Let’s start a thread here for the investors you consider the best or most successful. This thread can also serve as great motivation for retail investors.

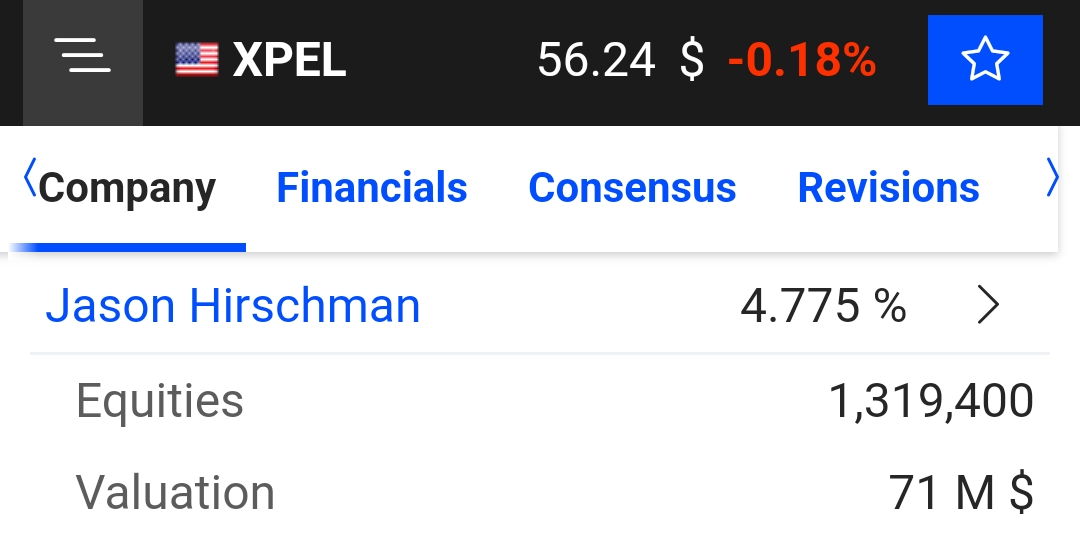

To kick things off, let’s look at Jason Hirschman, who is unknown to most. This retail investor started putting his money into Xpel stock when it was priced at $0.04. He still hasn’t sold his entire position, and his holding is currently valued at $71m. Today, he runs his own fund, Hudson 215 Capital. He’s a true diamond hand

Interesting topic! It would be nice to read stories about some of the lesser-known names who have been able to generate outperformance over the long term using various strategies.

I don’t have any such stories of my own to tell, but thumbs up for the topic, and I’ll be following this thread

I think Li Ka-shing’s story has some fascinating features. He is currently 95 years old, an entrepreneur and investor who retired a few years ago, and has been Hong Kong’s richest man for decades. His current wealth, according to Forbes, is $37 billion, although in recent years his companies have suffered due to, among other things, the difficult situation in Hong Kong.

Li arrived in Hong Kong as a refugee at around age 12 from mainland China in 1940 and started working at age 15 when he could no longer attend school after his father died.

“The most terrible experience during my childhood was witnessing my father’s suffering and ultimately dying of TB. I too was infected.

The burden of poverty and this bitter taste of helplessness and isolation sort of branded on my heart forever the questions that still drive me. Is it possible to reshape one’s destiny? Is it possible to minimize challenges through lessening complexities? And is it possible to enhance chances for success through meticulous planning?”

His first own business was founding a plastic flower manufacturing company in 1950. The company was modestly named Cheung Kong (a reference to how the Yangtze River is formed from many streams). When supporters of the Chinese Communist Party began rioting in then-British-ruled Hong Kong in 1967, Li believed the riots were temporary, stayed calm, and bought plenty of real estate while others were selling in a hurry. Later, the business expanded into the port, real estate development, trade, energy, and infrastructure sectors as suitable opportunities arose. These businesses are now under the CK Hutchison Holdings conglomerate and the CK Asset Holdings real estate company.

In this millennium, Li has also made numerous venture capital investments, especially through Horizons Ventures, and has invested in technology companies on the stock market as well.

Of course, not all lessons are applicable to the retail investor, but some certainly are (depending on the investment style, naturally), such as long-term thinking, staying calm in a tight spot, and adapting the investment style with the times. And of course:

“I am always vigilant about cash flow. I have adhered to a steady cash flow, high reserve and a healthy debt to equity ratio. “Seeking growth while maintaining stability” has always been my motto”

A video like this might fit well in this thread as a reminder of why fools earn more than the intelligent.

In short: Fools take bigger risks than the intelligent; eventually, one of these guesses hits the mark, and since there are more fools, more of them rise to wealth than among the intelligent. The intelligent invest more cautiously, so they only achieve mediocre results, but more reliably and better than the majority of fools.

So, when choosing someone to idolize, analyze their investments and their success a little. Is there just one lucky break, or are there multiple successes—and at times other than during insane bull markets?

A couple of lesser-known but interesting investors, in my opinion, are Shelby Davis and Peter Cundill, about whom I happened to read books recently: Davis Dynasty and There’s Always Something to Do.

Both have an extremely long track record; Davis apparently reached annual returns of over 20% and Cundill 15%, both over several decades. Quite nice compound interest.

Davis was interesting because he was an insurance specialist due to his previous background and invested almost exclusively in insurance companies. He also basically invested his own money, compared to Cundill, who was a Canadian fund manager.

Cundill’s track record is closer in time (1975–2008), and he was a proponent of currently unpopular asset-based / Ben Graham-style value investing. Extremely cheap companies, then, preferably well below liquidation value. Davis was also a value investor—having also read his Graham and even serving as the chairman of Graham’s analysis organization at one point. Both basically invested in very boring industries and companies, avoided what was trendy, and scrutinized the books carefully.

Anyway, a couple of lesser-known interesting investors. Also good for reinforcing one’s own value investor bias —digging through the trash can can indeed pay off.

This thread certainly deserves one ordinary (Polish) Markku! I’m talking about the father of all Canadian micro-caps (e.g., the (anti)success stories Oroco and Voxtur), Mariusz Skonieczny.

“Markku” graduated from Indiana University in 2003 with a degree in finance. From 2003 to 2008, the man worked in the commercial real estate industry as an appraiser and broker. During the financial crisis of 2008/2009, he left the industry and founded Classic Value Investors.

Disclaimer, the following is based on Markku’s own words:

In 2009, the fellow started investing with $10,000. By 2019, the account balance rose to $1.1 million. The coronavirus dropped it to $500,000. Between 2009 and 2019, the investment return (according to Markku’s own words) was about 100-fold. By March 2021, the account balance was $4 million, making it 400-fold. He has no idea how this compares to the Dow or S&P because he doesn’t follow them. According to the man’s own words, following indices can take the focus away from his own cases.

Markku is particularly interested in stocks trading on small exchanges. Especially the Canadian TSXV is close to his heart. Institutional funds and such don’t really touch the small firms on those grubby exchanges, so there is no competition. Markku is just trying to find a growing golden egg there.

Markku often arranges private placements for those companies, for which he receives finder’s fee commissions. I believe that, because of these among other things, Markku might stay married to even the poorer cases longer than he would like.