Wasn’t its valuation something like 45 billion in the 2021 funding round?

Seems like tax sales are coming…

Edit link:

Wasn’t its valuation something like 45 billion in the 2021 funding round?

Seems like tax sales are coming…

Edit link:

Klarna priced its IPO at $40 per share, valuing the company at approximately $15 billion.

The article also states that $1.37 billion was raised in the IPO, most of which, of course, goes to existing shareholders. The company reported a $53 million loss in the second quarter, but revenue still grew by 20 percent to $823 million.

Of the total amount being raised, $1.17 billion is going to shareholders with just $200 million going to the company.

https://www.cnbc.com/2025/09/09/klarna-prices-ipo-at-40-above-online-lenders-expected-range-.html

Klarna Groupin osake laski perjantaina ensimmäistä kertaa alle listautumishinnan, 39 dollariin.

Laskua vauhdittavat alla olevan jutun mukaan kiristyvä kilpailu fintech-sektorilla sekä epävarmuus Yhdysvaltain korkopolitiikasta, lisäksi Rivien Stripe ja Revolut painavat päälle.

Shares of peers Affirm Holdings Inc. and Block Inc. were also weak Friday. Like Klarna, the stocks extended at least four-day losing streaks.

The slump also comes after valuations on a string of competitor fintech firms, which have stayed private longer, were reported to rise. Stripe Inc.’s valuation has climbed to $106.7 billion, while Revolut Ltd. is looking to clinch a $75 billion valuation. Even Checkout.com, another European rival, announced on Friday a fresh $12 billion valuation with a tender offer to staff.

Klarna’s stock rose when the company announced a new partnership with Google Cloud. The aim is to accelerate AI-based development and improve customers’ shopping experiences.

The partnership will reportedly bring even more personalized and visual content to the Klarna app, such as AI-generated product recommendations. At the same time, AI will also be utilized to improve security and combat fraud.

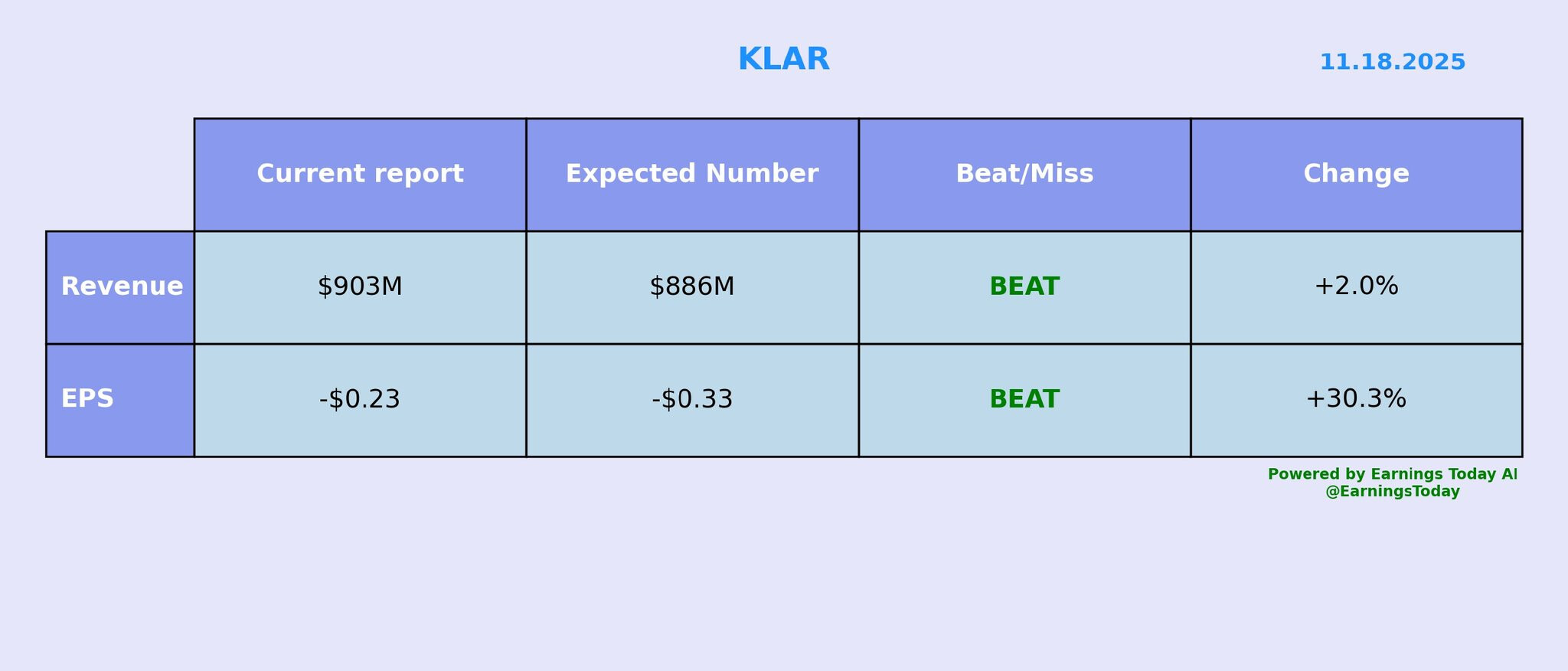

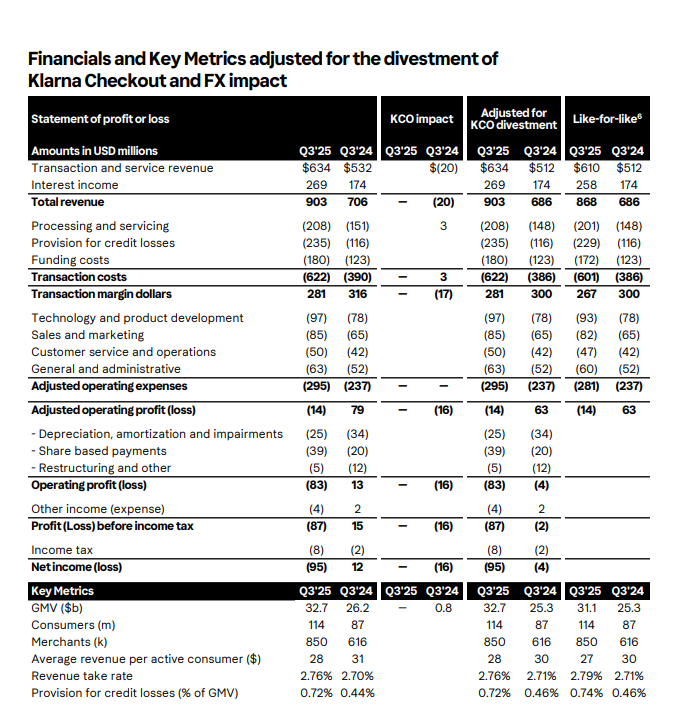

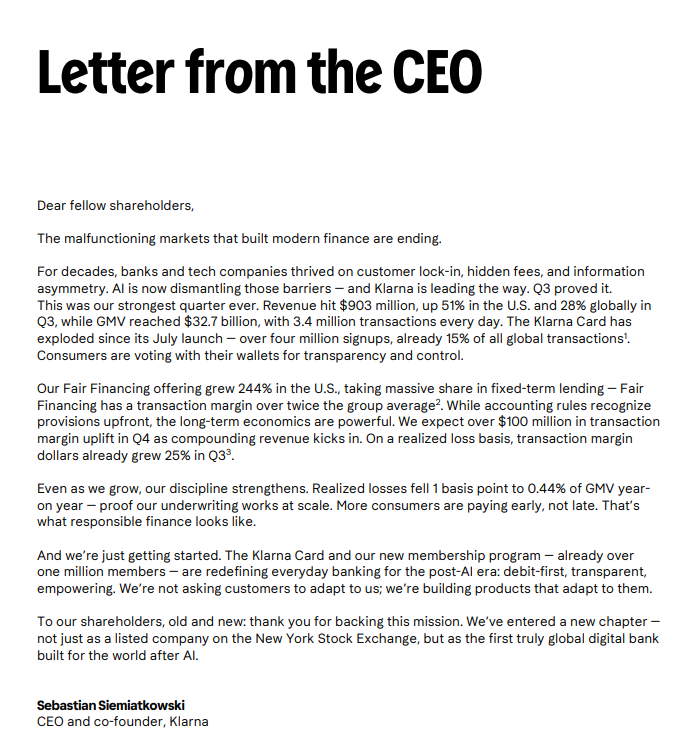

Klarna’s Q3 included record-strong growth, driven by strong traction and spending in the US and the breakthrough of the Klarna card. At the same time, aggressive expansion into longer-term credits eroded profits, as credit losses were recognized upfront. The company emphasizes that this is, however, only temporary pressure and growth investments.

Klarna is expanding some of its US credit products through an agreement with Elliott Investment Management. Funds managed by Elliott will purchase both existing and new US credit receivables, which in turn provides Klarna with flexible and off-balance-sheet financing. The arrangement supports the growth of consumer loans and additionally improves the company’s financial flexibility and, of course, capital efficiency.

https://x.com/EarningsToday/status/1990793772641497487

Klarna CEO Sebastian Siemiatkowski says that the credit card system “fleeces” the poor; for example, according to him, some card bonuses transfer about $15 billion a year from the poor to the wealthy.

Trump is calling for a 10 percent interest rate cap, while Siemiatkowski would like to see it as low as 0 percent. Klarna is growing in loans and cards, but promises, according to his words, to follow the rules.

The cap proposed by the president “could wipe out earnings from cards for a year,” Mike Mayo, an analyst at Wells Fargo & Co., has said in a note. The idea “would ruin card economics (eliminate most of card earnings today) and incentives would be to stop lending,” Mayo said.

Mayo added that if general availability of traditional credit card loans is reduced due to rate caps, the attractiveness of buy-now, pay-later firms such as Klarna and Affirm Holdings Inc. could increase.

Klarna is growing outside the stock market, and there is still a 180-day lock-up period for those who invested before the IPO.

Also, if credit card companies return part of their commissions to customers to encourage them to use the credit side, is it really taken from those who use credit?

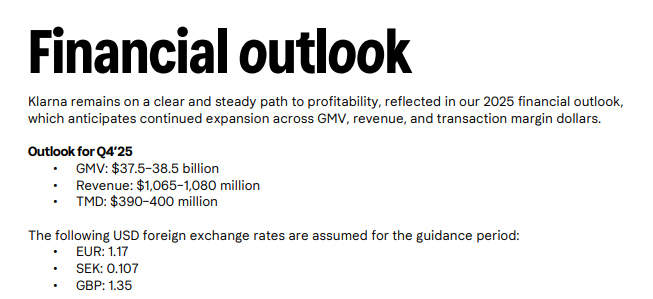

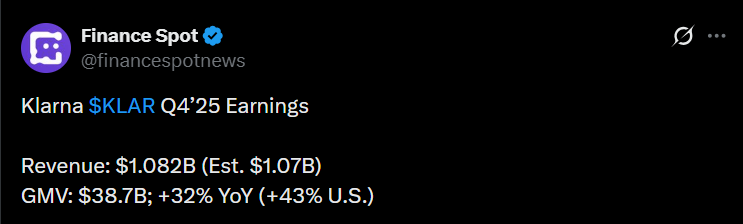

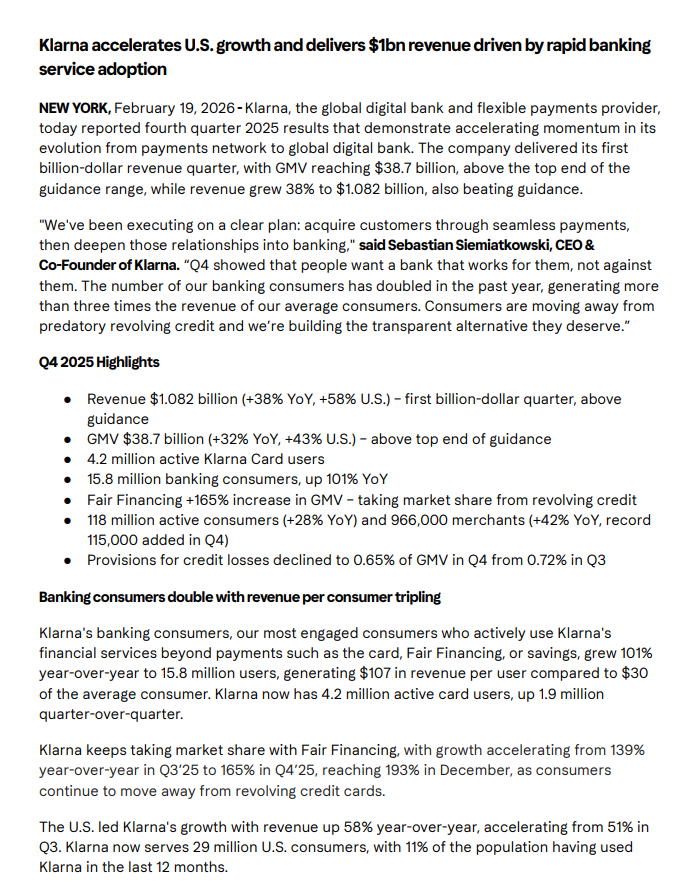

Klarna’s quarterly revenue exceeded the billion-dollar mark for the first time. In particular, the strong performance of the US market and the doubling of the number of banking service users boosted the company’s growth. But the big picture wasn’t all that great.

The company managed to grow its volume more than expected, but the reported loss and the “more moderate” than expected future outlook were not exactly to the market’s liking. Growth was impressive, but stabilizing profitability at a good level still requires work and time.

https://x.com/financespotnews/status/2024487824716620250

Klarna’s stock market journey has been peculiar. The share price has dropped like a stone

and if I understood correctly, 90% of the shares will only be released for sale on March 9th after the 180-day lockup.

Explain to me in simple terms why anyone would pay anything for this loss-making company? It brings to mind Oatly, or Beyond Meat… etc… And in this case, it’s not enough that it might eventually make a profit.

A dedicated company page for Klarna was created on inderes.fi today, so be sure to follow the company! ![]() A recording of yesterday’s audiocast was also published.

A recording of yesterday’s audiocast was also published.

Article about Klarna’s struggles, no paywall.

Jussi Halme has made a good video about Klarna ![]()

Klarna made headlines last year with its multi-billion IPO, but the party was short-lived. The stock’s valuation has melted away, and many retail investors have burned their fingers. But does the stock price tell the whole truth?

In this video, we dissect Klarna’s recent Q4 2025 results. Although the company generated its first-ever billion-dollar quarterly revenue, the market reacted sharply downwards. Why?

Klarna is no longer just a “pay later” button in online stores. It is transforming into a full-fledged digital bank that challenges traditional players with its Fair Financing model. Is this a sustainable revolution or just Wall Street hype?

Note! The video does not contain investment recommendations. Remember that investing always involves the risk of losing capital.

The text below reflects on when Klarna was one of the fintech stars of the 2021 hype era, but at the time, many considered the valuation to be too high. According to the author, the situation has changed; the IPO took place in 2025 at around $57, but the share price has since collapsed to about $15.

The author emphasizes that Klarna is no longer just a “buy now, pay later” service, but has expanded into a digital bank featuring cards, savings accounts, a shopping app, and even its own advertising platform.

The company now has 118 million users and nearly a million merchants; furthermore, revenue grew to approximately $3.5 billion last year. Growth is also supported by AI, which has reportedly helped cut costs drastically.

According to the author, the market may now be too pessimistic; the company is still growing rapidly and has plenty of cash on the balance sheet. He admits that there are certainly risks, such as credit losses, competition, and regulation, but at current prices, he believes the risk-reward ratio looks attractive.

I’ve been watching Klarna for years. It was one of those European tech stories that everybody talked about during the 2021 hype cycle, when Softbank and others pumped the valuation to almost $46 billion. Back then I stayed away – the numbers didn’t add up at that price. Fast forward to March 2026: Klarna IPO’d in September 2025 near $57 per share, the stock has since crashed to roughly $15.70, the market cap sits at around $6 billion, and suddenly the math looks very different.

I want to be transparent: I bought Klarna shares in the $13–14 range for both the Wikifolio and the Haas invest4 innovation fund. That position is already slightly in the green, but let me walk you through why I believe this is one of the more compelling fintech setups on the market right now, and also why this opportunity exists in the first place.

Iikka made a video about Klarna ![]()

Now that’s a title to my liking ![]()

Klarna off to a strong start for the year. My own optimistic expectations, as well as consensus, were exceeded, and surprisingly they even achieved profitable growth. This ticker remains a risky bet, but there might be an opportunity for brisk growth here.

Q1 2026 Highlights

GMV: $33.7 billion (+33% YoY); U.S. +39%, ex-U.S. +31%

Revenue: $1.0 billion (+44% YoY)

Transaction Margin Dollars: $389 million (+44% YoY)

Adjusted operating profit: $68 million, up from $3 million a year ago

Operating income: 17 million versus a loss of (90) million in Q1 2025

Net income: 1 million versus a net loss of (99) million in Q1 2025

Provisions for credit losses: 0.55% of GMV versus 0.54% in Q1 2025

Active consumers: 119 million (+21% YoY)

Merchants: 1 million+ (+49% YoY)