It’s time to create a thread for H&M, because a substantial report from @Rauli_Juva is now available.

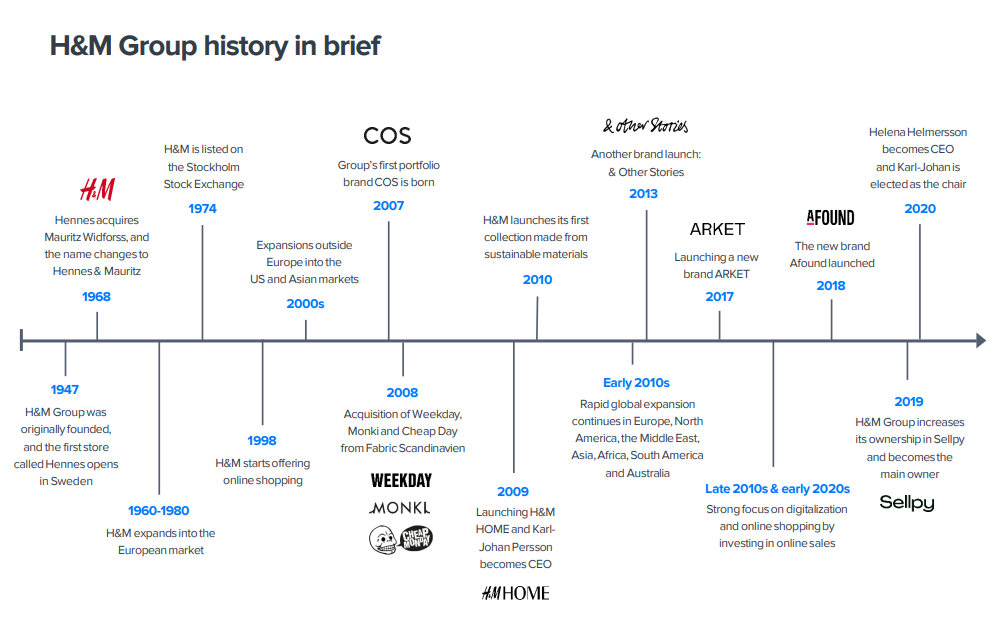

H&M, or Hennes & Mauritz, is a Swedish international retail group known for its clothing stores, which offer women’s, men’s, and children’s clothing, as well as cosmetics and, since 2009, home products.

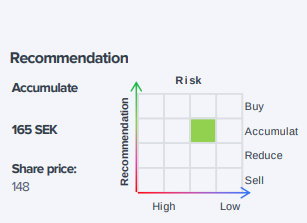

We believe H&M is on an improving margin trend and will get close to its 10% margin target in 2024, driving a substantial earnings growth y/y during 2023-24. We see solid growth potential for this globally strong fashion brand.

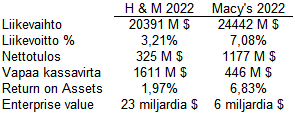

I couldn’t resist making a comparison between H&M and Macy’s, as both are in the same revenue bracket and are good points of comparison in terms of product range (fashion apparel, cosmetics). The exchange rate used was 0.091214 SEK/USD. The figures are taken from the companies’ 2022 annual reports.

H&M has better cash flows even when looking further back at historical comparisons, but the stock carries a high price tag. In my view, both companies are affected by similar secular trends in the form of challenges in apparel sales, general retail anemia for brick-and-mortar stores, and tough competition. I was therefore surprised by @Rauli_Juva’s strong optimism regarding H&M’s near-term outlook. Does this optimism apply to the apparel market in general, or do you see H&M taking market share from other players in the form of 5% revenue growth? In H&M’s business, revenue growth has been pursued at the expense of margins for a long time.

I slightly disagree about it being a good comparison point. Macy’s is a US-led department store company, while H&M is a global fast-fashion company. There are similarities, but in my opinion, it’s not a good peer, and it’s not on our peer/competitor lists either.

The clothing market certainly doesn’t grow by 5%, especially in developed markets, so that requires/assumes market share growth and, on the other hand, presence/growth in faster-growing markets. In our estimates as well, 5% growth only starts from 2025 onwards, when the current cyclical weakness is behind us.

Generally, fast fashion in a nutshell: cheap labor, poor working conditions (dangerous working conditions, violence, rapes at the factory, non-existent pay…) and H&M has been aware of these problems and has turned a blind eye for a long time; the pollution of waterways, environmental damage from “recycled” clothing…

Pretty much the same things can be found in that free comprehensive report by Rauli as in this tweet thread, but if someone doesn’t feel like reading the report, a tweet thread is available for the lazier ones.

H&M’s entire history is somewhat full of crises. At the turn of the millennium, there was a crisis over child labor; Persson said it would be banned. Eventually, he stated that it is difficult to monitor subcontractors.

Then there was a crisis regarding a living wage. Again, Persson promised that the goal would be to pay everyone a living wage. Later, they noted that it seemed there was no willingness to pay for this. The goals were quietly abandoned.

Now there has been a crisis over material choices and recycling. They will probably put as much effort into these as the law requires.

Overall, H&M’s business logic as fast fashion fits very poorly with current EU goals. The entire business idea is based on being able to make massive purchases and sell in high volumes, cheaper than others, and offering the latest fashion trends that become outdated quickly.

The EU aims to mandate companies to sell durable clothes that are repairable. This kind of thinking does not increase volumes.

This requires a fairly significant brand renewal, which was indeed mentioned in the report.

These foreign coverages are very useful for me, as I feel that Finnish companies are relatively easy to follow, and US stocks are pushed too much from everywhere. There should be even more analyses of large European companies, as digging for information on them is more laborious.

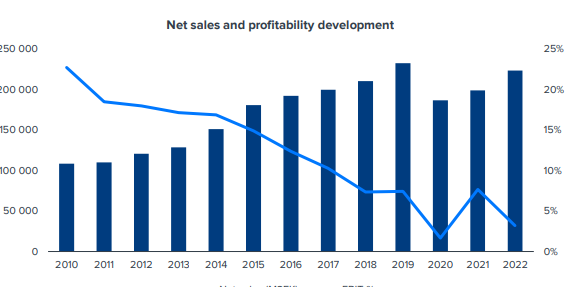

That 5% margin is indeed incredibly low compared to Lindex’s figures, for example. Overall, Lindex’s clothes do not really cost much more.

How are potential competitors examined and conclusions drawn in these reports, when the competitive landscape of an export company can be challenging to analyze from home here in Finland? Does the assessment come from the company or other sources? Is revenue in different market areas or the similarity of the product range examined? Satisfying the same need?

I agree about Zara based on my “Finnish gut feeling”.

How do you see it yourself (of course you can’t know, only guess), will H&M succeed in turning a brand based on volume trading around fast enough as the world changes?

Is H&M a paying customer for Inderes, or was coverage started to support the analysis of Stockmann and/or Inderes’ growth in Sweden?

They are looked at in the same way as in other companies; of course, if it’s a Finnish-led company, the situation is easier to grasp. In this case, we looked at the larger players in the industry, which H&M belongs to, and tried to choose ones that are somehow relevant to H&M, i.e., similar in price level/selection, so that we don’t, for example, compare H&M to luxury or sports brands. Since H&M is global, in this case, no one was selected or excluded based on market area; instead, we aimed to choose peer competitors whose focuses are in slightly different regions (Zara is global, Uniqlo Asia, Old Navy North America, and Bershka, Next, and Primark Europe). Of course, the company is always asked who they see as competitors/benchmarks, but it’s rare to get any ready-made list from them.

Indeed, that remains to be seen, but I do believe that if the whole industry changes/is forced to change, one of the strongest global brands is still in a strong position in the competitive landscape. Of course, if the volume of the clothing trade were to enter a clear downward trend, it would hardly be a very good situation for any player in the industry.

It is not a paying customer; this can be seen on the front page of the report, where paying customers have the relevant text. So, this is related to supporting growth in Sweden, which I believe has been publicly mentioned—that a few (or something like that, I don’t remember the exact wording) larger companies are being brought under coverage pro bono. Nibe and Nordea, alongside H&M, are the ones that have been published now.

If you’re even slightly interested in H&M as an investment but don’t yet feel like reading the excellent report on the company found in the opening post, among other places, check out this excellent tweet thread by @Kaisa_Vanha-Perttula to start with.

In this context, I must mention that Kaisa has actually done a large part of the work on the H&M report, even though only my face appears in the report

These are noteworthy points that I have been thinking about myself as well. H&M has been part of my portfolio for about a year. For diversification purposes, the Stockholm Stock Exchange offers a wide range of companies from various sectors, and the tax treaty works well for dividends.

On the other hand, it might be easier for large, established players to adapt to the change. Some kind of change is coming; I can see it in my own child, who prefers to buy used clothes rather than new ones. I used to buy everything for them from H&M’s good online store

Was @Kaisa_Vanha-Perttula involved in making the report this time as well? (or was it that Kaisa did it and only your face ended up in the report? )

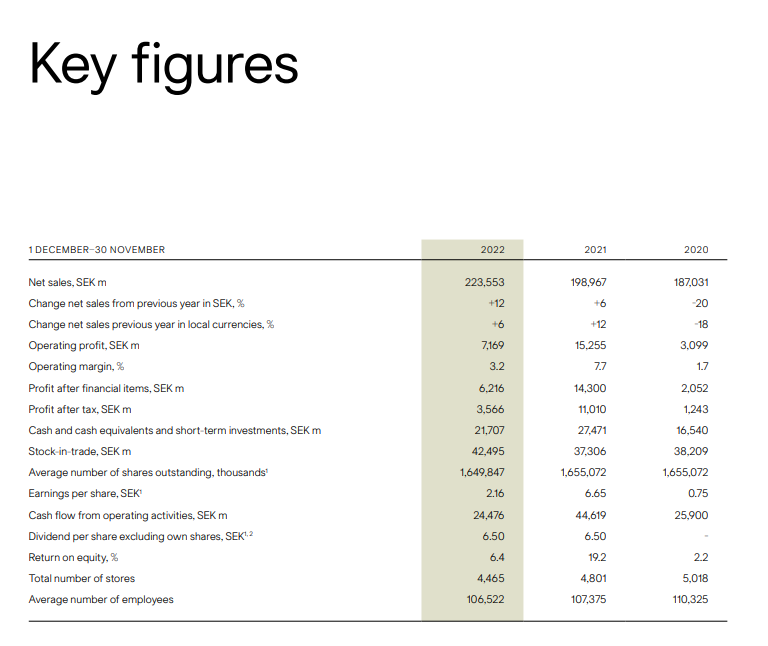

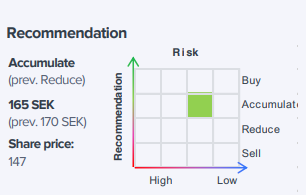

H&M’s Q4 sales development was slightly behind our forecast, leading to minor estimate cuts. The share has performed well since our initiation and the multiples have corrected to quite fair levels in our view (P/E 19x for 2024).

CEO Helmersson is leaving the company. No paywall.

SWEDISH clothing giant H&M’s CEO Helena Helmersson is resigning from her position. Daniel Ervér has been named as the new CEO to replace her, the company states in its press release.

Helmersson worked at H&M for 26 years, the last four of which as CEO. The company did not disclose the reason for Helmersson’s resignation in its press release.

H&M’s Q4 earnings fell short of expectations and also fiscal 2024 seems to be off to a soft start. This pushed our EBIT estimates down 8% and 1% for 2024-25 respectively.

I wrote a few words over on the Sweden forum about Inditex’s results today. They have performed clearly better than H&M in recent years, so you can’t draw a direct link from that to H&M, but the good momentum at Inditex seems to continue.