I am opening a thread for an Australian-born renewable energy infrastructure company called Iris Energy (NASDAQ: IREN).

Basic Information

Founded: 2018 in Australia

Listing: Nasdaq, November 2021

Industry: High Performance Computing (HPC) infrastructure — specifically Bitcoin mining and generative artificial intelligence

Market capitalization (May 2025): approximately 680–700 million USD

Management: Founding brothers Daniel and Will Roberts, both operationally and administratively involved

Asset location: North America (Canada and United States), with an emphasis on renewable hydropower

Debt-free company, which is exceptional in the mining sector

Core Business & Infrastructure

The company’s core expertise is:

Building, owning, and operating data centers near renewable energy sources

Optimizing these centers for high energy efficiency computing, such as:

Bitcoin mining

Cloud-based AI computing (HPC / AI)

Data Centers:

Four production sites (British Columbia & Texas)

Capacity April 2025: 9.4 EH/s (Bitcoin), 160 MW (AI computing under construction)

Readiness to expand capacity up to 760 MW without additional land acquisition

Business Model

Iris Energy owns the entire infrastructure chain: land, buildings, electricity contracts, and equipment

No intermediaries such as hosts or renters

Electricity prices are highly competitive: approximately 3.1–3.5 ¢/kWh (hydropower)

Sensitive to BTC price, but break-even at electricity level around 15–18k USD/BTC

→ Current price (over 60k USD) makes operations highly profitable

New Growth Driver: HPC (AI Computing)

Collaboration with NVIDIA

First AI cluster in delivery; client is a US federal agency

Strategy to shift some capacity from Bitcoin to HPC

→ Margins

Iren builds and operates HPC data centers that serve both Bitcoin mining and AI computing. The company utilizes very affordable and renewable electricity (3.1–3.5 c/kWh) in Texas and Canada. The total capacity is already 2.3 GW – and only a portion of it is in use. The growth rate is rapid: hash rate is increasing from 5.6 → 31 EH/s within a year, which would be the fastest growth ever in the history of a publicly listed miner.

A significant part of the growth comes from the Childress data center (750 MW), and a larger 1.4 GW AI center in West Texas will be completed in 2026. Infrastructure and electricity connections are already in place. With these resources, the company can offer capacity to large players (AWS, Google, Microsoft) – but also to private AI computing users.

I believe that the demand for private AI computing (e.g., fine-tuning, inference, AI-startups) will grow rapidly. Cloud giants are slow and expensive to scale. $IREN has a significant head start in capacity, costs, and energy availability – and this is also reflected in profitability: the current fleet operates at an efficiency of 16 J/TH (target 15 J/TH), while the industry average is around 20 J/TH.

Iren’s break-even price for Bitcoin is approximately $18,000–20,000, meaning the company can mine profitably even if the market price drops significantly from the current (~$60,000). This provides a significant safety margin and stability to cash flow.

Combining AI and mining makes $IREN a unique player – not just a miner, but also a scalable AI infrastructure platform.

I personally invested and look forward to the company’s development.

I also have a small position in this, mainly based on the thesis that Bitcoin mining is already profitable in itself, and then the real upside comes from potential cooperation with a major AI player. The price has been crawling for a couple of months now, even though Bitcoin has recovered close to its peak, so I believe there’s significant upside potential.

Iris Energy (IREN) – May 2025 Update

(Nasdaq: IREN)

Iris Energy’s latest financial statements and operational report confirmed that the company has successfully increased its hashrate very efficiently – rising from 12.2 EH/s to 22.6 EH/s in just one quarter. The result was reasonably good, and the company once again demonstrated strong execution capabilities in scaling capacity. An EBITDA margin (52%) and liquidity (427 MUSD) indicate a well-managed and financially sound business, especially in the current interest rate environment.

On the AI front, growth has been moderate so far:

· Q1 FY2025 (September 2024): AI Cloud revenue 3.2 MUSD

· Q2 FY2025 (December 2024): AI Cloud revenue 2.7 MUSD → Slight decrease quarter-over-quarter

Although the clusters (816 H100 + 1,080 H200) have been deployed and initial customer deliveries (e.g., US federal level) have commenced, revenue growth does not yet meet expectations. I would have liked to see stronger revenue growth from AI computing services, but on the other hand, long-term preparation may yield significant results later when the 1.4 GW West Texas colocation campus opens in H1/2026.

The company’s trump cards remain unchanged:

· a completely debt-free balance sheet, which creates flexibility and stability

· significantly lower electricity costs than competitors (approx. 3.1 ¢/kWh with spot pricing)

· fully owned infrastructure without intermediaries

Although the company is progressing steadily, a new addition to my portfolio would require stronger evidence of AI computing commercialization. I would also like to see a potential strategic partnership or merger with a larger data center or hyperscale operator, which could act as a catalyst for the next phase of value creation.

Summary: IREN performs well technically and operationally, especially in the mining sector. The AI business is building promisingly, but the game is still on for revenue growth. A strong balance sheet and a competitive advantage in electricity prices provide security. I will follow the company with interest and hope that the carefully built AI infrastructure will start converting into larger volumes on the income statement as well.

Excellent find, this company! An interesting collection of energy production, computing power, and modern gold without significant dependence on its value fluctuations.

A big minus is that the ‘MINE SAFETY DISCLOSURE’ section of the 20-F has not been used again, even though the company has a mining business

However, I personally perceive the company as riskier than in the quote above. A large amount of hosting has not yet been sold out, and I cannot find any mentioned revenues from balancing the local electricity grid during times when electricity is expensive enough to be profitable compared to BC mining. The latter could, of course, be hidden in the electricity price, but if you find it separately somewhere, I would appreciate it (my reading task is still at the beginning).

Returning to the balance sheet, in the latest report, the majority of the balance sheet funds + a significant dilution of the share base were needed for investments:

so the balance sheet weakened considerably

… and property plant equipment grew explosively.

All of this seems to be fine and bullish because it still looks like the business is in a ramp-up phase and that something bigger is coming.

But I myself cannot yet say whether the company needs more of these same kinds of investments, or perhaps even bigger ones?

This quarterly/semi-annual routine makes me wonder:

But still, as I said, a particularly interesting case

What kind of problems are you referring to with these? My feeling is completely the opposite - of course, the same companies have invested and are investing tens of billions in this. E.g., when a new version of DeepSeek appeared, it took two days for it to be available for purchase as a service from the cloud.

Good reflection – this is precisely why I sometimes type these writings here.

I must raise my hand in error: my previously mentioned “completely debt-free balance sheet” no longer holds true as such. A large share base dilution and a loan were used for investments, which changes the balance sheet structure more than I initially thought.

I did not find revenues from balancing the electricity grid as a separate line item in the report. However, I can’t think of any good reason why they wouldn’t utilize it – the technical capability exists, and as the share of renewable energy grows, its need and value only become more emphasized.

It’s hard to say how much new capital the company will still need in the future, if any. However, as it stands, I would say that the balance sheet can well withstand additional debt if needed.

I currently see mainly two key bottlenecks hindering the growth of AI computing: energy and hardware availability.

Regarding electricity capacity, we are talking about massive needs, and energy connections for new data centers are often a multi-year project – especially when discussing liquid cooling and Tier 3/4 level redundancy. Similarly, the availability of hardware, i.e., GPU chips, remains a bottleneck, particularly for H100/H200 class devices.

Additionally, I believe there is growing interest in the market for smaller players. Not all companies want their business-critical AI workloads directly in the cloud of the largest tech giants. The need for more independent, yet scalable alternatives is growing – and it is precisely in this category that a player like IREN could position itself strongly, if execution is successful.

Ah, this was my own misinterpretation. They generate benefits for locals by balancing energy consumption with their own battery.

The goal is to optimize the cheapest possible electricity for everyone.

Iris seems to have all sorts of support programs etc. for locals and, according to their claim, always hires 100% local people. The more I read, the more I believe.

Judd Arnold wrote about the industry, and especially Iren, at the turn of the year. He stopped using social media after becoming a CIO of some fund in the spring. However, his writings and podcasts still serve as good primers for the industry.

His Twitter account is Lake Cornelia Research, I recall this space was good at least.

Yep. Business cannot be based on BT mining indefinitely, even if with sufficient muscle (compared to others) one could still run that uphill race, which ends in 2040, for some time.

IREN seems to agree

“Our current focus is on expanding our targeted installed hashrate capacity to 50 EH/s in the first half of 2025 and pursuing a strategy to expand and diversify our revenue streams into new markets. We intend to pause Bitcoin mining expansion upon completion of the 50 EH/s buildout to narrow our focus on potential growth opportunities for HPC solutions, including AI Cloud Services and potential colocation services.”

So presumably, the additional investments I feared will follow more AI Cloud demand in the future. Capacity could then be transferred from the mining side, at some cost(?):

“We are exploring the potential opportunity to replace Bitcoin ASICs with GPUs under cloud or colocation service contracts at some of our data centers.”

Currently, the already seemingly profitable (cf. opex) mining is done at less than 37 EH/s (end of March) and the target of 50 is on the verge of summer.

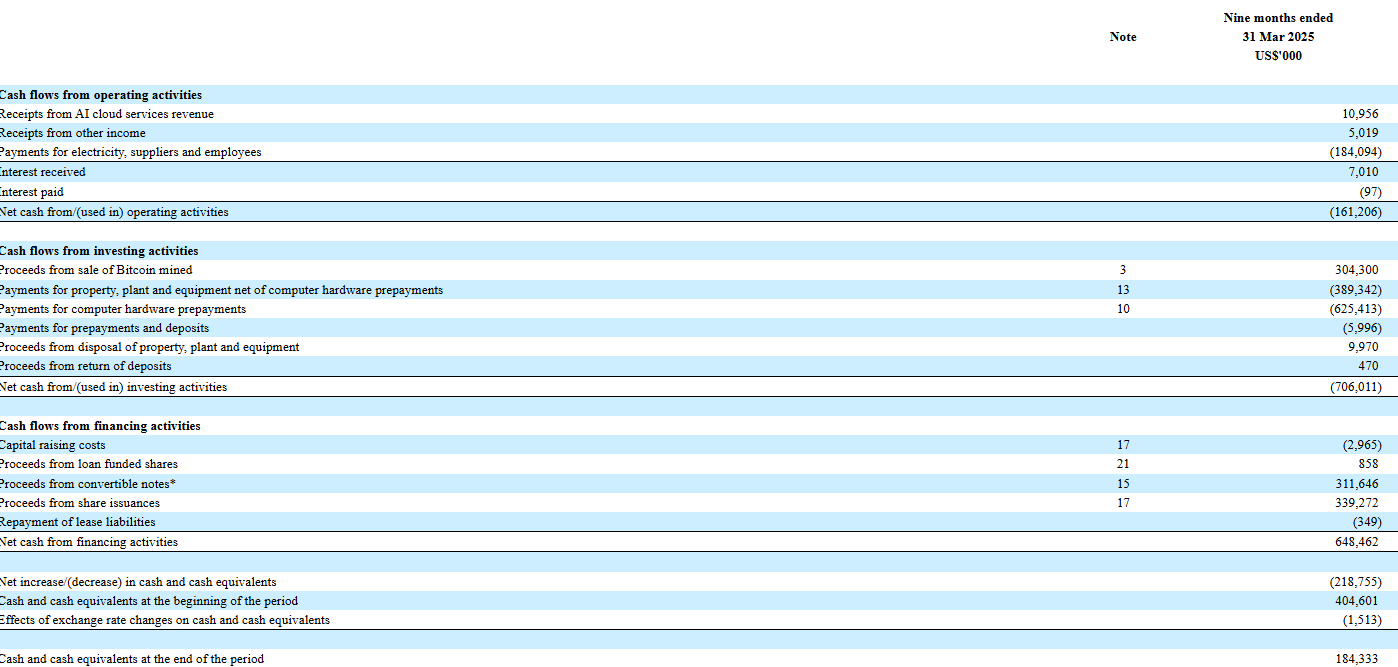

The need for investment in the future is what defines the investment case. It is very difficult for me to estimate; in the latest cash flow statement (note: 9 months), large investments still weigh heavily into the negative.

Most of it has gone into mining equipment

“Payments for computer hardware prepayments included payments of $583.6 million relating to mining hardware purchases and $41.8 million relating to NVIDIA H200 GPUs purchases. The $583.6 million mining hardware purchases and $41.8 million NVIDIA H200 GPUs purchases were paid in respect of the Hardware Purchases Agreements as outlined in “Hardware Purchases” included within this MD&A. Our $389.3 million payment for property, plant and equipment net of computer hardware prepayments primarily related to the purchase of equipment in connection with the continuing expansion of our data center capacity at Childress and payments relating to long lead high voltage equipment and civil & land preparation works at Sweetwater 1.”

If the mining world is ready by summer and AI orders are still negligible, one could guess the capex and 50 EH/s mining revenue accordingly and how many dollars the company generates from that. First, I need to get to know the management, perhaps through podcasts, and weigh whether they are grounded enough not to start investing excessively ‘because we’ll be asked for that AI capacity any minute now’

I read Culper’s report carefully. It contains many well-reasoned observations, and several risks should be taken seriously. At the same time, I believe that in many places we are looking at things from a different perspective, which also explains the different conclusions.

At the core of the report seems to be the view that Bitcoin has no long-term value or role – if this idea is held to be true, it is understandable why IREN’s business appears poorly justified. However, I personally still see Bitcoin as a relevant and potentially strengthening part of the digital infrastructure. On that basis, mining operations could still have years of profitable lifespan left.

It is true that IREN’s current mining infrastructure cannot be directly converted to suit AI computing. However, that is not the company’s claim either. AI investments relate to separate new development projects – for example, the West Texas greenfield project. In that project, AI is being built from scratch, and it is not about recycling existing mining equipment.

The AI business is still in its early stages, and commercial development has been slow, which is natural for such a new area. I personally do not expect quick results, but I consider it important that the company has an alternative growth direction in the long term, should the profitability of mining ever decline.

In summary: I appreciate Culper’s analysis and understand their concerns. At the same time, I interpret the situation differently, especially regarding the long-term potential of Bitcoin and IREN.

A few months ago, Trump appointed a working group to consider crypto regulation. They were given 6 months, after which the group will present its proposals on their regulation and possibly their inclusion in currency reserves. I consider it likely that the working group will come up with a proposal that favors cryptocurrencies.

June will mark roughly six months. Bitcoin could relatively easily reach the 125 - 150,000 level if it is made acceptable at the U.S. federal level, and some other countries might follow suit.

Iren naturally benefits from this.

Additionally, for example: Sofi benefits because it lost the opportunity for crypto operations to obtain a banking charter. It’s likely that the rules will be loosened, allowing it to get back in and gain more revenue/customers.

Yeah, I don’t think mining will be regulated too much very easily.

However, if I significantly increase my position, I might take a BTC short alongside it purely for risk management – kind of as a hedge, so that market risk doesn’t get out of hand.