Before Harvia, Hagemeier served as Sales Director at DMF Lighting in the United States from 2022 to 2025. He has also worked in several different leadership positions at Lutron from 2007 to 2016 and 2019 to 2022, most recently as Managing Director of the Europe and Africa division in Great Britain. Hagemeier also served as a director at Lonestar Electrical Supply in the United States from 2016 to 2019.

Does Harvia report Canada separately or has it mentioned what kind of figures have been obtained from there? As a country, it’s huge and the climate is similar to Finland. One would think there’s huge potential. I’ve also been thinking that Harvia says it wants to be a “backyard paradise” but hot tubs are missing from its selection. It feels like, at least in Finland, if a house is built, no one talks about wooden hot tubs but rather dreams of a yard sauna and a hot tub. Why isn’t Harvia willing to enter the hot tub business?

I would guess that a couple of big reasons why hot tubs are not pursued are at least:

If one thinks purely from a mechanical standpoint, it’s a more complex or at least a slightly different device. This would mean that they would hardly integrate with current assembly technology, etc.

It’s also a much more competitive product category globally (e.g., Jacuzzi alone has over 4000 employees) => would require large investments, and maintaining margins at Harvia’s excellent levels would probably be difficult.

In other words, revenue would certainly be generated, but ultimately, the bottom line would hardly be as good as with the current product portfolio, even if some level of synergy with the current portfolio would, in a way, exist.

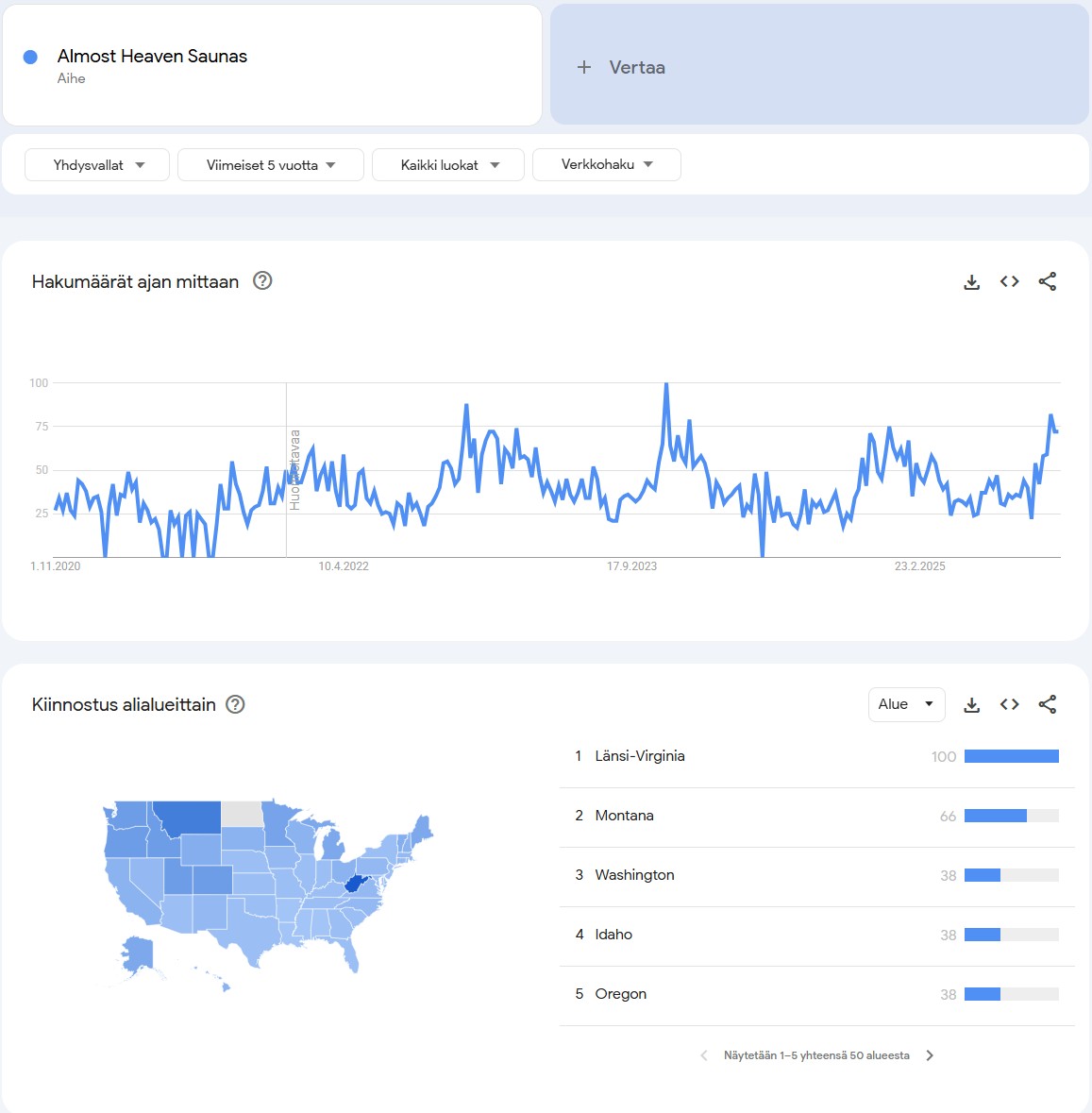

Good reflection. If you want to get a little grasp of the problem, researching the Almost Heaven Sauna provides a good case. I don’t know about all delivery methods, but you can at least order one of these in pieces and then assemble it yourself – and quite a few people seem to assemble them. You can find videos on YouTube showing how this is done. Sometimes a little better, sometimes worse. And there are all sorts of modifications involved, e.g., related to electrification.

Someone had bought a glass-walled barrel model from Costco, and the worst happened: the tempered glass wall exploded during installation. I’ve had a similar experience myself when a guest was showering in the bathroom behind locked doors. A rather unpleasant situation.

AHS, however, is small and efficient. The business structure is, shall we say, “hygienic” (you can order it online and assemble it yourself like IKEA furniture…) and when everything goes well enough (no lawsuits), money pours in from all directions. However, then Alibaba is also already overflowing with barrels at a fraction of the price.

But my point is that the next step is bigger. I personally see Thermasol as a different business, but on the other hand, at least according to trends, this brand has not made any breakthrough. These are million-dollar questions – do we focus on products with high margins, or do we get involved in businesses that inherently include a more significant service component – either ourselves or through partners?

I’d like a “cautious” entry into the hot tub market… something like a drop design pool style purchase, and then scale that up. Good-looking design, and it would probably work in America. All services for the backyard under one roof… but I still don’t see a reason to get into swimming pools.

If Harvia were to expand its product portfolio into something like hot tubs now, I would see it more as a negative thing. We could even give up Kirami and focus solely on the essentials, i.e., saunas.

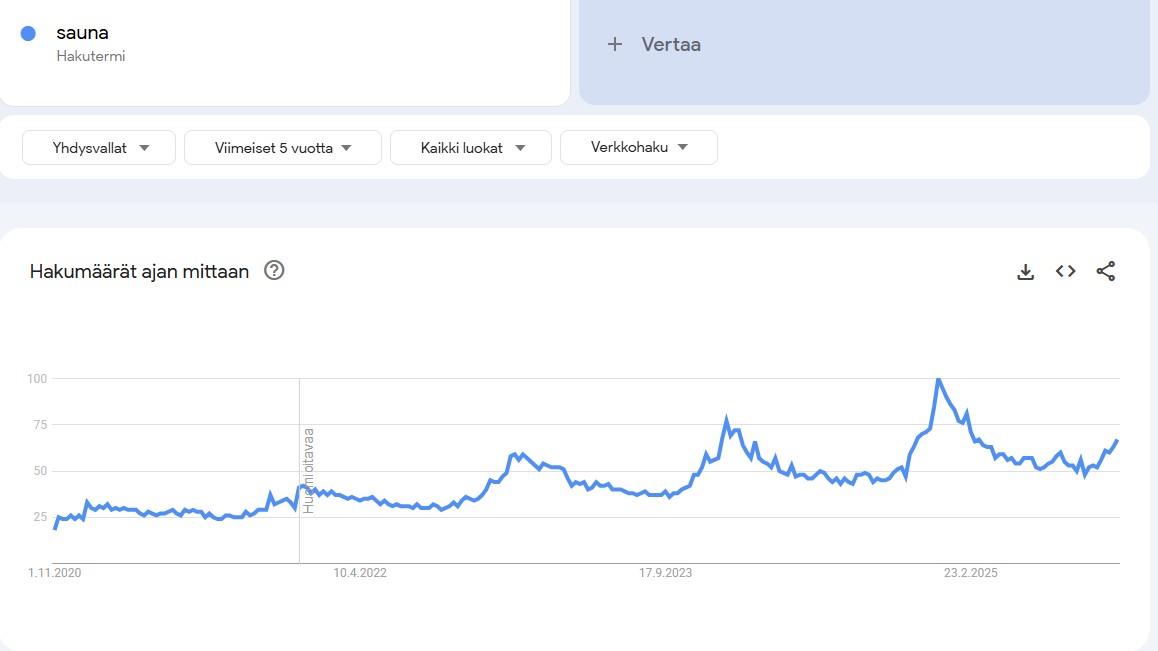

By the way, it would be interesting to see data on how the visitor numbers of reddit’s r/Sauna have developed; if anyone knows or finds a way, please let me know. The only thing I found was the website gummysearch.com, according to which the number of visitors would have grown by 65.2% in a year, with 99k visitors now. It came to mind when I saw a post there where the owner of an American sauna camp complained about how several HUUM heaters had broken down. From there, you can get a good sense of which companies’ heaters are recommended for purchase; in that particular post, several American commentators highlighted the US sauna company Kuuma and IKI. Kuuma probably refers to this company: https://www.lamppakuuma.com/ Fortunately, there was also one comment about Harvia.

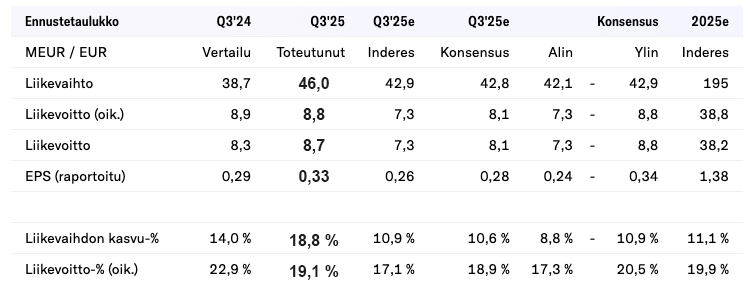

Here are Rauli’s preliminary comments as Harvia publishes its Q3 results on Thursday. We expect the company’s organic revenue growth to have accelerated from Q2 levels, but the result to remain lower than the comparison period in the seasonally weakest quarter. This is explained by the exceptionally high material margin in the comparison period and the company’s continuous growth investments, which increase fixed costs.

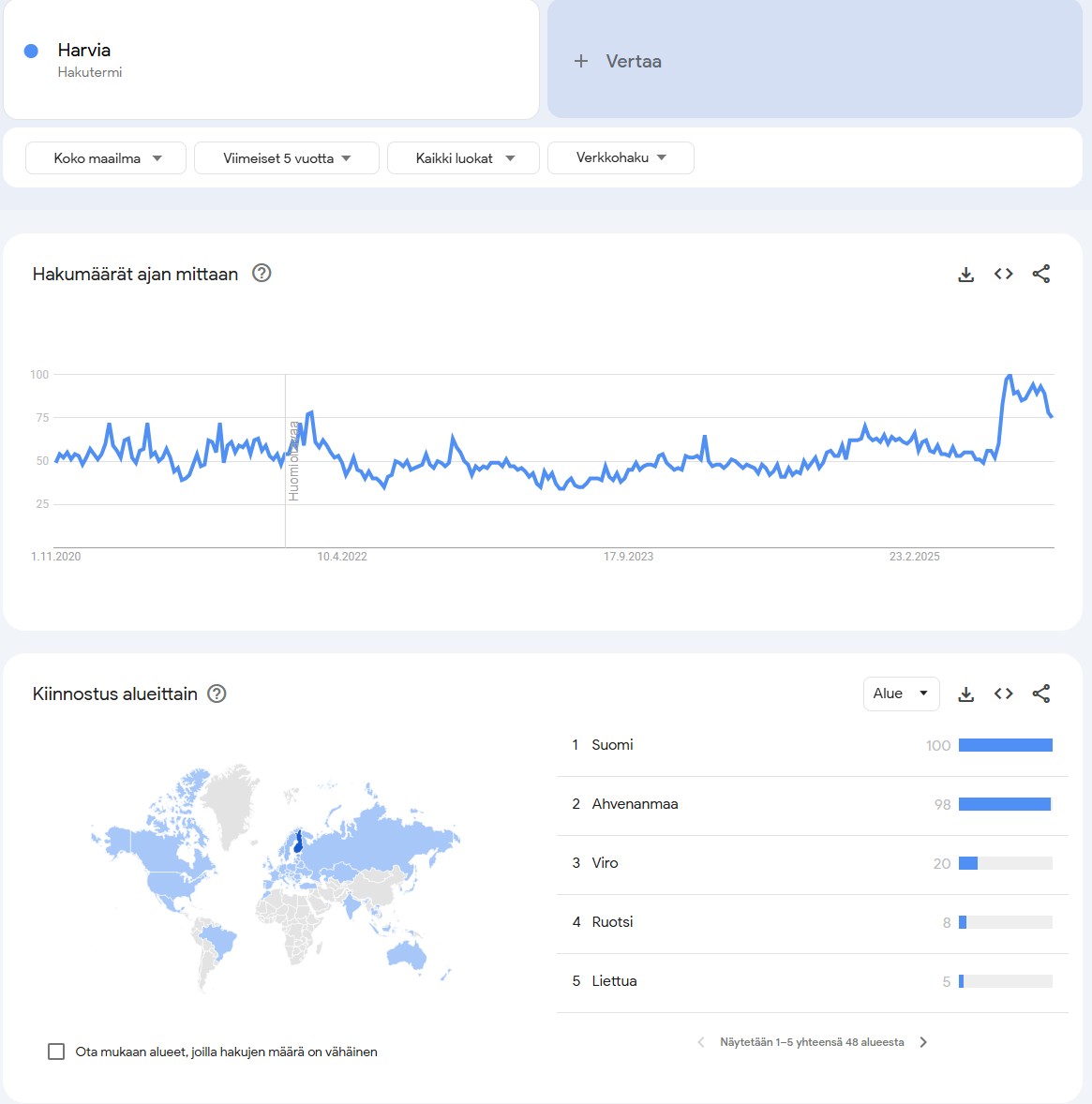

Small trends update. Harvia as a search term saw a large global spike during Q3. Could it be a celebrity effect, as Harvia’s heaters have been featured by many “super celebrities”?

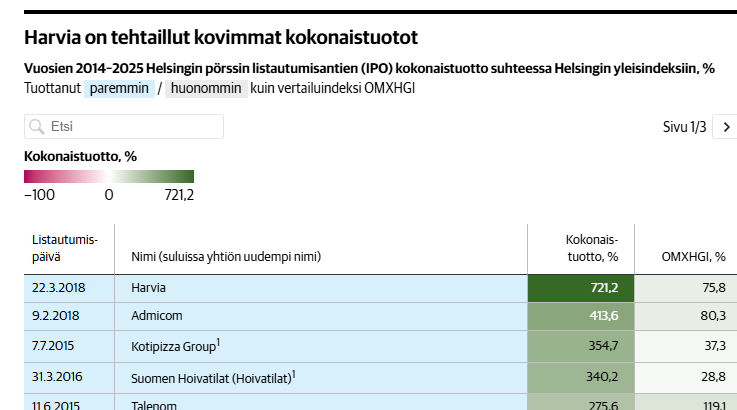

Kauppalehti has an article about companies listed in recent years and their success. Harvia has been the best performer among companies listed between 2014-2025.

“According to Puttonen, a poorly timed or overpriced offering is almost a catastrophe for the company.

”An IPO is a situation you can’t mess up,” he summarizes.

Puttonen names the sauna company Harvia, which went public in 2018, as a successful listing. Its start was upward-trending. During the COVID-19 pandemic, the stock overheated, after which the price melted down, but since then, the trend has stabilized.”

North America has emerged as the largest and fastest-growing market area. Against this backdrop, it’s a bit surprising that no one with specific knowledge of America or even American trade has been appointed to the company’s board.

On the other hand, there are, for example, two individuals with a CapMan background (who, of course, probably have good background information about the company), even though CapMan, as I understand it, sold its shares a long time ago.

Is the nomination committee asleep, or what is the issue here? Or could this be the recipe for success in the American market?

Good point! The composition of the board partly reflects the big changes in ownership in recent years, as the board’s composition has not kept pace with ownership changes. Perhaps that’s a good thing; too frequent changes on the board are not necessarily good for a company with a long-standing recipe for profitable operations.

But the board definitely needs some new blood for expertise in American trade and industry. Another thing that bothers me is the CEO’s lack of share ownership; there are many justifications, but a suitable stake would be desirable so that we would be in the same boat.

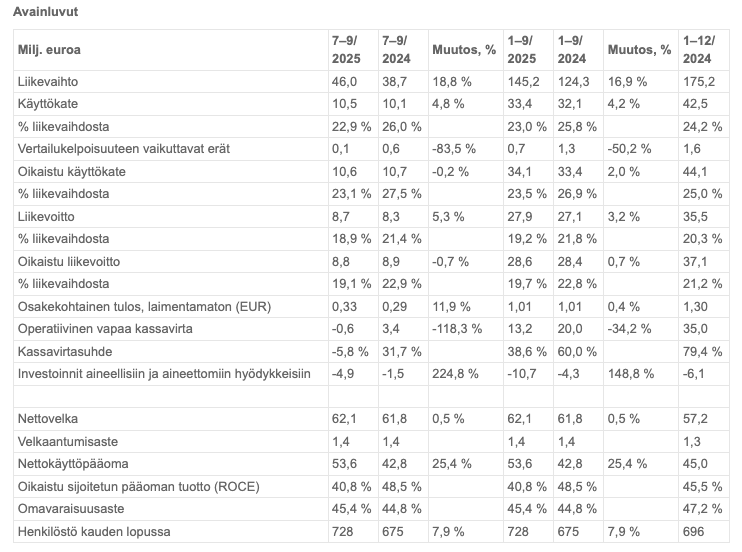

Revenue grew by 18.8% to EUR 46.0 million (38.7). At comparable exchange rates, revenue grew by 22.3% and was EUR 47.3 million. Organic revenue growth was 16.1%.

Operating profit was EUR 8.7 million (8.3), or 18.9% (21.4%) of revenue.

Adjusted operating profit was EUR 8.8 million (8.9), or 19.1% (22.9%) of revenue. At comparable exchange rates, adjusted operating profit was EUR 9.1 million (19.2% of revenue).

Operating free cash flow was EUR -0.6 million (3.4) and cash conversion rate was -5.8% (31.7%). The change was primarily due to Harvia’s significant investments in operational efficiency and facility improvements in the third quarter.

January–September 2025:

Revenue grew by 16.9% to EUR 145.2 million (124.3). At comparable exchange rates, revenue grew by 18.4% and was EUR 147.2 million. Organic revenue growth was 10.7%.

Operating profit was EUR 27.9 million (27.1), or 19.2% (21.8%) of revenue.

Adjusted operating profit was EUR 28.6 million (28.4), or 19.7% (22.8%) of revenue. At comparable exchange rates, adjusted operating profit was EUR 29.3 million (19.9% of revenue).

Operating free cash flow was EUR 13.2 million (20.0) and cash conversion rate was 38.6% (60.0%).

Net debt was EUR 62.1 million (61.8). Gearing, calculated as net debt to adjusted EBITDA for the last 12 months, was 1.4 (1.4).

Really strong performance against a strong comparison period, even though analysts’ crystal ball showed something completely different. Great work from Harvia again, against all odds

Great result from Harvia. Sales grew in all geographical areas, and it’s great to see signs of recovery also visible in Europe! As a downside, one could mention that sales grew by 19%, but variable costs increased by 45%, meaning the gross margin weakened quite significantly. Perhaps the sales mix was the reason. The CEO’s review mentions tariffs and exchange rates. These have probably had an impact, but I don’t believe their effect was that significant. But it’s good to continue from here!