Kesla, a small company with a market capitalization of around 18 million. It is definitely one of the smallest companies on our stock exchange.

It is an entrepreneur-owned company operating in the forest machine industry. The company has improved its profitability over the past few years after the crisis caused by Russian sanctions, and the company is now starting to stand on solid ground in terms of results. Somewhat ironically, the European economy is just heading into recession, as the company survived the previous crisis. The company is a good example of how risks completely outside the company’s sphere of influence materialize. This is worth learning from!

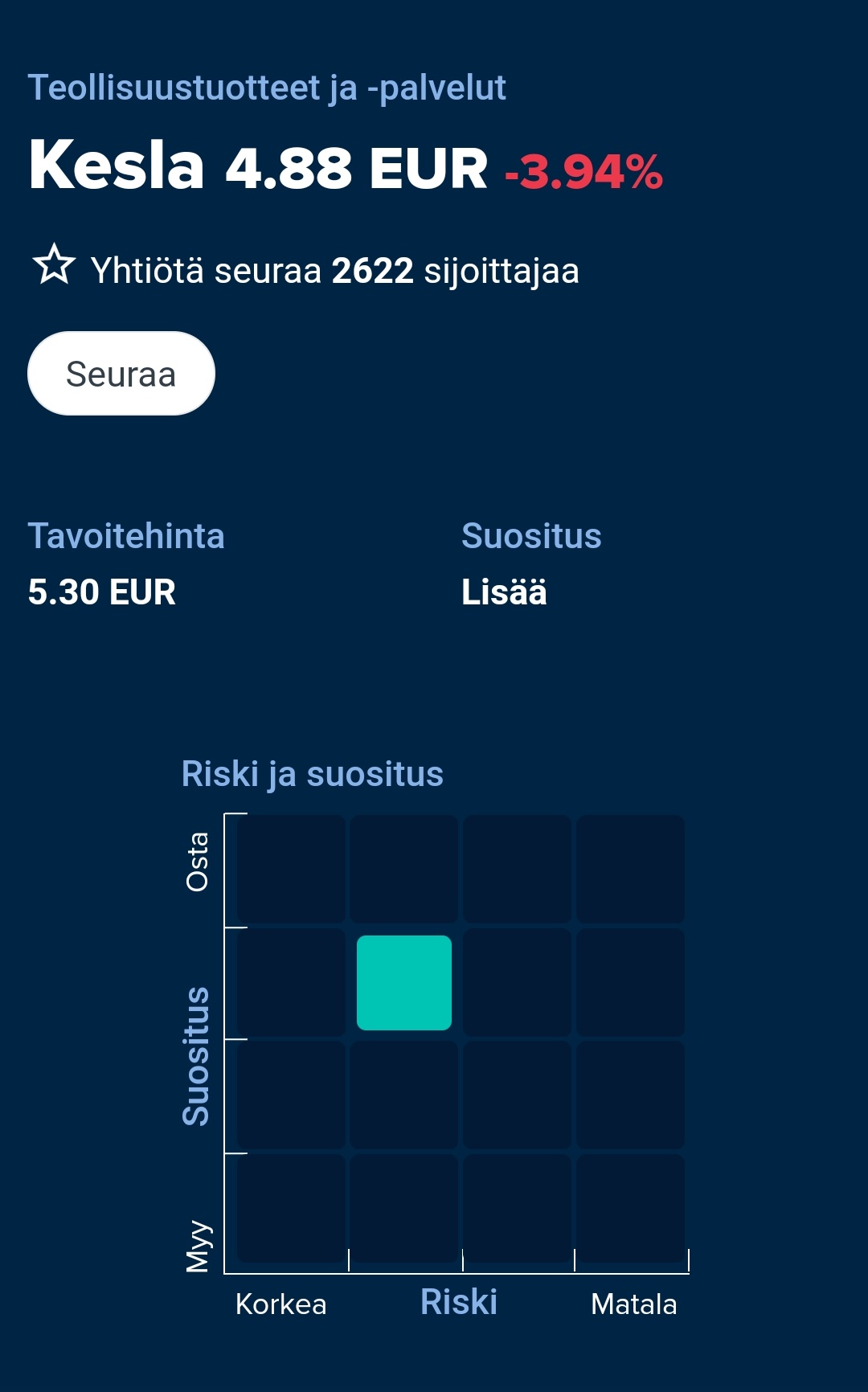

Kesla, in my eyes, is cheaply priced: P/E for this year well under 10, P/B slightly over 1. The equity ratio is around 40%, so there is still risk.

Now, let’s present the reason why I started the discussion: the company published its results today, and Inderes’ expectations were exceeded. The EPS forecast for this year is 64 cents, and based on current information, this is underestimated. The company mentions in its earnings release that the upcoming downturn will negatively affect the market, but at least the company is not in a price bubble. If the EPS is 64 cents, the P/E for this year is 8.5.

What views do forum members have on the company? Is it just such an illiquid company that there is no sense in price formation, especially in the short term? Or is the upcoming recession already priced into the stock?

When talking about Kesla, it’s important to keep in mind that the company is extremely cyclical. I remember like yesterday watching during the financial crisis how sales came down at a rate of over 50 percent. As there is no significant service business, this is the result.

Considering the company’s cyclicality and business cycle, I still think it has too much debt. In addition, it should be noted that a significant part of the business comes from Russia, and this has historically been a difficult market.

The stock is (seemingly) cheap for a reason. On the other hand, fortune favors the bold, but I’m not interested myself.

KESLA OYJ INITIATES COOPERATION NEGOTIATIONS CONCERNING ALL PERSONNEL

Kesla Oyj is initiating cooperation negotiations concerning all its personnel (251 people) in accordance with the Act on Cooperation within Undertakings, to adjust the number of personnel and reduce the use of workforce to match the demand in early 2020. The negotiation process is estimated to last until the second week of next year.

According to the company’s preliminary assessment, the negotiations may lead to a reduction of a maximum of nine (9) people and temporary layoffs for a maximum of 90 days, to be implemented by June 30, 2020.

The value of orders received in October-November is clearly smaller than the accumulated value for the corresponding period last year. The company’s invoicing rate has also been higher than the order intake in recent months. Demand in the Russian market, which is significant for Kesla, has remained sluggish in the second half of the year, and uncertainty in demand in the domestic market, also significant for the company, has increased due to shutdowns in the forest industry.

This is how it quickly turns in the other direction too

That’s how it seems to work. Low valuation multiples are completely justified for such a cyclical company. I’ll have to keep an eye on it if it goes too cheap. Currently, I don’t have any of the company in my portfolio.

This company doesn’t seem to have much buzz on the stock market or on discussion forums

So one can always hope or imagine having found some forgotten gem.

However, there’s apparently COVID-19 vaccinations, sector rotation, a Santa Claus rally, and an upcoming January rally, so let’s bring this company back to life for a moment.

Negatives: investment slump in target markets

Negatives: ECB-indicated banking crisis in 2021

Negatives: EU and Russian economies crushed by COVID-19

Positives: stimulus packages/Green Deal = massive infrastructure boom

Positives: pent-up demand

Positives: unused money in accounts returning to the economy

Are there good prospects for the company’s future? Or even good information about the company’s current state, e.g., from the grassroots level?

Hello Ummon, in case you haven’t noticed our comprehensive report on Kesla published at the end of October, and although the report doesn’t address all the points you’ve raised, I’m bringing it up here: Kuntokuurin jälkeen kisasuorituksiin - Inderes. Best regards, Eki

KESLA OYJ STOCK EXCHANGE RELEASE 7.1.2021 at 1:30 p.m.

EU DECISION TO EXTEND SANCTIONS ON BELARUS IMPACTS KESLA OYJ’S BUSINESS IN THE 2021 FINANCIAL YEAR

On December 17, 2020, the European Union decided to extend its sanctions on Belarus to include Belarusian businessmen who benefit from the Lukashenka regime, in addition to key government officials. The decision affects Kesla’s business with the Belarusian forestry and earthmoving machinery manufacturer Amkodor. This is a significant OEM customer for Kesla. The sanctions decision has halted all business between Kesla and Amkodor. If prolonged, the sanctions decision will significantly weaken Kesla’s revenue growth opportunities in 2021.

The sanctions decision is not estimated to have an impact on Kesla’s 2020 financial statements.

{“content”:“At least in my eyes, the result was quite good compared to expectations, which the stock is certainly thanking for a bit today. It seems to have slightly exceeded the forecast of the last broad report in both revenue and profit. \n\nI was wondering why 2 million was adjusted out of the order book, is this about Belarus?”,“target_locale”:“en”}

Good momentum will probably also reflect on Kesla. I believe the Q1 result will also give direction for Kesla’s rest of the year. I personally added it to my portfolio around 4.3 euros, because in my opinion, the valuation is very affordable.

Ponsseltoday reported strong results and a very strong order intake. As noted above, this probably also reflects a good demand environment for Kesla and the Q1 report due the day after tomorrow. We eagerly await Thursday.

It seems that others are also getting interested in Kesla, as it’s seeing a nice rise today. Hopefully, the situation in Belarus won’t weigh too heavily on the results, and they’ll put out good numbers.

Kesla was also mentioned in yesterday’s Kauppalehti as a potential riser in guidance:

The guidance of another forest technology company, Kesla, can also be considered moderate: “The company’s 2021 net sales are estimated to grow, and its operating profit is expected to remain at least at the previous year’s level.” Kesla will publish its results on April 22, 2021.

Q1 was a disappointment, but on the other hand, it was expected that the risks related to Belarus would be high in the short term. January was heavily loss-making, which seems to have been recovered well during March, as the result was not more in deficit. Anyway, the result was weak. On the other hand, the order intake was much higher than forecasts, which indicates a stronger continuation. If one wants to speculate, if the situation in Belarus were normal, the result would have been in a completely different league. Good, however, to note that the guidance was kept unchanged.