Hopefully, people in the US don’t generally sauna in that style, because the sauna experience might be a bit lacking. So, Bryan saunas in the video with clothes on and an ice pack in his pants and on his scalp. Every day for 20 minutes at a time in a dry 93C sauna immediately after training. No löyly is allowed because the water might contain “toxins”. Then Finnish studies on the benefits of sauna are referenced… how many of these were done without throwing water on the stones? He only drinks water/electrolyte drink before and after the sauna… couldn’t he drink during the 20 minutes in the sauna too? And then, unfortunately, it’s a Huumi sauna.

A little continuation to this speculation. Now the CEO also mentioned that Thermasol has launched a new premium sauna collection. When one sifts through the main concerns of these pool owners, the length of the season (which naturally varies geographically) and the energy required to heat the pool emerge. Many different setups are already available for heating: solar energy, heat pumps, covering…

For this, Thermasol’s solar-powered sauna is a perfect fit. The sauna itself could extend the pool season because a sauna enables a pleasant swimming experience even in slightly colder water. On the other hand, a sauna would require an outdoor shower for hygiene reasons.

So, Thermasol’s pages would benefit from complete model concepts for these pool solution complements. One could be, for example, a sauna and an outdoor shower (and a small shaded lounge area), covered by a unified roof with solar panels on top. The system would include not only a heater and a radiator, but also a water tank for the shower under the benches. If and when there is surplus energy, it would be used to heat the pool. With this model, the implementation of the sauna would thus provide energy rather than consume it.

The potential of this unified, neat panel roof came to mind when I saw what kind of setups were otherwise available for collecting solar energy.

Of course, Americans will create their own culture, but at least various model solutions for the pool environment would be welcome. These are just idle Saturday musings..

In this respect, these off-grid solar energy solutions would seem very potent and even strategic in many markets. Because we have already seen how fluctuating electricity prices affect the demand for saunas and sauna bathing in general. And in these times of AI boom, prices can jump quickly.

I have to be satisfied once again with Harvia’s performance. The company is in good shape all around, profitability is excellent for this industry, and profitability has remained good despite investments in longer-term growth.

It’s quite a remarkable achievement that good results have been achieved decade after decade without any truly bad times – Harvia has things in order. This company doesn’t need any transformation or upheaval, as long as they continue on the proven path.

Harvia continues to emphasize the health benefits of sauna in North America with a new collaboration. Nothing new or revolutionary is likely to be announced.

Harvia, the global market leader in the sauna and spa industry, announces a brand ambassador and content collaboration with Dr. Emilia Vuorisalmi. Vuorisalmi is a Finnish medical doctor, best-selling author, and wellness expert known for her approach to integrating science into everyday wellness practices. The collaboration begins in North America and covers Harvia’s three regional brands – Harvia, Almost Heaven Saunas, and ThermaSol.

Together, Harvia and Vuorisalmi will produce science-based content and inspiring sauna experiences that highlight the researched health benefits of sauna bathing and honor the Finnish philosophy of sauna wellness.

I noticed a video on Cboys’ Youtube channel showcasing the group’s facilities, and in the backyard, a barrel sauna that has seen some life, with a Harvia stove, can be seen.

The sauna is introduced with the words: “Actually a kind of piece of shit.”

Not exactly Christian Ronaldo marketing material, but a video published 4 days ago has garnered 2.2 million views, so quite a few pairs of eyes will see it over time.

I chatted with ChatGPT about Harvia’s future investments, and according to it, the Almost Heaven factory would be expanded. Has there been any announcement about this, or is it still coming? Below is a direct copy of ChatGPT’s text.

Findings (summary)

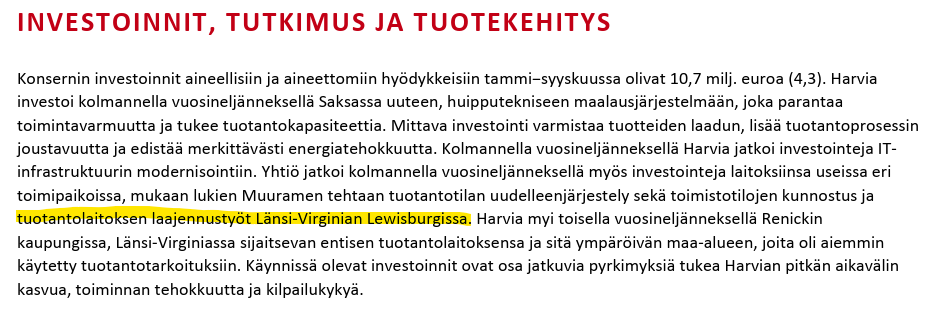

A public notice from the West Virginia DEP (May 15, 2025) states that Harvia USA Inc. has applied for a Class-5 UIC permit for stormwater discharge into an “improved sinkhole” system during and after construction (parking area + building addition) — this directly refers to a factory expansion in Lewisburg (Almost Heaven Saunas, 3567 N Jefferson St).

Lewisburg City / Planning & Zoning materials include a site plan review for Harvia US Inc. — The Planning Commission meeting document dated 12/12/2024 mentions Harvia/Harvia US Inc. and a plan describing a building expansion at the current parking area, as well as a new parking area. This indicates that local planning stages have progressed.

Well, there hasn’t been a separate announcement about it, and probably won’t be, but it has been mentioned several times in connection with the results. Last year, land was purchased and this year construction is already underway. It is also mentioned in the Q3 report.

Stock Exchange Release 17 November 2025 at 7:00 p.m.

Following the announcement by Chairman of the Board Heiner Olbrich that he will step down from his position as Chairman, the Board of Directors of Harvia Oyj has, in its meeting on 17 November 2025, elected from among its members Vice Chairman of the Board Catharina Stackelberg-Hammarén as the new Chairman of the Board. Stackelberg-Hammarén succeeds Olbrich in the position. Olbrich has served as a member of Harvia’s Board of Directors since 2022 and as Chairman since 2024. The aim of the change is to ensure the seamless continuity of the Board’s work following Olbrich’s announcement that he will step down from his position as Chairman, and that he will not be available for re-election to the Board at the Annual General Meeting in April 2026 due to personal reasons. Olbrich will continue as a Board member until the end of the current term. Markus Lengauer was elected Vice Chairman.

Catharina Stackelberg-Hammarén has served as a member of Harvia’s Board of Directors since 2023, and as Vice Chairman and a member of the Board’s Human Resources and Remuneration Committee since 2024.

With the change in the Chairman of the Board, the Board also decided on changes to the composition of the Board committees. As of 17 November 2025, they are as follows:

Human Resources and Remuneration Committee: Chairman Catharina Stackelberg-Hammarén, members Anders Holmén and Olli Liitola.

Audit Committee: Chairman Petri Castrén, members Hille Korhonen and Markus Lengauer.

As Chairman of Harvia’s Board of Directors, Catharina Stackelberg-Hammarén will, starting from her election as Chairman, serve as an expert in Harvia Oyj’s Shareholders’ Nomination Board in place of Heiner Olbrich, without being a member of the committee. The Nomination Board will submit its proposal for Board members to the company’s Board of Directors for the Annual General Meeting no later than 31 January 2026.

At one point, I didn’t invest in tires because Hille Korhonen was the CEO. And when I heard information from someone who worked there, I apparently made the right decision.

The role of board work is, of course, different. Is there any information and/or insight here regarding Hille’s competence and added value for board work at Harvia?

Hille Korhonen’s track record in operational activities isn’t very flattering. Of course, on the board, she is just one among others, and naturally, these days, when there needs to be an equal distribution of members, that can give a boost to some.

It’s a pity that Mr. Olbrich had to step down from the position after a rather short (1.5-year) chairmanship. But Harvia will surely do well under someone else’s leadership too. The change seems to stem from Olbrich’s own reasons, so it’s unlikely to have much of an impact on the company.

Hille certainly has a long career in leading consumer product companies, which should be a perfectly suitable background for Harvia. The stint leading Renkaat was not very successful, but otherwise, I cannot evaluate him.

I follow Almost Heaven’s online store from time to time; it seems that delivery times have stretched during the autumn from about 3 weeks in the summer to the current two months. Based on that, one could assume sales have been good if there haven’t been any major bottlenecks in production. Through Costco, one can certainly get it a bit faster, usually always 3-4 weeks delivery. In my opinion, there’s also more value for the customer in those Almost Heaven packages priced by Costco. Of course, for Harvia, it’s certainly a clearly lower-margin business than sales obtained through their own online store.

Are there still people on the forum following these numbers more closely or following European resellers? I’d be interested to hear views on the current situation. My own monitoring is mainly occasional glances without any precise tabulation. My long-term trust in Harvia is strong, and the intention is to stay invested for at least 5-10 years, if nothing unexpected happens.

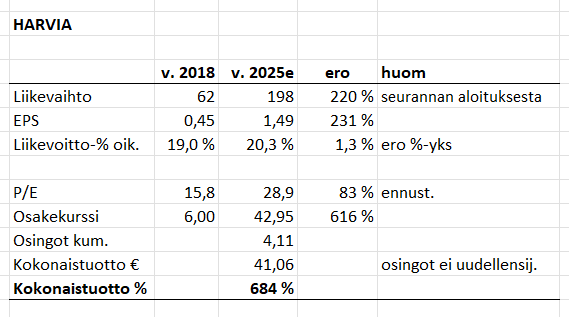

I made a small analysis of Harvia’s total return from summer 2018 - present, based on Inderes’ reports. Now I delved a bit deeper into the sources of shareholder return, hopefully it went at least roughly correctly, as I’m not very good at valuation. @Rauli_Juva if you wouldn’t mind taking a look at my thoughts, I’d love to hear your comments!

Harvia’s business has developed strongly:

Revenue +220%

EPS +231%

Adj. operating profit % 19.0% → 20.3%

So, the business has performed excellently. Now let’s look at valuations and returns:

Share price has risen +616% (since the start of coverage, i.e., €6.00)

Dividends have totaled €4.11 over the entire period

Total return is +684% if dividends were not reinvested

Now to an interesting figure, namely valuation:

P/E has risen 15.8 → 28.9, i.e., +83%

In reports back then, an “acceptable P/E” ratio for Harvia was floated around the 14 level. Now the question is, what would be today’s “acceptable P/E” ratio?

Harvia has expanded quite a bit, so its risk profile has, in principle, decreased. Additionally, growth targets have been raised, and profitability is (slightly) better. So, by all accounts, one could assume the valuation level has also increased. But by how much?

Well, this was a brief outline but roughly illustrates how the company has grown and where the returns have come from.

A larger portion of the return has come from earnings growth (which is a good sign), but the increase in valuation has also brought significant gains. And dividends have been substantial (considering that the subscription price was €5.00 and dividends have already totaled €4.11).

It did. From what I glanced at those numbers myself, they look to be in the right direction. However, for the 2018 P/E, you have picked the P/E according to the reported EPS, when otherwise you use (quite reasonably) adjusted ones. The adjusted P/E in the initiation of coverage report for the current year seemed to be 13.4. (This can also be calculated from that table: 6/0.45). In this case, the impact of the multiple expansion is somewhat greater, i.e., about 115%.

A very good exercise, and that has been the main question for me too for the past couple of years: what would be an acceptable valuation level, as the company is excellent.

A slightly lighter perspective: how do you think the change in the dollar exchange rate will affect market expectations for the upcoming earnings release? The change in the dollar’s value affects Harvia’s results quite significantly, as North America is the largest reported market area.

It would be interesting to hear your views on the subject! And of course, an analyst’s opinion on the matter would also be of interest, if you have time to share a few words about it @Rauli_Juva .