https://norbit.com/media/NORBIT-ASA-Annual-Report-2024.pdf

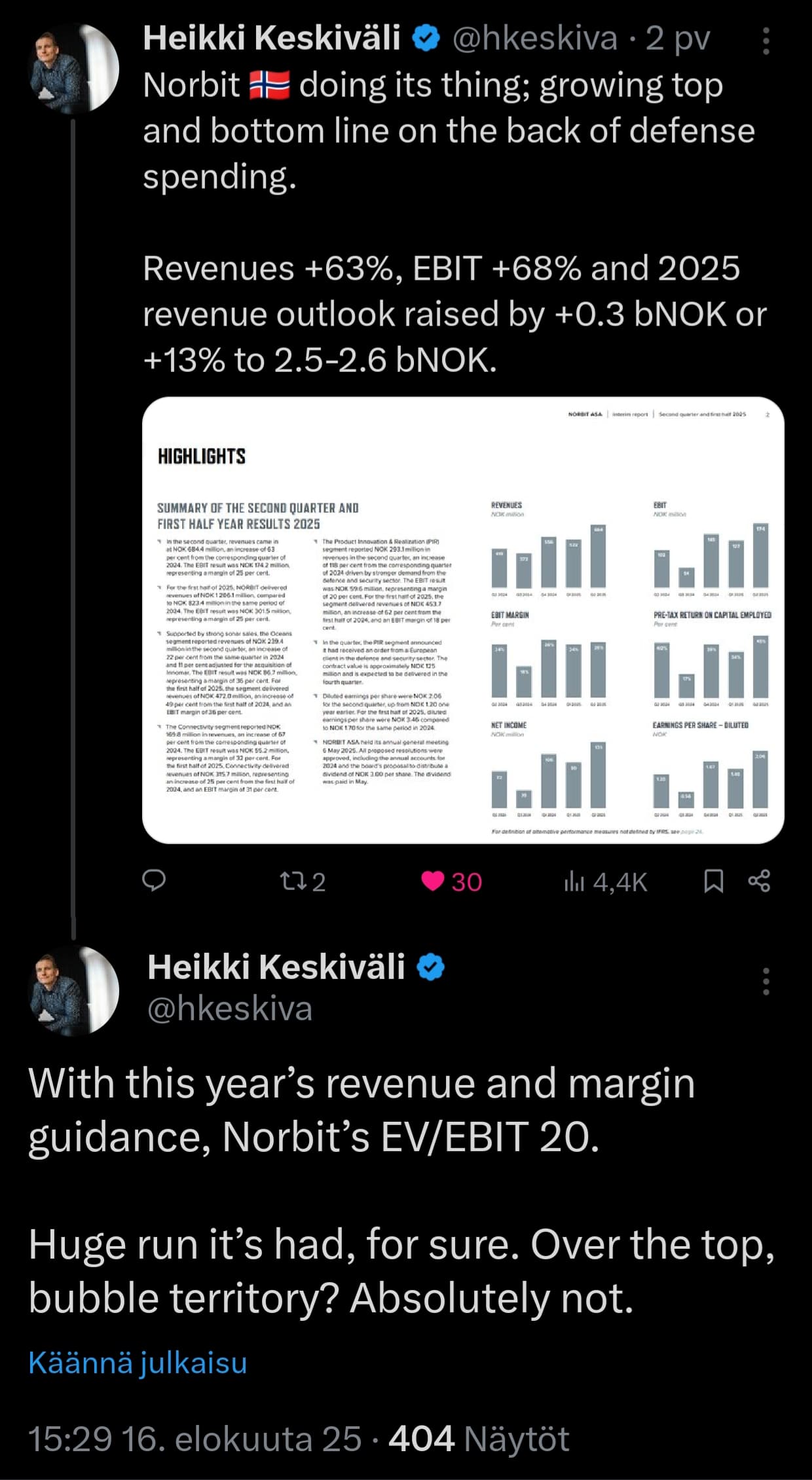

2024 annual report is out. I’ll get back to the content later regarding what I deem necessary.

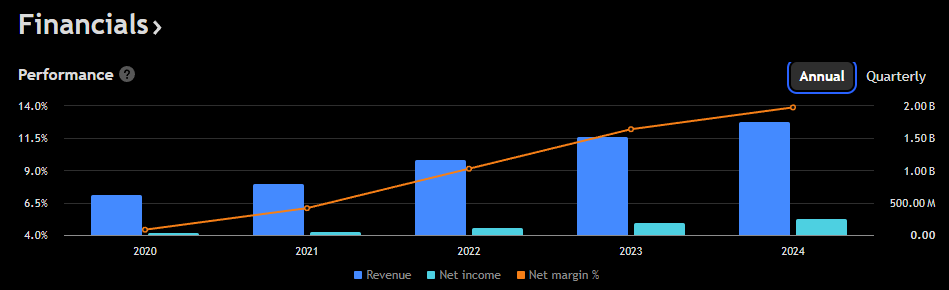

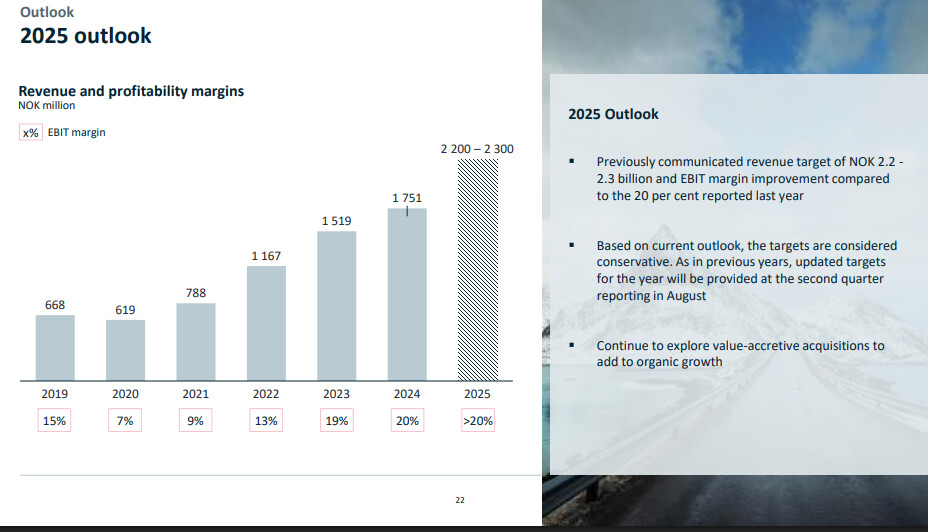

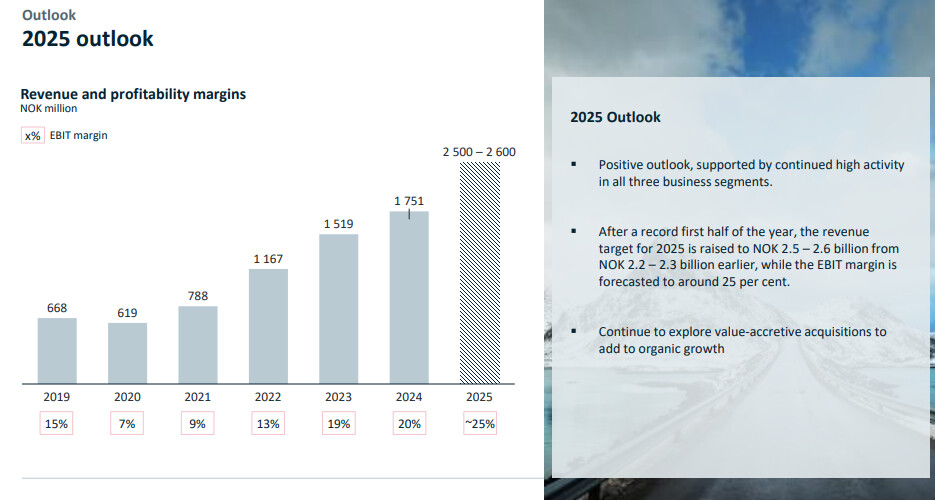

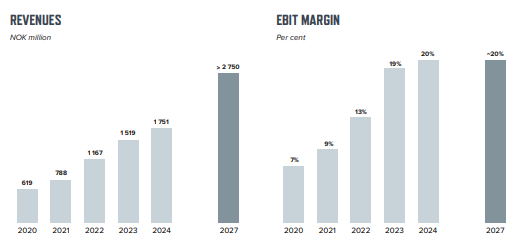

This year, we aim to reach a top line between NOK 2 200 and 2 300 million, with an EBIT margin that surpasses the 20 per cent we achieved in 2024.

I’ve been slowly trying to read through Norbit’s annual report. For 2025, a revenue of 2200-2300 MNOK with an EBIT margin >20% is guided. Revenue growth is thus guided at 25-30%. This is starting to give me a feeling that the 2027 target of >2750 MNOK revenue will be achieved ahead of schedule again. If we assume robust growth continues in 2026, a “modest” 20-25% revenue growth would be enough to meet that 2027 target a year early again. Oh right, the target is with organic growth. In addition, there is cash flow for acquisitions, the latest of which has been at least preliminarily very successful.

The EBIT-% also seems to be quite firmly included in the company’s targets. Monster-like growth is guided for this year, accompanied by an even better EBIT margin. What could it be then, when growth starts to slow down? Which, of course, I hope won’t happen for years to come. ![]()

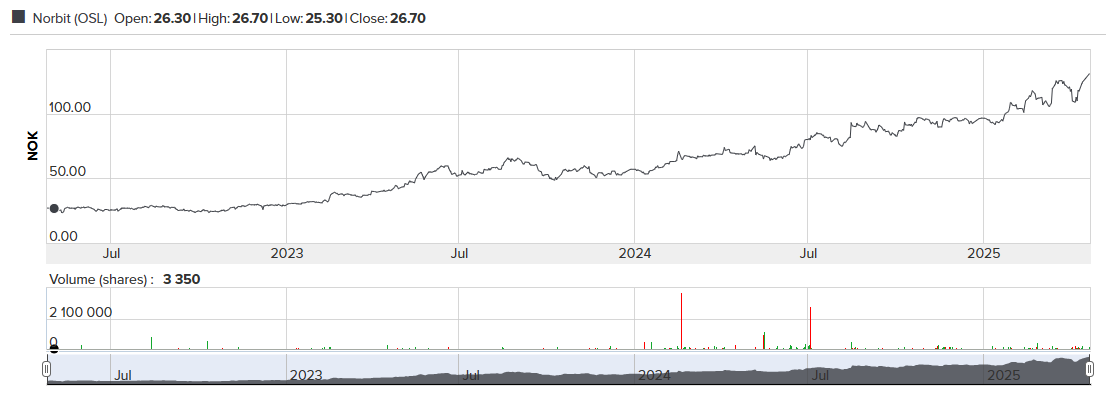

The company trades at approx. 14.5x EBITA (2025, if the midpoint of the guidance is achieved).

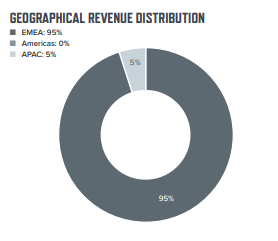

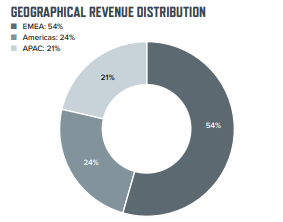

More on geographical diversification (tariffs apparently being tinkered with somewhere).

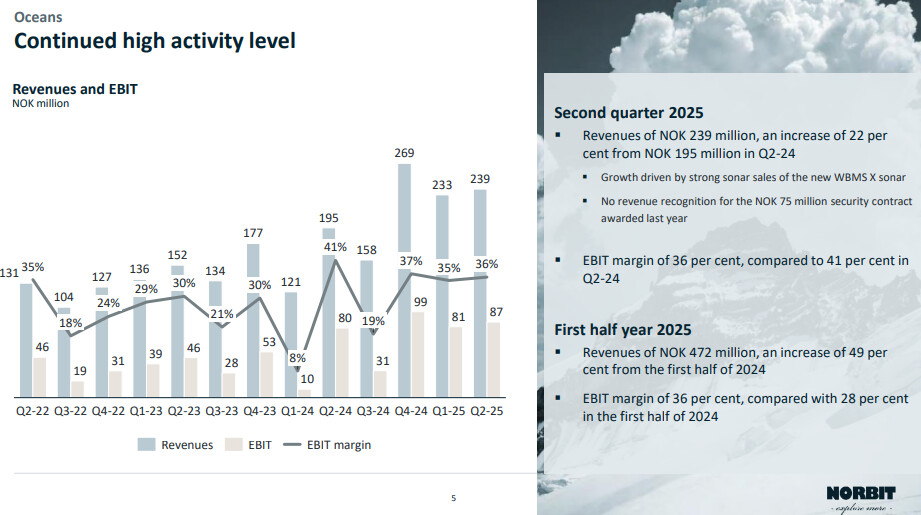

Only Oceans takes a direct hit from larger tariff cuts. For Connectivity and PIR, the impact is negligible. Part of Oceans’ production is done in the United States, so not the entire share of revenue is imported through the hairy hands of customs officials.

Direct tariff impacts are therefore quite moderate, but impacts can, of course, occur through customers.

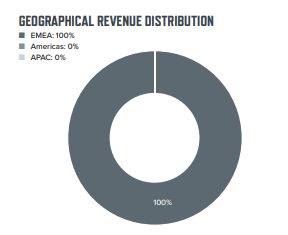

Oceans:

Connectivity:

PIR: