I wonder if anything has even been done about the cybersecurity issues yet. I wouldn’t want to have these problems dumped in my lap all the time (looking at you, Tietoevry).

Not such a strong performance from Klarna, which is planned to be listed in New York in Q1/2025. Swedish authorities have issued a SEK 500 million (EUR 43.4 million) fine for deficiencies related to preventing money laundering and terrorist financing.

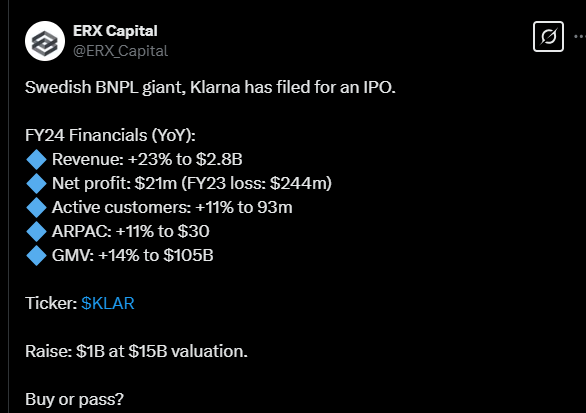

Swedish payment service company Klarna has filed an application for an initial public offering with the U.S. Securities and Exchange Commission. The company plans to list on the New York Stock Exchange under the ticker symbol KLAR.

No wall.

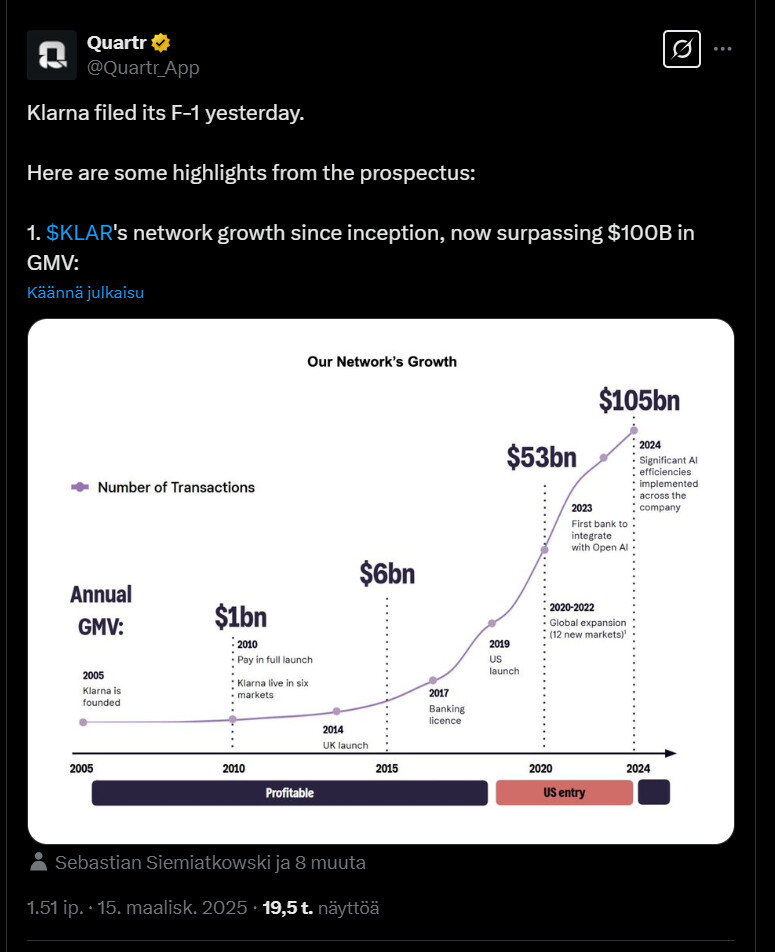

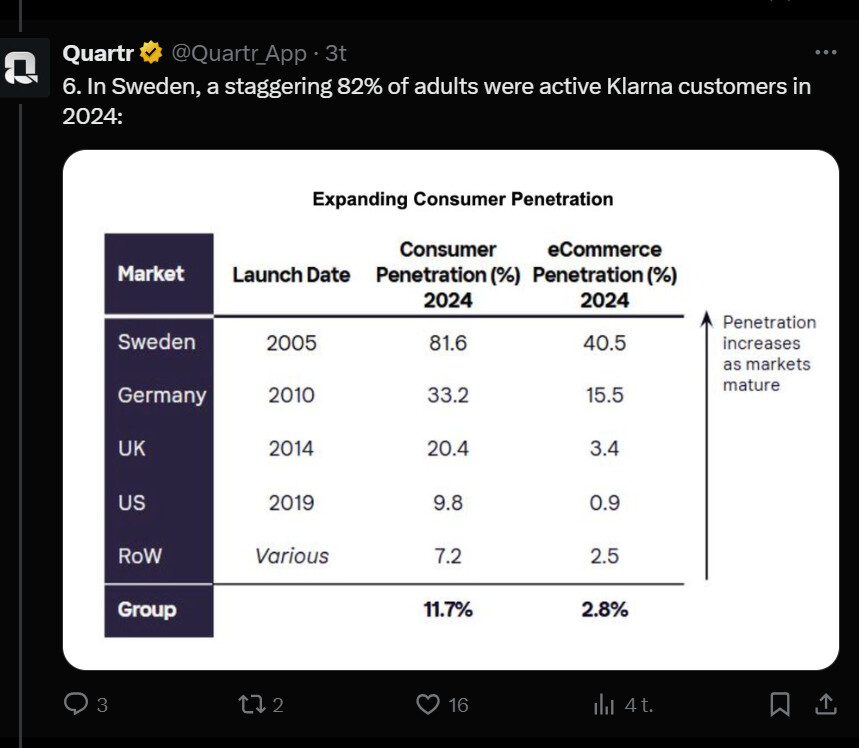

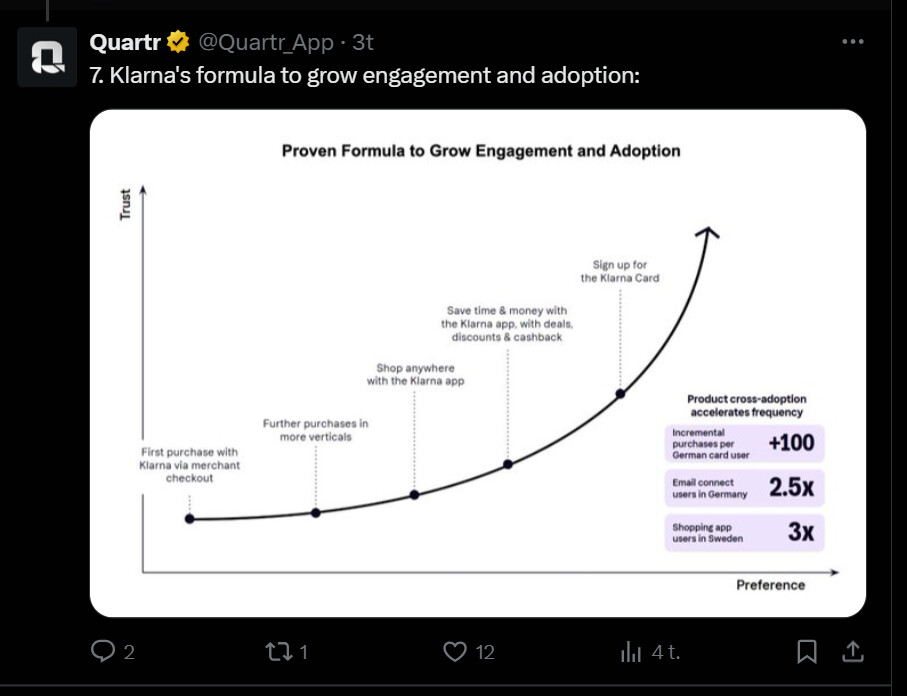

Here’s a tweet thread about Klarna.

The thread reveals how Klarna has communicated the company’s future outlook, such as growing operating profit margins and expanding its user base.

The company’s presentation highlighted its strong growth and profitability, as well as strategies for increasing market share and customer engagement.

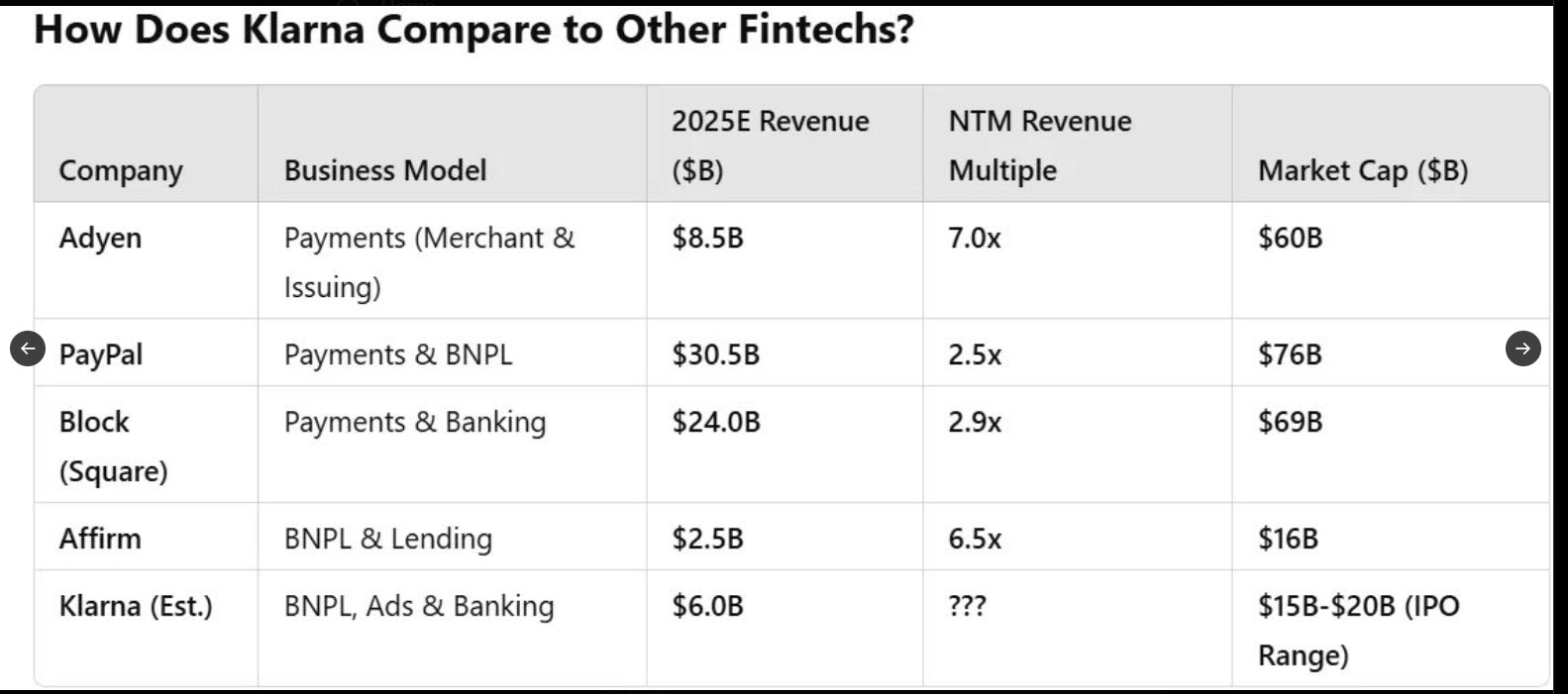

Below is a slightly longer story about Klarna’s IPO application in New York. The article mentions how the company competes against Affirm and Afterpay with its “buy now, pay later” services.

The news also mentions how the company suffered a significant stock price decline after the pandemic, but has since returned to profitability and is now valued at approximately 15 billion dollars. The company also aims to expand its operations in the United States by acquiring a banking license.

Market volatility could still get in the way of Klarna’s plans. The Nasdaq just wrapped up its fourth straight week of losses, closing on Thursday at its lowest level since September before rebounding a bit on Friday.

Data released Friday from the University of Michigan confirmed that consumer confidence has suffered from the ongoing tariff-related uncertainty that’s underpinned the opening weeks of the second Trump administration. Consumer sentiment dropped in March to 57.9, lower than the 63.2 economists polled by Dow Jones had expected.

Swedish fintech company Klarna has secured Walmart’s “buy now, pay later” loan partnership from its competitor Affirm.

This comes just before Klarna’s IPO in the United States. Walmart’s OnePay app handles the so-called “customer experience,” while Klarna decides on loan approvals. The deal is significant for both Klarna’s IPO and Walmart’s fintech expansion. Excellent timing.

The deal is no less consequential to Walmart’s OnePay, which has surged to a $2.5 billion pre-money valuation just two years after rolling out a suite of products to its customers.

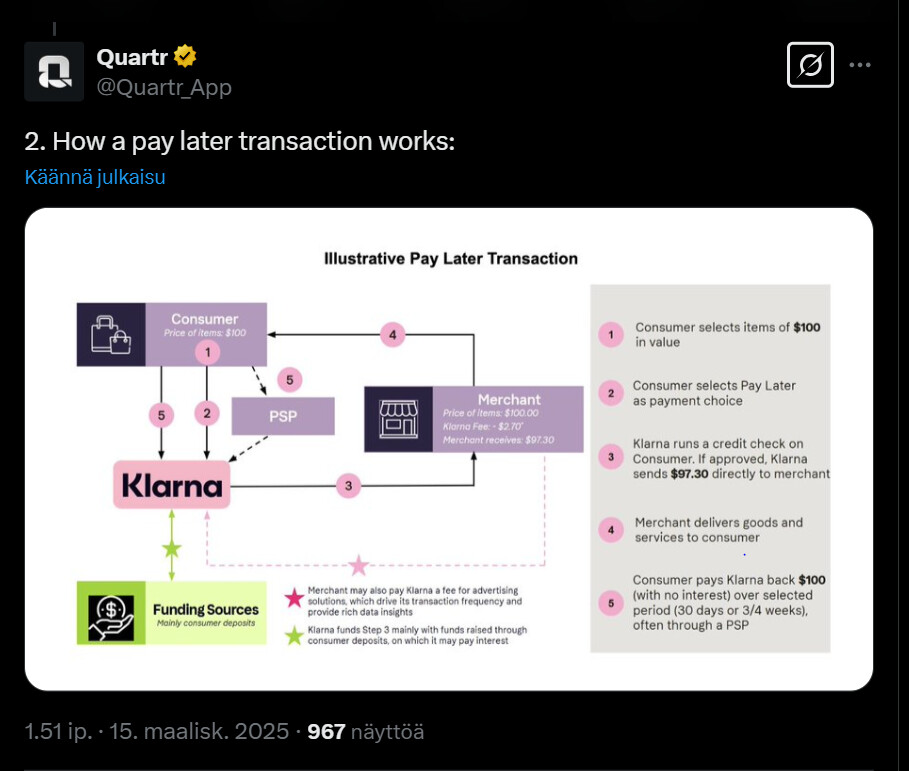

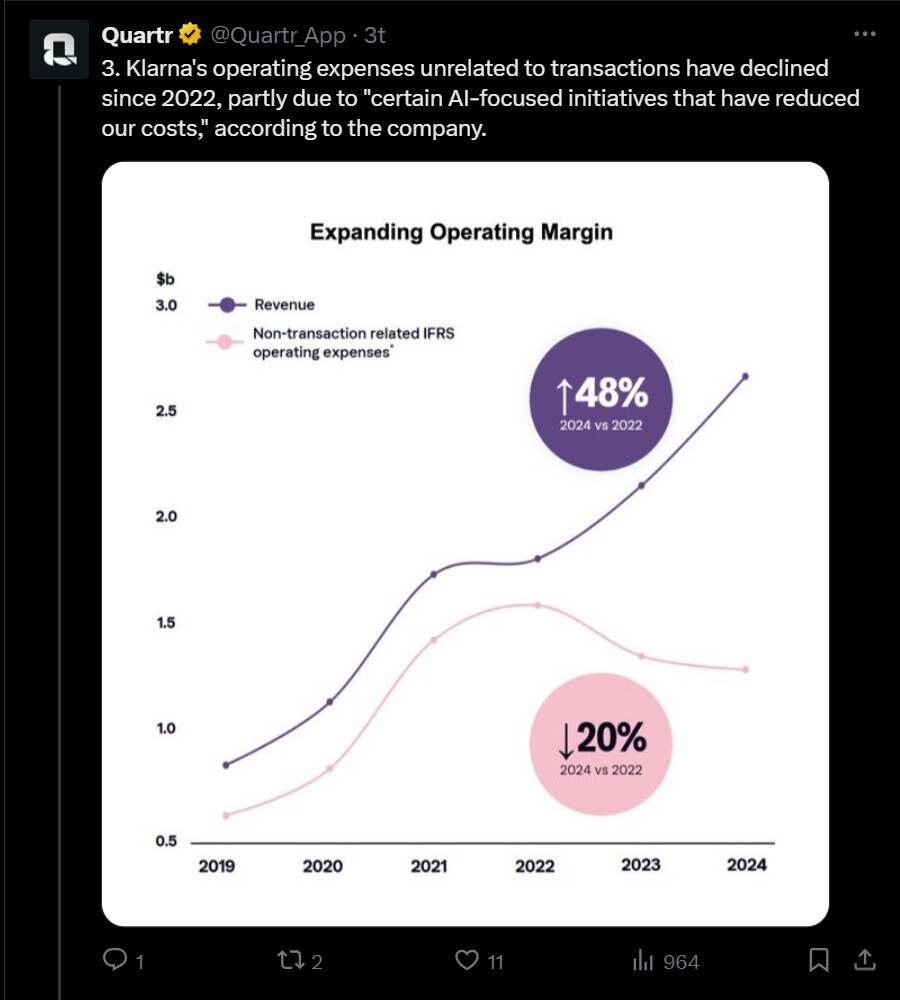

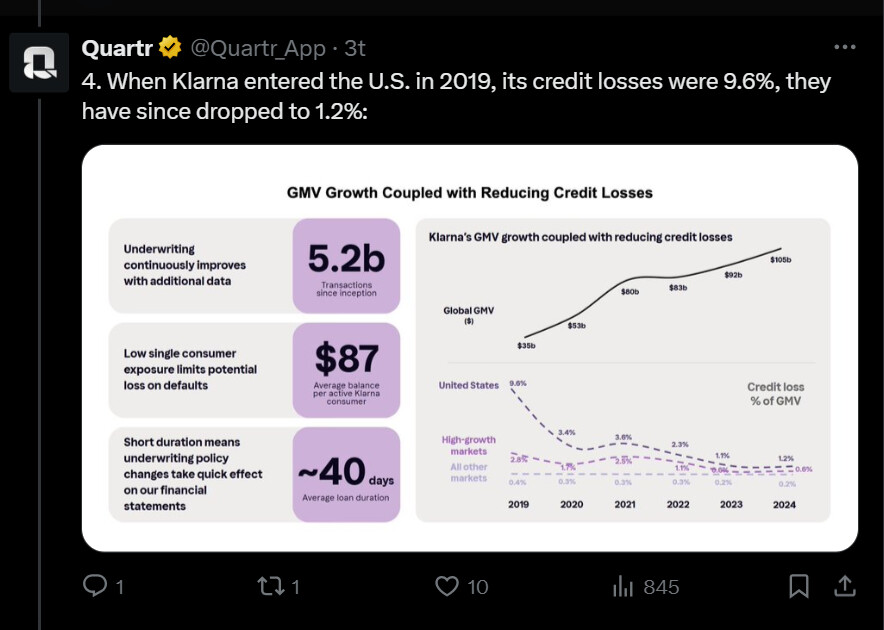

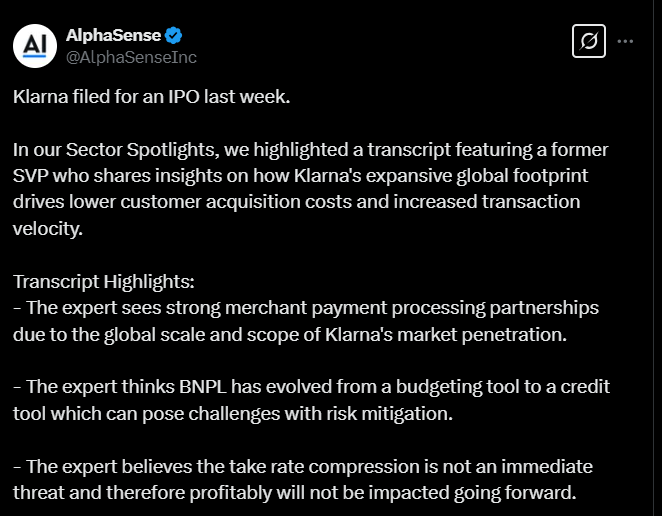

Below is a tweet regarding Klarna filing for an IPO last week. The tweet included some good points, such as:

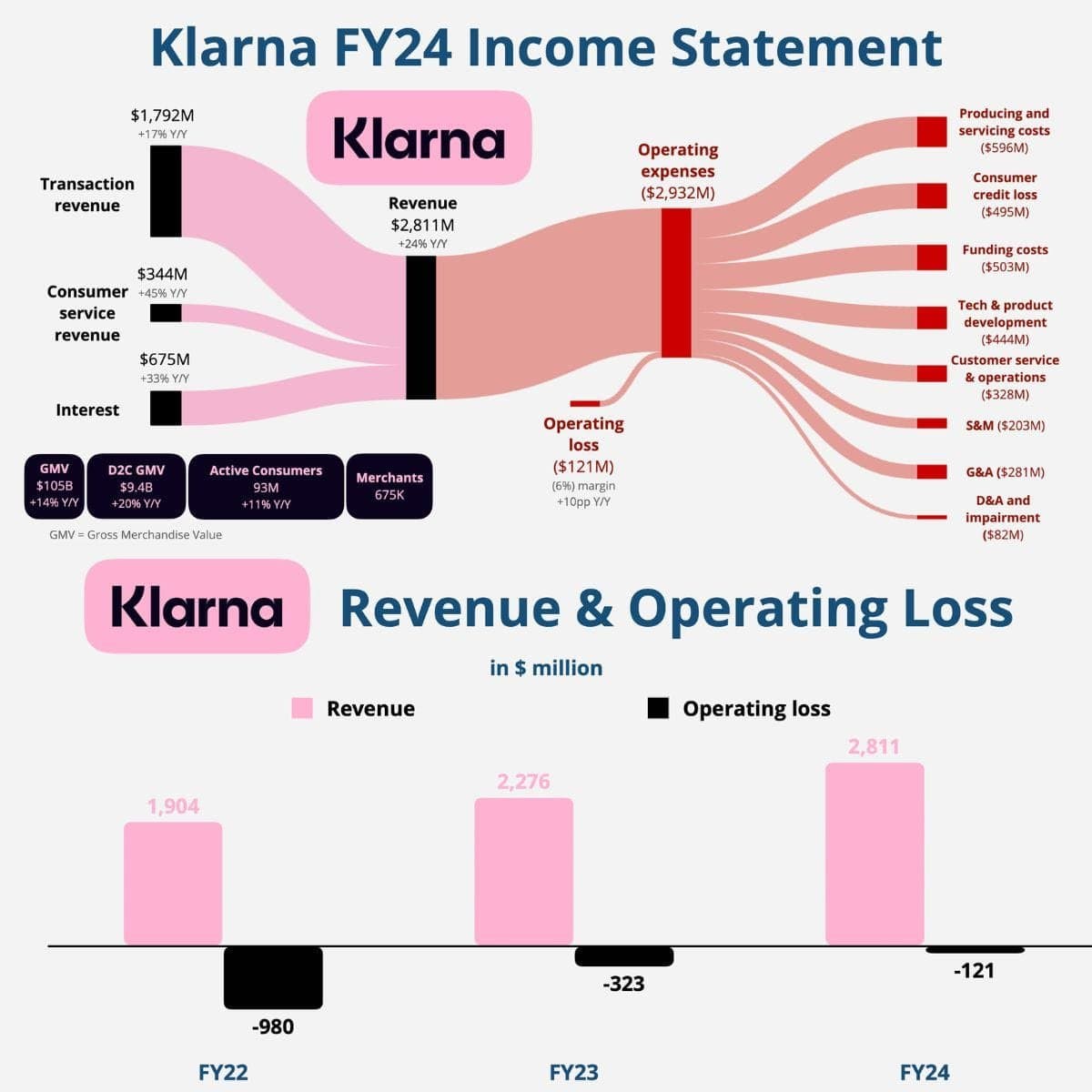

A former executive estimates that the company’s broad market position lowers customer acquisition costs and streamlines payment traffic. BNPL has transformed into a “credit product,” which increases risk management challenges, but a decrease in revenues does not threaten profitability in the near future.

Klarna will certainly benefit from its banking license and its advertising business, but both also have their challenges:

Advantages of a banking license:

Can finance loans with deposits instead of just expensive debt financing (unlike, for example, Affirm).

Enables a broader fintech ecosystem, such as payment accounts and cards.

Can improve margins and reduce dependence on external financing sources in the long term.

Challenge: Deposit growth is slowing, which could limit scalability and increase dependence on market financing?

Advantages of the advertising business:

Growing revenue stream (now ~6% of revenue, but with greater potential?).

Leverages Klarna’s data and user understanding – advertisers can target more effectively.

A natural extension, as Klarna is already at the center of the purchasing process.

Challenge: Is Klarna’s scalability and customer data sufficient to compete effectively in the advertising market?

Summary:

If Klarna can grow both its deposit base and its advertising business, it could transition from a BNPL firm to a full-service fintech platform, which would support a higher valuation. But if, for example, growth falters or regulation hits, the risk of valuation erosion increases?

Below is an article about Klarna and its CEO. The article itself is not particularly timely.

The article discusses how Sebastian Siemiatkowski has been Klarna’s CEO for 20 years and how Klarna is facing a listing on the US stock exchange.

Furthermore, it describes how he has built the company into a successful fintech firm known for its ‘buy now, pay later’ solution. The article also highlights that his career has, however, also seen various challenges, such as a sharp decline in the company’s value, the rise of competitors, and staff layoffs. The CEO defends his choices, states that the company utilizes artificial intelligence, and believes in the company’s future growth. The listing offers an opportunity to raise the company’s valuation and bring in many investors, which would perhaps strengthen Klarna’s position in the market.

According to the article below, Klarna has reduced its staff by about 40 percent as a result of AI investments and natural attrition.

The number of employees decreased from 5,527 to about 3,400. The company has extensively utilized AI, especially in customer service, where AI replaced 700 employees.

This week, Klarna announced that it would back down a bit from its somewhat ambitious goals. They intend to hire staff for customer service, as human contact still cannot be replaced by artificial intelligence.

As Mainari also noted, last year the company indeed replaced hundreds of customer service representatives with AI and praised the efficiency of GPT technology. Now, the CEO admits that AI alone is not enough – the customer experience suffered, and customers still wanted to talk to a real person.

As a result, Klarna is starting a new recruitment wave and is now looking for genuinely interested customer service representatives, including students and remote workers. AI will, of course, remain in use, but human contact will no longer be completely replaced.

A good reminder that technology is a tool – not always a solution to everything (especially in customer service sectors?).

Below is an article about how Klarna announced its first quarter losses doubled compared to the previous year, which was due to one-off costs, such as write-downs and restructuring.

The company has suspended its expected IPO in the United States due to market uncertainty, and even though revenue grew and user numbers increased, Klarna still struggles with profitability challenges.

Klarna haluaa kehittää superapin, joka tarjoaa sekä rahoitus- että arjen palveluja, kuten mm. liittymiä.

Toimitusjohtaja uskoo tekoälyn avulla saavutettavan henkilökohtaisemman käyttökokemuksen ja laajemman roolin digitaalisen “talousapurin” kaltaisena sovelluksena.

Klarna CEO Sebastian Siemiatkowski wants to make the platform more of an all-encompassing financial “super app” that’s personalized and can offer non-financial services.

“With AI, you can abstract and adopt the experience much more to the specific user you’re dealing with,” Siemiatkowski told CNBC in an interview this week.

On Wednesday, Klarna is set to announce the launch of mobile phone plans in the U.S. via a partnership with telecom services startup Gigs.

Here’s a story about Klarna planning to return to the US stock market with a valuation of approximately 13–14 billion dollars. That is clearly less than the previously targeted nearly 50 billion.

Klarna, which reshaped online shopping with its short-term financing model, said earlier this month that its second-quarter revenue rose 20% from a year earlier on a like-for-like basis to $823 million, while adjusted operating profit was up $1 million to $29 million.

The article below contains some overlapping information with the previous message, but also something new. Indeed, Klarna is seeking $1.27 billion in “funding” in its New York stock exchange listing.

Approximately 34 million shares are being offered at a price of $35–37, so the company’s valuation could reach around 14 billion. The ticker symbol will naturally be “KLAR” and the lead arrangers in this process are, of course, major investment banks.

The filing with the Securities and Exchange Commission also revealed the company’s latest financial figures. Revenue for the June quarter rose 20% year-on-year to $823 million. Klarna posted a net loss of $53 million widening from the same period last year.

This is not a thesis per se regarding Klarna’s value rising or falling, because the markets do exactly as they please, regardless of how anyone feels or how anything looks. But I myself, even with the best will in the world, could not invest in a company whose primary business model is to sell expensive money to those who cannot afford to pay it back. And I find it hard to believe that it would be profitable in the long run either.