Coverage of Lehto started today. I am also creating a dedicated thread for it on the forum. Here is the initiation of coverage report: Laatuyhtiö syklisellä toimialalla - Inderes

Everything on Lehto can be found here: Lehto Group - Inderes

Coverage of Lehto started today. I am also creating a dedicated thread for it on the forum. Here is the initiation of coverage report: Laatuyhtiö syklisellä toimialalla - Inderes

Everything on Lehto can be found here: Lehto Group - Inderes

TA gives a rather bleak picture of the target. Still in August, the stock was sold quite aggressively relative to normal trading volume. The target has all resistances met at the weekly level, even though this morning’s rise (certainly due to Inderes’ recommendation) did push the price above the MA4 level. Something is wrong with the company’s fundamentals, which the market has priced into the target, and I, for one, would not buy a target with such low trading volume before a clear weekly-level trend change. I would have included a picture of the TA, but it doesn’t seem possible. Does anyone have a different view of the target? Earnings are coming soon, which will tell whether the expectations for the end of the year have held true.

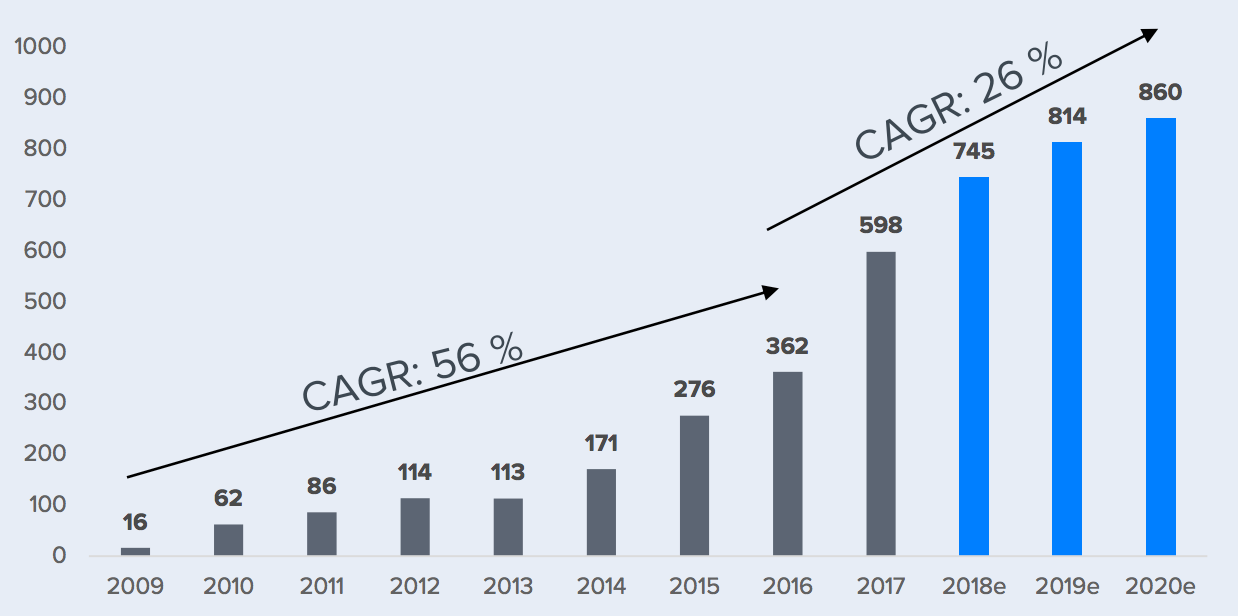

Lehto has increased its turnover 37-fold between 2009 and 2017. Quite an achievement: this has also been done profitably. This leaves even the stock market growth hogs Revenio iCare and Restamax in silver and bronze positions. ![]()

Should these growth curves also mention share issues, for the sake of honesty? In 2015, there were 45 million shares; in 2017, 58 million shares, meaning a growth of ~29%. Shareholders have largely financed the revenue growth out of their own pockets, and as a shareholder, I wouldn’t be surprised by this growth. The situation is the same with Citycon. Lehto has, of course, shown profitability during its history as a listed company.

By the way, I didn’t mention whether Lehto creates shareholder value at the same time. ![]()

The increase in the number of shares is related to the share issue that the company made when it listed on the stock exchange. EPS has still grown rapidly (as has book value per share), being 0.84 EUR in 2017 vs. 0.52 EUR in 2015 (+62%). So it seems that the increase in the number of shares has been compensated by an even stronger earnings growth.

A good podcast about capital allocation was made a couple of weeks ago, you should listen to it here.

The early years of a growth company should indeed be tough, but for this particular target, the future is what will be decisive.

After Negarin, the price of the note is now €6.14. Hmm.

Huh, half an hour after the negative news, there’s a -25% on the board and the price is €5.50.

Just last week in a video, I remarked to Olli that it was a bold move to go against Lehto with a buy recommendation… well, he who hesitates is lost.

I joined precisely on a buy recommendation, and I nicely justified it to myself for several days, relying on everything I read, listened to, and investigated about the company before buying. Well, now the portfolio took quite a hit from this, at least temporarily, but I guess it will crawl back up someday… The average purchase price is 7.46 at the moment, and even that was supposed to be cheap.

At least I have no idea what the real market price is after such negative news. I don’t want to believe it will stay at 5.33.

Now, one should probably buy more if one believes in the case… But in my case, it would reduce diversification and further increase the portfolio’s risk in the long run.

Monday could see a strong rebound… I’d be interested, too; it would lower my average cost. Hmm, I’m sweating here.

EDIT: The risk here is that it could drop again after the rebound, and then we’d be sawing at a really low level if the market is still struggling in the background and Q4 is presumably just as bad…

Maybe it’s just not worth touching this right now.

This company is difficult to evaluate due to its short history on the stock exchange. In terms of free cash flow, the company reached 20 million in its best year, 2015. If, optimistically, this is considered a normal level and the discount factor is 9%, the value of the share capital without growth would be 20 / 0.09 = 222 million. The company had 58,250,752 shares at the end of June, which would give a share price of €3.81. The valuation is on the low side if the construction market grows from this point or if Lehto gains a larger share of it. On the other hand, there is no complete certainty about future cash flows.

Bubbles are starting to burst.

Could you clarify what you mean by this comment? I didn’t quite understand and would gladly like to know…

The price of €LEHTO has been coming down all year; nothing exceptional has happened in its share price history. The most surprising thing about today’s (19.10) reaction was precisely such a sharp drop on top of an already long-standing decline.

However, let’s take into account that the company’s news coverage has specifically highlighted many positive things. A couple of days ago, there was even a full-page advertisement for the company in Helsingin Sanomat, meaning that visibility and a positive image are clearly intended to be conveyed.

To my understanding, Hannu Lehto also owns nearly 40% of the company, so a large part of the share capital is held by the company’s CEO (someone correct me if I’m wrong). This is also a significant sign of confidence from a small investor’s perspective, and I would understand the reaction if there had been radical changes in this ownership structure.

Inderes, among others, has considered the company defensive in a challenging market environment, which has also been a rationale for buying for investors like me.

There has been no strong parabolic rise here, nor has it been artificially accelerated upwards. This is what usually causes bubbles, like TILRAY, AMD, etc.

Dividend estimate currently 6.8%… ![]()

This is probably true in most cases. And even more so in Pohjanmaa (Ostrobothnia). ![]() One can glean some spark of hope from that ownership, but it’s not as essential as, say, significant additional purchases.

One can glean some spark of hope from that ownership, but it’s not as essential as, say, significant additional purchases.

New Inderes target price €5.5 / reduce.

@evolove173’s new target price €5.33 / sell.

They’re close, hats off to them. I’ll eat popcorn and see what the next 12 months bring.

What’s going to happen to Lehto’s stock price tomorrow? Guesses. Should I put on my buying sweatpants? Or did all the loose ends already come out in Lehto’s profit warnings?

It would probably be more constructive to ponder the outlook of Lehto’s business and study the company rather than guess where the stock will be tomorrow ![]()

HELPOTUSRALLI (Relief Rally) shouted! ![]()