Below is a link to the webcast starting at 11 AM:

5 Likes

Agreed. Sales growth is excellent, but the drop in margins is a bit concerning. Exchange rates explain part of it, but we are still at a couple of percentage points lower level.

3 Likes

Indeed, tremendous growth, with double-digit and forecast-beating growth in all segments, even though the group was already expecting over 10% growth…

I was at least on the right track regarding the material margin, as

70 Likes

But isn’t it great that there are still stocks with good opportunities to beat the market? Harvia’s attractiveness to small investors is further increased by the fact that no exact forecast is given. And apparently, no extra information is whispered to analysts during the quarter either. Hard work pays off here.

14 Likes

Indeed, Järnefelt further improves the say-do ratio.

26 Likes

The APAC & MEA region is starting to become interesting. It wasn’t long ago that the figures were negligible in the grand scheme of things, now they are already 50% of Northern Europe’s revenue. This inevitably brings to mind the situation in North America a few years ago.

I checked old quarterly reports and in 2020 Q3, “Other countries” revenue was around one million and North America approx. 5m.

Currently APAC & MEA 5.7m

North America 16.6m

55 Likes

Here you can see that world domination is only in its infancy! Such “side streams” grow and will soon be a solid part of the whole ![]()

Absolutely amazing ![]()

36 Likes

One explanation could be the large number of new products under almost every brand. It will surely take time before the lines “get hot” too.

All in all, I see many small, potentially highly scalable drivers.

- A lot of new geographical growth opportunities. Let’s say, for example, the Czech Republic and other Eastern Central Europe, Denmark, Ireland, Australia… Sauna (+ other wellness) is only just being discovered in a large part of the world.

- Product development and productization Under Every Brand are really well underway. New, finer, and smarter products are coming out at a good pace.

- And related to the above. It’s quite clear that competitors are falling behind more and more because others don’t have these investments and expertise to put in.

- And finally, services and maintenance. Just like with a company like Kone. The more saunas there are in the world, the more accessories, modernization, and maintenance will be sold. This significant (exp.) growth seed has not yet been fully realized, in my opinion.

In summary (can and should be questioned)

- More new saunas (and other wellness units) are being built in the world per unit of time.

x

- Due to the above, the size of the world’s sauna stock is growing at an accelerating rate.

x

- All saunas and wellness require continuous maintenance, modernization, and upkeep. People’s need and desire to customize these environments are also quite endless.

x

- Harvia’s market share in the sauna market is growing faster than the sauna market itself.

9 Likes

Although margin percentages have fallen, absolute margins are on an upward trend thanks to good revenue growth, which is the most important thing.

3 Likes

It seems that US tariffs on Canadian timber at least rose in Q3 (roughly +10% more, based on a hunch). As far as I understand, timber in the US is very often imported from Canada (or the domestic alternative is more expensive), so could this have become a significant expense for AHS, which would partly explain this? ![]() Of course, inflation has certainly affected other areas as well.

Of course, inflation has certainly affected other areas as well.

Apologies if this was already answered in the webcast or similar. I haven’t had time to listen yet.

EDIT: at least in the webcast’s initial overview, it was also mentioned that significant quantities of sauna heaters are still imported into the US, and tariffs naturally affect these.

1 Like

The reasons mentioned for the decline in the material margin, in addition to a completely exceptional comparison period, were mainly the weakening of the USD affecting heaters exported from Finland to the USA (when costs are in euros) and tariffs. However, in my opinion, the amount of these is not significant enough to fully explain why the material margin is about 62.5% when the normal level is a couple of percentage points higher, meaning there are probably some other elements that were not disclosed. Matias also referred to quarterly fluctuations in the interview. With Harvia’s pricing power, small cost increases should, of course, be able to be passed on to prices within a reasonable time.

30 Likes

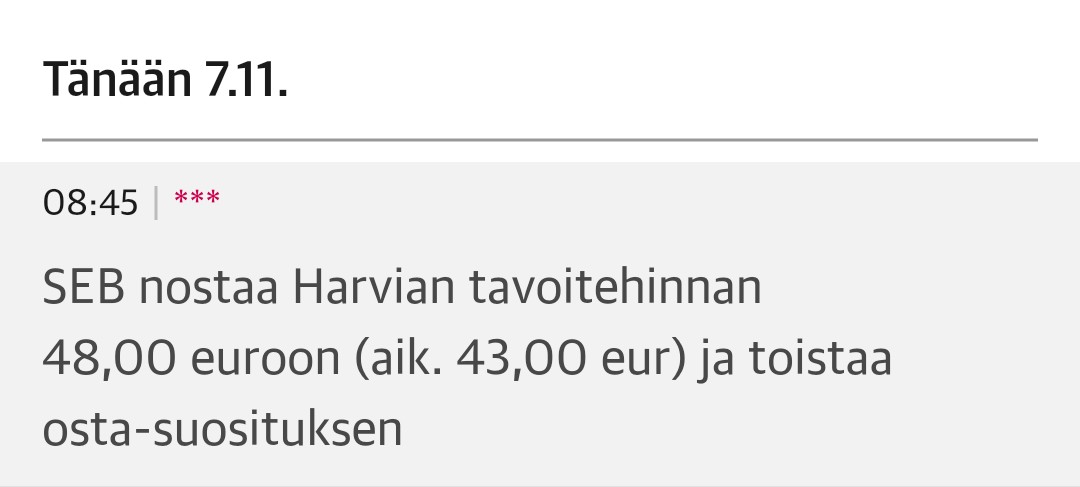

Here’s the CEO’s interview to watch, which hasn’t been linked yet. ![]() Strong performance!

Strong performance!

Topics:

00:00 Introduction

00:12 Broad-based strong growth

01:27 Development in the United States

04:09 Strong turnaround in Europe

06:00 Growth in APAC & MEA region

07:45 Material margins

09:19 Price increases

10:40 Growth in fixed costs

12:14 Outlook for the rest of the year

48 Likes

9 Likes

”We consider the company’s return on capital and cash flow generation capability excellent, and the multiples will moderate in the coming years.”

Again, the same story that has been repeated like a mantra… In the future, once again (hopefully), these theories will be moderately swept aside.

1 Like

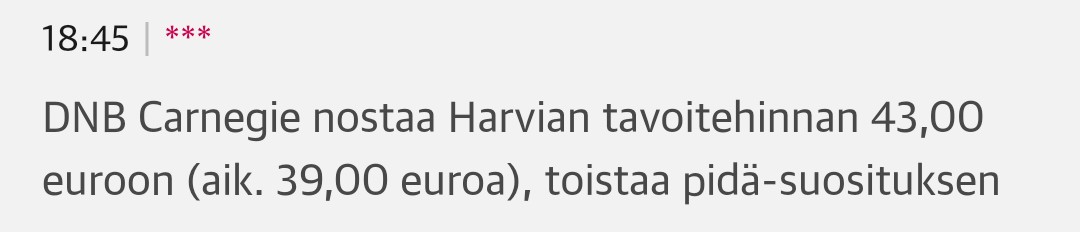

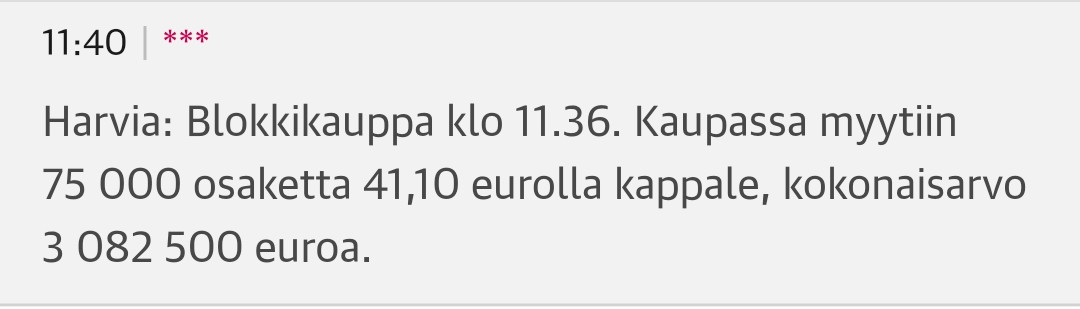

Yesterday I added to my portfolio at a price of €41.10, but I won’t tell if it concerned this trade ![]() The result was indeed impressive in all respects. I myself was already pondering the impact of a possible USD strengthening on the Q4/25 and Q1/26 results.

The result was indeed impressive in all respects. I myself was already pondering the impact of a possible USD strengthening on the Q4/25 and Q1/26 results.

4 Likes

Which part of that do you think is not true? And why?

21 Likes

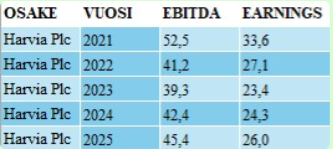

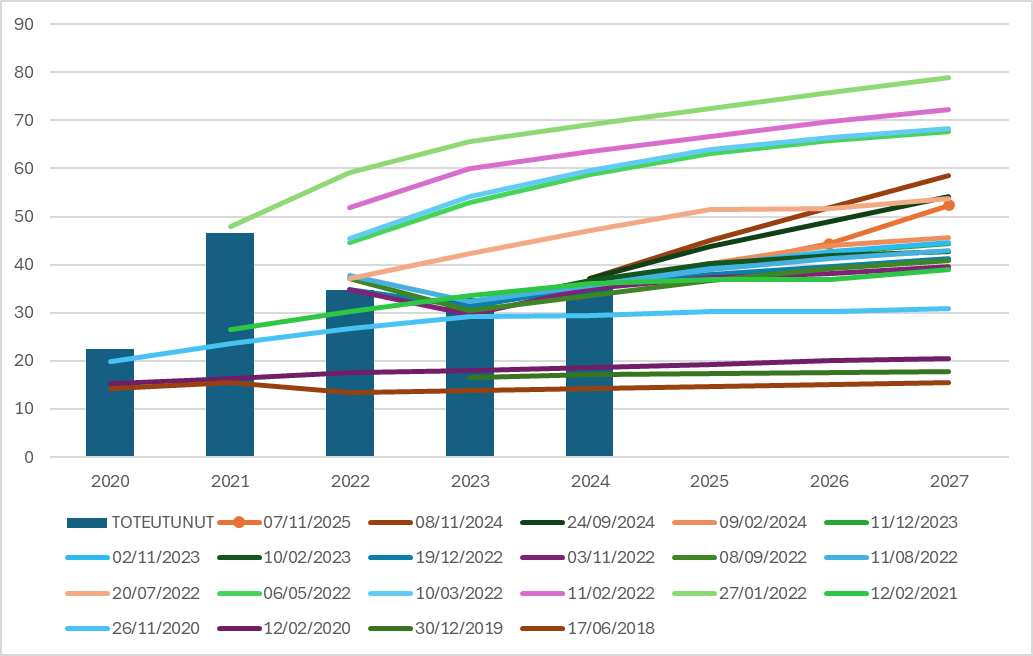

In the Harvia thread, @LeFevre’s pictures of historical forecasts haven’t been seen, so I put one together myself (fortunately, AI did it quite quickly). Harvia reports had been published so frequently that I had to cut quite a lot, but below are selected forecasts.

It’s probably clear that forecasts made before corona were ridiculously low compared to current levels (of course, there have been acquisitions along the way), and those made at the peak of the corona boom were over-optimistic. However, since summer 2022, the forecasts seem to have been quite accurate, and those growth curves don’t look completely outrageous to my eye either. So if all companies were as good as Harvia, then maybe the forecasts would also be more accurate ![]()

89 Likes

Especially regarding North American sales - an influential man recently published a video about the effect of sauna on his overall health, meaning that in this case too, we are amidst the megatrends of well-being. This is about the American entrepreneur Bryan Johnson, who titles himself as “the most measured human in the world.” In short, a potential billionaire who does everything to preserve his youth by various means and apparently, to quote Queen, wants to live forever. Also known from the Netflix documentary Don’t Die.

The channel has just over 1.85 million subscribers and 2 million on Instagram. A quick look shows that the most popular video has 4.4 million views. The video specifically discusses the Finnish origin of sauna, and Harvia naturally makes an appearance at 1:16.

35 Likes

Almanakka has done an excellent piece on Harvia after Q3. ![]()

Vesterinen notes in a side comment that in more traditional sauna markets, 70-80% of Harvia’s sales are replacement demand. In the USA, this dynamic naturally doesn’t work this way yet, because most people are only buying their first sauna. At the same time, Vesterinen points out that typically, the second sauna sold is also the company’s sweet spot. This certainly promises an incredibly good future in the USA, once a sufficiently large market share is captured in the minds of consumers and distributors.

https://www.sijoitustieto.fi/sijoitusartikkelit/harvia-q325-jarnefelt-maalasi

45 Likes