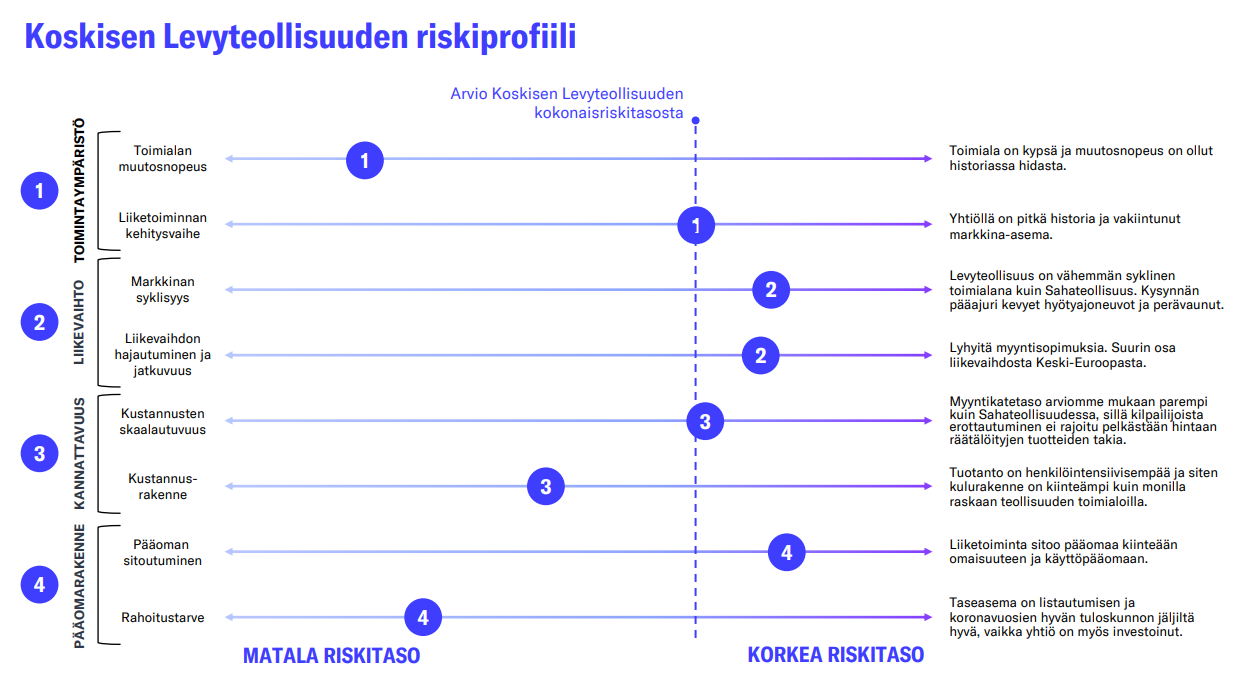

Antti has written a comprehensive report on Koskinen. ![]()

Koskinen is transitioning from the highly active investment phase of recent years towards a slightly calmer period of profitable growth. Furthermore, Koskinen’s earnings performance should receive a boost as global construction eventually recovers from the weak cycle that has prevailed for years. In our view, however, this is appropriately priced into the share, as most valuation methods indicate that the stock’s pricing is quite neutral. We reiterate our target price of EUR 9.00 and our reduce recommendation for Koskinen.

Quotes from the report:

Long-term forecasts

We expect Koskinen’s long-term organic growth outlook to be healthy as environmental awareness and the popularity of wood construction grow in the future. In the big picture, we expect the company to be capable of revenue growth roughly in line with global economic growth, which means 2-3% growth in the long term. However, we note that annual changes can be very strong depending on the stages of the economic and construction cycles. Our forecasts do not include M&A but are based on organic growth.