Yeah, I agree with this! Taxation can make a difference. I was speaking about the principle that one could reinvest those dividend funds to counter dilution. Taxation then depends on the investor and whether they use an Equity Savings Account (OST) vs. a regular brokerage account (AOT), etc.

6 Likes

But the matter itself, namely the large acquisition, is a good thing. It complements Kesko’s portfolio nicely. By the way, Antti Herlin just mentioned that old truth in an interview: if a company doesn’t grow, it shrinks relatively and begins to wither, because competitors will certainly grow and take up market share.

33 Likes

The Dahl acquisition summarizes quite well what Kesko has been about in recent years. Growth is being pursued, but the return on capital employed (ROCE) has slid from about 17% to just over 10%, and now over a billion more is being added to the balance sheet in one go.

I did a longer analysis on the subject.

I finally finished the video after a busy week of work. I was almost ready to film, but the Dahl announcement on the same day forced a pretty significant rewrite. ![]()

Link below. Corrections and differing viewpoints are more than welcome.

59 Likes

Thank you for the excellent critical analysis. It is exactly this kind of reflection that brings added value to fellow investors, regardless of the conclusion one reaches for themselves. I subscribed to the channel immediately.

8 Likes

Thank you for the well-structured analysis and the clear, calm delivery; I’m subscribing to the channel right away.

I enjoy listening to investment-related content when I have to perform manual, somewhat boring, and repetitive tasks—but if the audio is too entertainment-focused or some rambling stand-up style podcast, then multitasking either compromises the quality of my work or my ability to absorb the essential information.

4 Likes

Osakepoimija, thank you for the thorough analysis. I appreciate it when an investor like you digs deep into the numbers. It improves the quality of the discussions here. However, I feel your video paints an overly bleak and one-sided picture of Kesko’s situation. In this response, I will try to paint a different picture.

You are right; ROCE (Return on Capital Employed) has decreased from the peak years of 2021–2022. However, the reasons were exceptional (COVID-19, staying at home, cheap money, the renovation boom). In my opinion, a level of 10–11% is not a catastrophe, but a return to normalcy at the bottom of the cycle. I don’t know if you missed it, but Q1/2026 already showed a clear turnaround. Revenue grew in all segments, comparable profit improved, and cash flow turned positive. As I understand it, Kesko’s target (>14.5% ROCE) remains in effect, and measures are underway (efficiency programs, portfolio optimization).

The Dahl mega-acquisition is not a risk, but a strategic move. If I understood you correctly, you present the deal as a risk that ties up capital and dilutes shareholders. I believe it is a historic opportunity. The Building and Technical Trade division will become a leading player in Northern Europe. Dahl particularly strengthens B2B technical trade, which is a growing, less cyclical, and higher-margin area. The deal brings scale, synergies, and geographical diversification (Sweden, Norway, Denmark). Finland is a small market; growth must cross borders. Dilution is temporary. In the long run, high-quality acquisitions increase EPS (Earnings Per Share) and dividend payment capacity, not weaken them.

Kesko’s moat and business model are stronger than they appear. Grocery trade (64% of profit) is still the strongest runner-up in Finland. The K-retailer model combines the benefits of a chain with local entrepreneurship—something competitors cannot easily copy. Loyalty data (over 2.7 million active users) and over 800 million euros in benefits for customers create a digital head start. Building and technical trade and car trade are cyclical, but that is precisely why they offer turnaround potential. When construction picks up, Kesko stands to benefit significantly.

Dividend sustainability and shareholder value. Kesko has paid a dividend since 1968 without interruption, and that is no coincidence. It holds a “Dividend Aristocrat” status, which is rare in Finland. Although the payout ratio is high, a strong balance sheet and improving cash flow support dividend growth in the long term. The Dahl acquisition is an investment in future dividends, not a threat to them.

Quality scoring is always a subjective view. I see things differently. Kesko has a strong brand and market position, a diversely managed portfolio, the courage to invest in growth at the bottom of the cycle (a classic move), and leadership in responsibility and digital development (the K-Group is a pioneer in many areas).

56 Likes

Thank you for the thorough comment! It is exactly these kinds of comments I want to read; they make the discussion better.

I took the Q1 turnaround into account in the video, and you are right that the direction was upward. Revenue grew in all industries, cash flow turned positive, and comparable operating profit improved at the group level. A few clarifications, however: Earnings improved in only two out of three divisions, as the comparable result for car trade already weakened in Q1. And in May, car trade sales fell by more than 9% while the entire group’s comparable growth stalled at less than one percent. That is why I don’t see one quarter as a confirmed turnaround yet, as a cyclical turn is rarely a straight line upward.

I agree with you that the peak of '21 and '22 was born out of exceptional circumstances, and I am not comparing the current state to that. But the current ROCE of about 10–11% also falls clearly short of Kesko’s own long-term target of over 14.5%. So, it’s not just about cyclical normalization, but a level where the company is currently not reaching its own return on equity target. And it is precisely into this already below-target return level that significant additional capital is now being directed through an acquisition.

The Dahl deal needs to be looked at from many angles, and I agree with you that growth and internationalization are fundamentally good things. Analysts are also on different lines. Inderes is positive (Accumulate rating, sees long-term value creation and considers the price neutral), while many others, such as OP, are more reserved regarding the price and the lack of a synergy target.

Personally, I wouldn’t get stuck on the strategic logic of the deal; I think that is clear. Instead, I am concerned about the return on capital. The group’s Return on Invested Capital (ROIC) has already dropped significantly, and when more than a billion euros enters the balance sheet at once—with a large part of the purchase price recorded as goodwill—ROIC will sink in the short term due to pure mathematics. Synergies are a promise of the future, but the capital is committed immediately.

Regarding the moat, I brought up the points you mentioned (K-retailer model, loyalty data, store locations) in the video. The moat in the grocery trade is genuine and strong; there is no dispute there. My point is that Kesko’s competitive advantage is not as strong in the building and technical trade business as it is in the grocery trade. The Dahl deal targets specifically this segment with the weaker moat, which raises the group’s average risk level and lowers the quality profile.

Regarding the dividend, Kesko is not a true “dividend aristocrat.” The title of aristocrat requires a continuously growing dividend, and Kesko’s dividend hasn’t increased every year (for example, €0.90 in 2024 and 2025). Nevertheless, it has paid a dividend without interruption since 1968, which is certainly commendable. In capital allocation, it’s worth remembering that money cannot be “earmarked.” Euros are fungible, so one cannot say that some euros go to dividends and others to an acquisition. It is all from one and the same treasury, which simultaneously funds a high dividend, a billion-euro acquisition, and domestic investments.

On top of that comes the €500–700M share issue, which finances the deal partly with new equity instead of debt to keep leverage in check. The issue dilutes the current owners’ stake immediately, but the final impact depends on how well that invested capital eventually performs. This doesn’t make the deal bad, but it is a cost that should be included in the overall assessment.

Perhaps the biggest difference in our views is ultimately the time horizon. You are looking primarily at what Dahl can do for Kesko at best in five years. I, on the other hand, am looking primarily at what today’s realized figures say about the company’s quality right now. Both angles are justified; they just answer slightly different questions.

And you are right that the quality scoring is a subjective view, even though it relies on fixed thresholds. The scores also evolve over time. If ROIC turns up and the Dahl integration delivers, I will be happy to raise them.

Thanks again for the challenge; exactly this kind of discussion can sharpen the thinking of both parties. ![]()

37 Likes

Return on capital is obviously important to an investor, but as an amateur investor, I have always looked at earnings more than the return on capital. And perhaps other things even more so (since earnings are usually already priced in). I remember when Fortum once sold its electricity grids in Sweden and the Stockholm area, justifying it with a low return percentage—maybe 4-5%. I thought it was a stupid move then, and without investigating further, I still think it was stupid. Well, fortunately, as an investor, you get to choose your investment targets yourself; Kesko has always paid dividends and, as I understand it, has also financed larger acquisitions through share issues. That doesn’t bother me. I own a small amount of Kesko shares; I personally like this acquisition, and for me, it is the most important reason to increase my holding, if that happens. The dividend doesn’t play a big role, but it doesn’t hurt either—at least the taxman gets some income too.

21 Likes

This post might fit better in the “state of the economy” or “construction companies” threads, but since this involved discussions at a Kesko K-Rauta, I’ll write a few sentences here regarding the market sentiment (Note: from a single point of view!) from the perspective of a construction supply store.

I visited a K-Rauta this week and had the chance to talk for quite a while with a salesperson on the construction side while shopping. His comment was that, from their store’s perspective (in the Helsinki metropolitan area), construction hasn’t nudged forward in a way that is really visible in their shop. The “big players/developers” are still waiting, even though there are “permit applications etc.” pending with the cities. Small renovations aren’t being done because small operators (“a van, a trailer, and three employees”) aren’t really participating in customer tenders, leading renovators/buyers to postpone decisions. Companies want to keep their margins intact and would rather do, for example, just one renovation than five. One example of the former was when a customer told the K-Rauta salesman that they wanted to do a slightly more extensive renovation on a detached house (bathroom, sauna, etc.) and had requested quotes from 5 different local operators; the cheapest quote was only about €3k-5k different from the most expensive one. The customer stated that from their perspective, the cost was still a bit too high, so they decided to postpone the renovation since the need wasn’t acute yet. The K-Rauta salesman wondered about this—that smaller renovation firms want to hold onto high margins with tooth and nail and would rather do just one—if even that—renovation in the summer and rest on their “laurels” for the remainder of the time.

In summary, the salesman noted that the situation is rather poor; the bigger players haven’t started moving and smaller renovations aren’t turning the ship around yet either. He didn’t see a big difference compared to last summer and wondered what next year would be like… eventually, he noted that at some point the “ketchup bottle” has to open, properties eventually must be maintained and new ones built. Right now, this isn’t really showing yet in his K-Rauta store.

Regarding the discussion above, it’s good to note that this is a single salesman in a single K-Rauta. Maybe everyone has gone to Puuilo!? ![]()

PS. I don’t own Kesko shares, but I thought I’d spend the afternoon writing down today’s “lynching” (boots-on-the-ground observations) on the Kesko channel for those interested in Kesko / who hold the stock. ![]()

26 Likes

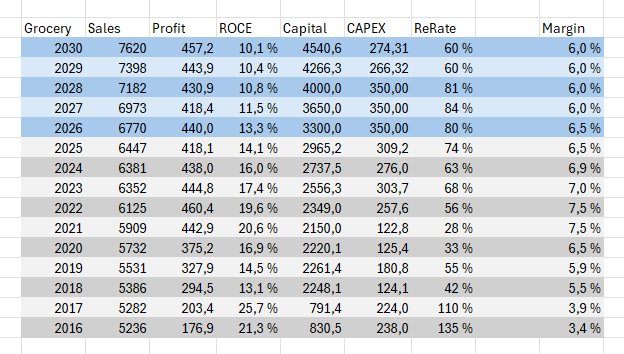

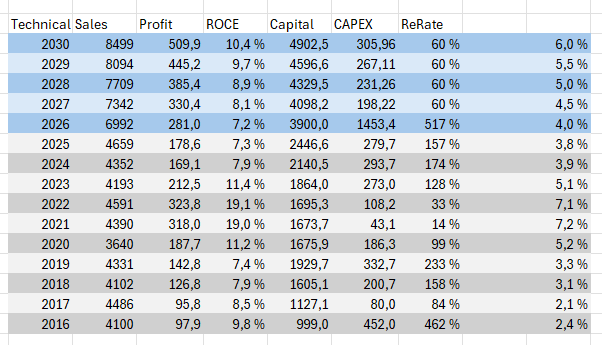

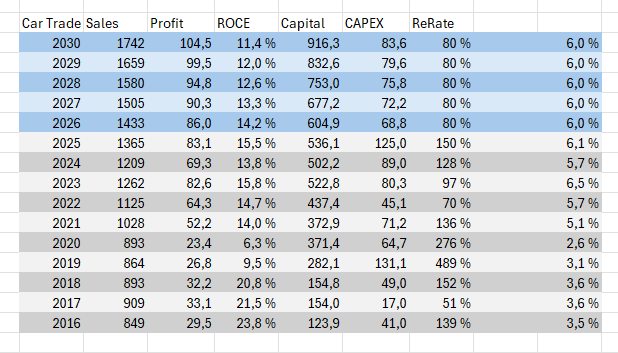

Kesko has one delightful side as a company – the format of their annual reports hasn’t changed much in the last decade, and they kindly report return on capital and investments by segment. The “Capital” line hasn’t been visible this decade, but if you know the operating profit and ROCE%, you can relatively simply calculate an estimate of the capital employed they use to measure their results.

By segment over the last decade, €2.16 billion has been invested in grocery trade, €2.25 billion in building and technical trade, and (to my surprise) just under €715 million in car trade.

Relative to investments, revenue growth has been modest (2% CAGR in grocery and technical trade and approx. 5% in car trade), but profitability has improved across all divisions.

Looking at the past 10 years as a whole, it strongly appears that the first half was spent successfully raising profitability, after which they started investing in growth. The flip side of this is that after five years of cost optimization, the capital return figures, which looked excellent, are taking a hit.

~15% return on capital and rapid growth to reach a €20 “yard” (billion) revenue have always been targets in tension with each other, and large acquisitions tie up significant amounts of capital, making it harder to reach the target – at least in the short term.

In my opinion, a 5-year time horizon is still short in an investment context. I don’t think you can assess a company’s quality over a shorter period, whether it’s reviewing performance or forecasting the future.

I share your concern that reaching the ROCE% target seems quite distant, but this doesn’t just apply to the technical side; they’ll have to work exceptionally hard in the grocery side too, and planned investments in new hypermarkets will weigh on figures there as well.

I prepared some small calculations to visualize the situation: the situation over the past 10 years and a schematic forecast until 2030. The figures are from Kesko, I haven’t bothered to double-check them – this is for fun and sport, after all. My own errors are also very possible.

In the grocery trade, I have tried to account for the investments planned for the store network until 2028, both as increased investment costs and as a higher sales growth percentage (compared to the previous 10-year period).

I have also made the assumption that the operating margin is declining. Personally, I see the >7% margins of the early 2020s as exceptional, from both a Finnish and a global grocery trade perspective. In such a scenario, capital returns face even more pressure.

On the technical trade side, I allocated Dahl’s reported figures to the year 2026, although the execution will likely only happen next calendar year.

The €95 million comparable operating profit is pulled from the “back of a matchbox” calculation I presented earlier in the thread, and I have allocated €1,200 million of the transaction to capital employed – that matches the purchase price nicely, but when estimating the resulting goodwill, I concluded that previous deals have generated about 1/4 of the purchase prices, and when you add approx. €300 million in lease liabilities as fixed assets, you end up back where you started. “Do work that has a purpose”

In the described situation, the consolidation of Dahl doesn’t actually weaken the division’s capital returns, as its profitability appears to be slightly better than the rest of the entity. I have assumed that growth investments would be put on ice for a moment to digest the large acquisition, and the investment rate would be approx. 60% (the industry average calculated from operational cash flow – in my calculations, I have assumed Kesko’s reported comparable operating profit to be the same figure).

I assume the operating margin will rise to the lower end of the target level, i.e., 6% by 2030, while assuming revenue growth will be slightly faster than general economic growth (not least thanks to investments in recent years). This naturally requires a positive turn in construction.

The end result by the 2030s would be building technology capital return figures perfectly in line with grocery trade – despite the impact of the Dahl acquisition.

In the car trade, I have simply assumed that current profitability and growth rates (on average) would continue until the end of the decade. An 80% reinvestment requirement accounts for the fact that the industry generally ties up more working capital.

Even with these figures, Kesko’s car trade would be excellently profitable.

Under these assumptions, the entire group in the 2030 financial year would generate approx. €18 billion in revenue, ~€1.1 billion in operating profit with a 6% operating margin, and the group’s capital employed would be a little over €10 billion. The return on capital would thus be just over 10% – a decent result in itself, and since the weighted average cost of capital (WACC) would be about 3 percentage points lower, the entity would indeed create shareholder value. The Dahl deal would also have been profitable.

Even though I conclude that all business areas would be roughly equally profitable in terms of both margins and capital returns when calculated this way, it’s good to note that the grocery trade is significantly less sensitive to economic cycles.

Therefore, it is more valuable to earn 100 million there than 100 million as an HVAC wholesaler, and both are more valuable than 100 million as a car dealer.

Regardless, I believe it is a good move for Kesko to focus on growing the technical trade; firstly, the Finnish food trade is saturated to the limit and cannot (in the long run) grow faster than the national economy even with the best will. Furthermore, Kesko’s competitive advantages in the field are limited to the domestic market – I don’t see them being reasonably transferable to international growth, and I don’t see Kesko’s moat being nearly as deep as many seem to perceive. The competitor (S Group) has a large number of structural competitive advantages of its own, and recent margins and capital returns were achieved in an exceptional situation and at the expense of future investments (Kesko has, after all, lost market share). To top it off, Kesko’s profitability hasn’t necessarily reflected in the K-retailers’ pockets, and the central organization cannot endlessly tip the scales in its own favor – the retailers are the ones who largely sell their goods. The growth outlook for technical wholesale, on the other hand, can deviate significantly more from general economic development in the short term, and the competitive landscape is more favorable to Kesko. Especially after the Dahl deal, they become by far the largest Nordic player, and no one else would be a corresponding market leader everywhere. Secondly, while Kesko’s performance in the Finnish grocery trade has been excellent by international standards, in the technical side, it is only “good” – in other words, it is entirely possible that it can be improved.

The current strategy or management gives no promises of this, but who knows what the future brings.

Is Kesko a slightly more mediocre company after the Dahl acquisition than without it? Probably.

Will Kesko’s return on capital be lower in the future? Probably.

Is the deal, however, in line with the strategy and in the interest of the shareholder? Probably.

Those are a few of my thoughts on the subject.

P.S. Since we are on an investment forum and I included everything necessary to perform a DCF calculation in my message, I’ll save the trouble for those who want to know the result. With my figures, the terminal value for 2030 comes to almost exactly €17 billion. Discounting with a 6.8% required rate of return, adding 5 years of dividends, and subtracting approximately €4,000 million in debt results (accounting for the 32 million new shares created in the approx. 600 million issue) in a per-share value of 19 euros and some change. I notice once again that I am a redundant analyst when the market always agrees with me…

60 Likes

The retail sector bursts into action – Such hot figures haven’t been recorded in years | Kauppalehti

So consumers have finally woken up from their coma in Finland. Other Nordic countries had already started living normally earlier. Now, Kesko has made an excellent acquisition to expand into an essential player in the Nordic construction sector at just the right time, as growth is finally accelerating and even in Finland, the construction industry has clearly been observed to have started growing. It is great that Kesko’s management has the courage to take great strides toward growth, exactly as has been desired for a long time. Kesko is realizing this desired growth and, given its strong position, can also continue to pay a good dividend.

23 Likes

The link is behind a paywall. Could you share some of the article’s content? What were the hot numbers exactly? (I’m guessing retail growth and consumer confidence).

4 Likes

This week, it was reported that the consumer confidence indicator rose in June to its highest level since February 2022. Consumers are waking up from their slumber, a conclusion that can also be drawn from the figures recorded in the trade sector.

Turnover in trade grew by as much as 7.6 percent in May, according to Statistics Finland (Tilastokeskus). The state of the trade sector is clearly better than a year ago, as working-day adjusted turnover is currently growing in both wholesale and retail trade.

The turnover of the largest sector of trade, wholesale, rose by an exceptionally strong 11.7 percent in May. When wholesale pulls ahead this strongly, it says a lot about trade expectations. In January–June 2026, sales growth has continued and, in part, accelerated.

“Positive rays are already visible”

The trade sector has been through several unusual years, as the COVID-19 pandemic in 2020 and Russia’s invasion of Ukraine in 2022 fueled uncertainty. However, the year 2026 has started better than the years 2023–2025.

Tuula Loikkanen, Managing Director of the Finnish Grocery Trade Association (Päivittäistavarakauppa ry - PTY), believes that the trade figures point to strengthening consumer sentiment. Since the value of the grocery trade this year is nearly 24 billion euros, much can be inferred from such a large sum.

“After six months, it can be said that small positive rays are already visible. The year 2026 has started with better figures than 2025,” Loikkanen states.

“In fact, all trade figures have been positive since last autumn,” she adds.

In PTY’s statistics, the sales of its member companies grew by 2.3 percent in January–May. In hypermarkets and supermarkets, sales grew by 2.8–3.2 percent compared to last year.

According to Loikkanen, the moderate growth in grocery sales overall continues. It is no longer just about value; sales volumes are also increasing.

“Positive sales volume tells even more about the direction of trade,” Loikkanen says.

6 Likes

If you register as a reader for Kauppalehti, you will get access to most articles - it doesn’t cost anything.

2 Likes

I am registered and logged in, and unfortunately, I still cannot see this.

Strange. I can see it even though I don’t pay anything - a shame if you can’t. HEH! Maybe it requires a K-Plussa membership ![]()

2 Likes

You can only get 25 news articles for free from Kauppalehti anymore | Kauppalehti

The revamped Kauppalehti has introduced a paywall. The paper offers 25 news articles per month for free.

7 Likes

Thanks for the info. I haven’t come across this before. As a long-term investor, short-term news isn’t really that relevant.

1 Like