I conducted an in-depth analysis of NextCell Pharma’s valuation, and I wanted to share a summary of the key findings and calculations. The analysis is based on the sum-of-the-parts (SOTP) method, which I believe is the most suitable way to value a company that has both a high-risk drug development project (ProTrans) and more stable cash-generating subsidiaries (Cellaviva, Qvance).

Here are two key scenarios: the current base scenario and a hypothetical scenario where a partnership agreement is reached this year.

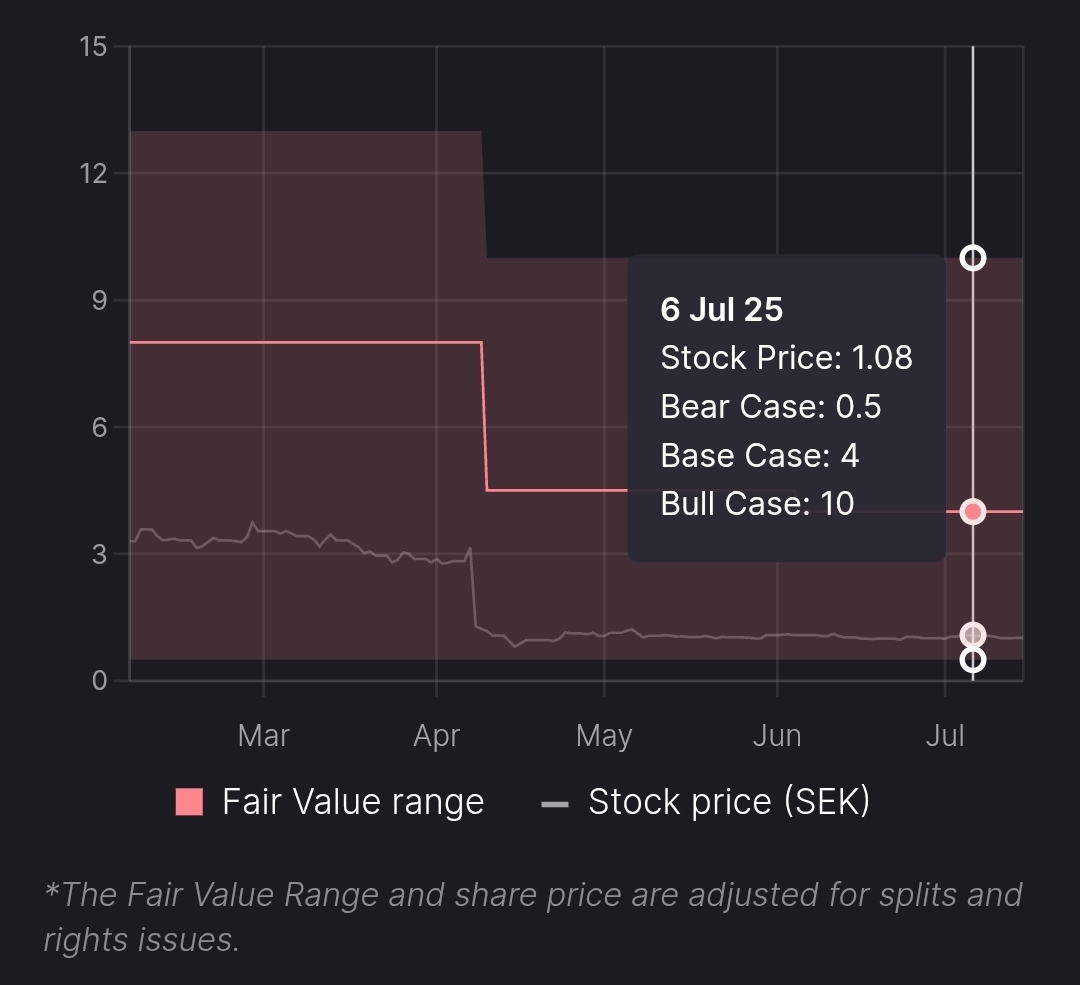

1. Current Valuation

This scenario represents the current situation, where there is significant uncertainty associated with the outcome of the ProTrans-Young study. The valuation is risk-weighted to reflect this uncertainty.

Target price: 5.01 - 6.86 SEK

Assumptions and Parameters:

Valuation method: Sum-of-the-parts (SOTP).

ProTrans value (rNPV): 453.2 million SEK.

Phase II study Probability of Success (PoS): 45% - 65%. I would say 45% is still conservative, even though it is higher than the typical Phase 2 success probability. However, Redeye uses a 40% success probability. I base the 65% upper limit on the very strong existing evidence from studies published so far.

Cumulative Probability of Success (Phase II → Approval): 23.7% - 34.3% [3]

Timing of partnership agreement: 2027 (after positive study results) [4]

Total deal value: 650 million USD [4]

Upfront payment: 130 million USD (20% of total value)

Royalties: Average 15%

Peak Sales: 1.4 billion USD

Discount rate (WACC): 16%

Value of other businesses: 87.5 M SEK.

Cellaviva: 62.5 M SEK (based on 5.0x EV/Sales multiple)

Qvance: 15 M SEK

FamicordTX ownership: 10 M SEK (placeholder value) [12, 13]

Number of shares: 111.39M

The base scenario reflects significant upside potential compared to the current share price level, but naturally involves considerable clinical risk.

2. Hypothetical Valuation: Partnership Agreement 2025

This is a purely hypothetical scenario that answers a previously posed question: what would be the company’s value if it succeeded in forming a partnership already this year? Such an agreement would eliminate a significant portion of the clinical risk and accelerate the realization of cash flows. The company has clearly already hired big pharma representatives for its advisory team and shifted discussions towards a partnership.

Target price: 13.16 SEK

Changed assumptions for the calculation:

ProTrans value (rNPV): 1,358.1 M SEK.

Phase II study Probability of Success (PoS): 100% (assuming the agreement is based on sufficiently strong evidence that Phase 2 can be expected to pass)

Cumulative Probability of Success (Phase II → Approval): 52.8%

Timing of partnership agreement: 2025 (two years earlier than in the base scenario)

Other parameters (total deal value, royalties, peak sales, WACC, value of other businesses) have been kept the same as in the base scenario for comparability.

The current valuation (5.01 SEK) prices in significant risk but at the same time offers considerable upside potential if the study succeeds and a partnership is formed as expected in 2027. The partnership scenario (13.16 SEK), in turn, highlights the potential inherent in the stock if the risk were to be removed earlier than expected. This figure illustrates how much of the value is currently tied up by the uncertainty of a partnership agreement.

It is also worth noting the bear scenario of the analysis, where the ProTrans project fails completely and its value is reduced to zero. Even in this case, the value of the company’s other parts (Cellaviva, Qvance, FamicordTX ownership) and existing cash is, according to my calculations, approximately 0.97 SEK per share. This supports the view that the current market price of approximately 1 SEK hardly gives any value to the success of ProTrans, but practically only prices the company’s existing businesses.

The analysis is somewhat in line with Redeye’s valuation.

In a situation where NextCell would receive a 130M USD upfront payment, it would of course be a bit odd if the entire company’s valuation was almost in the same ballpark, if a partner buys the rights to ProTrans and funds Phase 3. The entire valuation is almost entirely based on the upfront payment, and future potential cash flows from milestone payments and royalties are weighted years into the future through uncertainties and a high WACC. At this stage, it is also not really possible to guess whether Nextcell would succeed in generating new productive business with the money.