Toivottavasti osaan avata selkokielisesti tämän lopulta yksinkertaisen asian. Suomalaisten metsärahastojen arvonmääritysmenetelmät ja arvostukset poikkeavat toisistaan. Alla oleva metsälehden juttu on maksumuurin takana, mutta tässä paljastuksena rahastojen arvostuskerroin euroa/hehtaari:

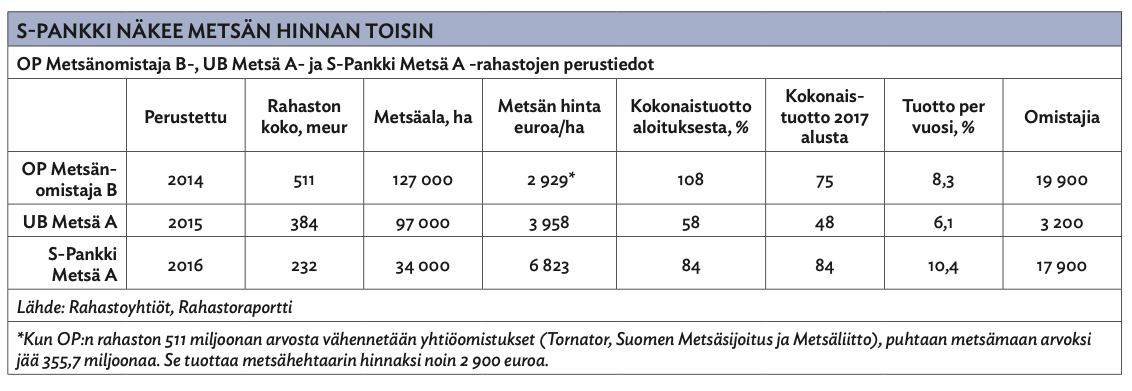

OP: 2900 €/ha,

UB: 3958 €/ha ja

S-Pankki: 6823 €/ha

Suomen keskiarvo vuonna 2024 oli 4007 €/ha. (Mediaani kauppahinta, Lähde mml, linkki alla).

UB ja OP metsä ovat Suomen keskiarvoa pohjoisempana ja niiden arvostus on ollut ainakin oikealla pallokentällä suhteessa maan keskiarvoon. S-Pankin arvostus on ollut selkeä kupla. Tämä on osin tietoa ja osin veikkaus, mutta käsitykseni mukaan maantieteellisessä sijainnissa ei ole näiden kolmen välillä merkittäviä eroja. Joskus olen raporteista niiden metsätilojen sijainteja katsellut. 70 % korkeampi arvostus mediaaniin ei ole mitenkään perusteltavissa kun metsää on kymmeniätuhansia hehtaareja. Ihan se ja sama vaikka on balttiaa vähän mukana tai vaikka strategia olisi sitä tai tätä. Yksittäinen hehtaari Lapissa voi olla alle 1000 €/ja, ja etelässä yli 10 000 €/ha, mutta ei kymmenien tuhansien hehtaarien portfolioissa vaan voi olla näin isoja eroja muuten kuin arvoja manipuloimalla.

Metsätietoja ei näin suurilla kokonaisuuksilla voi manipuloida, harvalla riittäisi Suomessa siihen osaaminenkaan. Metsä ja metsänkäsittely on isossa kuvassa samanlaista toimijoiden välillä. Kasvumallit ovat kaikilla samat Luken mallit. Sieltä se tuottoero ei synny. Kuten aloitin, kyse on arvostusmenetelmästä ja ennenkaikkea syötetiedoista. Arvostusmenetelmä, diskonttokorko ja kantohinnat. Näistä syntyy ero arvostukseen.

Sitä en tiedä, eikä ole siihen vastausta, miksi S-Pankilla oli ok pitää metsärahaston arvo kuplatasolla 2024 asti, ja laskea sitä alas juuri vuonna 2025. Mutta se on selvää, että kallis se on ollut tähän asti ja lienee edelleen.

Mielenkiintoinen ero! Aikasemminkin on tällä palstalla on puhuttu metsän arvostuksen eri tavoista, tässä ne tulee konkreettisesti ilmi. S-pankin metsärahaston esitteestä löytyy seuraava kuvaus:

“Rahastoon kuuluvien metsäkiinteistöjen käyvän arvon määrityksessä käytetään

lähtökohtaisesti ulkopuolisen riippumattoman asiantuntijan lausuntoa. Jos luotettavaa

metsätilojen transaktioihin perustuvaa markkinahintaa ei ole käytettävissä, määritetään

arvo Rahaston käyttämien arvonmääritysmallien mukaisesti, jossa huomioidaan

laskentaperiodin mukaiset diskontatut kassavirrat. Päätearvona käytetään lähtökohtaisesti

hakkuuarvoa.”

Kuvaus viittaa siihen että arvostuksessa käytetään tietoa metsätilojen kaupoista jos sitä on riittävästi saatavilla, muuten käytetään hakkuusta saatava diskontattu kassavirta, eli käytännnössä puuston arvo. OPn metsärahastossa sen sijaan käytetään puhtaasti puuvaratietoa.

Rahastojen arvostusero voi osittain syntyä tästä erosta. Jos S-pankin metsärahasto on ostanut metsää kovaan hintaan kilpaillulta alueelta, kauppoihin perustuva arvostus on varmasti kova. Metsärahaston omat ostot vieläpä vaikuttaa kauppahintoihin, jos metsärahastot taistelevat metsätiloista, niiden arvot nousee. Puuston arvoon perustuva arviointi ei ole yhtä helposti metsätilojen kauppahintojen mukaan heilahteleva. Toisaalta voi hyvin olla että S-pankin metsärahasto on vain syystä tai toisesta keskittänyt ostot etelään. Pitäisin kyllä puuston arvoon perustuvaa arviointia turvallisenpana. Ylipäänsä tästä tulee hyvin ilmi kuinka tärkeää on perehtyä metsä/kiinteistörahaston arvonmääritykseen ja arvostukseen ennen sijoittamista.

Onko tässä m2 laskelmassa huomiotu se, että OP:n salkusta lähdes 20% on Tornatorin osakkeita, 5% Suomen Metsäsijotusta ja 5% Metsäliittoa? Oletan että kaksi jälkimmäistä ovat myös osakkeita, eivätkä suoraan metsätiloja.

Täytyy vielä disclaimeriksi todeta, että itse en ole yhteenkään näistä sijoittanut enkä näihin mitenkään muutenkaan sidoksissa. Metsässä työt ja siksi kiinnostelee seurata. Kulutaso on se haaste omasta mielestä pitkän aikavälin tuotoille.

Arvostusmenetelmät tosiaan vaihtelevat. Kävihän Karokin grillissä niitä hyvin läpi (katselusuositus). Tämä €/ha on karkea mutta helppo tunnusluku arvioida eroja. Sama kuin kiinteistöyhtiöllä P/B. Book tuottaa eri tavalla eri yhtiöillä, ja kertoimet vaihtelee mutta tämä ero on jo liian räikeä ollakseen mitenkään perusteltu.

Yhteismetsät tarjoavat vähemmän likvidin mutta kulutehokkaamman ratkaisun sellaiselle metsäsijoittajalle, jota ei kiinnosta muuta kuin passiivisesti omistaa tätä hienoa omaisuusluokkaa.

Oli kiikarissa yks noin 30 ha metsä joka on 7:ssä eri palassa. Missähän mättää kun itse katselin Stora Enson nettilaskurilla kiinteistönumeron perusteella puuston arvoksi reilun 60 000 euroa. Tänään tuli välittäjältä OP:n metsäarvio jossa puuston arvo oli noin 144 000 euroa!! Kummatkin arviot on tehty ilman maastokäyntiä. Nämä nettipalvelut käyttää jotain ilmakuvaus -aineistoja tms. Ostohousut putos pois jalasta. Kun ei ole intoa/taitoa lähteä relaskoopin kanssa pyörimään kaikkia 7 aluetta läpi, en lähde tarjoamaan ollenkaan. Olen kuullut että ilmakuvaus-aineistoihin perustuvissa arvioissa voi olla isoja heittoja ja niin totisesti näyttää olevan! Hieman ihmetyttää, miksi ko. arviota ei ole pistetty suoraan myynti-ilmoitukseen jossa myydään taloa ja metsää.

Pitäisi verrata yksittäisiä palasia ja katsoa onko hintaero systemaattinen, vai onko vaan pari kuviota jossa se ero tapahtuu. Se että arvio tehdään ilmasta käsin, pitäisin hatusta tuumattuna aika epäluottana. Aina täällä MHY on saapastellut metsät 10v välein ja niiden pohjalta on hyvin pitkälle kyetty tekemään tuotto ja kululaskelmat mitä on seuraavan 10v aikana eteen tullut. Eikä se saapastelija ole ollut kuka tahansa toimistolla, vaan siihen dedikoitu henkilö, joka tekee vain tätä arviointi-työtä.

Aiemmin oli puhetta metsiin liittyvästä poliittisesta riskistä, Suomessa omistus on hyvin hajallaan, eli on paljon yksityishenkilöitä, Y-tunnuksella tai ilman. Tämä laaja äänestäjäkunta tiedostetaan(paitsi vasemmalla), eli ihan mitä tahansa hullua ei mene helposti läpi. Riskiä on lähinnä siinä, että ilmeisesti yhä useampi ei ole enää riippuvainen taloudellisesti metsätuloista, eikä edes itse asu maaseudulla, eli “ojitus ja hakkuut seis”, ei enää hetkauta niin paljoa.

Uusia, oletettavasti entistä tarkempia, laserkeilauksia tehdään paraikaa ympäri suomenmaata. Ainakin aikaisemmissa aineistoissa varsinkin taimikoiden tilavuudet ovat päin prinkkalaa ja aivan liian yläkanttiin. Vanhemmissa metsiköissä kyllä näyttävät mitat/tilavuuden aika hyvin

Rahastot tuli markkinoille niin maksoivat ihan yli hintaa palstoista, eihän noita enää yksityinen kyennyt ostamaan kun hinnat karkasivat. On aikakin että totuus tulee julki ja arvot palautuu oikealle tasolle. Sijoittajia tämä tulee kyllä harmittamaan kun luvatut tuotot eivät toteudukaan.

Tämä on kyllä niin totta. Rahastoihin tulvi rahaa kun puun hinta nousi, kun sen Venäjältä tulo loppui. Rahastot sitten tällä rahalla ostivat kaiken mitä sai hinnoista niin välittämättä. Metsässä ja puunhinnassa on suuri alennus tulossa, kun Ukrainaan saadaan rauha ja raakapuuta alkaa virtaamaan taas Venäjältä. Harva haluaa uskoa, että kauppa Venäjän kanssa aukeaa, mutta kyllä se vaan aukeaa.

Kiitos tiedoista.Jossain mettihaastattelussa mettäammattilainen antoi ostoharkintaan myös hyvät tärpit: Maastossa tapahtuvassa arvioinnissa harvan metsän puusto arvioidaan helposti yläkanttiin ja tiheä metsä alakanttiin. Suositteli ostamaan rehevän maapohjan metsän koska tuleva kasvu kuroo helposti kiinni karumman pohjan metsän joka ois vähän halvempikin. Hän oli ostanut ilmakuva- arvioidun hankalapääsyisen palstan jossa oli sitte lopulta paljo enempi puuta kuin etäarviointi oli näyttäny. Tieto ois valttia kun vaan ois sitä tietoa!

Pohdiskelen tässä parhaillaan uutta avausta ryhtymällä metsäsijoittajaksi ja punnitsen eri tapoja toteuttaa se mahdollisimman vaivattomasti. Erityisesti kiinnostaisi kuulla näkemyksiä passiivisista omistusmalleista. Rahastot ei kiinnosta.

Yhtenä varteenotettavana vaihtoehtona olen miettinyt metsätilan vuokraamista Tornatorille. Malli houkuttelee passiivisuuden ja ennustettavan kassavirran vuoksi. Toisena vaihtoehtona harkinnassa on perinteinen yhteismetsäosuus.

Nyt kysyisinkin foorumilaisten kokemuksia ja näkemyksiä:

Onko kenelläkään omakohtaista kokemusta Tornatorille vuokraamisesta? Miten vuokratasot ovat kehittyneet suhteessa yleiseen puunhinnan kehitykseen ja onko sopimusteknisesti tullut vastaan yllätyksiä?

Kiinnostaisi kuulla erityisesti näkemyksiä siitä, nähdäänkö vuokramalli hyvänä hajautuksena osana laajempaa sijoitusvarallisuutta?

Samaa mieltä. Metsärahastojen kulut ovat aivan järkyttävät, luokkaa 2% vuosittain. Se on lähes puolet metsän tuotosta. Esim isoissa yhteismetsässä hallinnointikulut ovat luokkaa 0.1-0.2% vuosittain.

Itse kanssa uskon, että raja aukeaa puun ja muunkin kanssa joitakin vuosia rauhan jälkeen. Niin se aukesi aikanaan toisen maailmansodan jälkeenkin tavaralle ja osalle ihmisistä, niin Suomessa ja Saksassa, vaikka tappaminen oli aivan eri sfääreissä kun nyt. Raakapuun hinta tulee laskemaan eikä nykyisillä piikkihinnoilla kannata metsää ostaa eikä metsärahastojakaan.

Itse olen kokenut yhteismetsän hyvänä passiivisen metsäomistamisen tapana. Liitin omat metsäni suurehkoon yhteismetsään noin 5 vuotta sitten. Nykyään metsäomistukseni on sitä, että yhteismetsän osinko/ylijäämä putoaa kerran vuodessa tilille.

Yhteismetsän valinnassa itse painottaisin seuraavia:

Riittävän suuri koko (vähintään 1500-2000 ha, mielellään enemmän), jotta rahavirta on tasainen ja saadaan skaalaetuja puun myynnissä ja hoitotoimien hankinnassa

Toimii useiden kuntien alueella (myrsky-, tauti- tuholaisriskien hajautus)

Monipuolisesti erilaisia ammattilaisia hoitokunnassa (metsänhoito, talous, laki)

Sijoittajaintressin painottaminen hoitokunnassa ja hallinnossa. Älä laita rahojasi yhteismetsään, jossa hoitokunnan tärkeä motiivi on vuosittainen ilmainen ryyppyreissu Tallinnaan osakkaiden rahoilla

Yhteismetsä ei itse osta lisää (ylihintaista) metsää, vaan laajenee vain siihen liitettyjen tilojen kautta

Riittävän hyvä raportointi, jotta voit ennustaa tuloja ja menoja 20-30 vuoden päähän

Näen nykyhetken vähän huonona hetkenä liittyen yhteismetsään, jos sinun pitää ostaa osuuksia tai ostaa (ylihintainen) tila liittääksesi sen yhteismetsään. Puun hinta ei oman näkemykseni mukaan ole kestävällä tasolla Suomessa ja uskon sen laskevan lähivuosina joko jalostuslaitosten sulkemisen kautta tai venäläispuun palatessa tuonnin muodossa Suomeen.

Täältä näet Yhteismetsiä, joihin voit liittyä, jos sinulla on jo metsään:

@Karo_Hamalainen:n kanssa keskustelemassa oli metsäsijoittaja Mika Venho

Tuollaisilla tuotoilla haastetaan vakavasti osakemarkkinoiden pitkän aikavälin tuottoluvut, mutta sijoittajan ei parane tuudittautua odottamaan vastaavia hintamurskajaisia jatkossa. Kuusi prosenttia voi olla realistisempi keskiarvo-odotus.

Keskimääräisen tuoton ympärillä aktiivinen metsäsijoittaja voi kuitenkin parantaa omaa tuottoaan merkittävästikin. Puuta kannattaa myydä silloin, kun sen hinta on syklin hyvässä vaiheessa. Metsänhoitotöiden oikea-aikaisuudella edistetään puuston laatua ja tukkipuusaantoa – ja niin edelleen.

Mika Venho muistuttaa myös ostohetken tärkeydestä.

”Ostohinta ratkaisee tulevat tuotot.”

Tämä ei tarkoita pelkästään oston ajoittamista sellaiseen hetkeen, jolloin metsätilojen hinnat ovat matalalla, vaan myös sitä, että ostaessa pyrkii samaan enemmän kuin mistä maksaa. Venhon mukaan yksi systemaattinen väärinhinnoittelu liittyy siihen, että hinnat tapaavat keskiarvoistua: hyvästä metsästä pyydetään vähemmän kuin pitäisi, huonosta maksetaan enemmän kuin pitäisi.

*Mika Venho itse vaihtoi osakesijoitukset metsään ja on tehnyt metsäsijoittamisesta itselleen ammatin. Hänen perustamansa Suomen Sijoitusmetsät toimii metsäsijoittajien apuna tilakaupoissa ja pitää yllä hintarekisteriä. Yhtiöryppäästä löytyy myös yhteismetsä ja yhteismetsätilojen kauppapaikka. *

Jaksossa käsitellään monipuolisesti metsäsijoittamisen lainalaisuuksia ja keinoja altistaa itsensä metsäomaisuusluokan tuotoille.

Kiitos @Karo_Hamalainen taas todella hyvästä grillistä. Näitä on kyllä ilo kuunnella kun vieraita haastetaan kunnolla vaikka kaupallinen yhteistyö on kyseessä.

Olen pitkään haaveillut metsään sijoittamisesta mutta kylmä fakta on vaan se, etten tiedä aiheesta paljon mitään joten riski siitä, että sijoitus menisi metsään (pun intended) on iso. Vaimoni veli ylläpitää alati laajenevaa metsä”imperiumia” Itä-Suomessa ja tuotot ovat olleet mukavat. Mutta hän tietää mitä tekee, omaa verkostoja ja tuttuja ja varsinkin pienempiä metsäpalstoja myydään ilmeisesti aika paljon myös tiskin alta oman kylän tutuille ym. Hän on myös todella työteliäs ja yrittäjähenkinen. Ilmeisesti viime vuodet ovat myös olleet melko epäotollista aikaa hankkia metsäpalstoja, hinnat ovat nousseet kovasti ja tuotto-odotukset ohentuneet.

Yhteismetsä kuulosti ajatuksena varsin houkuttelevalta mutta tuo Karonkin esiintuoma avoimuuden puute on kyllä vähän kulmia nostattavaa. Sitäpaitsi itselle tuo metsään “sijoittamisen” romanttinen puoli, eli omassa metsässä käyskentely ja asioiden opettelu ja itse tekeminen jäisi tuosta pois. Eli sijoittaisin vaan epälikvidimpään omaisuuserään.

Asiaa pyöriteltyäni mieleeni alkoi herätä seuraava ajatus; kun Stora Enso ensi vuonna listaa Ruotsin metsäomaisuuden omaksi yhtiökseen ja erityisesti jos tuota saa alennuksella verrattuna tasearvoon, mitäs jos ostaisin pienehkön metsätilan hinnalla (eli 50 t€) osakesäästötilin täyteen tuon firman osakkeita. Oletusarvoisesti yhtiö jakaisi kassavirtaa puun myynnistä aika avokätisesti osinkoina jolloin OST verohyödystä pääsisi nauttimaan (osingot takaisinsijoittaisi firmaan). Tottakai toki tässäkään en pääsisi halaaman omia mäntyjäni, mutta sijoitus olisi kuitenkin huomattavasti yhteismetsää likvidimpi ja arvonmääritys olisi avoimempaa. Ja omistaisin silloinkin metsää, ainakin epäsuorasti.

Miltä tällainen ajatus kuulostaa kanssasijoittajista?

Stora -Enson Tukholman pörsiin avattava metsäpörssiyhtiö on todennäköisesti likvidi ja läpinäkyvä.Siisti metsäsijoitus.SEn omistajat saanee ilmaisosakkeita tai ainakin merkitä osakkeita alle merkintähinnan.En ole koskaan edes ajatellut sijoittaa metsärahastoihin.Yhteismetsät(riittävän suuret) toimii hyvin ja taloudellisesti kannattavia.Yleensä toimiva johto osaavaa.Olen osakkaana yhdessä YMssä,en kuulu sisäpiiriin.

Olen maatalon poikia,metsätyöt tuli jo 50-luvun lopulla koulupoikana tutuksi.Oman metsän omistamisessa on sitä jotakin.Ostin- 94 ensimmäisen oman palstan .Sittemmin ostettu lisää.Metsänhoito ei ole rakettitiedettä.Netissä paljon hyviä videoita metsänhoidosta.Metsäpalstoja myy MHY Metsätilat,huutokaupat com,monet kiinteistövälittäjät.Palstalle matka alle 100km.Mielellän yhteiskunnan hoitaman tiestön lähistöltä.Pitkät metsätiet(sillat) lisää kustannuksia jossakin vaiheessa.tosin verotuksessa vähennyskelpoisia.Turvemaita pitää vältellä,niille tulossa hakkurajoituksia.Rehevä kasvupohja hyvä,ei suuria korkeuseroja eikä pahoja kivikoita.Luonnollisten purojen( ei kaivetut ojat) varret metsälakikohteita ja ne pitää jättäää hakkuiden ulkopuolelle.Havupuusto koivupuustoa arvokkaampi,metsätilakaupassa puustolla odotusarvoja,jotka saattaa hämmästyttää.Metsän istutukset ja taimikonhoidot kannattaa MOn tehdä itse.Työkaluina pottiputki,kuokka,vesuri ja raivaussaha.Metsäreppu,jossa hyvät eväät

Ensiharvennuksia olen tehnyt hankintahakkuina vuosittain,mutta nyt ikääntymisen(78v) takia lopettanut.Puutavaran ajon ostanut paikallisilta maanviljelijöiltä.Hankintahakkuut osa parasta metsänomistamista,liikuntaa jopa pientä jännitystä puiden kanssa painiessa.Mielestäni taloudellisempaa ostaa ensiharvennus puutavarayhtiöltä

Suosittelen oman palstan hankkimista,jos tykkää liikunnasta ,luonnossa elämisestä

Tämä pätee minusta vain paikallisiin pienehköihin tai keskisuuriin yhteismetsiin.

Kaikki metsäsijoittajan näkökulmasta varteenotettavat suuremmat yhteismetsät jakavat hyvää talous- ja puustodataa, jolla ennustaa tuotot vuosikymmenten päähän. Esim tuotto-%, ylijäämähistorian, hallinnointikulujen osuuden, Tuotot/kulut-%, Kehitysluokkajakauman, puuston kasvutiedon, hakkuusuunnitteen,kasvupaikkajakauman jne.

Nämä on helposti saatavilla ainakin LähiTapiolan, UPM:n, Metsähaltijan ja Kuusamon yhteismetsistä ja varmasti monesta muutakin. Ei välttämättä kaikkea löydä netistä, mutta aina voi pyytää hoitokunnalta, jos ostoa tai liittymistä harkitsee.

Paikallisia yhteismetsiä välttäisin muistakin syistä sijoittajana mm. hajautushyötyjen menetyksen takia. Mutta jos haluaa puuhastella yhteismetsän toiminassa mukana tuttujen paikallisten kanssa, niin ne voivat sellaiseen sopia hyvinkin.

Ruotsi taitaa periä 15% lähdeveron osinkoista ja OST tilillä ei ole tuplaverotuksen purkua joten täytyy pitkään pitään, että OST tulee kannattavammaksi kuin AOT.

Yhteismetsillä yleensä paljon dataa metsäomaisuudestaan.Oman metsätilan liittäminen yhteismetssään ilmaista,mutta pitää hyväksyä YMn osakkuussopimus,joka määräytyy markkina-arvoisesti.Ei varainsiirtoveroa,tietääkseni(en aivan varma asiasta)metsävähennys ei tuloudu(voi olla oman isomman metsäpalstan suoramyynnissä jopa kymmeniätuhansia euroja)

Samoin myytävä/ostettava YM-osuus on markkina-arvoinen.Netissä useita välittäjia esim Metsänhaltija, MMLn sivuilla hyvää tietoa

YM ottaa usein myös ostositoumuksia YM-osuuksista,esim 30000-50000e ja hankkii myöhemmin markkinoilta kertyneillä varoilla metsää