, but may not achieve the same level of pathogen reduction.

- Composting: Good for producing soil conditioner, but requires space and time.

- Chemical treatment: Can be simpler and cheaper, but not necessarily as effective in volume reduction or energy production.

Business segments

The company introduced new business segment divisions at the Q3 2023 CMD.

Technology:

This includes the design, manufacturing, and installation of THPs. This accounts for 75% of revenue.

Solutions:

This includes maintenance of installed equipment, spare parts, expansions, etc. (i.e., fairly continuous revenue), as well as Grønn Vekst, which packages and distributes material derived from waste in Norway, used, for example, in gardens. For instance, the field of the Ullevaal athletics stadium has been made with these materials.

The Technologies segment is slightly more profitable. Its gross margin percentage has been above 50%, while for the Solutions segment it is approximately 45%.

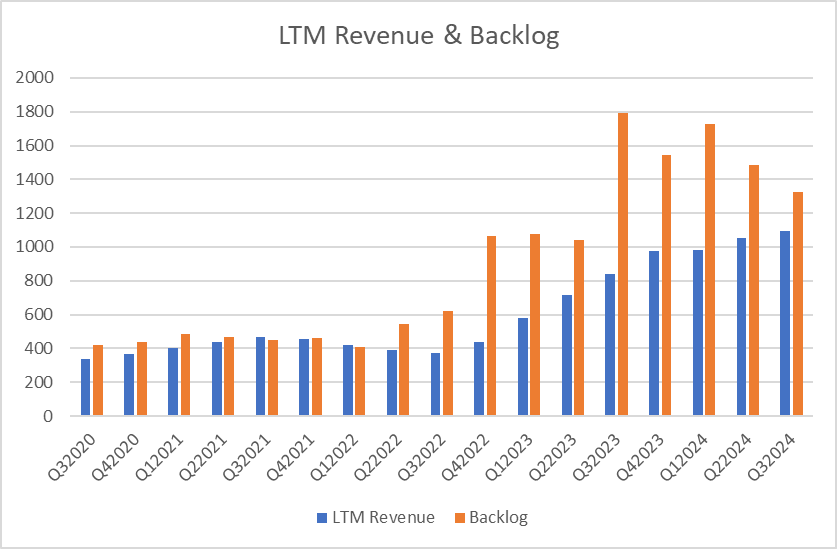

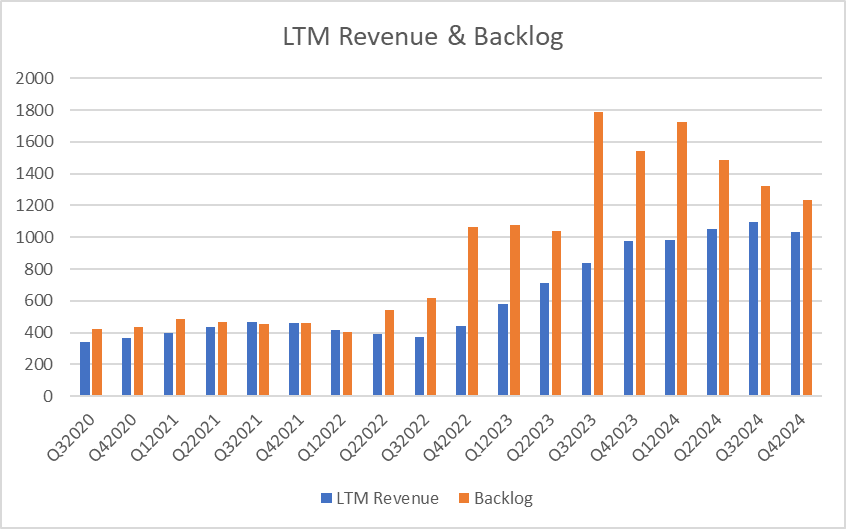

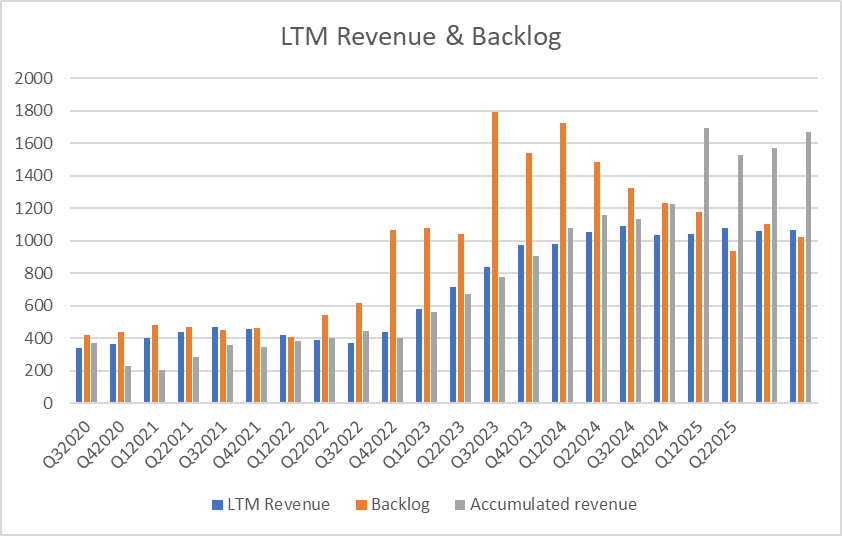

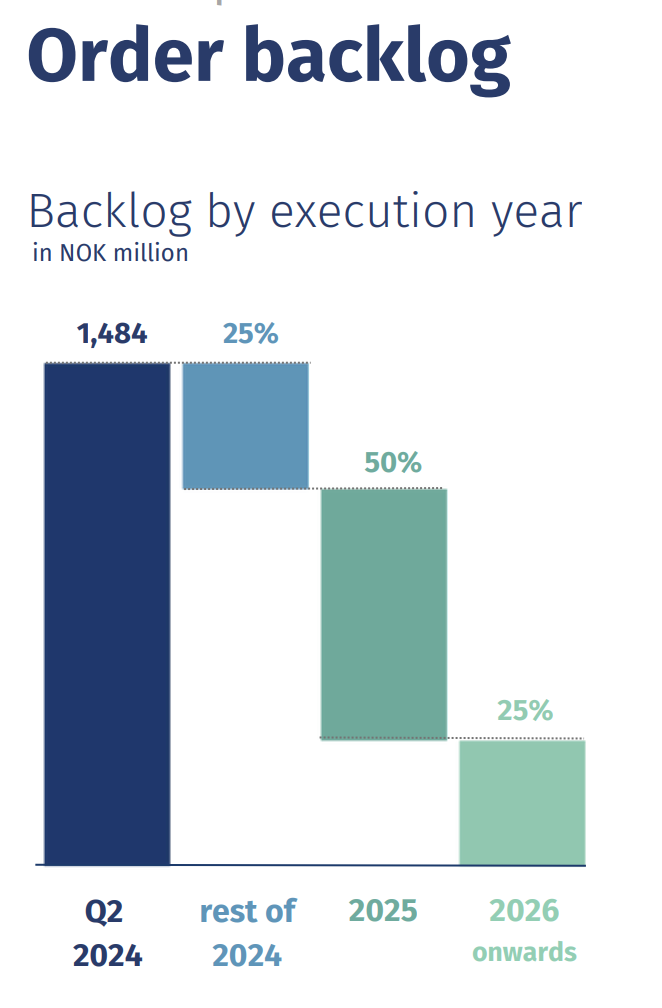

Their order backlog is currently distributed as follows.

Financial situation

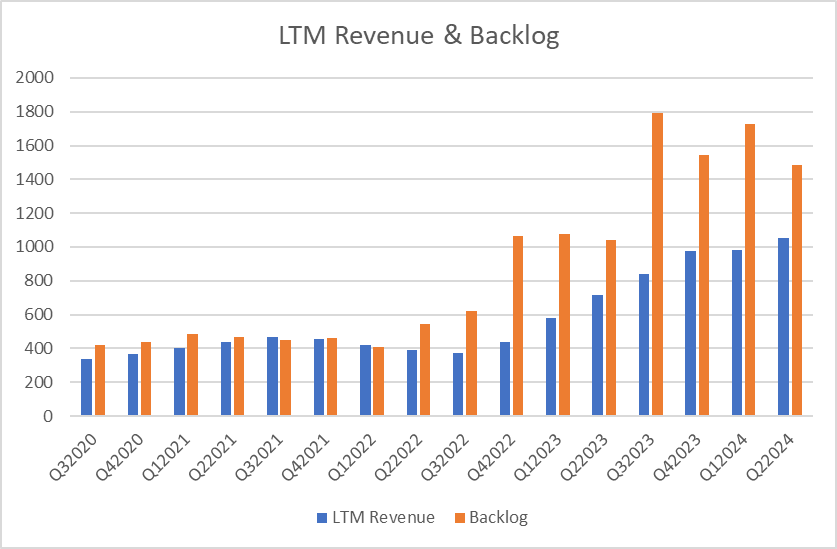

In 2022, Cambi’s order backlog took a big leap, which has naturally started to reflect in revenue.

I haven’t thoroughly investigated the reason for this leap.

Projects last approximately 2-3 years, and the order backlog is currently expected to convert into revenue according to this timeline.

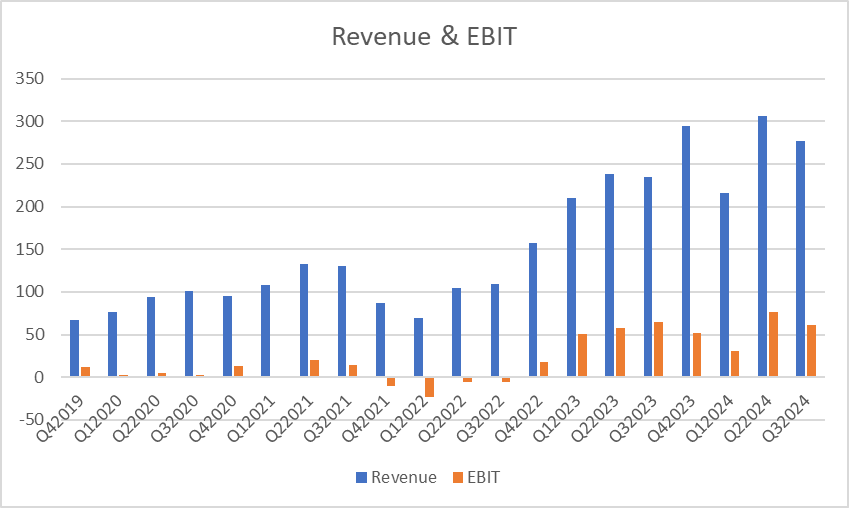

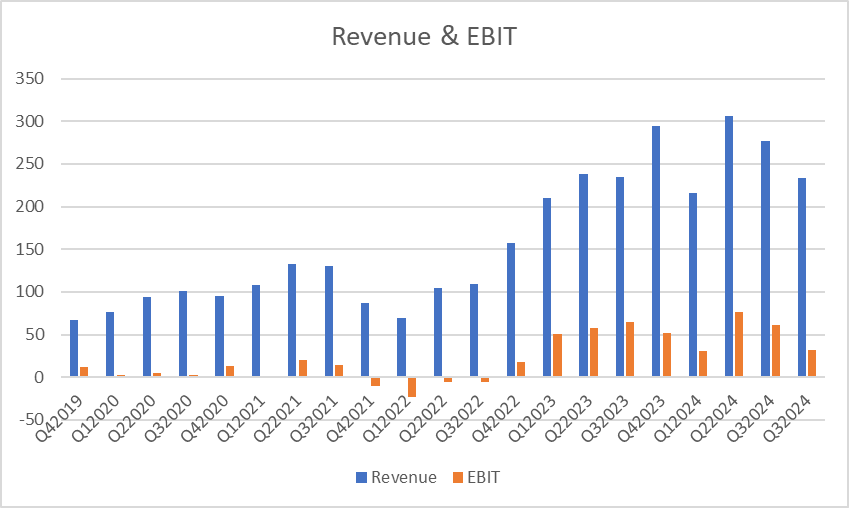

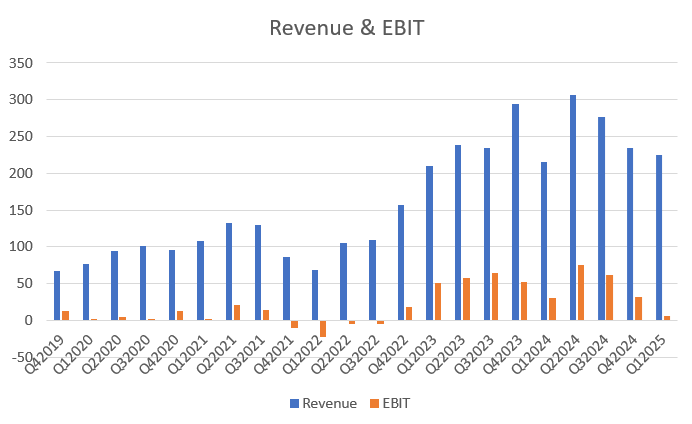

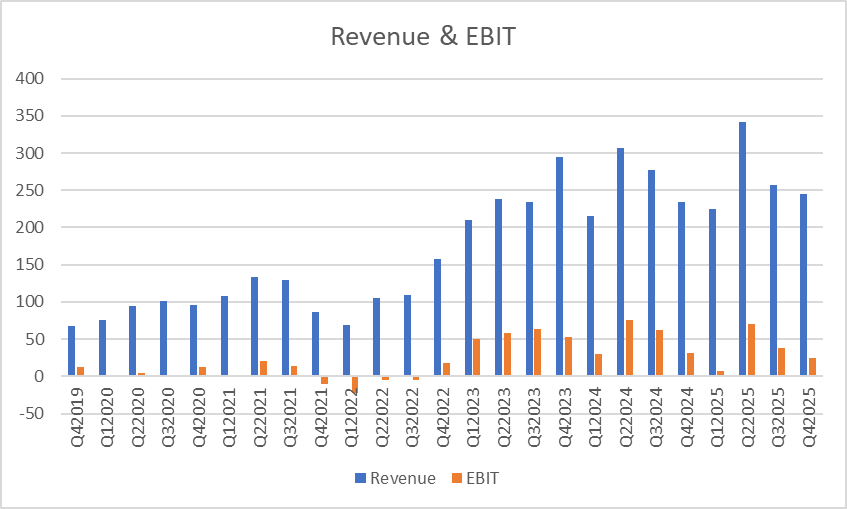

Regarding EBIT, a kind of profitability breakeven seems to have been around 100 MNOK in quarterly revenue.

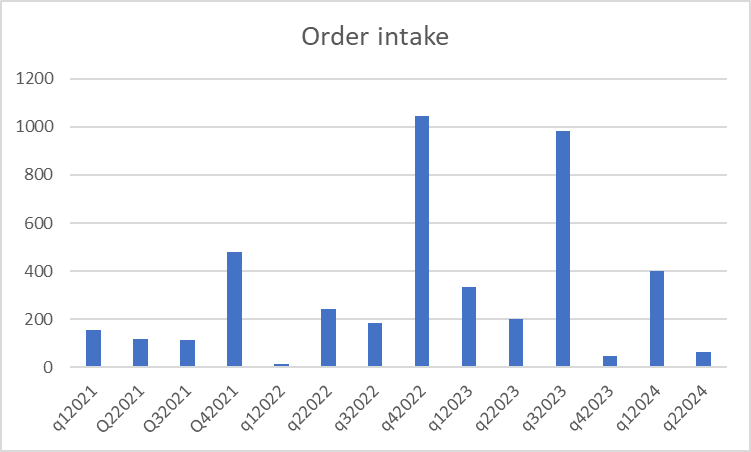

Order intake has varied quite a lot quarter by quarter over time.

To my recollection, the growth of the order backlog was at some point hampered by the company’s resources; however, I understand that investments were made in this area at the beginning of this year, which was also reflected in Q1 profitability.

About Valuation

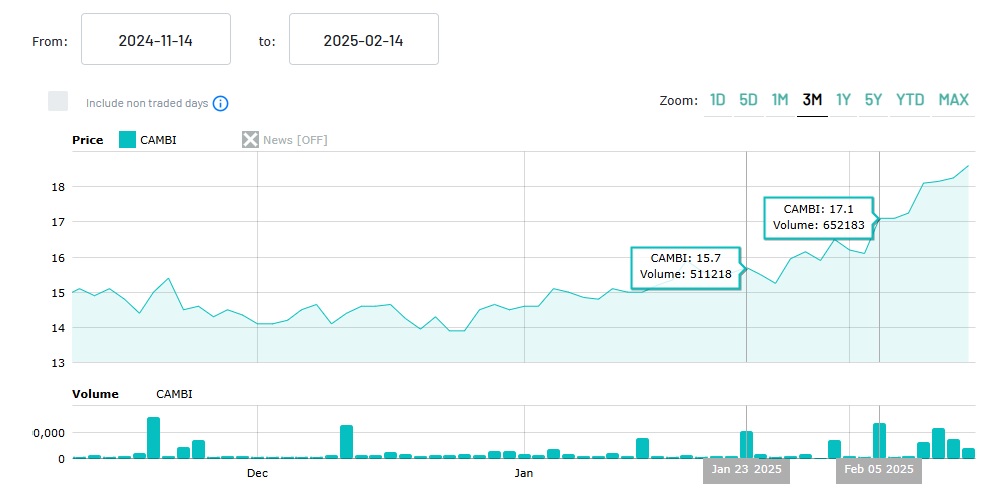

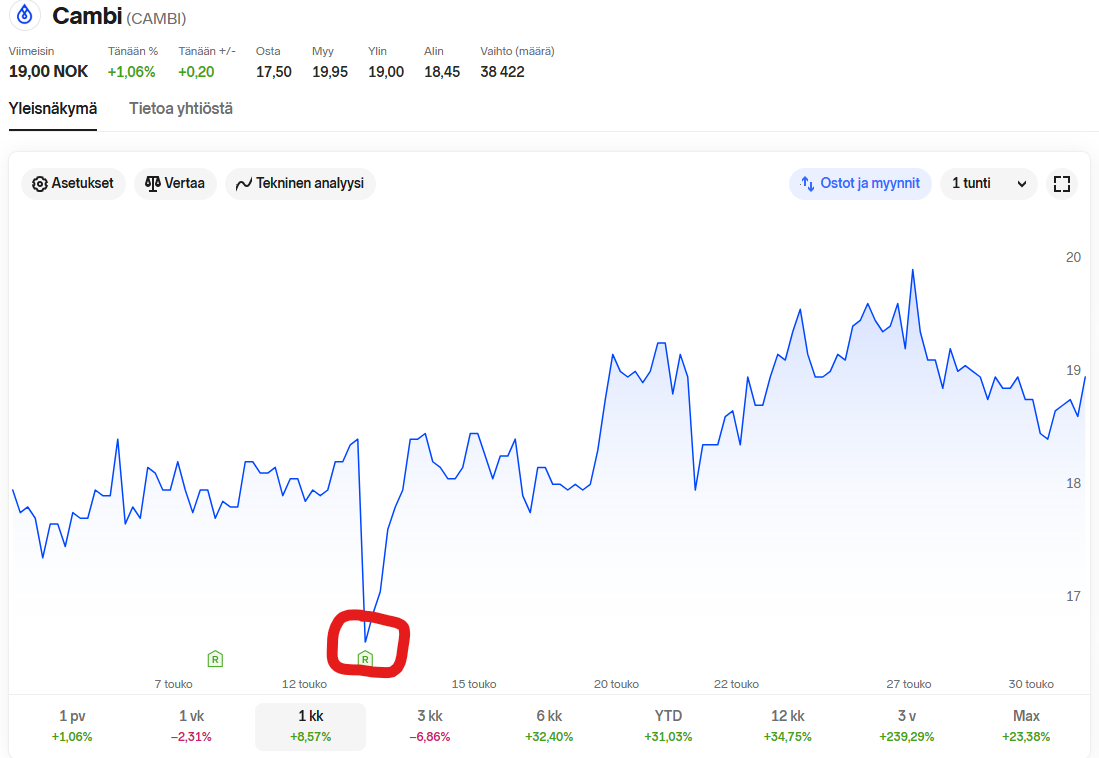

Cambi’s stock performance has looked like this.

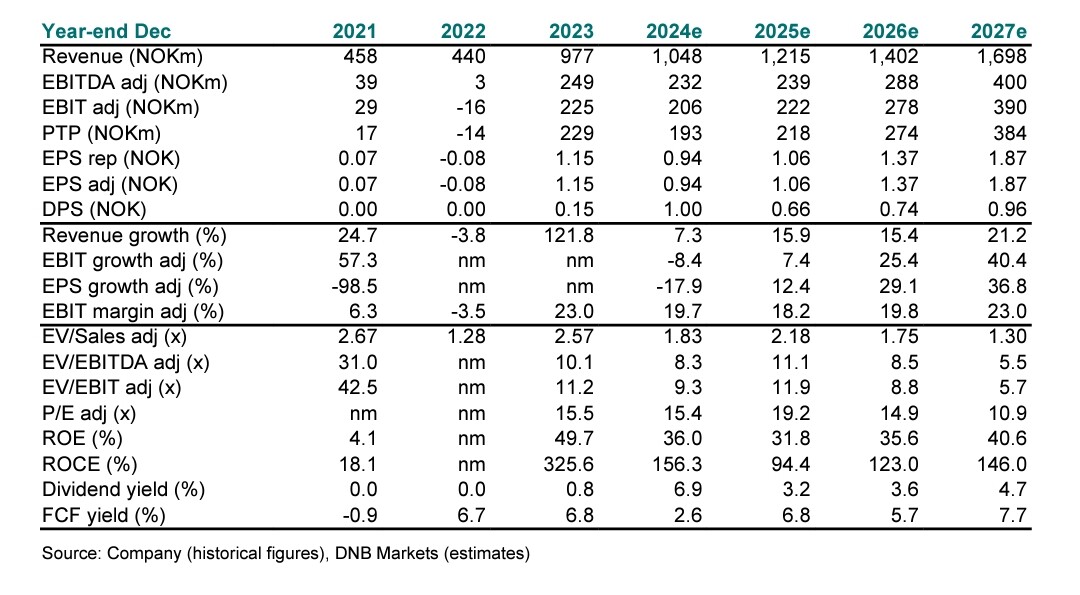

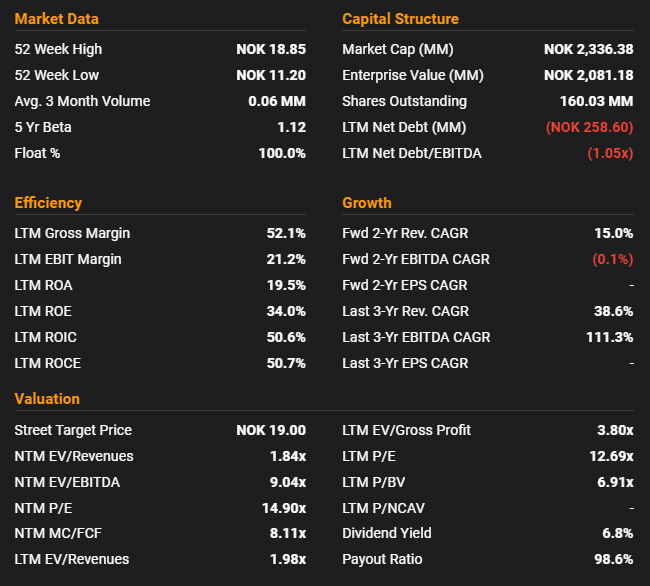

TIKR gives Cambi the following figures.

For the dividend party, please note that Cambi aims to distribute 60-80% of its earnings as dividends. Last year, a dividend of 1 NOK was paid, so at the last closing price, the dividend yield would be around 7%.

Cambi is followed by DNB, which at the time of writing gives a target price of 19 NOK (current price 14.40 NOK). Their investment case is based on the valuation of peers, which measured by the EV/EBITDA multiple, is significantly higher for them than for CAMBI (x12 vs. x9).

https://www.dnb.no/seg-fundamental/fundamentalweb/inst/companyreportsa1024.aspx?cid=10553&uid=&auth=&pwd=&popup=n

Current Situation and My Own Thoughts

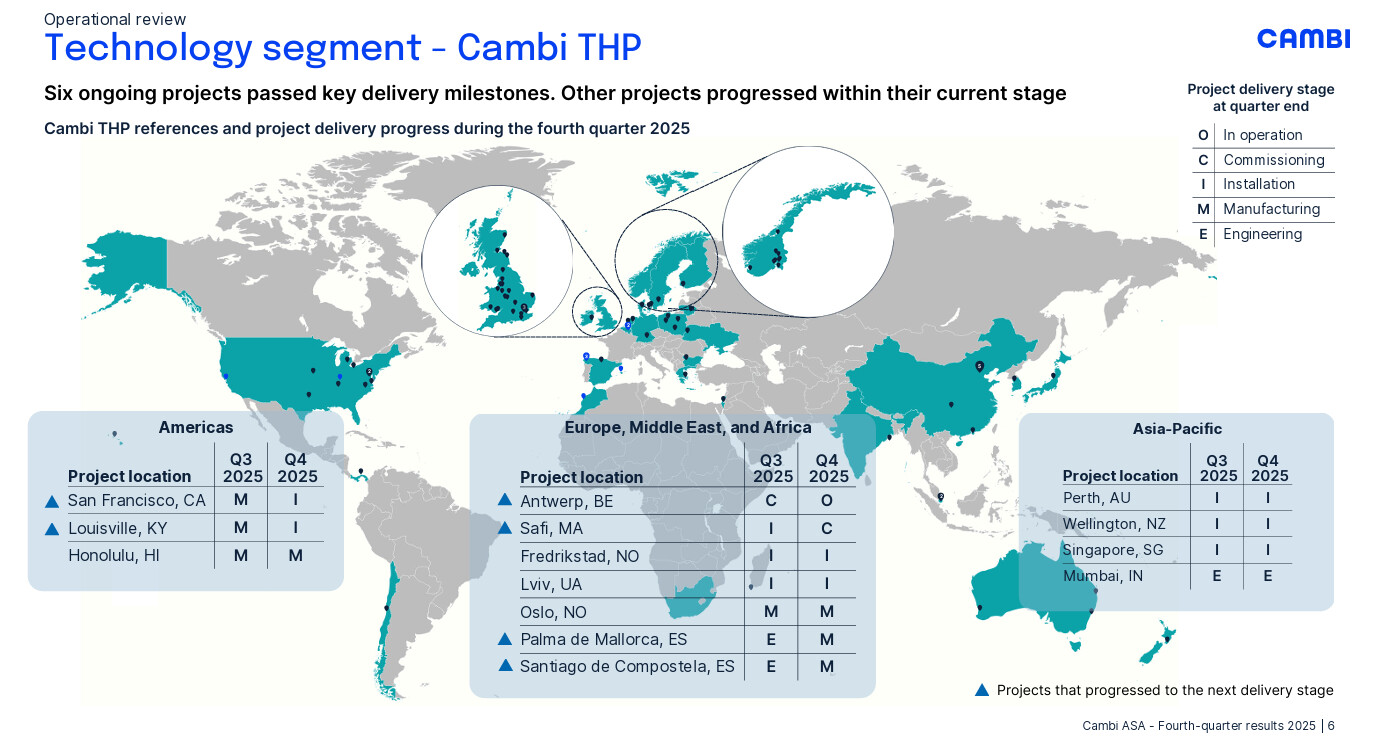

Cambi currently has 18 projects underway. My investment pitch was that after a weak Q1 result, management announced that several project milestones would fall into future quarters, so I guessed Q2 had the potential for a good result. This indeed happened, and it was a record quarter.

Initially, the market reacted positively, but the well-started day was ruined by a press release, which stated that the CEO had sold all of his investment company’s Cambi holdings. Three days later, a new announcement followed, stating that the CEO was leaving and Per Lillebø, Chairman of the Board, founder, and main owner of the company, had been appointed as interim CEO.

Although there is still a way to go to DNB’s target price, and I believe it is well-justified, I currently see no short-term drivers for the share price to rise. Such drivers could, of course, be new large orders. In the earnings call, the CEO did say that the sales pipeline was quite good, but due to the subsequent CEO turmoil, it is difficult to assess its development.

In the earnings call, the CEO mentioned their biggest challenges as increasing awareness of the technology and the slow purchasing and decision-making cycles of public sector-focused customers.

In my opinion, Cambi has an interesting niche product in a sector suitable for current trends. Who wouldn’t want cleaner wastewater, especially when its end product can be utilized in gardens and energy production? I own a few percent of the company.

Time will tell if the company succeeds on the administrative side as well, in what is the basic idea of their business: “PUT THE SHIT TOGETHER”

Acknowledgements

Thanks to users @Polakki , @Bjorninen , @Hapzu , @Deep_Value and @Contrafun for their contributions to this company so far. Hopefully, it will continue in this thread, and we’ll get more discussants involved.

Thanks also to Co-pilot for writing the Thermohydrolysis section.

I will post in the thread if I update this.

=>

=>