These positive signals keep coming from all over. This was more of an elaboration on previous news, but Harvia definitely has good prospects to continue strong growth for a long time to come.

31 Likes

The US market is only just opening up, and there is great potential there. This is going to make another surge similar to the one during the COVID era, but this time the rise will likely be on a more sustainable foundation. By the summer at the latest, we’ll see strong growth figures, just like we did last year. I wouldn’t be surprised if Harvia has to expand the Muurame factory once again.

13 Likes

Here are Rauli’s preview comments as Harvia reports its Q1 results this Thursday, the day after tomorrow. ![]()

Harvia will publish its Q1 report on Thursday, May 7th at 9:00 AM, and you can follow it on the earnings livestream starting at 8:55 AM. The company’s webcast can be followed from 11:00 AM onwards here. We expect revenue growth to be moderate and earnings to decline slightly due to an exceptionally strong comparison period. Overall, however, we expect the company’s development to remain stable and in line with long-term targets.

18 Likes

Ladies and gentlemen, don’t forget the earnings livestream hosted by Rauli starting at 8:55 AM ![]()

35 Likes

Harvia Q1 2026: Record revenue and strong profitability

This release is a summary of Harvia Plc’s interim report for January–March 2026. The full report is attached to this release as a pdf file and is also available on Harvia’s website at https://harviagroup.com/.

Highlights of the review period

January–March 2026:

-

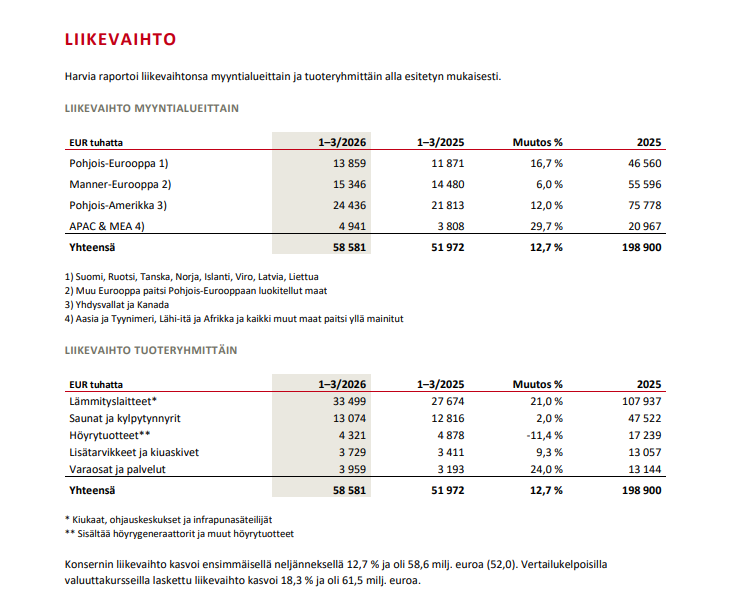

Revenue increased by 12.7% to a record high of EUR 58.6 million (52.0). Revenue at comparable exchange rates increased by 18.3% to EUR 61.5 million. Revenue growth was entirely organic.

-

Operating profit was EUR 12.8 million (11.9) or 21.9% (22.9%) of revenue.

-

Adjusted operating profit was EUR 12.9 million (11.9) or 22.0% (22.9%) of revenue. Adjusted operating profit at comparable exchange rates was EUR 13.8 million (22.4% of revenue).

-

Operating free cash flow was EUR 12.0 million (10.2) and cash conversion was 80.5% (73.7%).

-

Net debt was EUR 49.4 million (51.1). Leverage, calculated as the ratio of net debt to the adjusted EBITDA of the last 12 months, was 1.0 (1.1).

-

Equity ratio was 49.9% (47.7%).

-

Earnings per share was EUR 0.50 (0.45).

95 Likes

Harvia’s performance was brisk once again, with organic growth at 18%. Regarding the outlook, the following is worth noting, meaning a small temporary hiccup for Q2.

| Forecast Table | Q1’25 | Q1’26 | Q1’26e | Q1’26e | Difference (%) | 2026e | |

|---|---|---|---|---|---|---|---|

| MEUR / EUR | Comparison | Actual | Inderes | Consensus | Act. vs. Inderes | Inderes | |

| Revenue | 52.0 | 58.6 | 54.6 | 54.8 | 7 % | 222 | |

| EBITDA | 13.8 | 14.8 | 13.2 | - | 12 % | 54.2 | |

| EBIT (adj.) | 11.9 | 12.9 | 11.4 | 11.7 | 13 % | 46.7 | |

| EBIT | 11.9 | 12.8 | 11.3 | 11.6 | 13 % | 46.4 | |

| EPS (reported) | 0.45 | 0.50 | 0.43 | 0.44 | 16 % | 1.68 | |

| Revenue growth % | 22.6 % | 12.7 % | 5.0 % | 5.4 % | 7.7 %-pts. | 11.8 % | |

| EBIT margin % (adj.) | 22.9 % | 22.0 % | 20.9 % | 21.4 % | 1.1 %-pts. | 21.0 % | |

| Source: Inderes & Modular Finance, 7 analysts (consensus) |

76 Likes

Yeah, great momentum. Just have to remember that you need 1.18 dollars from the States for one euro.

I don’t see the pre-announced Q2 hiccup as an issue at all, because it’s just going to lead to a Q3 burp!

One could snap up some Harvia here, even though spot electricity is currently 19.55c/kWh ![]()

42 Likes

The retail level has likely been informed about the IT and process reforms, so a portion of the revenue recognized now may also be so-called pulled-forward demand.

28 Likes

The webcast is about to begin, here is the link:

9 Likes

The sauna folk of the North are starting to wake up from their hibernation and the US continues to roll forward excellently; this is a joy to own.

It would be interesting to hear how the revenue is distributed between the APAC & MEA countries—which Asian countries are seen as having the greatest potential? If, for example, the middle class in China, Japan, and Korea can be inspired by the sauna culture, it wouldn’t take many years for Northern Europe to be overtaken in sales.

38 Likes

An interview with the well-spoken CEO, Järnefelt.

Harvia Q1’26: The year began with record-breaking heat

Harvia’s revenue rose to a record level driven by strong organic growth, and the gross margin remained high. Particularly positive was the broad-based nature of the growth across all geographical regions, as well as North America’s strong performance on top of a very tough comparison period. Harvia CEO Matias Järnefelt interviewed by analyst Rauli Juva.

40 Likes

Did any additional info come out regarding this, for example from the webcast? Is there any estimate on how much of the quarter’s growth might be explained by pulled-forward demand that has been “borrowed” from the next quarter?

The company commented in the report:

“Operating profit included EUR -0.1 million (0.0) in items affecting comparability, mainly related to acquisitions and restructuring.”

Can @Rauli_Juva say if these expenses could still be related to the Thermasol acquisition?

7 Likes

Matias went through the impacts of the IT reforms in the webcast. I will directly quote a couple of points from the webcast transcript here.

Matias: "Now, this is quite a significant piece of work for us, and it will have an impact on our deliveries during Quarter Two. It will include such things as actually ramping down production for a temporary period of time in Muurame, transforming the systems from the old to new, and then ramping the production up. And because of this, we estimate that there will be roughly €3 to €5 million worth of shipments shifting from Q2 to Q3. And this will, of course, move also the related gross margin from quarter two to quarter three. And as we will be working long hours, there will not be savings in, for example, employee costs, as direct labor will still be present and involved in these transitions and ramp-ups.

So we also expect that there’s going to be some impact on the OpEx level as well during the quarter.

Now. However, this is very well planned. The customers have been informed in advance. We have confidence that we will not be losing any sales. So while this would have a negative impact on our quarter two, it should have a clear positive impact on our quarter three.

And in addition to having the sales back in the quarter three, we believe that this transition to the more modern, efficient, and scalable system will start to pay back rather soon."

Second Q&A question: "Was there anything in Q1 revenue that would not occur again later in the year? Or was everything just driven by robust normal demand? "

Matias Järnefelt: "There’s nothing particular to mention.

I think one question might be that since we informed the customers about the longer lead times during Q2, whether that has turned into what I would call advanced buying.

But as we’ve been analyzing that, our assessment is that that didn’t have any significant impact on our Q1 results. The impact will be seen in quarter two and quarter three, and hopefully we will be able to catch up fully by the end of quarter three. Of course, that remains to be seen, but we feel fairly confident about that."

So, in short: They have analyzed the situation and concluded that there was no significant impact on Q1. The effects of the IT reform will be seen in Q2 and Q3. An estimated €3–5 million worth of deliveries will shift from Q2 to Q3. This will also be reflected in the Q2 results, as production must be temporarily ramped down, while the cost side remains fixed.

51 Likes

I can’t say for sure; there might be some residual tails from the Thermasol integration, but other things are perhaps more likely. It’s no secret that Harvia is constantly scouting for new acquisitions. In connection with the Q4 results, the commentary sounded to me like something might happen soon, so a process could well have been underway. It didn’t come up in the same way during Q1, although Matias did say in our interview (again) that they should find an acquisition target in the infrared segment.

I added this potential “front-loaded demand” to my list of questions yesterday when I noticed @Black_Swan’s comment, but it was forgotten during the interview. But that is indeed what they said. It’s perhaps worth noting that Harvia cannot know with absolute certainty what thoughts all customers have behind their orders, though they likely have some idea regarding larger ones, e.g., customer inventory levels. Ultimately, we will see later in the year how sales have performed overall during the year.

Let’s hope the company handles this IT system renewal efficiently; there are examples of these where operations get quite badly tied up in knots for a long time.

44 Likes

Target price increases:

OP: €38 → €43 (“strong growth will continue in the coming years”), recommendation ACCUMULATE.

Danske: €47 → €49

Nordea: €49 → €52

56 Likes

Yeah, after Friday’s share price drop, the gap to the target prices just keeps growing…

Rauli remains on a cautious stance…

14 Likes

Almanakka has written about Harvia once again ![]()

Valuation: Harvia is valued at ~16x the next 12-month forward EBIT. In my opinion, this is closer to a buying level than a trimming level. If Harvia weren’t already the largest holding in my portfolio, I would certainly be adding at prices below forty euros. The stock isn’t dirt cheap even now, but for a high-quality company that I believe will grow structurally for a long time to come, this is not a bad price.

Some value must also be given to Järnefelt, who has at least convinced me. However, it should be noted that things also looked good at Harvia’s helm under Tapio Pajuharju, who suffered a complete crash at Kamux. A good enough company can be led even by a ham sandwich, but on the other hand, when leading a poor enough company, even a good management’s polished image starts to tarnish easily. This is loosely quoting W. E. Buffett.

43 Likes

Pia and Rauli discussed Harvia in English ![]()

Harvia’s Q1 earnings exceeded our estimates, but the estimate changes for the full year remained small. Q2 earnings will be weighed down by the shift of revenue to Q3. We expect Harvia to continue its strong earnings growth and value creation in the coming years. Analyst Rauli Juva summarizes.

Topics:

00:00 Intro 00:14 Estimates exceeded in Q1 01:25 APAC & MEA 02:29 Muurame plant 04:03 Holistic sauna experiences 05:45 Potential M&As 07:54 Valuation & recommendation

12 Likes

Small news for the present moment, but bigger news when considering long-term prospects.

“The higher education institutions of Jyväskylä; the University of Jyväskylä and Jyväskylä University of Applied Sciences (Jamk), together with the Jyväskylä Educational Consortium Gradia, are launching a partnership cooperation with Harvia, where education, research, and development are combined with the needs of an international growth company and future innovations.”

The project is currently in its early stages, but it is great that the company is networking and innovating together with the university and the university of applied sciences; these will bring long-term expertise to the company.

36 Likes