I’ve been meaning to start a thread for Norwegian Huddly for a while now.

This is a recent IPO case from Norway, listed on the Norwegian Merkur Market in February of this year. Before this, the company was on the (N)OTC list.

ISIN: NO0010776990

In all its dullness, the company manufactures cameras. It’s worth getting to know the company by reading their latest company presentation, which can be found here: https://www.google.com/url?sa=t&rct=j&q=&esrc=s&source=web&cd=&cad=rja&uact=8&ved=2ahUKEwjekI-8yMbvAhXk-ioKHYakAdwQFjABegQIBBAD&url=https%3A%2F%2Fwww.huddly.com%2Fcontent%2Fuploads%2F2021%2F02%2F080221-Huddly-Investor-Presentation.pdf&usg=AOvVaw1xY2Fau52ENMxbkcD0EpDi

Q4 report here: https://www.huddly.com/content/uploads/2021/03/Huddly-Q4-2020-Report.pdf

Q4 presentation here: https://www.huddly.com/content/uploads/2021/03/Huddly-Q4-2020-Presentation.pdf

Information document available for download here: https://www.google.com/url?sa=t&rct=j&q=&esrc=s&source=web&cd=&ved=2ahUKEwjAn5HsyMbvAhXt-yoKHdQuDIAQFjAAegQIBBAD&url=https%3A%2F%2Fwww.huddly.com%2Fcontent%2Fuploads%2F2021%2F02%2FHuddly-AS-Information-Document.pdf&usg=AOvVaw2gyoHJ8J2aUOhLYc0wRn95

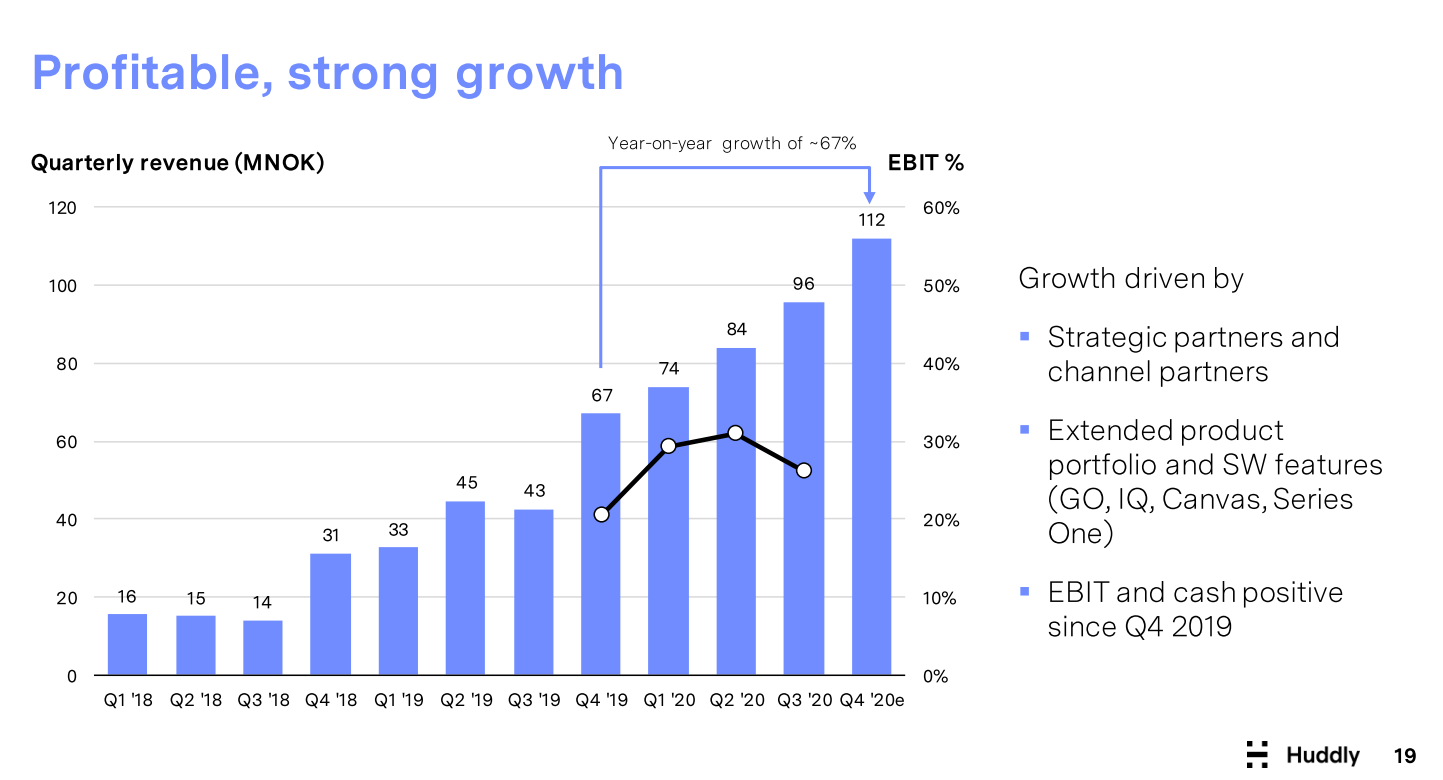

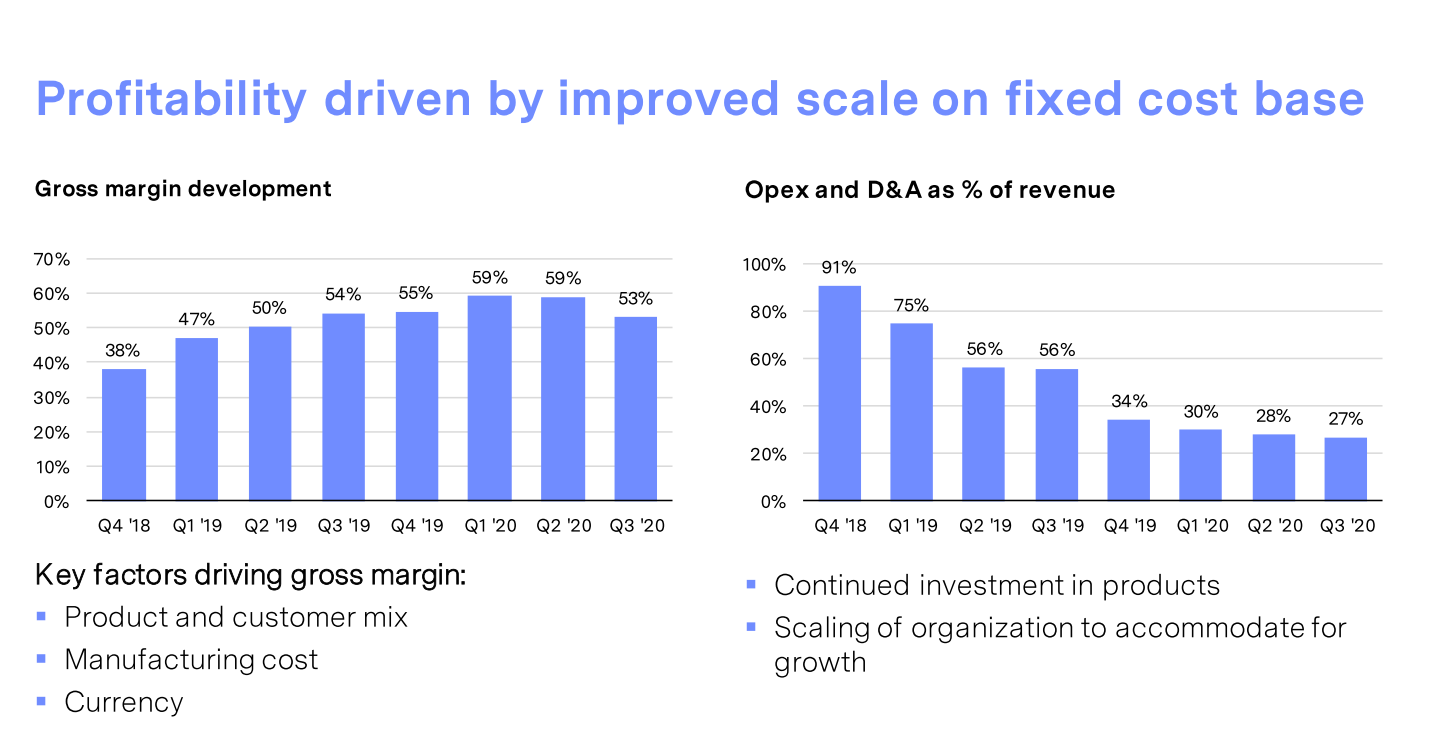

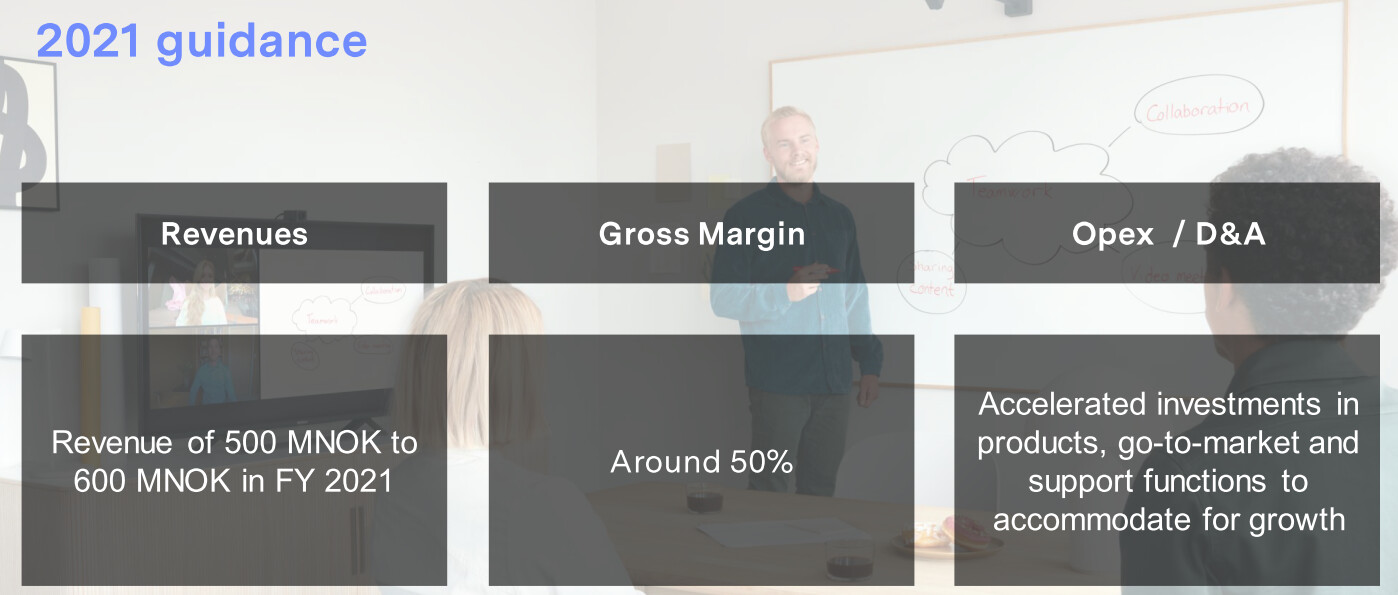

Nowadays, it seems to be the custom not to bother opening links, so here are a few screenshots.

2021 guidance

Today, a partnership with Mersive Technologies was announced: NewsWeb

Previous news

I own shares in the company. This is not an investment recommendation, etc.

Edit: @III21 It’s here ![]()