Someone has decided to divest their holdings after the results. 0.5% of Harvia’s total share capital has changed hands.

Of course, the flip side of the coin is that someone has also been on the buying side.

Someone has decided to divest their holdings after the results. 0.5% of Harvia’s total share capital has changed hands.

Of course, the flip side of the coin is that someone has also been on the buying side.

Hasn’t North American revenue growth clearly slowed down now? Last year, YoY growth was well over 10% every quarter, and in the final quarter of this year, growth was only a couple of percent compared to a year ago (although the result for the full year was still good). For comparison, Q4/24 vs Q4/23 growth was over 60 percent.

Additionally, Q3/25→Q4/25 growth was probably (in percentage terms) half of what it was for Q3/24→Q4/24, even though major campaigns were running during Black Friday and other shopping days.

It’s still pushing forward well, and I personally wasn’t planning to do anything with my holding, but it’s not particularly surprising that the share price would drop.

Here is a fresh CEO interview! In my opinion, Järnefelt answered Rauli’s pertinent questions quite well regarding growth, profitability, and, for example, the lackluster quarter in the North America and APAC & MEA regions. If you look past the quarterly figures and consider the full-year development and the big picture, I wouldn’t be worried about the company’s direction. ![]()

And it was as if the answer to the last question suggested that news might also be expected from the M&A front in the near future. It’s been a while since the last deal, after all. ![]()

Despite exchange rate changes, tariffs, and a tough comparison period, Harvia achieved slight growth at the end of the year. Although profitability improved both year-over-year and from the previous quarter, it still remained slightly below the target level. Harvia CEO Matias Järnefelt comments in an interview with analyst Rauli Juva.

Topics:

00:00 Introduction

00:10 Main events of Q4 and the full year

03:54 Demand in Northern Europe awakening

05:24 Growth in APAC & MEA regions fell short

07:28 Slight growth in North America

09:29 Decline in steam products

11:49 Profitability slightly below target level

13:15 Outlook for 2026

15:10 M&A market

Thanks for the great interview @Rauli_Juva! I can’t really feel too worried about Harvia’s future, when the full-year targets were missed practically only due to the weakening dollar and tariffs ![]()

Yeah, I agree, Harvia’s strong earnings performance continues and with the stock, you have to see the forest for the trees.

There’s no point in going through the interim report with a magnifying glass just for the sake of nitpicking.

A great 2025 ahead and let’s keep the momentum going.

Thanks! Matias performs really well regardless of the questions, but today’s session felt particularly smooth ![]()

The acquisition card was hinted at quite clearly both in the webcast and in that last question, as Tomi mentioned above. Of course, it has been clearly communicated before that they do want to make deals when suitable targets are found.

Rauli upgraded his recommendation by two notches at once, now to BUY with a target price of 44 euros (previously REDUCE at 43 euros).

You hardly see the “Inderes effect” in mid-caps anymore, but I’m quite satisfied that I already added to my position on Thursday. If the share price stays stagnant for a moment longer, even the Model Portfolio might get a chance to add this quality company to its portfolio.

Personally, I like Harvia’s way of not publishing any short-term guidance. For a company like this, the broad strokes are perfectly sufficient. Of course, I understand that analysts would like an outlook with a precision of a few months. Funny enough, someone in the webcast suggested that Harvia should only report results every six months. I won’t admit to being that proposer.

There might indeed be an acquisition in the works. Matias has mentioned several times that he hasn’t bought Harvia shares himself because he is constantly involved in insider projects. Not in those exact words, but everyone gets the point. Let’s just hope it’s a successful purchase. Kirami wasn’t, but in my understanding, the others have been.

At this stage, I have to take my hat off to Matias’s excellent, down-to-earth, and clear communication towards us investors in these earnings releases and interviews.

I’ve been on the journey with Harvia for 5+ years, and all sorts of things have happened along the way. Currently, however, I feel very confident about the company’s future. There’s no overreacting from one quarter to the next; the train just keeps chugging along with a clear strategy & focus. Sometimes exchange rates provide headwinds and sometimes tailwinds. The stock price then lives a life of its own.

In my opinion, easily one of the most trust-inspiring CEOs on the Helsinki exchange ![]()

Personally, I always think some kind of guidance is better than no guidance at all. In Harvia’s case, the company could well provide guidance on an annual level, for example, stating they believe they will reach their financial targets this year (10% growth and 20% EBIT). It might not affect the stock volatility caused by quarterly results, but it would provide some direction on an annual level as well. Of course, this can also be handled through verbal communication, which Matias indeed handles excellently. Apparently, Matias would have known how to provide guidance for this year too, as he said at the beginning of the year the goal was 200 MEUR and 20%. If he had added “approximately” to those, the guidance would have held for the whole year ![]()

Agreed, and just to add, yesterday’s interview was exceptionally convincing in that even all the old figures came from memory without hesitation. It almost brings Rain Man to mind, in a good way. ![]()

PS. Been along for the Harvia journey for almost 8 years now. ![]()

Almanakka has written about Harvia following the Q4 results ![]()

I and other Google Trends watchers let our expectations get a bit too high ahead of the fourth quarter. It definitely didn’t go poorly, but a valuation like this cannot withstand even minor disappointments. Somewhat surprisingly, the most positive surprise of the quarter was found in the domestic markets as Northern Europe returned to strong growth, while at the same time North America appeared more subdued, at least on the surface. After a 10% correction, the company is still at 18x the trailing 12-month operating profit.

We bought Harvia shares for the Model Portfolio with a 6% weight. In our view, Harvia possesses strong competitive advantages and growth prospects, and is capable of a strong return on capital. We believe the growth supports an annual return expectation of over 15% for the coming years. After the trade, the Model Portfolio’s cash weight fell to a fairly low 8.5%, and thus opportunities for new acquisitions are now limited.

The previous Harvia shares from the model portfolio were sold almost exactly 2 years ago (13.2.2024) when the share was hovering around €31-32.

It is better for the model portfolio to admit a mistake regarding the previous sale and return now that the share price has fallen without any solid justification. Harvia fits the model portfolio perfectly as a long-term investment.

Bottas is promoting Harvia:

https://x.com/valtteribottas/status/2028759435343278500?s=46&t=UOAR__YJT3hJUdqJ5kUU4A

Spotted on the BBC:

The article discusses saunas in general and their development in Southern England. I thought it was a light and feel-good piece that I’d recommend reading, even if it doesn’t necessarily break any ground in terms of informational content.

Highlights that might interest forum members the most:

Purchase of 400 shares

Always coming up with something new, Finland mentioned.

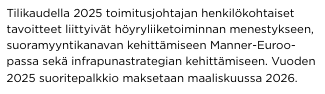

I was browsing Harvia’s annual report released today, and it caught my eye that they kindly disclose the CEO’s annual bonus “personal targets” retrospectively, which account for 30% of the bonus, with EBIT determining 70%. Below are Matias’s focus areas from last year. Of these, Matias received only about half of the maximum reward, so not everything progressed quite according to plan.

The highlighting of the infrared strategy strongly suggests that Harvia is heading more heavily in that direction one way or another in the coming years, which is a good thing for international growth. This isn’t surprising, of course, but if a strategy was developed last year, then perhaps we’ll start to hear something concrete this year. Naturally, if the strategy requires an acquisition, its realization isn’t entirely in their hands. I’ll have to ask about these in future interviews.

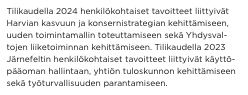

For comparison, the 2023-24 targets; compared to these, I think the 2025 targets were more specifically defined areas.

I was just reading an analyst’s Q4 analysis, as I also jumped on the Harvia bandwagon with a small sum. At the end, it was also mentioned that Harvia is considered a possible acquisition target. Has there been any indication of this before, or where did such an idea come from, and who could be potential buyers?

My understanding is that this speculation has been part of analyses for quite some time, with 5/2025 mentioned, for example. I haven’t seen any concrete evidence or further details on this topic. Perhaps those wiser than me can correct my view if needed?