Hopefully, this would bring equally valuable specialized expertise and a moat effect to IREN in its field, similar to what has been seen in the world of AI experts or in Japan concerning the finest ball bearings.

1 Like

Execution is the only moat, someone said. That probably includes investing in people and the community ![]()

1 Like

From small streams, etc. ![]()

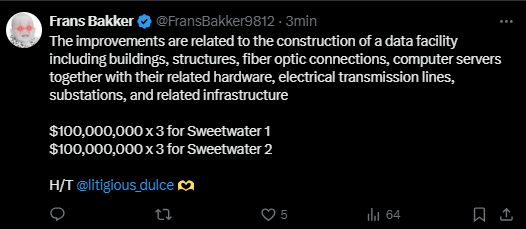

600k tax reliefs confirmed for Sweetwater 1&2 ![]()

https://x.com/FransBakker9812/status/1953810241508061191

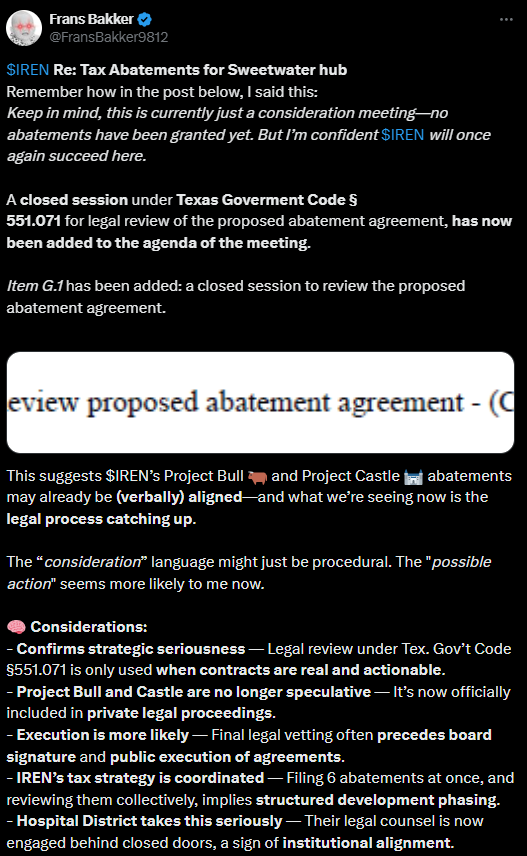

Background:

https://x.com/FransBakker9812/status/1939273761317871618

7 Likes

7 Likes

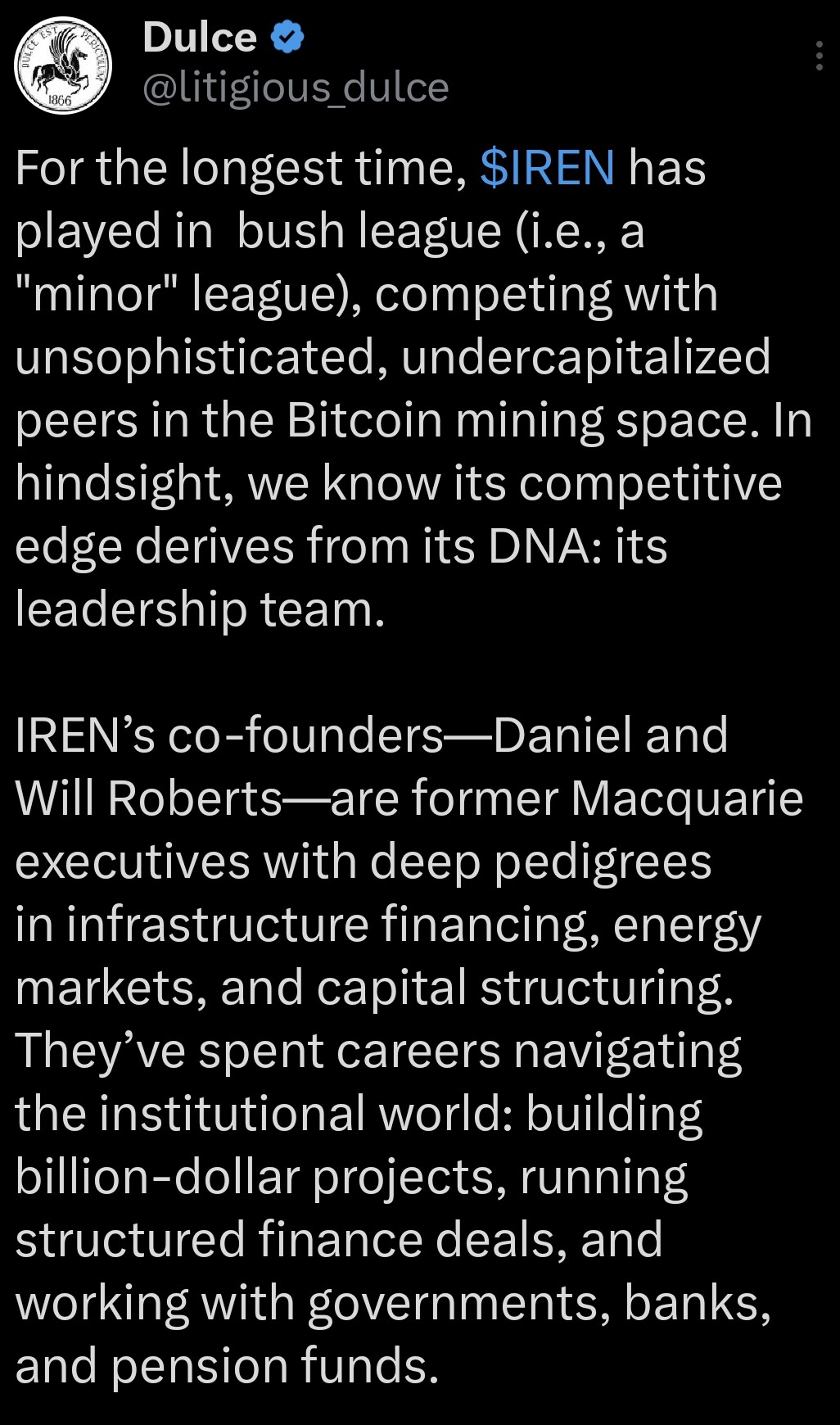

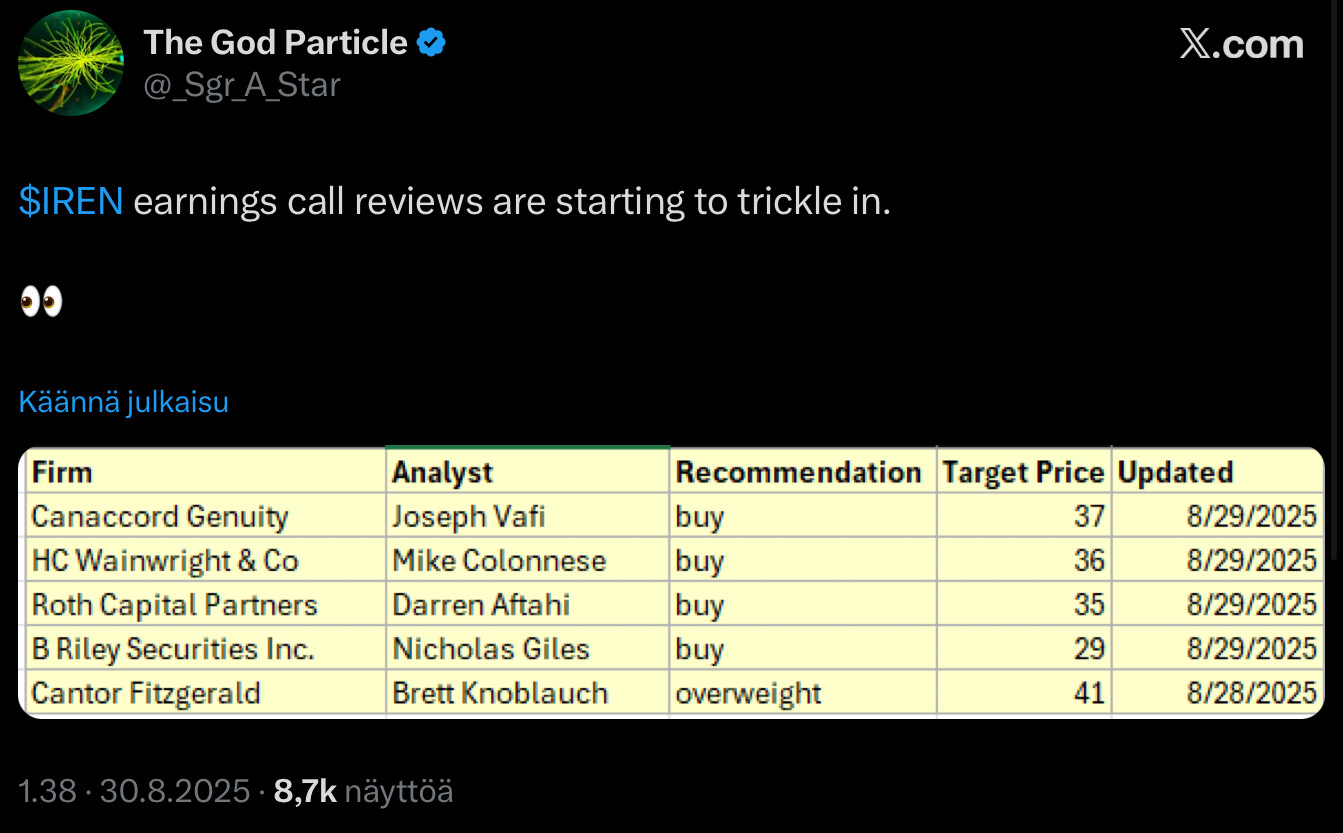

Exactly. More from IREN’s leadership:

Full tweet: https://x.com/litigious_dulce/status/1953848605795623411?t=TJ8QlO2T2ncokhxPcFn7cw&s=19

4 Likes

The AI and HPC director (manager, lead?) is apparently moving to San Francisco for work. I am moderately optimistic about what this could mean for the company.

14 Likes

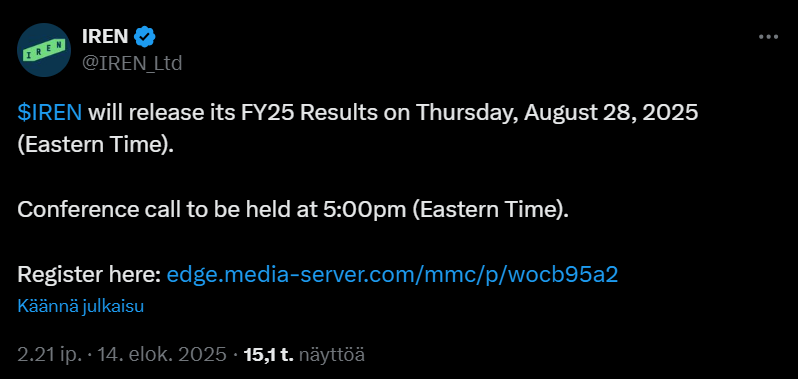

2 weeks to IREN’s annual report.

10 Likes

It’s picking up pretty well now. Any bets on whether we’ll hit that predicted 25 or go back to 16-17 next week?

![]()

I have outlined the company as massively undervalued; I assume it will be priced in the hundreds of dollars within 5 years.

Short-term price movements are mainly interesting for entertainment.

But if you’re interested in more precise price movement probabilities, then #1 is https://x.com/nanotitan28?s=21&t=Gf87bhKtIDEQ8PoQTL96bQ

Franc’s nickname is then chart uncle (chart uncle) ![]()

E:

10 Likes

![]()

![]()

![]() BREAKING

BREAKING ![]()

![]()

![]()

beaf464c-f8a4-4d22-9bfc-a2a339199569

EDIT:

On Thursday after NYSE closes, the fiscal year’s earnings report will be published, the Finnish translation of which is likely an unaudited financial statement. This will likely generate a lot of discussion, so the very next day Dan will again come to the familiar palkoloitsu (podcast) to chat. Plenty to enjoy before the weekend ![]()

https://x.com/McnallieM/status/195998661405950457

26 Likes

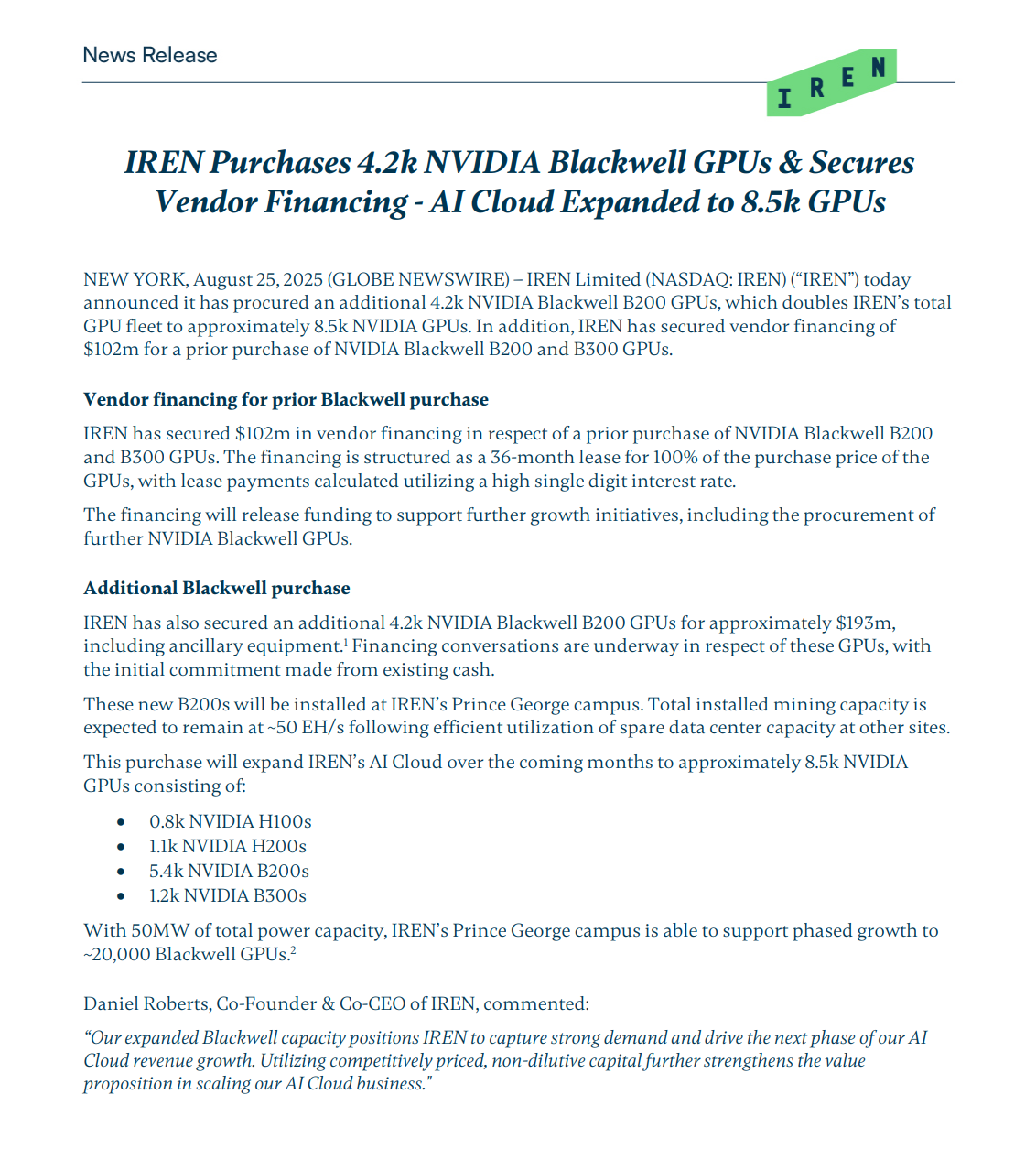

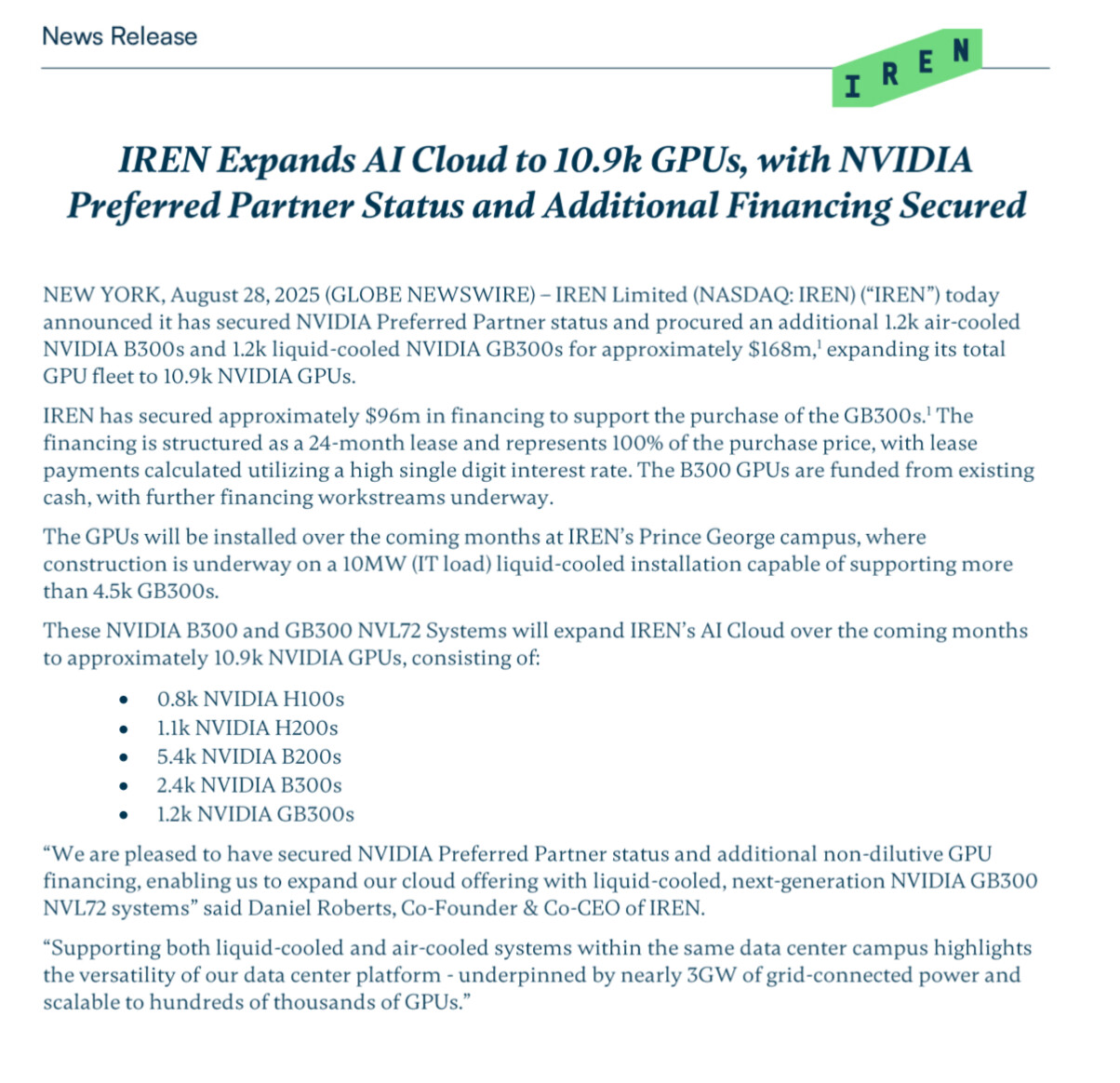

Earnings are out and apparently well-received by the market, maybe tomorrow I’ll have time to delve into it - the call isn’t until midnight.

I didn’t expect additional news, but there was some anyway

https://irisenergy.gcs-web.com/static-files/a152edfc-1748-4d9d-b12e-d85fdfbc86cd

One thing about the earnings I have to comment on:

The Queen vs kid analysts: knockout ![]()

EDIT

Earnings call transcript (some automatic translation, IREN usually heard as IRON etc)

19 Likes

What a result! Confidence in the management is growing, and the revaluation of the stock from a miner to data center infrastructure is likely to continue. However, one must exercise caution with this and understand that risks are always hidden, even if they are not always visible. Nevertheless, it must be said that the potential is still very strong when compared to industry peers, the quality of the company and its management, and future projects. A significant multiple sounds ambitious, but when the calculations are made time and again, it is not impossible at all, and even in a relatively short time. Financing and dilution risk also decreases if the price of Bitcoin remains high and cash flow starts coming from multiple pillars. Projects are being completed at a good pace, and the story is still in its early stages.

19 Likes

Does anyone have facts on how the current 810MW active power is distributed between BTC mining and AI Cloud? I couldn’t find this in the company’s presentations.

This is going back into the portfolio. Yes, at a much higher price than I sold it for, but that’s how it is. AI growth is, in my opinion, now sufficiently proven. Good result and management focuses on the right things.

3 Likes

Here’s a listening recommendation (45 min). Numbers, capacity, and the future roadmap.

My belief in the management’s ability to create shareholder value only strengthened further. The ability to be flexible and make decisions based on where the best ROI is assures me that management will continue to make decisions with short/medium/long-term perspectives in mind. This flexibility is one of their competitive advantages.

I was left with the impression that by the end of the year, we’ll hear about a deal for the current capacity, and more chips will be ordered soon.

When Wall Street finally understands that this is not a Bitcoin mining company (though it’s the best at that too), the valuation multiples will expand very quickly.

I will buy back the shares I sold before the earnings call, probably as early as next week.

18 Likes

It hasn’t been specifically announced, to my understanding. Below is a general article stating that most of Childress will go towards it. Something in Canada that might be moved away, the situation is evolving, I won’t speculate.

Here are new targets at the same time

5 Likes

I haven’t studied the company in great detail, but I started digging through the numbers to better understand why there’s such a buzz around this company. What caused the most wonder were the comparisons to Nebius and how IREN is apparently a better investment… I just don’t see it myself (at least not yet). Please correct me if I’m wrong.

Of course, almost 3GW of reserved power is a lot and provides opportunities for anything, as long as we can squeeze as many dollars out of it as possible. But if we try to calculate the ARR/MW figure based on current AI cloud numbers, doesn’t it remain quite modest, at least at the moment? Or if we calculate ARR/MW based on management’s previous Horizon1 comments

IREN is developing a cutting-edge 75MW liquid-cooled AI data center, named Horizon 1, at its Childress site in Texas.

IREN estimates that Horizon 1 could generate between $75 million and $100 million in average annualized revenues upon completion

$1M-1.3M ARR/MW? And since the company is so eagerly compared to Nebius, it’s worth mentioning that Nebius has guided for $900M-1.1B ARR for the end of the year and 220MW of power.

What am I not grasping here?

Edit: Let’s correct this further: Nebius’s guided 220MW is “connected power”. “Active Power” is estimated to be 100MW by the end of the year.

3 Likes

I haven’t looked into Nebius in detail, but I know that these can’t really be compared.

Nebius likely guides cloud service sales and Iren guides ‘bare metal’ sales. This was discussed in the earnings call. Sophisticated customers want to bring their own software stack to specific GPUs (not a cloud).

There is demand for this, so it is being sold as quickly as possible.

Nebius’s ARR might look good, but underneath, they are bleeding money. It doesn’t own much itself, unlike Iren, which currently owns everything from the ground up.

Here’s a comparison between data center providers by a smarter guy, including nbis and iren.

https://x.com/jiahanjimliu/status/1961315096162181444?s=46&t=Gf87bhKtIDEQ8PoQTL96bQ

Edit: So bare metal is the lowest margin operation in these own GPUs; cloud is also available for willing buyers ![]()

But it’s typical for Iren that some future ARR is calculated from the lowest point.

The kicker is this: Because Iren owns everything from the ground up, that lowest margin is very attractive thanks to the new CFO’s Dell (+others in the future) leasing deals.

Edit2: I’m currently watching the Mcnallie money - podcast where Dan talks a bit more plainly about fy2025. Due to my poor expertise, I may have confused something in that bare metal service; it might actually count as ‘cloud services’ in some way because Dan talks about cloud services all the time.

In itself, a very dangerous podcast because it makes me want to push all my chips into Iren.

Quote ‘We were asked about the utilization rate and we didn’t really understand. Apparently, other operators have GPU utilization rates below 100%. It was hard for us to grasp this. We noted that there is some extra for testing’ ![]()

Quote 2: Vertical integration brings other benefits besides direct financial ones. Other service providers leave a ticket with the colocation provider in case of problems. We walk into the machine room and fix it immediately. However, the most common situation is that we warn the customer in advance about a potential problem.

One more - when asked generally about others’ ‘pipelines’ (megawatts etc.) Dan replied ‘pipeline is word for a massive spreadsheet of “things we don’t have”’ ![]()

![]()

![]()

12 Likes

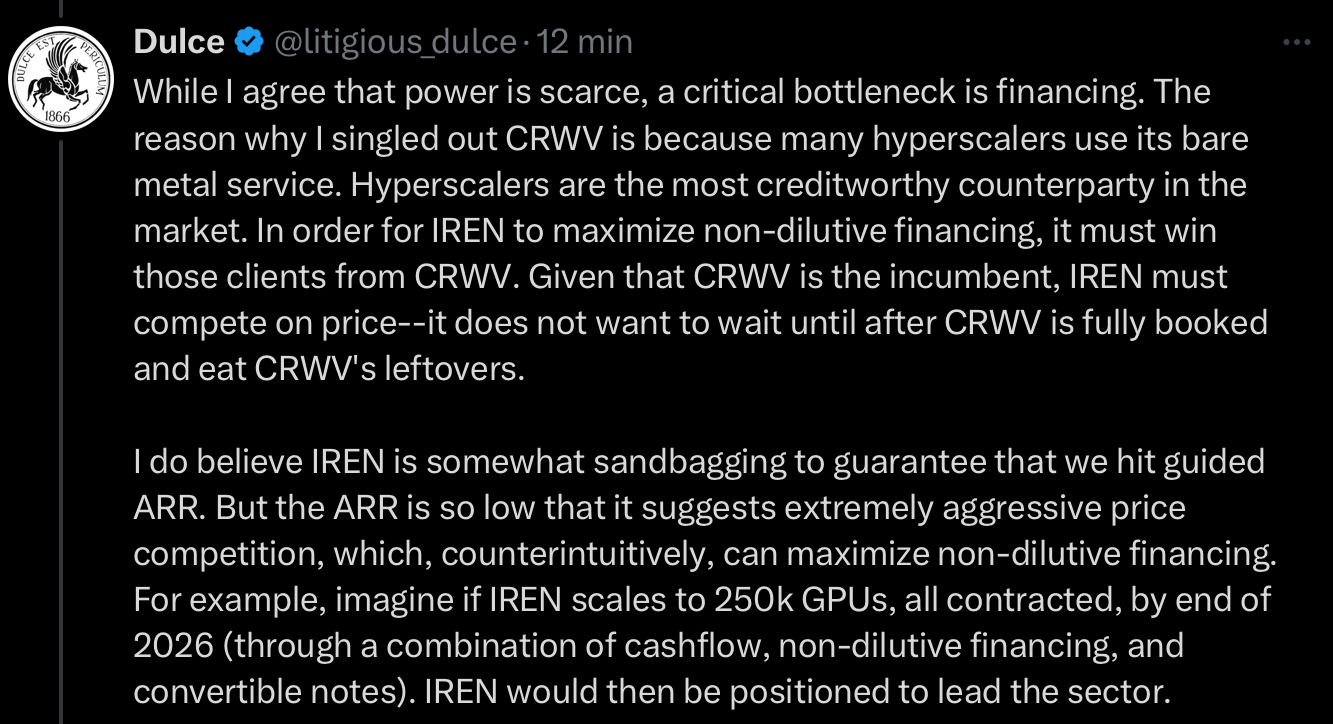

Apologies for the spam, I’m putting this in a separate message so it doesn’t get buried in my previous crammed one, but I just stumbled upon this comment from Dulce which explains the prices a bit.

4 Likes